VichienPetchmai/iStock via Getty Images

Investment Thesis

Calumet (NASDAQ:CLMT) has improvements in its earnings and most of its margins. The company is working hard on its Montana Renewable project to bring it online as expected. Its cash flow remains volatile but its growth prospects are bright. We expect major updates in its next earnings report but also see most of the upside has been priced in by the market .

Company Overview

Calumet Specialty, headquartered in Indianapolis, Indiana, is a specialty refiner that manufacture, formulate, and market refinery products that go into consumer-facing and industrial products as raw materials, on top of conventional gasoline and other fuels. The company has three reportable segments: Specialty Products and Solutions, Montana/Renewables, Performance Brands, and Corporate.

Strength

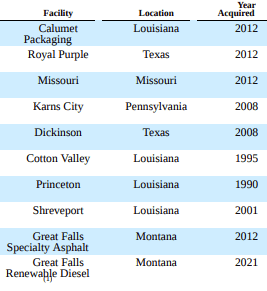

Calumet is one of the largest specialty refiners in the U.S., with a long history of capacity expansion through asset acquisition and organization.

Calumet Facility Acquisition Timeline (company 2022 10k)

When refinery capacity development in the country has been stagnant for over a decade, and new facilities are less likely to be built and invested in, the company’s specialty refiners asset base has increased long-term value strategically and financially. This is the big picture.

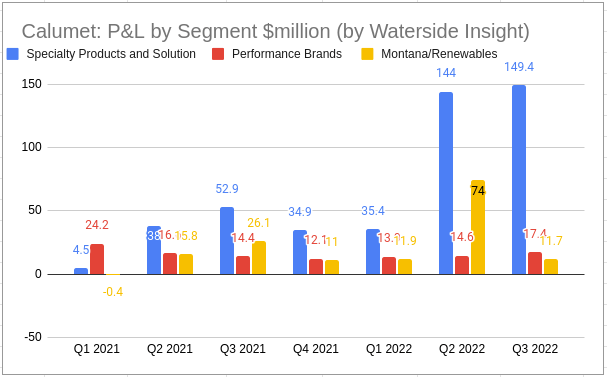

By segments, Calumet’s profit and loss have the highest contribution from Specialty Products and Solutions that which almost accounted for 83.7% for Q3 2022, and it is good to see this segment has grown by almost 4x in recent quarters. At the same time, the Montana Renewables segment has gone from a narrow loss in Q1 2021 to solid profit six quarters later, although it came down from a high of $74 million in the previous quarter.

Calumet Profit and Loss by Segment (Chart by Waterside Insight with data from the company)

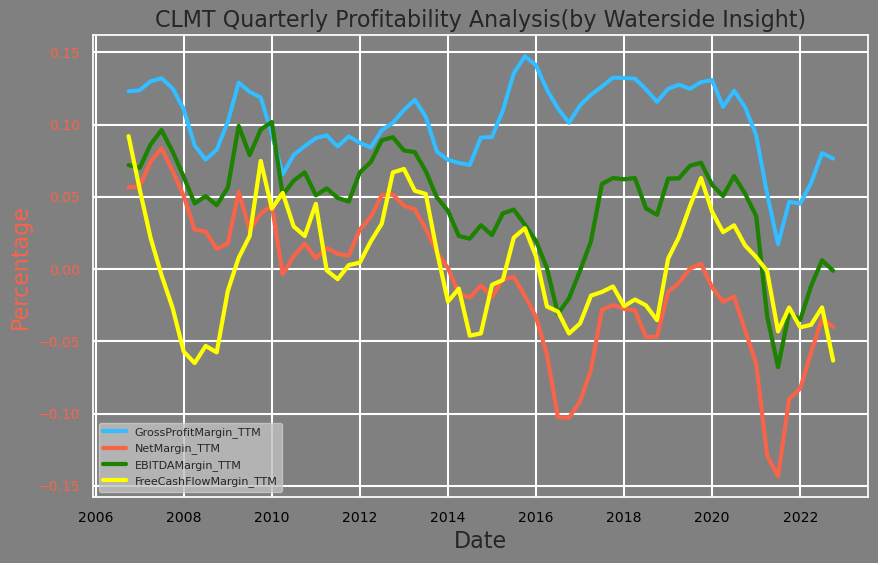

All of Calumet’s margins have staged a turnaround in the latest quarter, except its free cash flow margin.

