Editor’s note: Seeking Alpha is proud to welcome Joudi Capital as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

DrDjJanek

Introduction

We believe iShares 20+ Year Treasury Bond ETF (NASDAQ:TLT) will temporarily go up in price due to the market believing that the FED will pivot. However, due to global demographic collapse and de-globalization, temporary supply shortages will increase and will most probably cause the CPI to keep rising. Consistent higher inflation alone is worse off for bonds. Inflation will probably keep rising until domestic supply handles the supply shock. A high inflationary environment would be worse off for bonds regardless if the FED pivots or not.

Investment Idea

Since there’s a strong chance that inflation will stay high this decade, we take a bearish position on US bonds by shorting TLT through put options with a $85 strike price and a Jan 2024 expiry based on the belief that bond yields will reach 5% by the end of 2023.

TLT – A Deep Dive

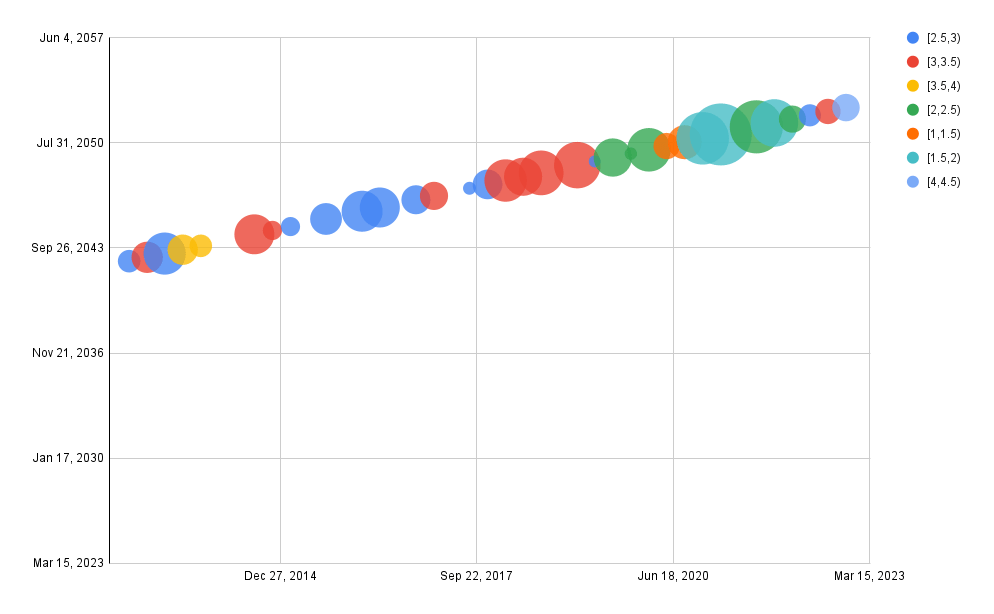

TLT holds treasuries to ensure maturity 20-30 year ahead of current date. Hence, it holds onto 30-year treasuries for 10 years, and 20-year treasuries for a single year. TLT shows a low amount of holdings in 30-year treasuries with high coupon rates, hence it is not fully benefitting from the current high coupon market.

TLT Holdings (iShares)

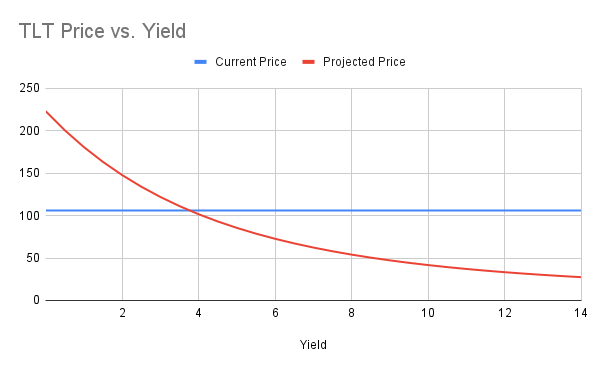

TLT is very sensitive to bond market yields and its Net Asset Value (NAV) can quickly drop to around $85 if yields go up to 5%.

TLT Price vs Yield (iShares)

