Urupong/iStock via Getty Images

Written by Nick Ackerman. A version of this article was originally posted to Cash Builder Opportunities on December 21st, 2022.

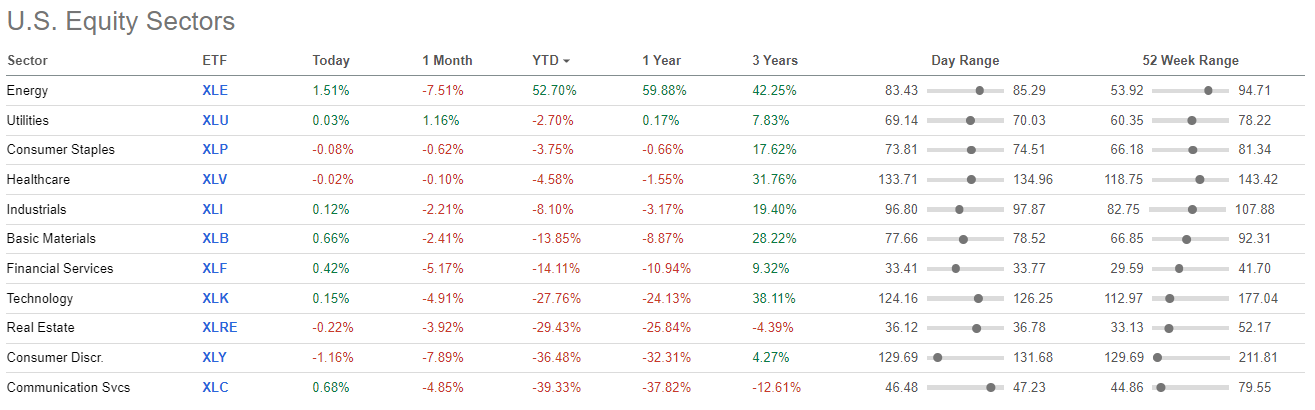

Real estate investment trusts, or REITs, were hit quite hard in 2022. They were one of the worst-performing sectors. That’s also in a year where we aren’t seeing a lot of winners overall, so it certainly isn’t specific to REITs.

SPDR Sector Performance (Seeking Alpha)

However, REITs do have a couple more factors to deal with when higher interest rates hit. The two most notable negatives with higher interest rates are the higher costs for REITs in terms of financing. The other hit is that when risk-free rates rise, the attractiveness of the yield on a REIT becomes less tempting.

That being said, in a recent report from Cohen & Steers (CNS), they highlighted several things that REITs have going for them. C&S are REIT experts whose assets are tied up to REITs in a big way. A majority of their funds are REIT or infrastructure related.

Therefore, understandably, there will be some positive bias in their reports. I’d still encourage giving the entire report a read, it isn’t long, but I am only going to focus on a couple of the main points.

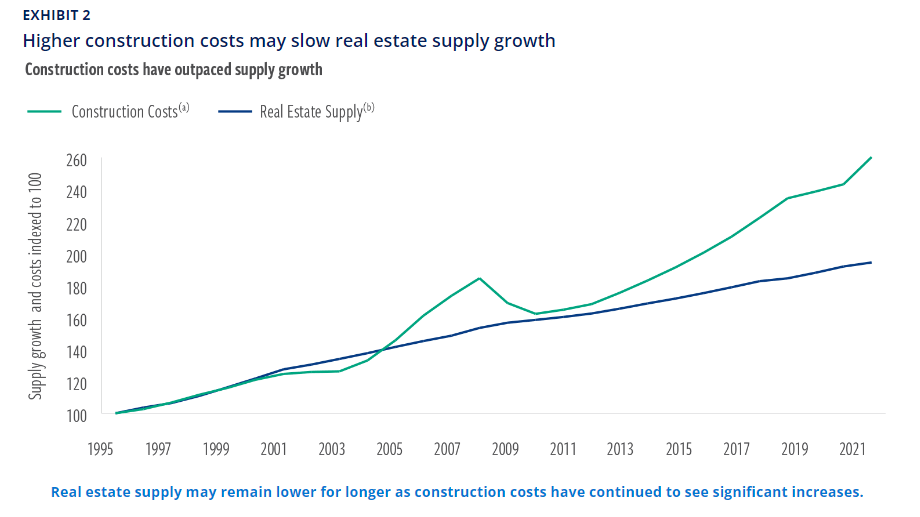

First, they noted that they are taking down their growth expectations for REITs for next year “amid a slowing economic backdrop.” They noted that construction costs are higher – there is the negative impact of inflation playing a role.

