deepblue4you

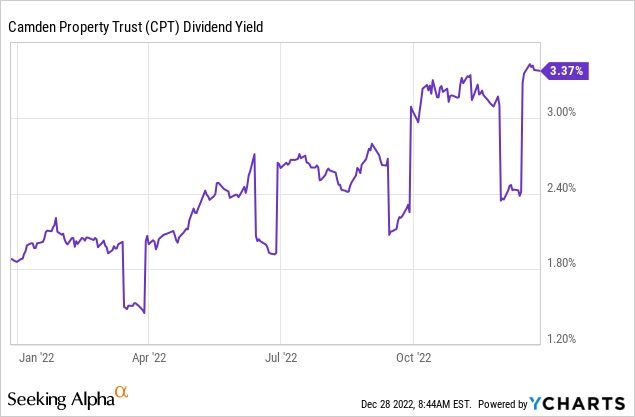

I’ve been buying Camden Property Trust (NYSE:CPT) in recent weeks following a 37% year-to-date drawdown that has seen the yield of its quarterly cash dividend payouts swell to 3.4%. The last quarterly per share cash dividend payout of $0.94, in line with the prior payout, came on the back of a broader macro discombobulation of REITs which are almost always leveraged.

Hence, rising Fed fund rates meeting Camden Property’s trailing 12-month debt-to-capital ratio of 42% and an expected slowing of rental demand on the back of a weaker economy has understandably pushed common shares of the REIT lower. To be clear, 2022 was one of the worst years for stock market performance since the 2008 financial crisis due to underlying dynamics that will peak next year. I think this opens up the specter for more near-term underperformance of the commons, and an opportunity to reach a full position.

Indeed, Fed fund rates are expected to reach a 17-year high of between 5% to 5.25% next year, with inflation only expected to fall closer to the 2% target towards the start of 2024. My investment in Houston, Texas-based Camden Property was built on four pillars. The inherent diversification of its apartment portfolio, the comparatively low risk of this, the reliability of the dividends, and the healthy moat.