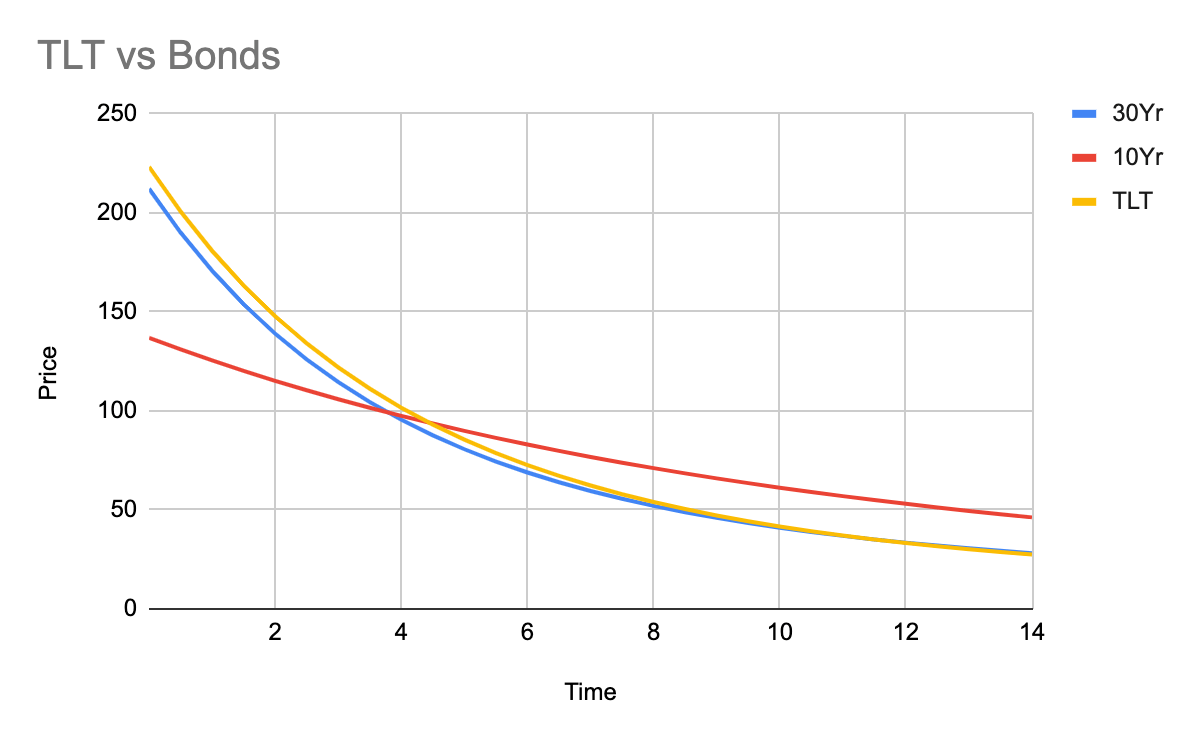

When comparing TLT to the 30Yr and 10Yr bonds we can see that TLT has a slight price sensitivity advantage to the 30Yr bonds.

TLT vs Bonds (iShares & Treasury)

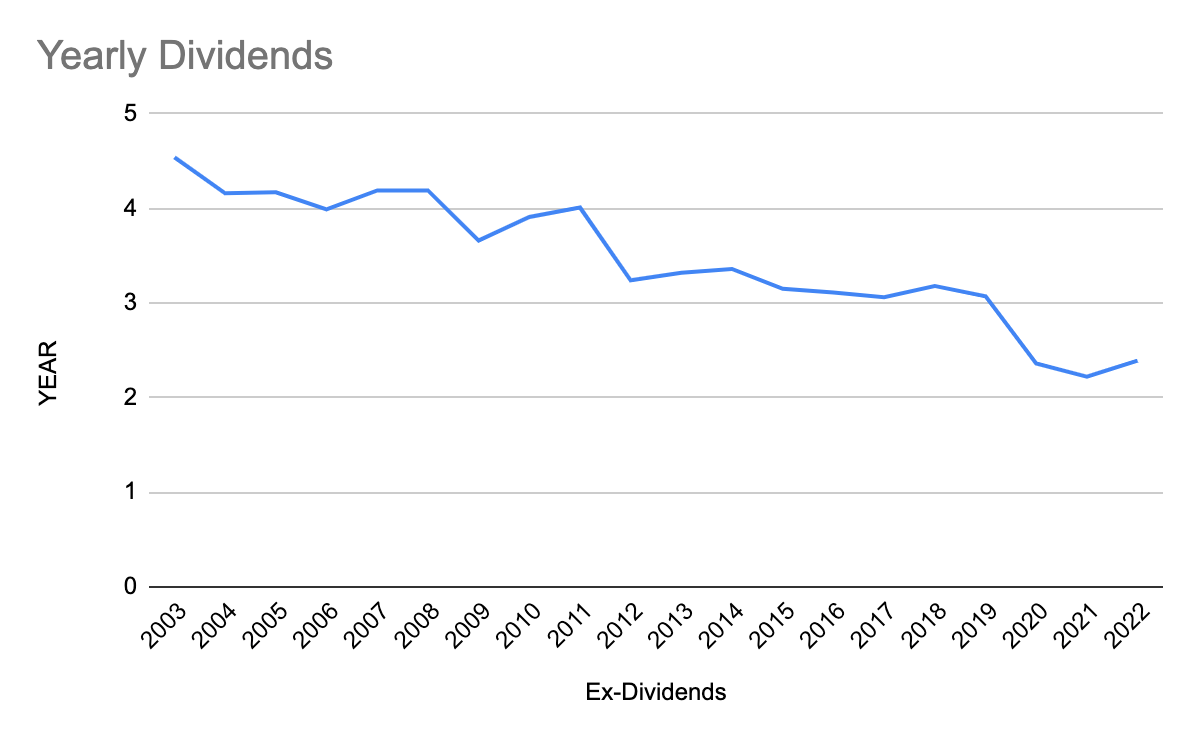

As of 2022 the yearly dividend returned is around $2.5 per share, which is less than what you get with a portfolio of treasury bonds from the most recent auction. Hence, it seems the main benefit of TLT is the ease at which you can buy and sell your share.

TLT Yearly Dividends (iShares)

TLT lost around 30% of its market price this year and it is now back to 2014 price levels. The price was initially high because treasury bond prices spiked due to Quantitative Easing. The price is currently decreasing because treasury bond prices have decreased due to the Federal Reserve raising the FED funds rate.