Calumet Margin Analysis (Calculated and Charted by Waterside Insight with data from the company)

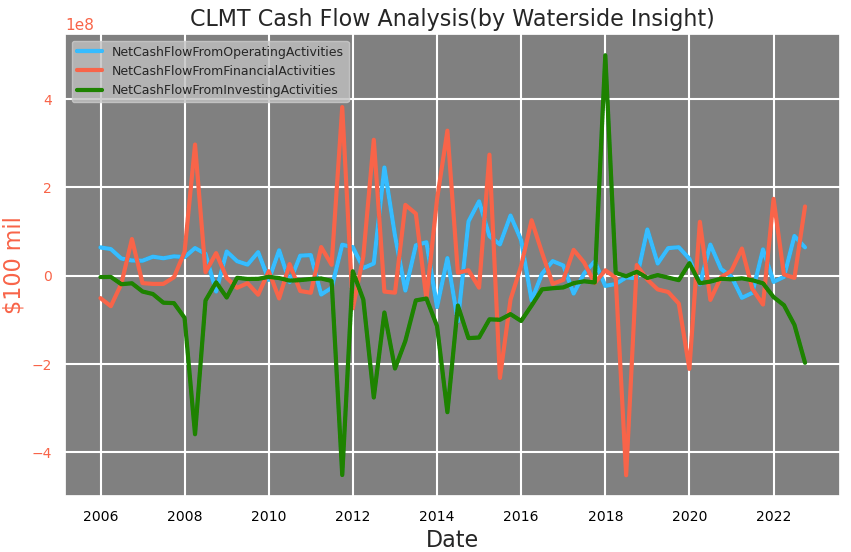

In a breakdown, its cash flow from operating and financing activities is still strong, only from the investing activities dropping. The investing activities used cash of $376.1 million in the first 3 quarters compared to $34.2 million during the same period in 2020. According to the company, the change is mostly due to an increase in cash expenditures related to the renewable diesel project.

Calumet Cash Flow Analysis (Calculated and Charted by Waterside Insight with data from the company)

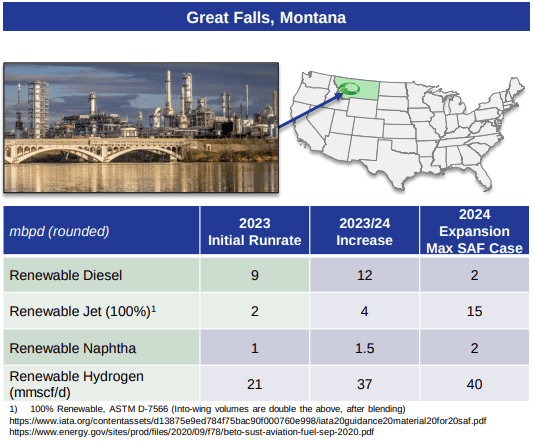

This renewable diesel project is the latest push by Calumet to transition to generate more renewable products while reorganizing its current facilities. The current highest priority for the company to enhance the profitability of its current asset is to complete the renewable diesel project in Great Falls, Montana. It is expected to finish by Q1 this year, and the capacity would be the largest producer in North America in Sustainable Aviation Fuel (SAF), with renewable diesel running online in December last year, and renewable hydrogen and feedstock pretreater growing online in February and March this year – right about now, and more expansion starting in ’24 and ’25.

