NurPhoto/NurPhoto via Getty Images

We updated investors in our previous article to prepare for volatility as Verizon Communications Inc. (NYSE:VZ) prepared to report its Q4 and FY22 earnings release.

Today’s (January 24) earnings release didn’t cause investors to bail out, suggesting that significant pessimism could have been reflected. Therefore, we believe it has helped to reset expectations, as investors parse management’s commentary on its FY23 outlook.

Wall Street analysts on the call didn’t seem convinced about management’s outlook. Verizon’s FY23 guidance suggested wireless service revenue growth of 3.5% (midpoint). However, that is markedly below FY22’s full-year growth of 9.6% and FQ4’s 6.1% increase.

Investors need to pay close attention to Verizon’s wireless service revenue parked under its consumer base, which accounted for nearly 60% of its segment revenue for FY22.

As Verizon’s key growth driver, we believe investors are justified to ask questions about whether the competitive landscape with AT&T (T) and T-Mobile (TMUS) could have impacted its growth cadence.

Furthermore, Verizon’s FY23 outlook suggests that its adjusted EBITDA growth is expected to be flat against the midpoint of its guidance range. Moreover, Verizon’s adjusted EBITDA guidance of $47.75B (midpoint) for FY23 is below the Street’s previous estimates of $48.79B (1.8% YoY growth).

Hence, we could understand why some investors may be concerned whether Verizon can manage its CapEx buildout through 2024 while sustaining its profitability growth.

Management highlighted its confidence that investors should continue to assess the company’s ability to drive adjusted EBITDA profitability and free cash flow (FCF) conversion.

As such, management’s tepid outlook could have disappointed some investors, given the company’s relatively optimistic outlook at an earlier January conference which we highlighted in our previous update.

Furthermore, its adjusted EPS guidance range of $4.55 to $4.85 came way below the previous consensus estimates of $5.04. Management updated that it’s seeing an adverse interest expense impact of between $0.25 to $0.30 “due to higher floating rate debt costs and higher securitization costs for the growing device payment portfolio.”

Relative to FY22’s adjusted EPS of $5.18, it represents a significant decline of more than 9% at the midpoint of the company’s guidance range.

Hence, investors need to decide whether they are convinced that the company’s outlook could have de-risked its execution risks sufficiently, or worse downward revisions could follow.

It’s a critical concern because management didn’t answer directly whether its guidance has baked in a mild recession or deep recession, with CFO Matt Ellis accentuating:

In terms of the macroeconomic assumptions, in the guide. I wouldn’t say we have anything too dissimilar to what you’ve heard from a number of other people during earnings season. But one of the things I come back to is the resiliency of our customer base. We’ve been through different types of economic environments in the past. We know customers pay their phone bills before they pay other bills and other outgoings. We fully expect that to continue. (Verizon FQ4’22 earnings call)

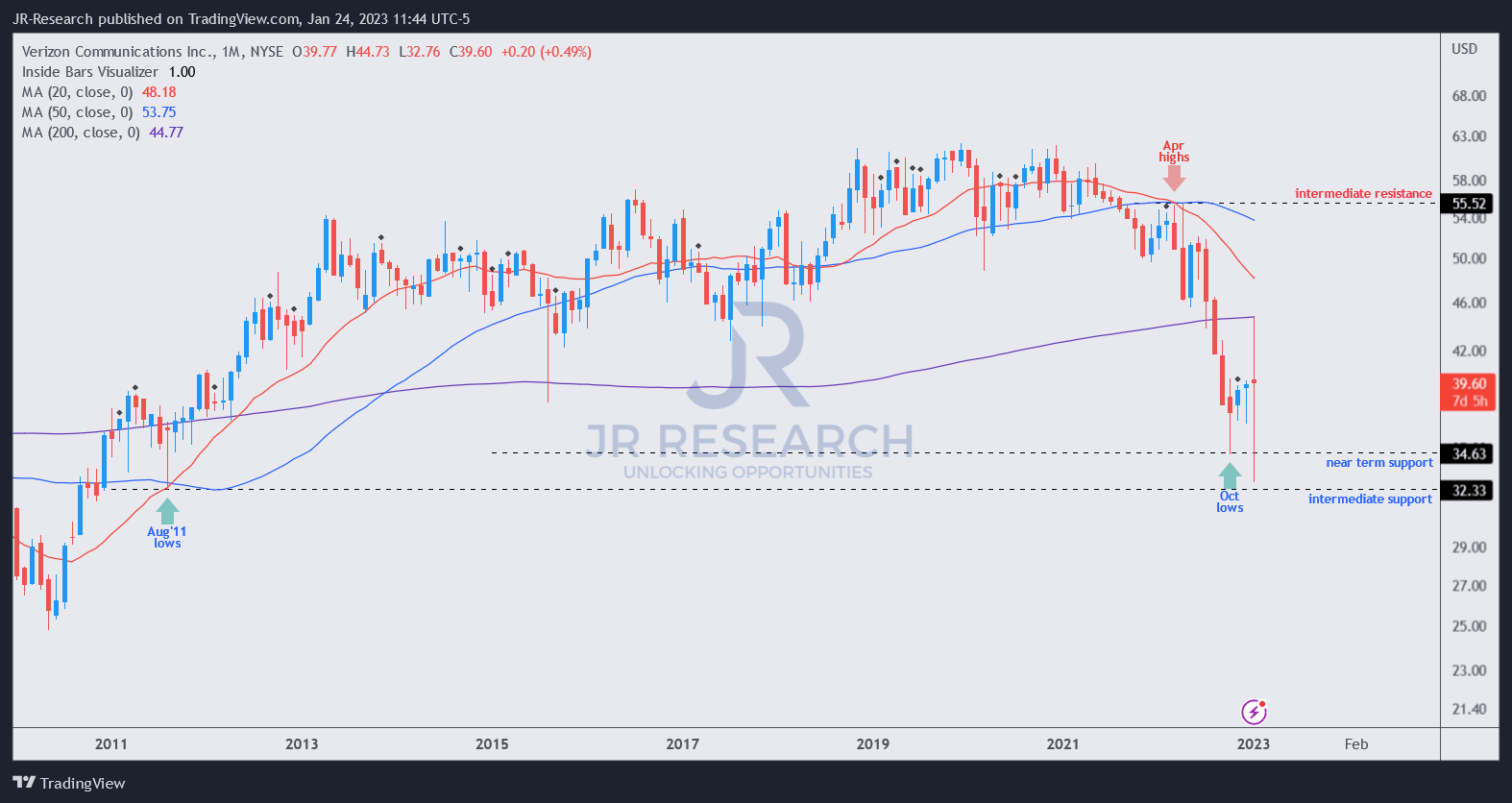

VZ price chart (monthly) (TradingView)

Hence, investors must decide whether the company’s guide has baked in a hard or soft landing scenario.

VZ’s price action indicates that its October lows remain robust, as buyers are likely looking ahead to lowered estimates that could help de-risk its execution.

Hence, if the macro outlook turned out better than anticipated, Verizon could potentially revise its outlook upward subsequently, which could drive a re-rating given its valuation of 7.1x NTM EBITDA.

Rating: Buy (Revise from Hold).

Be the first to comment