Real Estate Construction Costs (Cohen & Steers)

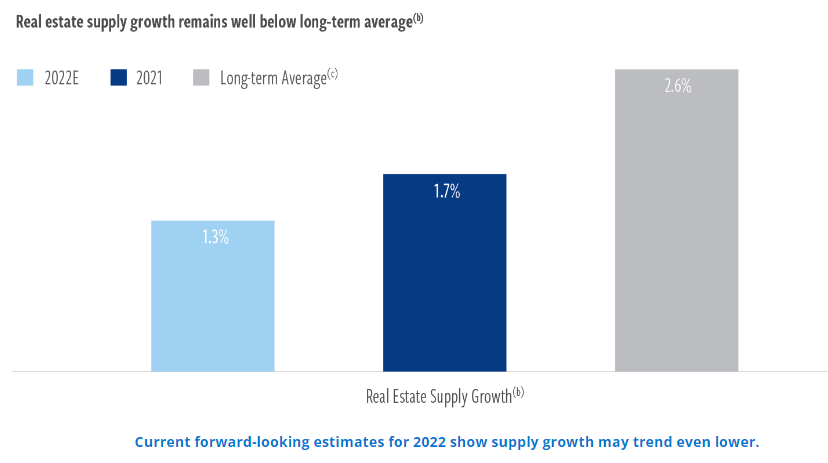

At the same time, they noted that the real estate supply is lower. That’s a key difference for this down cycle, since construction costs are up, meaning real estate supply should stay lower for longer. That could make what’s already available out there more valuable.

Real Estate Supply Growth (Cohen & Steers)

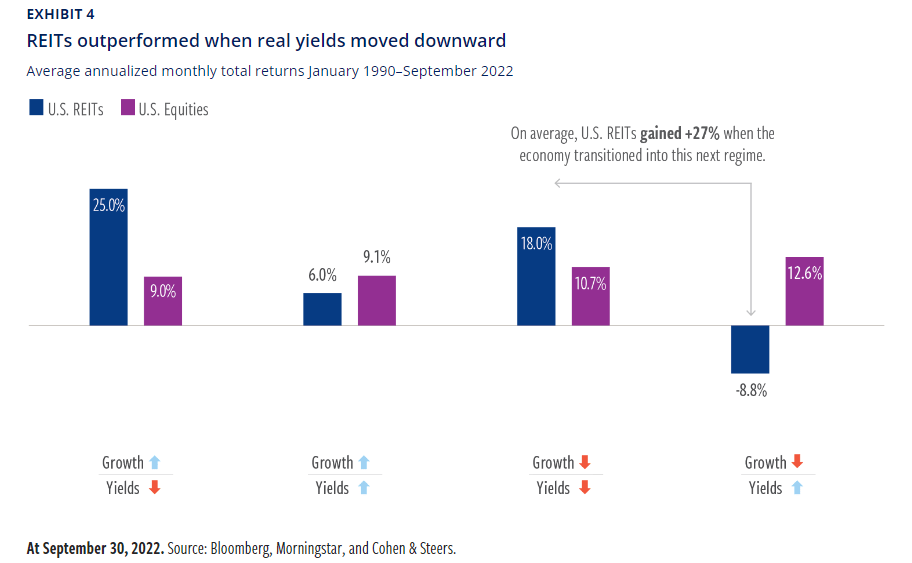

The second point that I believe is worth a specific highlight is the potential for REITs going forward. Yes, rates are expected to continue to rise through 2023, at least according to the latest Fed announcements. Whether that ultimately happens or not is yet to be determined. The main point here is the “buy low, sell high” mantra. Or my preferred twist of “buy low and possibly never sell.”

When switching from an economic transition of a high yield to a low yield, REITs have proven to be huge beneficiaries. They get hit with low growth and high yield, but ultimately that unwinds at some point. At least according to history from January 1990 to September 2022.