Calumet Montana Renewable Project Runrate (Company Presentation Jan 2023)

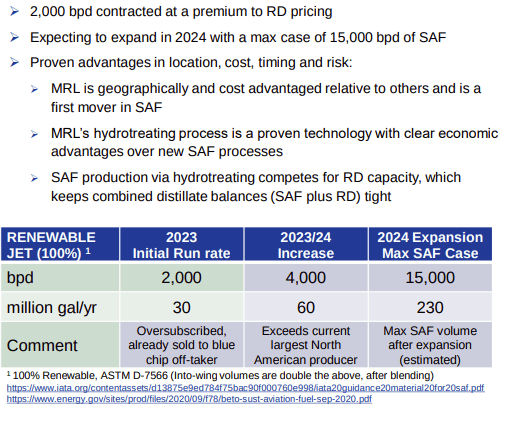

As the company gave a glance at the SAF capacity and contractual activities, we can see the current capacity from the initial run rate of SAF has been oversubscribed and sold. And most of its clients are blue chip, large industrial giants. The later increase in ’23/24 is expected to reach 4000 bpd and 60 million gal/yr, doubling its initial run rate currently reached.

Calumet Montana Renewable Project Capacity (Company Presentation Jan 2023)

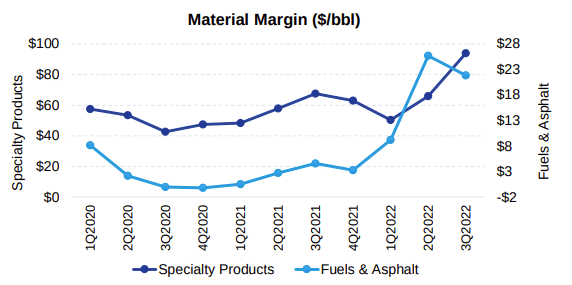

Calumet’s margin by material are going strong by Q3 last year, but the company expects it to be normalized over time.

Calumet Material Margin (Company Presentation Jan 2023)

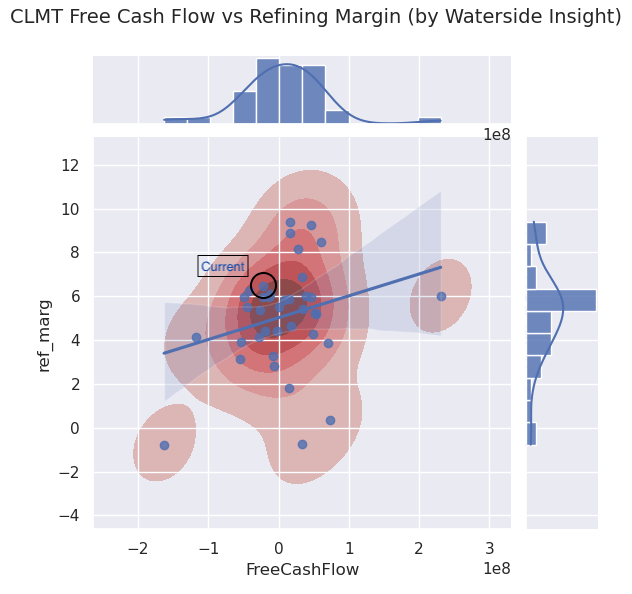

Then we run the historical data to see what would be a normal margin correlated with its free cash flow. With its large spending in investments, its current free cash flow is surprisingly in line with its historical average, given where the refinery margin is. If the cash flow from investing activities subsides, its free cash flow could increase by 30- 60%, even if the refinery margin stays the same. But given its expansion plan at the Montana Renewable, this investment spending with cash could still go on into 2024.