TLT Price (seekingalpha)

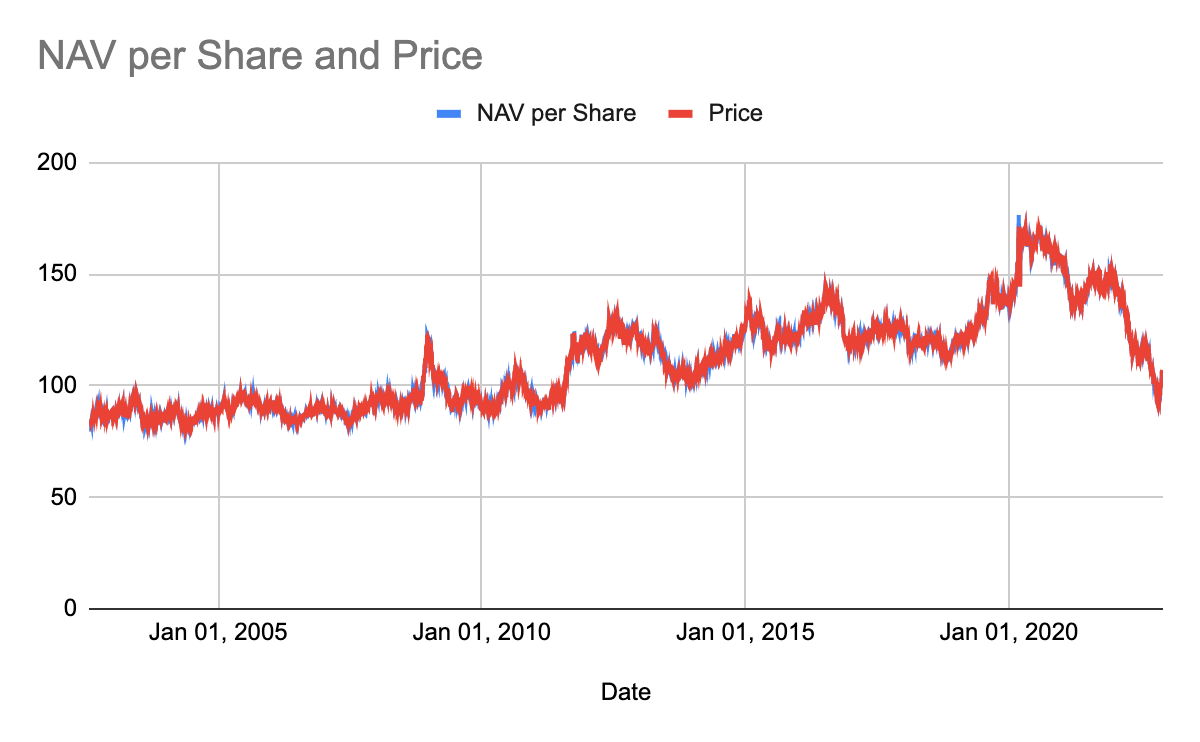

TLT’s market price matches its NAV almost perfectly. Therefore, any TLT trade decision is purely based on whether the treasury bond rates will go up or down in the future.

NAV vs Price (iShares)

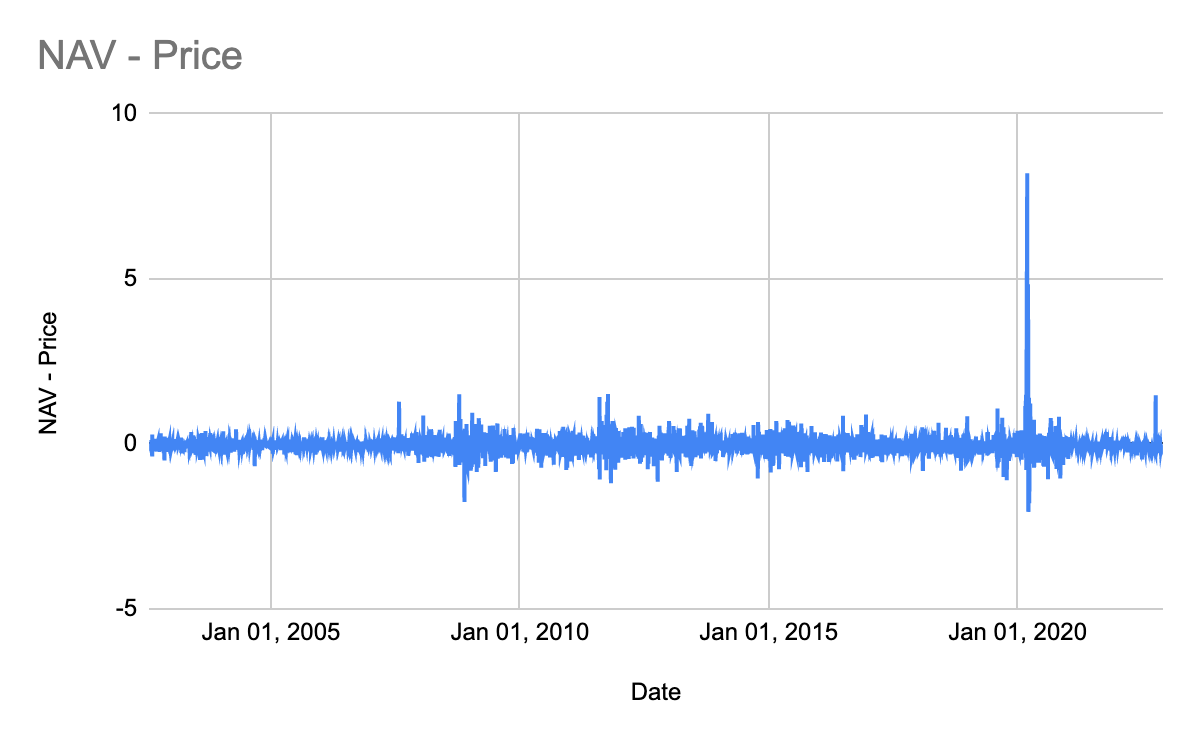

There are some cases where NAV did not follow the price efficiently. For example, during the COVID-19 shock in March 2020, we saw a spike to 8.5 in the deviation between NAV and Price, as the chart below shows.