REITs Performance In Different Situations (Cohen & Steers)

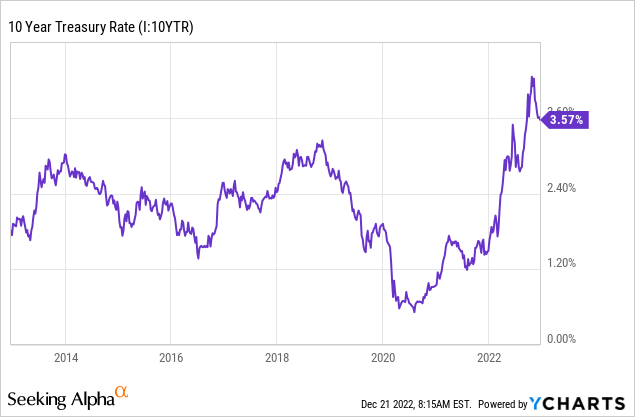

We know that yields were rising, but more recently, they had cooled off despite the Fed’s expectations for no cut in 2023.

Ycharts

On the other hand, we have some market participants who believe that a cut could be coming anyway, despite the tough talk from the Fed. That would only send yields lower.

At the very least, I would anticipate that interest rates don’t increase as much as we saw in 2022. Most of the interest rate increases we have are already in. That’s evidenced by the Fed only hiking by 50 basis points from the 75 basis point hike streak they were on. 25 basis point hikes could be next until an actual pause or even pivot.

Again, the main point here is that slowing or moderating interest rate hikes can mean that REITs can also stabilize their prices. If rates come down, that could be even better news for REITs, as cheaper financing would again be on the table for growth going forward. As well as their yields becoming attractive again.

For yields, I think the biggest appeal for REITs is that they are likely to continue growing at some pace, which means they have a good chance of still growing their dividends going forward.

This is all my general take on the REIT space going forward, but I also want to highlight two REITs that could be worth considering at this time.

STAG Industrial, Inc. (STAG)

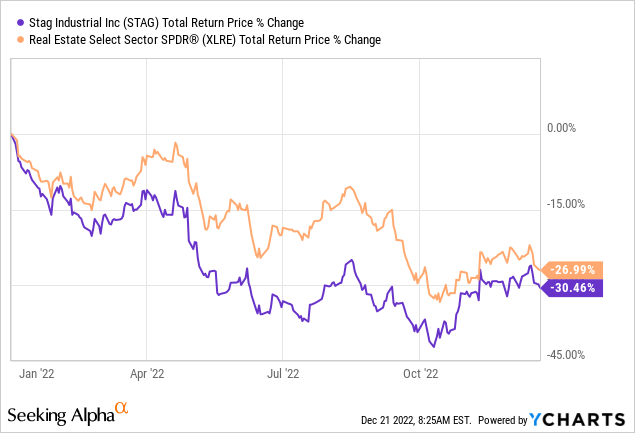

STAG is a name that I’ve written about several times, and it is a name where I continue to reinvest dividends. I’ve even sold puts that ultimately expired worthless recently. Overall, it’s a position that I wouldn’t mind adding to at this level because I believe it is undervalued. STAG was down significantly further than Real Estate Select Sector SPDR ETF (XLRE) at one point.

It is still underperforming the exchange-traded fund (“ETF”), although they’ve clawed back some of the losses while XLRE had dropped towards it. XLRE represents a basket of REITs, so it’s a good barometer to employ against REITs.

Ycharts

Just because a share price falls doesn’t mean it’s cheap, though. For that, we can look at a few other metrics.