Calumet Free Cash Flow vs Refining Margin (Calculated and Charted by Waterside Insight with data from the company, Nasdaq Link)

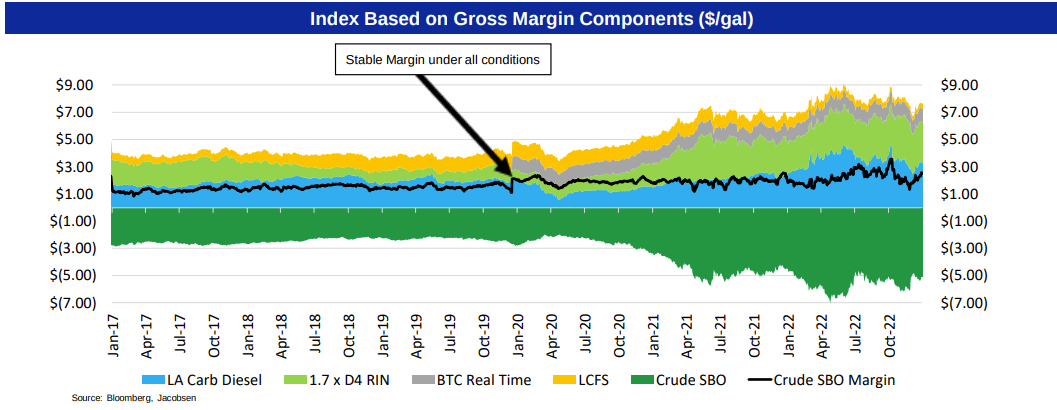

Underlying Calumet’s business model is a stable renewable diesel margin.

Calumet Gross Margin Components (Company Presentation Jan 2023)

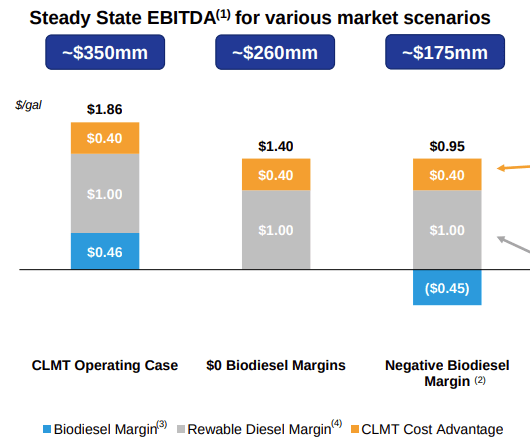

The company gave margin scenarios for its EBITDA depending on where biodiesel and renewable biodiesel margins are. In the bearish negative margin case, it is still having $175 million EBITDA, which is still above its current TTM EBITDA of $132.6 million.

Calumet Steady State EBITDA for various Market scenarios (Company Presentation Jan 2023)

Weakness/Risks

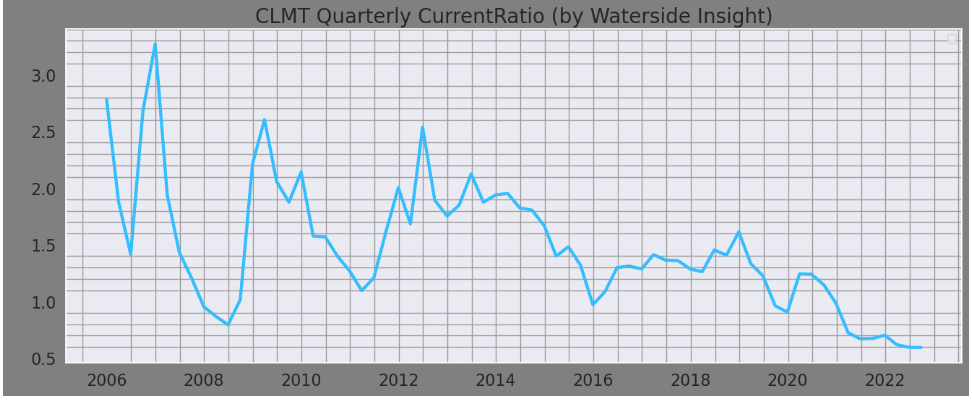

Calumet’s current ratio is running even lower than its lowest point in 2016. It highlights the urgent need for the Montana project to come online and generate cash flow soon for the company, given the cash spending bringing down the liquidity for the company.

