Lacheev

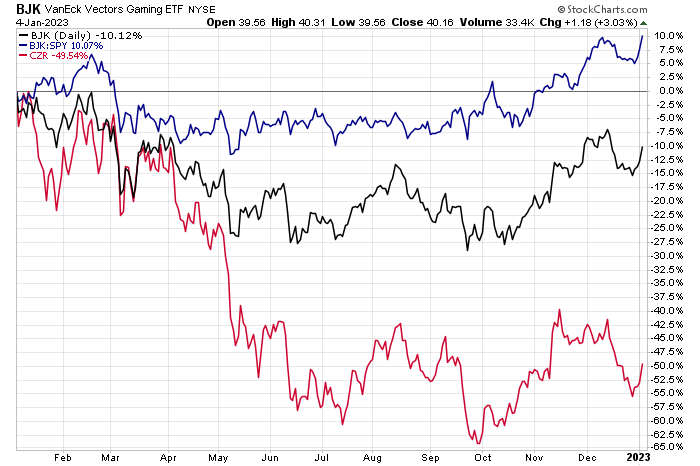

Looking for some alpha and momentum in this tough market? You might want to place your bets on the VanEck Vectors Gaming ETF (BJK). The fund that holds many casino and gaming stocks has beaten the S&P 500 by about 10 percentage points in the last year.

One name was mired in a steep downtrend before recently showing some bullish price trends. But how do the growth and fundamentals line up with Caesars? Let’s take a look.

Gaming (Relative) Gains

StockCharts.com

According to Bank of America Global Research, Caesars Entertainment, Inc. (NASDAQ:CZR) is a US gaming operator formed after the combination of ERI and CZR in July 2020. The company has a significant footprint in Regional Gaming and Las Vegas. The company operates casinos comprising poker, keno, race, and online sportsbooks; dining venues, bars, nightclubs, and lounges; hotels; and entertainment venues. It also provides staffing and management services; accessories, souvenirs, and decorative items through retail stores; and online sports betting and iGaming services.

The Nevada-based $9.1 billion market cap Hotels, Restaurants and Leisure industry company within the Consumer Discretionary sector has sharply negative trailing 12-month GAAP earnings and does not pay a dividend, according to The Wall Street Journal.

A bounce back in Las Vegas gaming revenue is a tailwind for many casino and gaming stocks, but there remain uncertainties with respect to how the sports betting landscape evolves along with legislative and regulatory concerns. But BofA notes that asset sales and more JVs and licensing agreements could be good for Caesars.

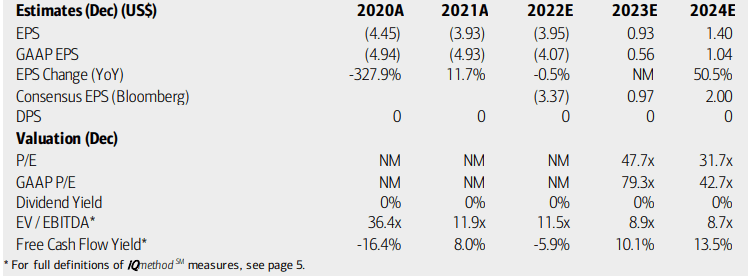

On valuation, analysts at BofA Global Research see earnings reversing course from big losses since 2020 to per-share profits by FY 2023. Strong EPS advances are then expected in 2024. The Bloomberg consensus forecast is slightly more upbeat compared to what BofA sees, too. Still, no dividends are expected on this volatile and cyclical stock. Both the operating and GAAP earnings multiples will be considerably above the market while the firm’s EV/EBITDA ratio is actually about on par with the average in the S&P 500 right now.

What’s encouraging is that CZR is projected to generate significant free cash flow starting in its next fiscal year. Overall, I think more time is needed to see if gaming and sports betting revenue is accretive to earnings before getting long on valuation.