NAV-Price (iShares)

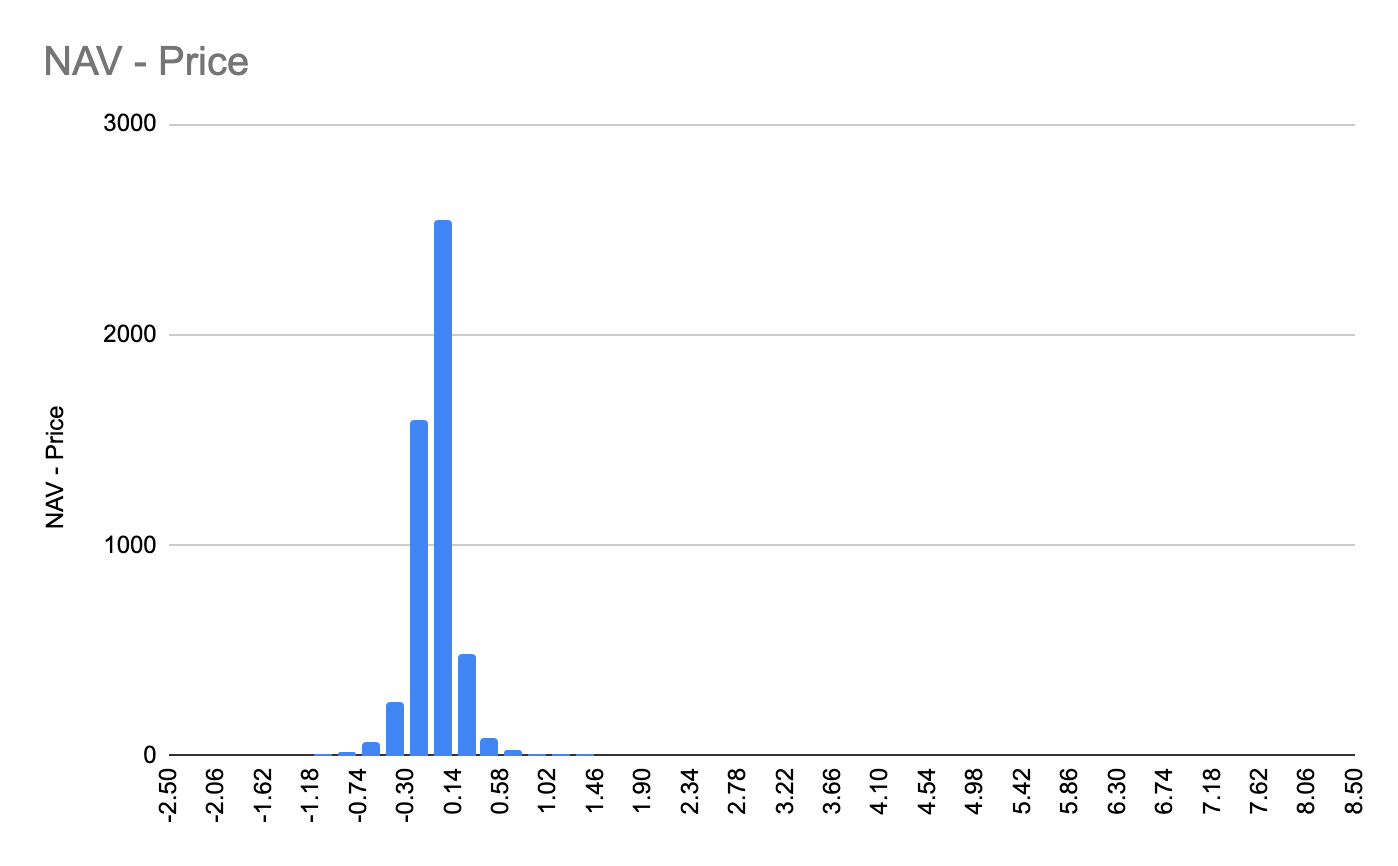

It’s quite rare for this to occur, as can be seen below. Majority of the cases NAV meets price with only a slight deviation of around [-0.3$, 0.14$].

NAV-Price Histogram (iShares)