The Multifamily Fundamentals Are Great

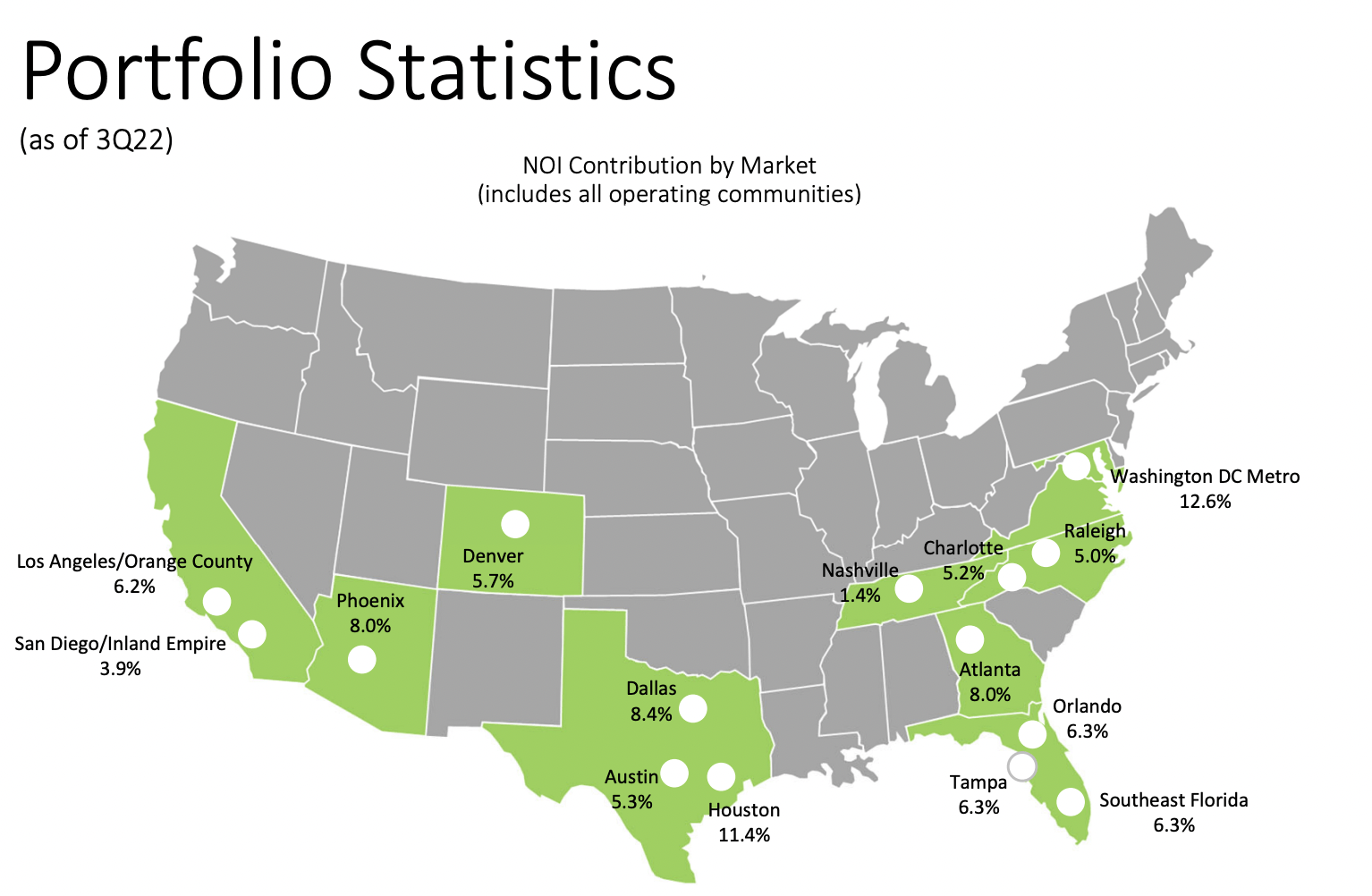

As of the end of Camden Property’s fiscal 2022 third quarter, the REIT held over 58,000 apartments mostly located across 15 states and with a focus on the sunbelt. The portfolio statistics are incredibly attractive. Firstly, net operating income is diversified across a number of good locations with Houston, Phoenix, and Washington DC all being top markets.

Camden Property Trust

The portfolio is further diversified across urban and suburban locations with a focus on areas benefiting from positive population and economic growth as well as locations that offer a healthy business environment. Occupancy at the end of the third quarter stood at a healthy 96.6% but had dropped to 96.1% post-period end in October. This was down 110 basis points from the year-ago comp, with the broader macroeconomic climate weighing down on leasing demand and reflecting a pullback seen by a number of REITs across several property types.

I think Camden will continue to see some level of weakness, but not to the extent that the underlying FFO guidance will be threatened. Indeed, the balance sheet provides a near fortress-like quality and is an undeniable moat. The company had a 3.7% weighted average interest rate on all debt, with 93.9% of these being fixed-rate debt.