Caesars: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

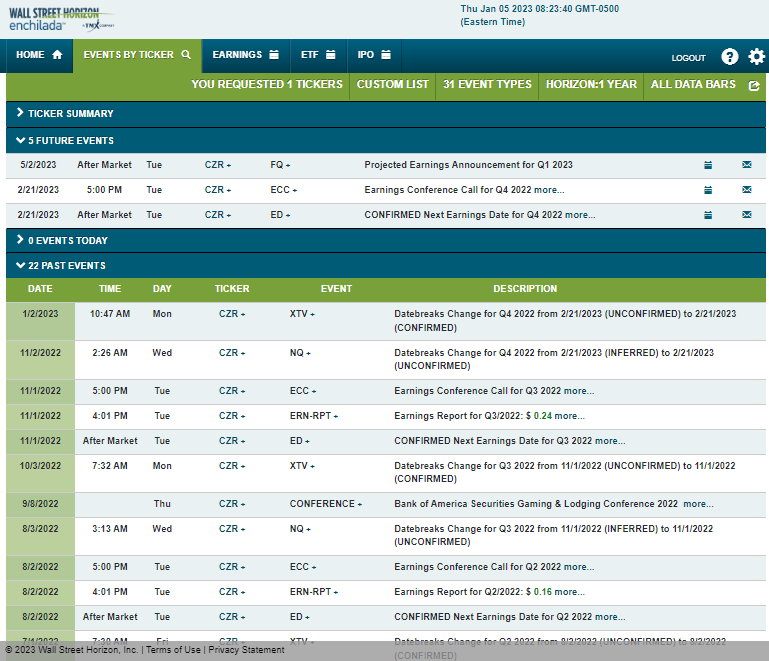

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Tuesday, February 21 AMC with a conference call immediately after results hit the tape. You can listen live here. The calendar is light on volatility catalysts aside from the earnings event.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

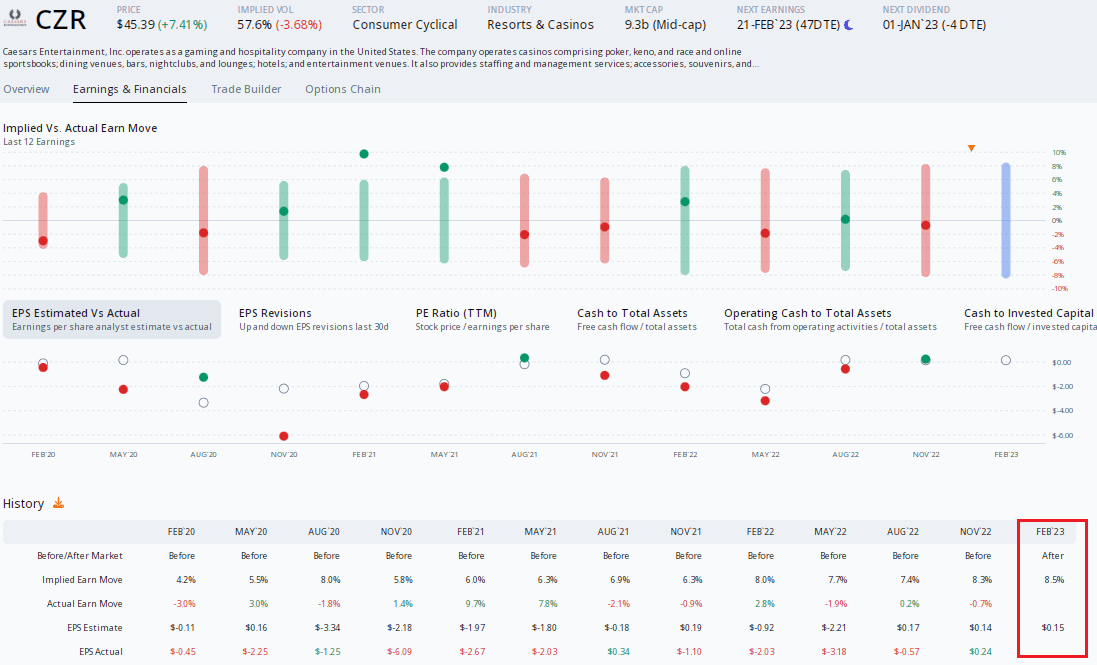

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS figure of $0.15 to be reported in February, which would be a positive turnaround from $2.03 of per-share losses endured in the same quarter a year ago. Unfortunately, the company has a poor earnings beat rate history, but there has been a single upward analyst EPS revision since the last reporting date, per ORATS.