Calumet Current Ratio (Calculated and Charted by Waterside Insight with data from the company)

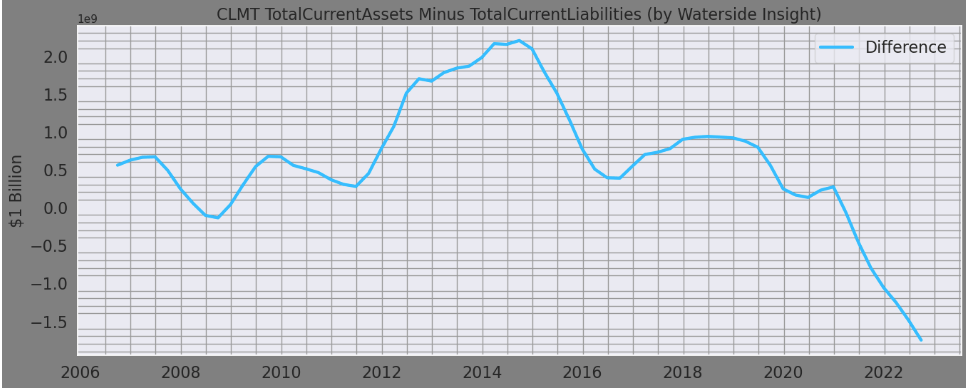

In the meantime, it’s deep in the red when deducting its current liabilities from its current assets. This has been a new phenomenon since 2021 for the company.

Calumet Total Current Asset Minus Current Liabilities (Calculated and Charted by Waterside Insight with data from the company)

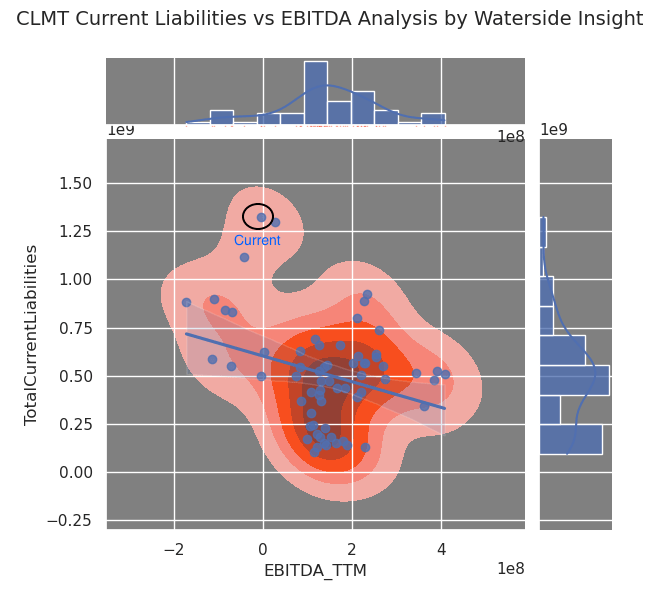

What’s generally valid for Calumet is that the higher its current liabilities, the lower its EBITDA would be. But the good news is its current liabilities are at a historical record, so as long as it could pay them down over time, its EBITDA is more likely to gain from here on than not.

Calumet Current Liabilities vs EBITDA (Calculated and Charted by Waterside Insight with data from the company)

Big Picture

Renewable Biodiesel (RB) differentiates from biodiesel in a way that it is chemically equivalent to petroleum diesel and nearly identical in its performance characteristics, while biodiesel is chemically different. This constraint limits biodiesel can only be blended into petroleum diesel between 2% and 20% of the diesel fuel by volume. But renewable biodiesel can be consumed by traditional diesel engines with any level of the blend, including in pure form, without causing any side effects. And for the producers, RB also has the advantage of being distributed through normal petroleum diesel pipelines. For the benefit of reducing greenhouse gas, RB has some of the highest scores with existing fuel pathways in programs that include the federal Renewable Fuel Standard (RFS), the California Low-Carbon Fuel Standard (LCFS), the Washington State Clean Fuels Program and the Oregon Clean Fuels Program.