Camden Property Trust

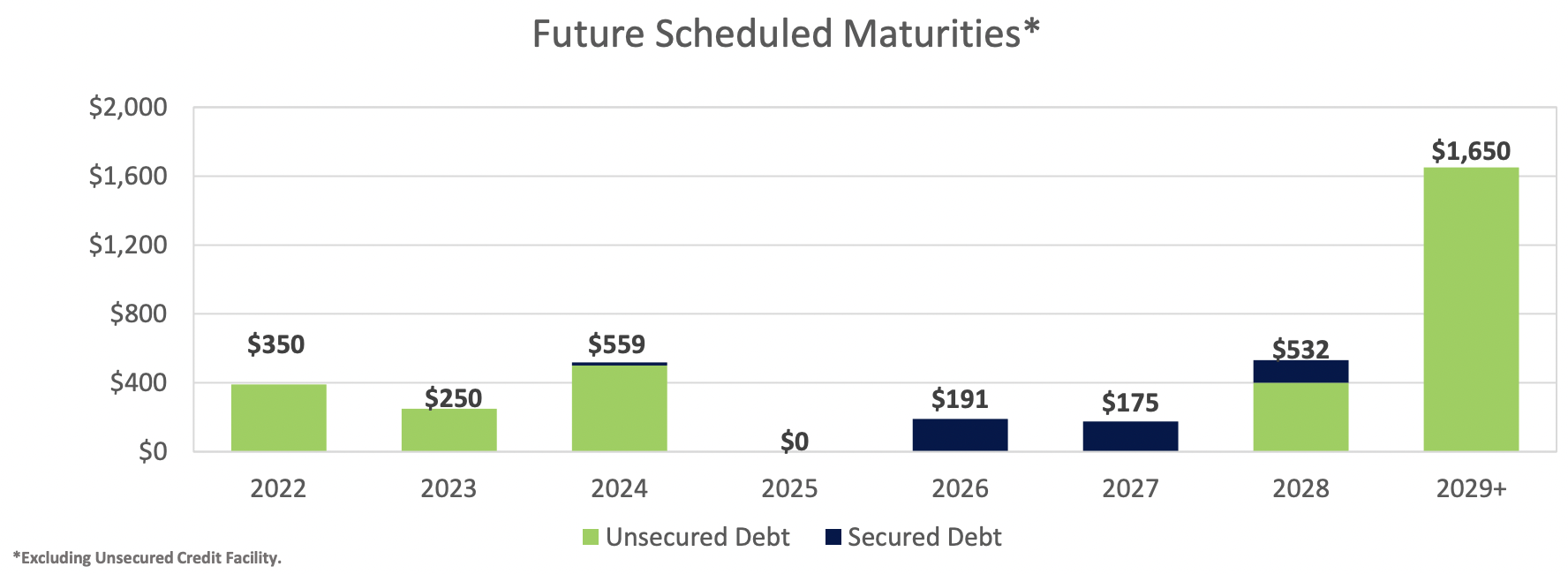

This is an incredibly advantageous position as it means Camden is not forced to execute expensive hedging strategies from interest rate swaps and caps to early debt repayments to mitigate overall expensive variable interest exposure. Critically, it’s this fixed and relatively inexpensive balance sheet that helps form a moat against the broader economic volatility and rising interest rate environment. Near-term liquidity available to the REIT also stood at $1.5 billion from an unsecured credit facility. This comes as only $250 million in debt comes due in 2023 and with the REIT commencing the development of two properties at a total estimated cost of $155 million during the quarter.

Sleeping Well At Night With The Camden’s Common

FFO per share during the quarter came in at $1.70, up 25% from the year-ago quarter. This of course more than covered the company’s last dividend payout and creates stability and confidence around the future dividend outlook.

Camden Property Trust

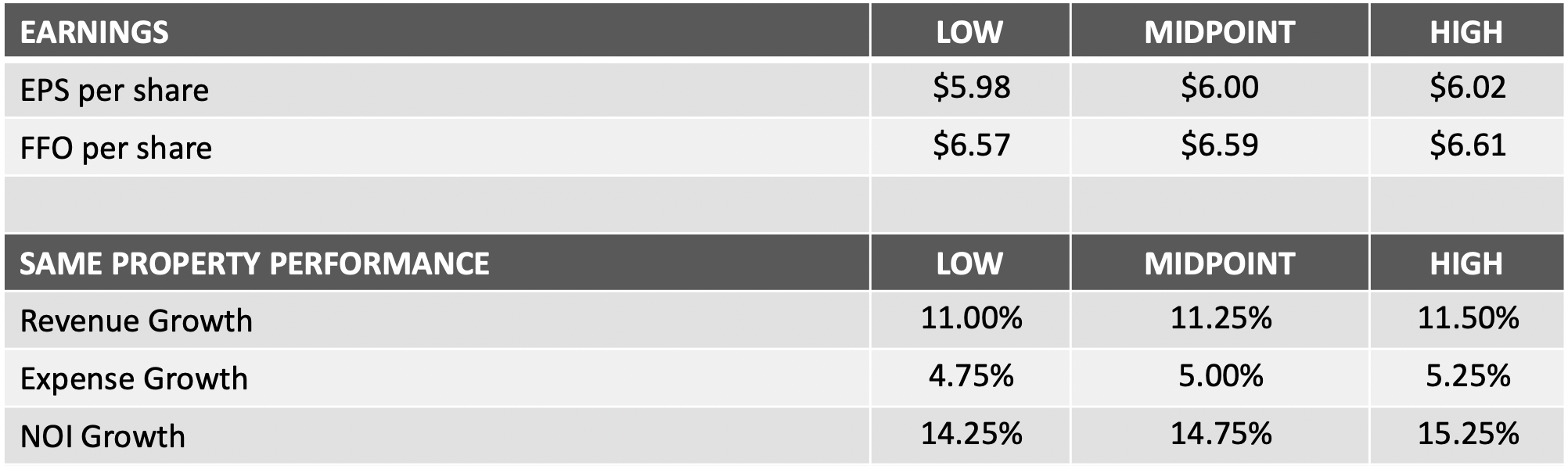

This REIT expects FFO for its full fiscal 2022 to be $6.59 at the midpoint, with NOI growth of at least 14.25% for the year. Shelter and safety are the key provisions of a home. These will always remain in demand even as other property types experience oscillations and volatility due to tectonic behavioural shifts either brought about by digitization or the pandemic. That said, bears would be right to flag that higher interest rates will form a permanent headwind to future FFO growth by making the cost of new developments comparatively more expensive than its near-term average. This combined with a prolonged period of poor economic growth and subsequent slowdown in rental demand would weigh down on future FFO growth.

I expect Camden’s underlying fundamentals to remain strong next year, even though we will see some weakness in occupancy rates and overall leasing demand. The best-case scenario for bulls will likely be the share trading flat throughout the chaos expected. Hence, whilst the 3.37% yield might not be as fat as some other REITs, shareholders are getting a healthy and diversified FFO generator not facing creative destruction of rental demand. The dividends are safe, and I intend to continue to add to my Camden position with a view that the common shares will really only start to recover from the second half of 2024.

Be the first to comment