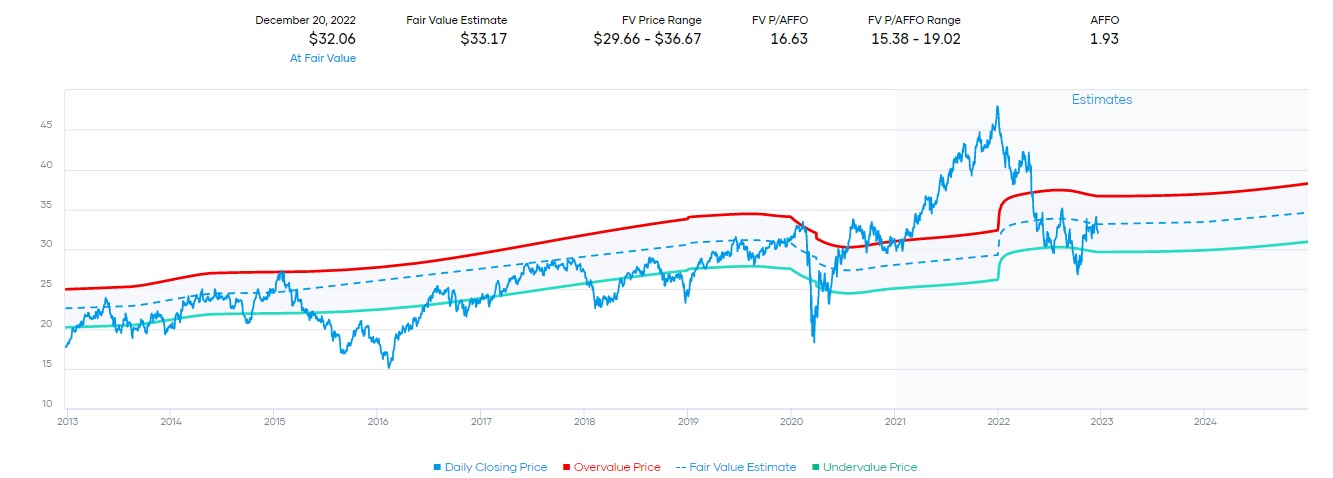

One metric we can use is the NAV of the REIT. According to Simon Bowler’s latest “The State of The REITs,” the consensus NAV is reported at $37.53. At the time of writing, STAG closed at $32.06, which would work out to a discount of around 14.6%.

Another metric we can take a look at is the P/AFFO range the REIT had traded at historically. In that case, we can see that it was more overvalued at one point before coming crashing down. It has recovered a bit, but is still a bit below what could be considered its fair value.

STAG Fair Value Estimate (Portfolio Insight)

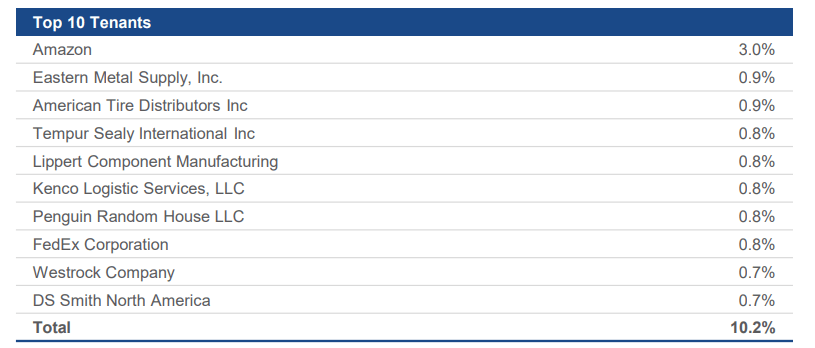

One of the reasons that STAG blasted off higher was the positive impact of Amazon.com, Inc. (AMZN) during the pandemic. That optimism is coming back down, which is one of the reasons why STAG is getting hit so hard in the first place.

AMZN is an important tenant, as it’s their largest by quite a significant margin. However, they are also fairly diversified, too, with no overreliance on any one tenant that could make or break them.

STAG Top Ten Tenants (STAG Industrial)

One of the biggest negatives I hear about STAG is their dividend growth or lack of meaningful dividend growth. This has been addressed but is always worth addressing again. Ultimately, they were getting their payout back into their target range of 80%.

They noted earlier this year that they are now there. Therefore, growth going forward should be better, at least according to the CFO when he made this remark in the Q1 2022 earnings call.

So, our first quarter payout ratio is 80%. We communicated a couple of years ago that we wanted to bring that payout ratio to the 80% level. We would like to be there for this year.

We will continue to evaluate it, but we are getting close to the point where we think that we can begin growing the dividend distribution in line with our CAD per share growth. It may not be this year, but we are getting close to the moderation level that we had communicated.