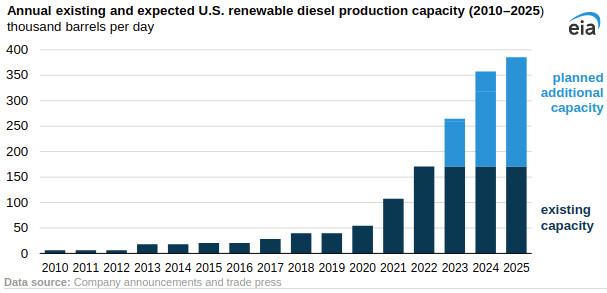

Existing and Expected US Renewable Diesel Production Capacity by 2025 (“EIA”)

The renewable biodiesel production capacity in the U.S. could double in 3 years’ time. If this is the case, the majority of the West Coast’s distillate fuel needs could be met by renewable diesel instead of by importing. This is both the tailwind and increasing competition for Calumet’s development in RB and other renewable products. In other words, the company cannot afford to fall behind when almost seven other similar projects are announced or undergoing.

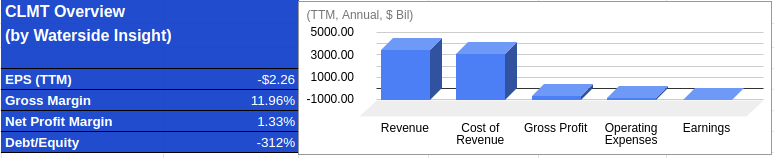

Financial Overview

Calumet Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

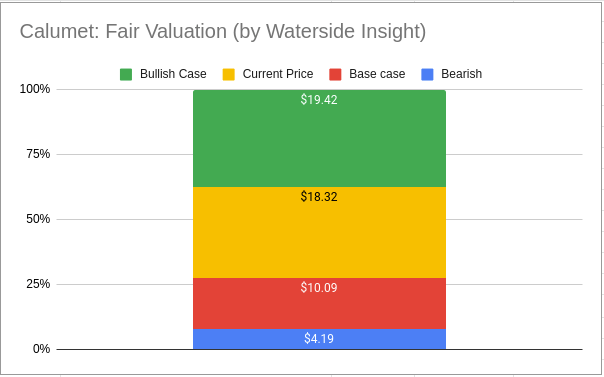

Valuation

We summarize all our analysis above and use our proprietary models to assess Calumet’s fair value with a ten-year projection ahead. Calumet has a volatile cash flow history, not least because of the acquisitions that have been strategically important for the company over the years and the capacity expansion. We expect this trend to continue as more of the refining capacity in the country is consolidated and upgraded. In our bullish case, Calumet has four years of positive cash flow growth from here on and another explosive growth spur down the road, and we priced in at least two more significant acquisitions; the stock was valued at $19.42. In our bearish case, we move up some of the acquisition spending as the company continues its renewables upgrade. While it still has explosive growth down the road, it also encountered more costs and expenses; it was valued at $4.19. In our base case, we expect a smoother growth path five years from now than in the bearish case; while still expecting four years of cash flow growth, the spending schedule also moved up as well. In this case, it was valued at $10.09. The current market price is a tad below our top-line estimate.

Calumet Fair Valuation (Calculated and Charted by Waterside Insight with data from the company)

Conclusion

Calumet has made improvements in its financials in the latest quarters, making not only large increases in profits in its core specialty products but also significant progress in its renewables. Under the current backdrop of the domestic push for renewable fuel, Calumet’s Montana Renewable project not only holds the promise of delivering the results of its own expectation, but also establishing a solid foothold for the company in this sector. Although the company currently has the largest debt burden on record, its growth can help it reduce this burden and improve earnings. Investors have good reasons to be enthusiastic, but much of the projected upside could have been baked into the price. We have been investors in Calumet on and off in the past ten years; at the current level, we recommend a hold but maintain an optimistic view.

Be the first to comment