As for the implied stock price swing post earnings, the current at-the-money straddle that expires soonest after the reporting date shows an 8.5% move up or down priced in. What’s interesting is that the stock rarely moves much after reporting, so that option premium could be expensive. I would be a net seller of the straddle based on that.

CZR: Expensive Options Ahead Of Earnings

ORATS

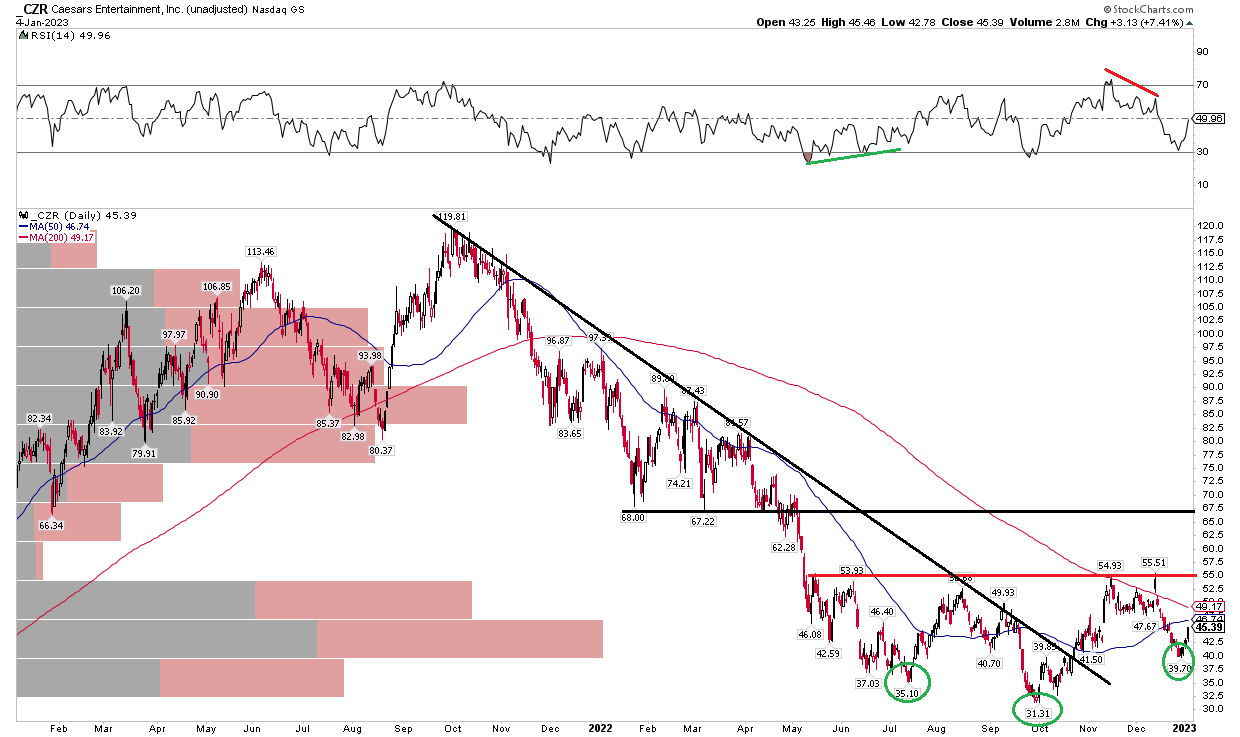

The Technical Take

There are some green shoots in the chart of CZR. Notice in the chart below that shares have broken a downtrend resistance line off the October 2021 peak near $120. After hitting a July 2022 low just above $35 and undercutting that spot in October, around $31, the stock appears to have put in a higher low just shy of $40 recently. But a move to $55 and change came on bearish divergence, which led to a swift pullback.

Overall, I’d like to see shares rally above the falling 200-day moving average and the $55 to $56 zone – there is not much overhead supply until near $75 on the chart. Overall, there are constructive signs here, but more work is needed by the bulls.

CZR: Downtrend Broken, But No Uptrend Yet

StockCharts.com

The Bottom Line

Both the fundamental valuation and technical chart show some positive signs looking ahead, but there is more for both facets to prove to get truly bullish on Caesars.

Be the first to comment