That higher growth could be seen in early 2023. Historically, they’ve announced the hike in January mid-month for prior years.

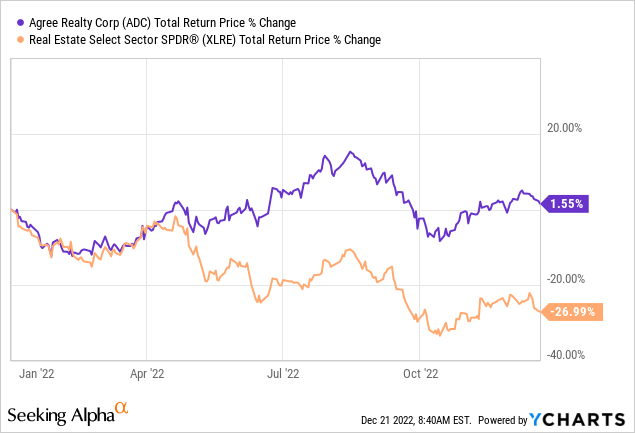

Agree Realty Corporation (ADC)

ADC is another attractive name in the REIT space. Albeit not one that has underperformed this year but outperformed the broader REIT space by a large margin. As mentioned above, just because a stock falls doesn’t make it cheap. Well, just because a stock outperforms significantly or even rises, it also doesn’t make it expensive.

Ycharts

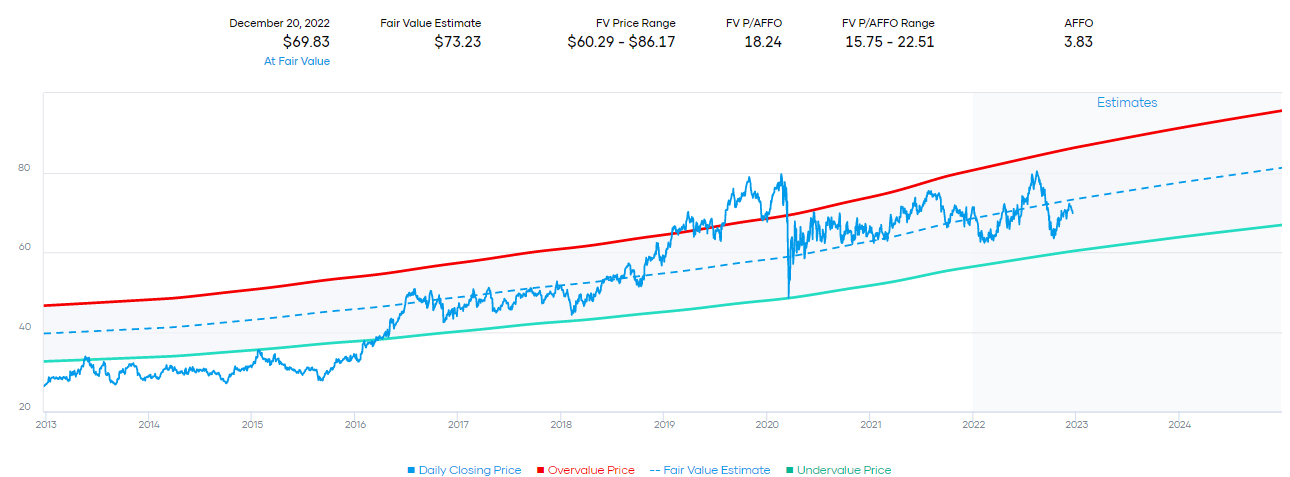

In this case, ADC is trading well above its consensus NAV of $59.67, as shown in Simon Bowler’s article. That would mean the current share price of $69.83 means the REIT is trading at around a 17% premium. That’s certainly not that appealing on the surface. Although, that’s not the sole metric we rely on.

On the other hand, ADC is trading in the lower half of its estimated fair value range based on the historical P/AFFO.