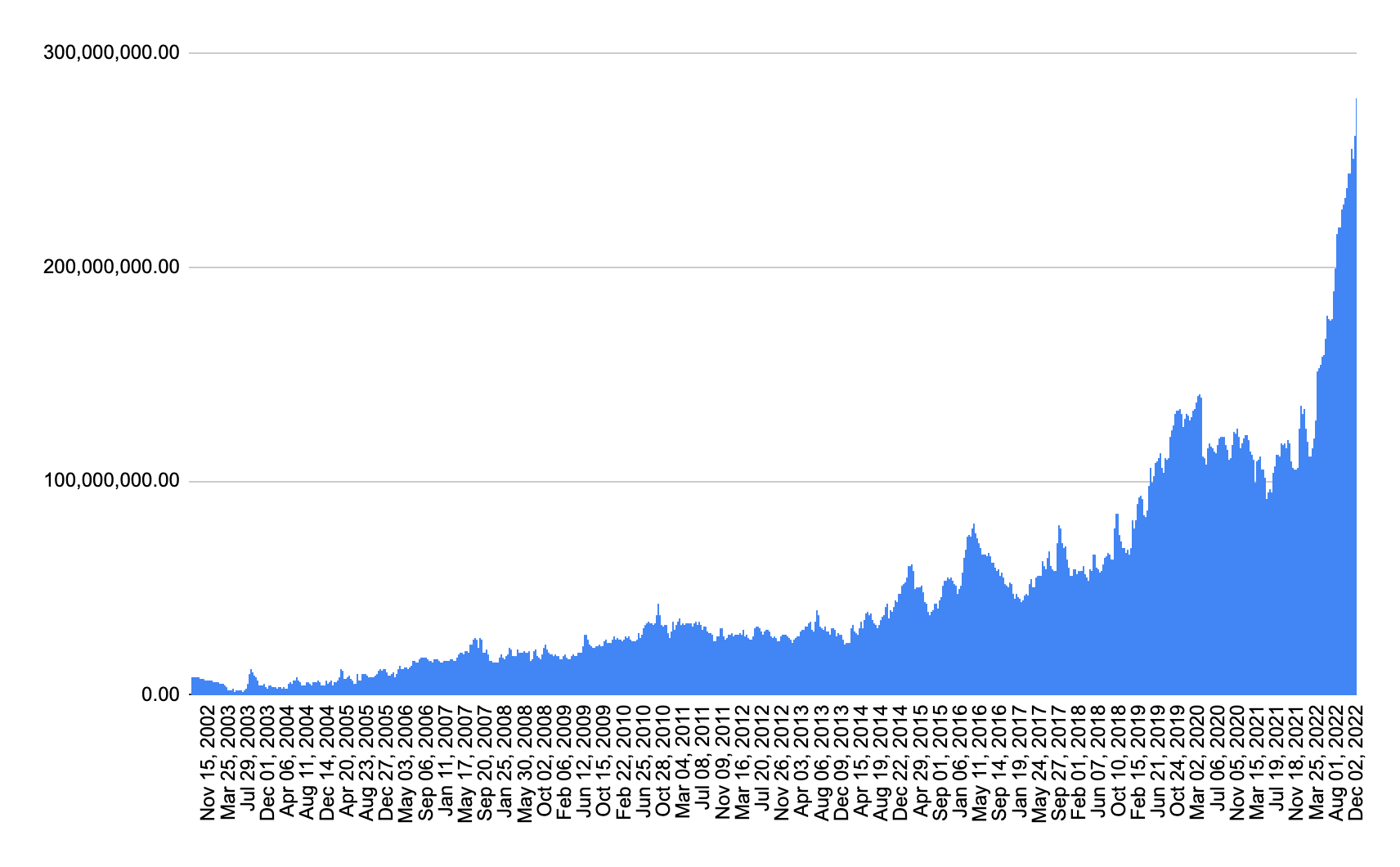

TLT shares outstanding has recently reached around 270 million which is nearly 5x the amount in 2014. Roughly around 150 million of these shares came in 2022 alone. Around 270 million shares hold around 28 billion in bond holdings with effective dates between 2012 and 2022. If bond prices stay on a downward trajectory it can be harder for TLT’s share price to match its NAV since it’ll have to exchange much more shares with Authorized Participants (APs).

TLT Shares Outstanding (iShares)

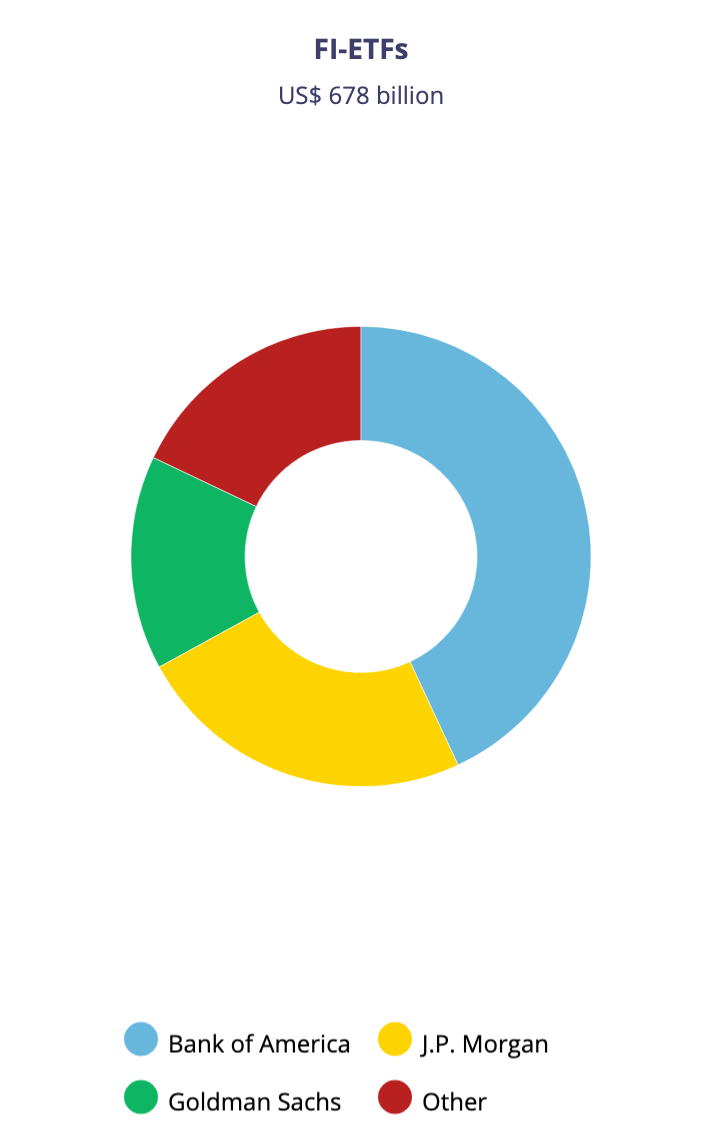

Based on a study conducted by the Bank of Canada, in 2019 Bank of America, Goldman Sachs and J.P. Morgan were the APs for around 82% of fixed income ETFs. This risks a crowding problem where lots of fixed income shares exist and only 3 banks are available to redeem 82% of them. Any illiquidity in the bond market will cause large deviations between the NAV and the share price of the ETF. The potential risk here is if inflation keeps going up consistently until bond holders lose confidence in the market, prices can misalign with their NAVs since APs will not want to exchange shares for the underlying bonds. However, we do not see a high chance of this happening since we believe bond holders won’t lose confidence very easily and would hold at prices below NAV.

FI ETF Concentration 2019 (bankofcanada)

Since TLT’s share price efficiently follows its NAV which is purely based on the treasury bond market, the main thing we’re speculating on is whether the bond market will decide to raise rates in 2023 or not. Hence, our trade decision is purely a question of whether inflation will stay rising until the bond market decides to raise the rates to 5%. We do believe that to be the case.

Has Inflation Peaked?

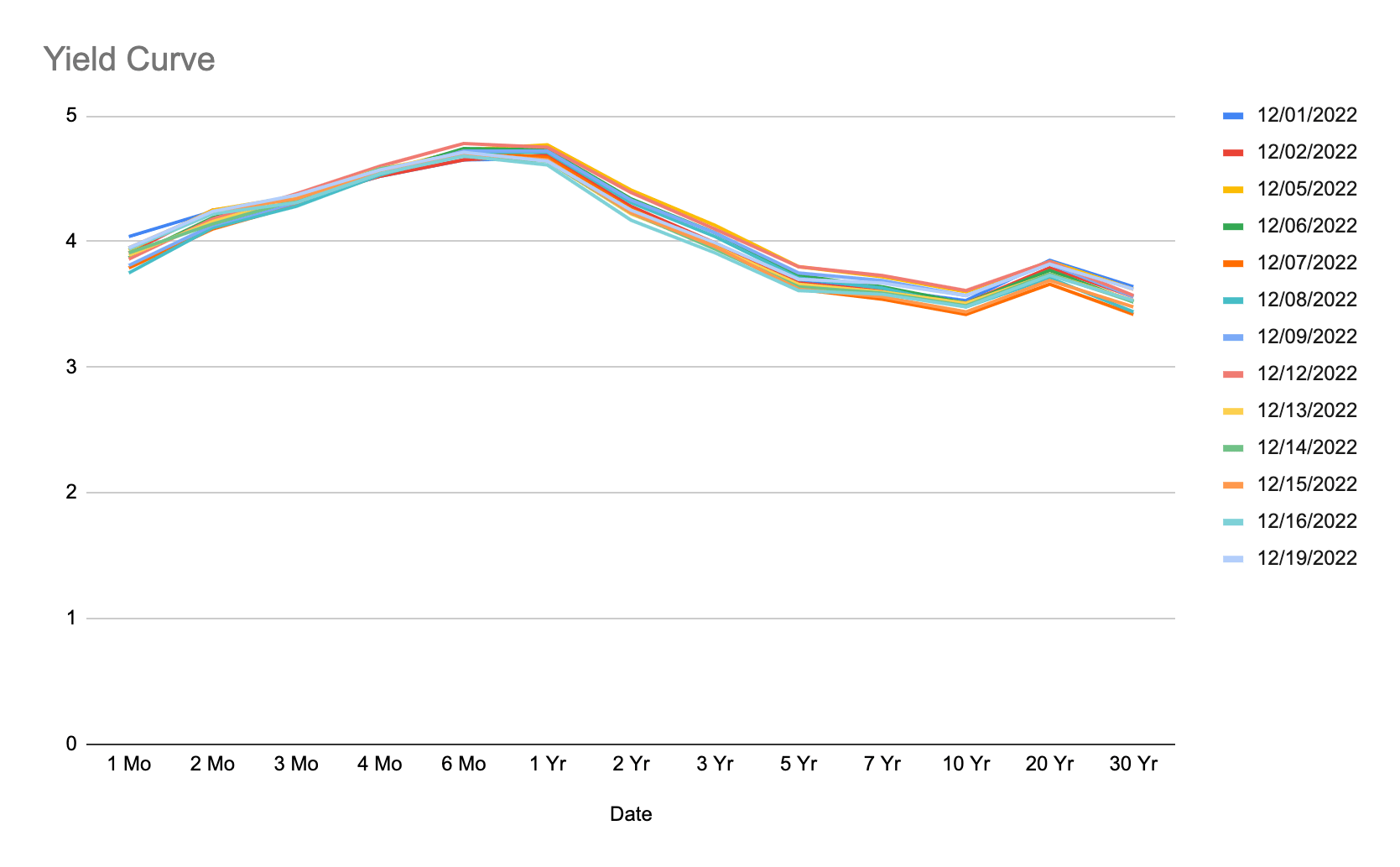

The narrative is that a recession has been reached, inflation is going down, and the FED’s hawkishness will break something in the financial system very soon. This means the FED will pivot and that inflation is resolved, which means that the bond market will have a strong rally soon. We can already see the yield curve inverting which usually signals an upcoming recession.

Yield Curve (Treasury)

However, we believe that inflationary pressures will consistently stay rising in 2023 much higher than deflationary pressures and the bond market will eventually raise rates to increase real bond yields.