ADC Fair Value Estimate (Portfolio Insight)

It is a bit faster-growing REIT in its retail REIT subsector, which often means it can trade at a higher P/AFFO. For example, Realty Income Corporation (O) trades in a more narrow P/AFFO range, and the upper end is 20.28. We see the upper end of the P/AFFO range for ADC at 22.51. This also would indicate that ADC is more volatile, but that can be expected as O is a much larger, more mature retail REIT. I have little doubt that ADC can achieve the same status in the years to come.

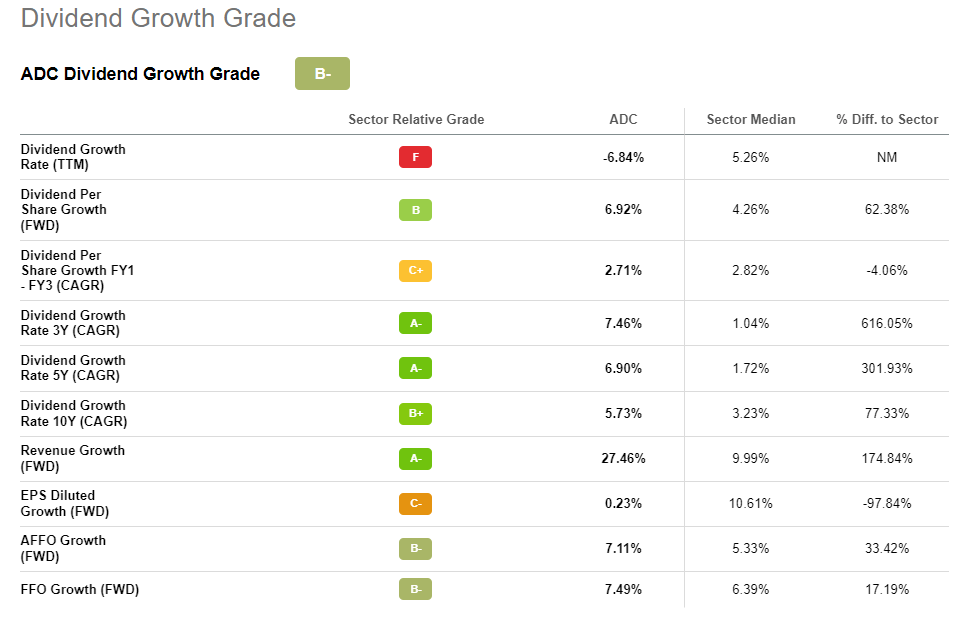

This relatively faster growth has meant it has been able to grow its dividend at an attractive clip too. The dividend growth has topped the sector median in the last 3, 5 and 10-year periods.

ADC Dividend Growth Scores (Seeking Alpha)

Agree Realty Corporation 4.25% Preferred (ADC.PA)

As a bit of a bonus for consideration to some REIT exposure, this was a position I picked up relatively recently. Though this isn’t a position that can benefit from any dividend increases, it could potentially benefit from some appreciation.

As interest rates were rising, fixed-rate preferreds got hit hard. That’s particularly true for ADC.PA because it is a perpetual preferred.

ADC.PA Price Decline (Seeking Alpha)

If rates fall back down, that means there could be some upside. If rates flatten out, that could also mean less downside, at the very least. Additionally, with the face value of $25, if it were ever redeemed, that could be a potentially significant upside. It becomes callable after 2026.

Considering the dividend yield of 4.25%, it may never be called, as ADC is unlikely to get significantly better rates to replace this. It was dirt-cheap financing that they could get in 2021 when rates were 0%.

While being called isn’t likely, thanks to the big drop in price, I was able to pick up some of the preferred at $15.75. That ultimately meant that I locked in an investment-grade preferred at ~6.75% for potentially ever. Even while the price has come back up since the initial purchase, it is still a rather attractive consideration. Based on the $1.064 annual dividend, it works out to around a 6.3% yield.

Conclusion

Buying things while they are down is hard. It is especially hard when there is nothing but seemingly endless doom-and-gloom pessimism everywhere. On the other hand, if you are brave enough to put capital to work, this is where some money can be made. There are certainly headwinds currently to consider. No investment is without risks. So this isn’t to say that you’ll be rewarded next month or even a year from now. It could take a couple of years before reaping the ultimate benefits. I try to invest in things I believe are cheap and hold for years.

Be the first to comment