Historically No

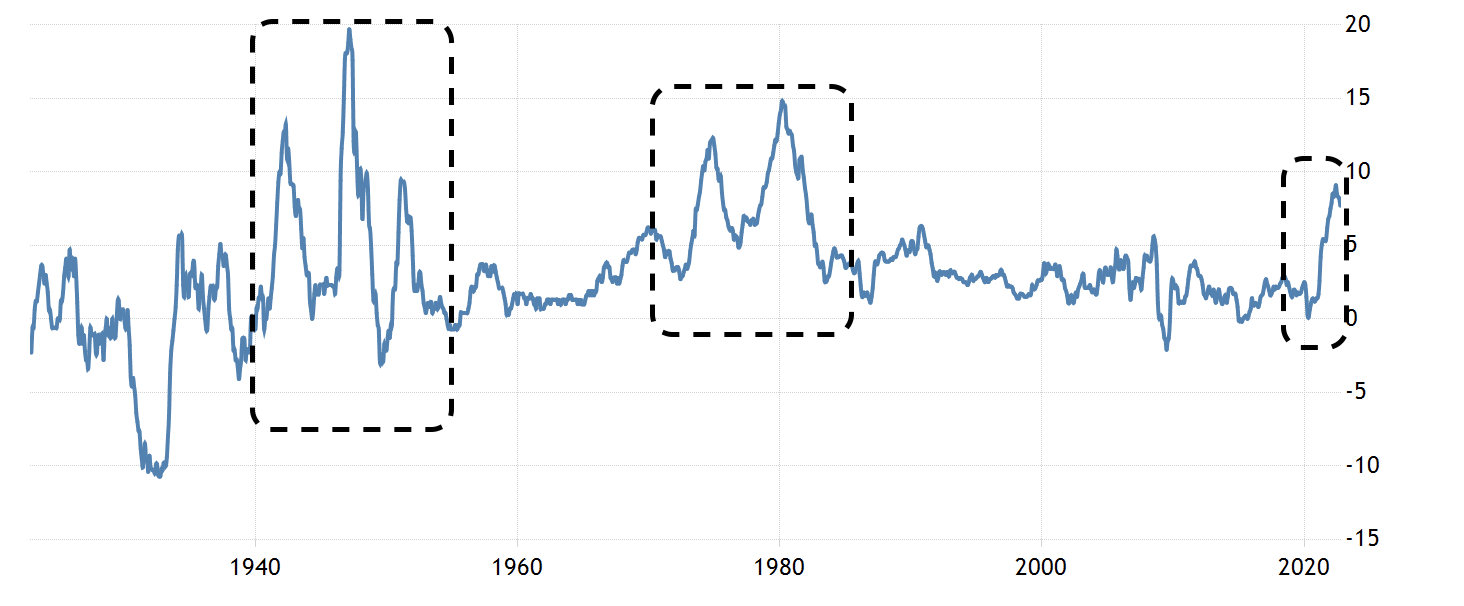

Firstly, whenever inflationary pressures occurred in the US market, the US market went through at least two peak-trough cycles. Of course, this does not necessarily mean it will also happen this time. But it’s highly likely to happen since it happened twice in the past 2 times that inflation hit the markets.

US Inflation (Trading economics)

Global Demographic Collapse

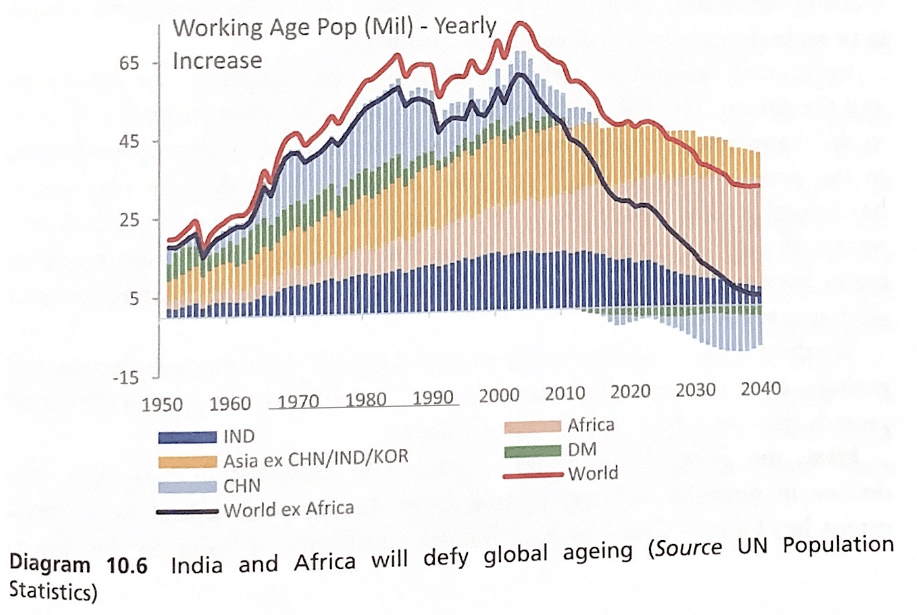

Secondly, the global demographic collapse has a high chance of occurring this decade. As can be seen in the figure below taken from the book The Great Demographic Reversal, higher labor shortages will take place. Developed markets’ working force has been decreasing since 2012. The developing markets’ increasing working force will not be enough to handle the decrease in the work force globally. Higher labor shortages will push wages higher which will cause further price increases.

Working Age Population Decline (The Great Demographic Reversal)

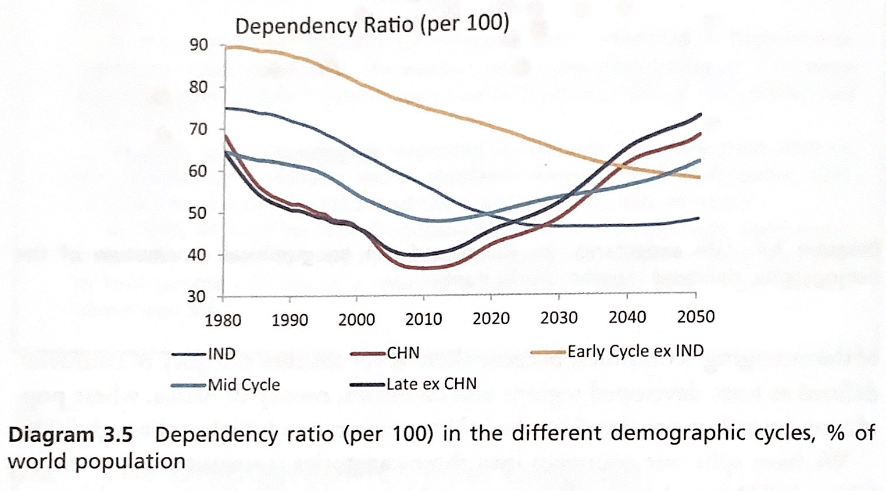

We can also see a forecasted 1000 bps increase in the developed market’s dependency ratio this decade. Roughly 5-7% of the developed markets’ population will retire and add onto the retiree population, which can impact pensions and the stock market negatively. This will also push tax revenues lower causing governments to place a higher dependency on debt.

Dependency Ratio (The Great Demographic Reversal)

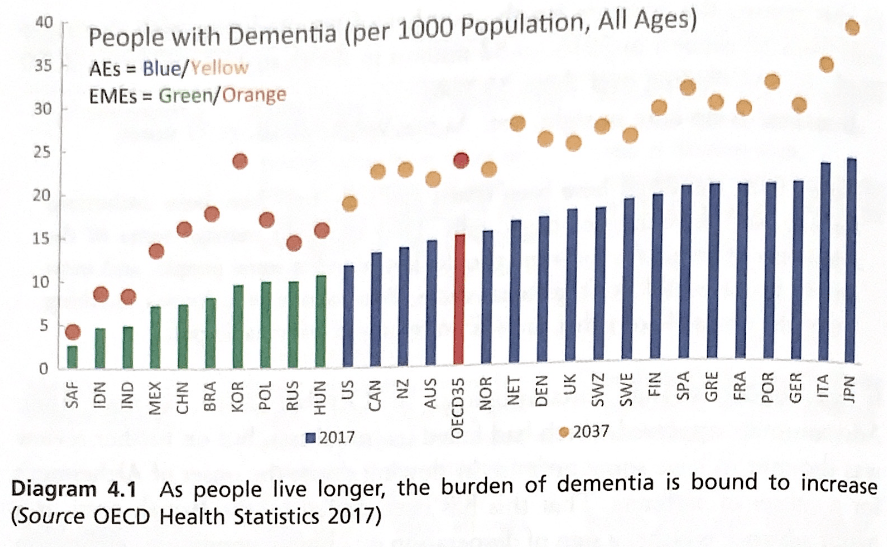

Aging-related diseases will be abundant in the aging developed markets. This will cause higher healthcare costs and can contribute to an increased CPI.

Dementia Rise (The Great Demographic Reversal)

De-Globalization

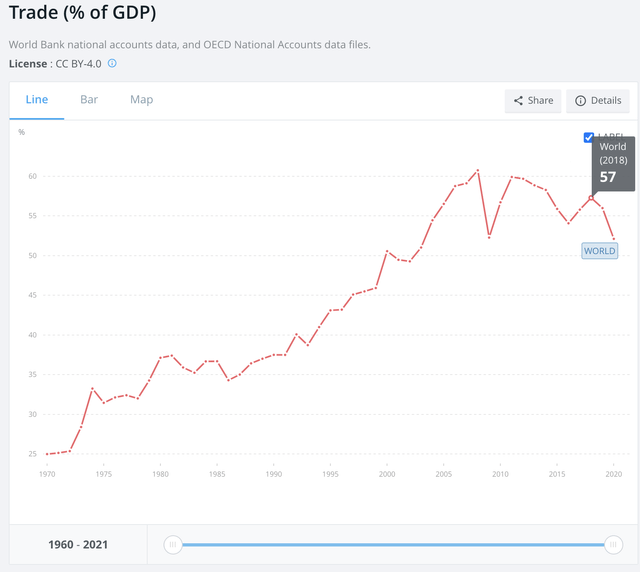

Thirdly, de-globalization has a higher chance of occurring this decade. We can already see the trend downwards for global trade as a percent of GDP. A global demographic collapse can disrupt export/import flows which will further reduce trade and this can increase tensions between countries. This can cause global supply chain shocks which will further increase prices.

Trade vs. GDP (data worldbank)

These 3 points make quite a strong case as to why inflation has a high chance to keep on rising in the US this decade. Hence, we speculate that the bond market will raise rates in 2023 to counteract the loss in real bond yields.

Risks vs Thesis

The main risk to the thesis is if US domestic supply quickly handles de-globalization and population collapse impacts. We already see the US working on improving its manufacturing capability and investing in its infrastructure. Semiconductor manufacturing and Lithium production companies are already working towards expanding their domestic production in the US. However, these things do take time to fully materialize.

A second risk to the thesis is that the hawkishness by the FED actually pushes demand much lower than the expected supply shocks. If that’s the case then inflation would stop increasing. However, we believe that the upcoming supply shocks are much stronger than the expected loss in demand.

A third risk is that the upcoming housing market crash can show strong deflation which can keep reported inflation low in 2023. This can possibly push bond prices high temporarily. However, we believe that when the deflationary pressure from the housing market subsides, inflation can come back even stronger.

Finally, shorting TLT by buying put options with a 1-year horizon is highly risky since every dollar increase in TLT would lose $15 on the trade. Additionally, every day that passes would lose around $0.7. Sizing the trade is important to reduce losses in case any of the above-mentioned risks take place.

Conclusion

In conclusion, we believe inflation will keep trending higher this decade and this will cause bond prices to drop even further. Hence, we take a short position on TLT through put options with a $85 strike price and Jan 2024 expiry. We believe there’s a high probability that inflation will keep trending higher due to supply headwinds from the demographic collapse and de-globalization. A high inflationary environment is worse off for bonds even if the FED pivots.

Be the first to comment