LeoPatrizi

Co-produced by Austin Rogers for High Yield Investor.

Whether or not it actually accomplishes its stated purpose of lowering inflation, the recently passed “Inflation Reduction Act” will almost certainly have the effect of increasing the rollout of renewable energy assets across the country.

For example, the Solar Energy Industries Association estimates that the IRA will result in the installation of 69% more solar panels than would have occurred in lieu of the legislation.

SEIA & Wood Mackenzie

In 2032, a decade from now, the SEIA estimates that the U.S. will have 5x as much installed solar PV capacity as it does today.

Now, the SEIA is an explicitly pro-solar organization, so one should take their estimates with a grain of salt. In any case, though, the IRA’s substantial and long-lasting tax credits for renewable energy assets will surely have positive effects on the deployment of such renewables.

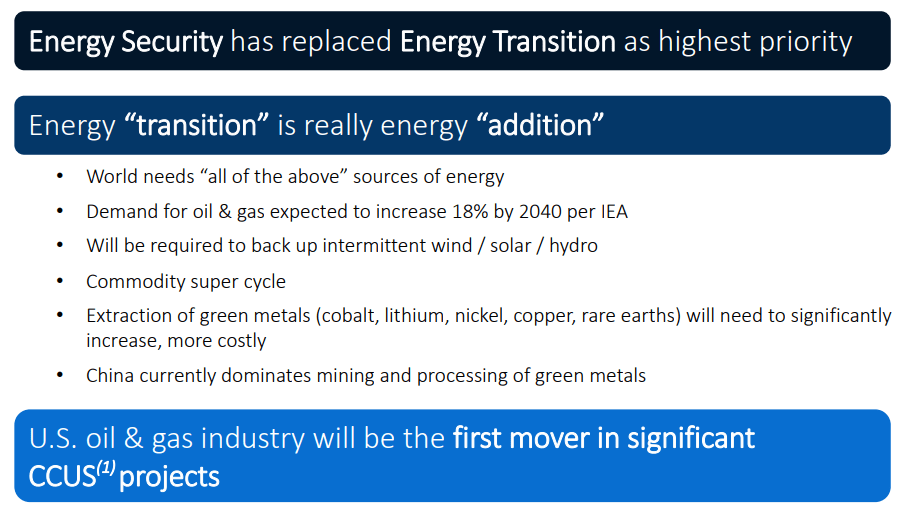

At the same time, the shortage of power sources around the world does not bode well for a global energy transition, because that implies traditional power sources will be taken away as green power sources take their place. With a growing population and expanding energy consumption, renewables are more likely to be additions to the energy landscape rather than replacements for carbon-emitting power sources.

EPD November 2022 Presentation

Perhaps usage of fossil fuels will gradually decline in some developed countries, but it is likely to continue increasing on a global basis as developing countries continue to consume increasing amounts of them.

Thus, from an investment perspective, we do not believe one needs to take sides in the “renewables vs. fossil fuels” debate. It is not an “either/or” proposition but rather a “both/and” one.

That said, even though demand for all kinds of energy sources will continue to grow, that doesn’t mean every player in the energy production industry will succeed. Instead, in two of our favorite sectors (renewable power producers and midstream oil & gas), we think it’s prudent to stick with the established industry leaders.

With that in mind, below we will highlight two of the largest and strongest players in their respective spaces. Both of these industry leaders feature best-in-class balance sheets with BBB+ credit ratings and $3 billion+ in liquidity, and both of them enjoy top-tier management teams with strong records of shareholder-friendly capital allocation.

We start first with the leader in renewable power production.

Brookfield Renewable (BEP, BEPC)

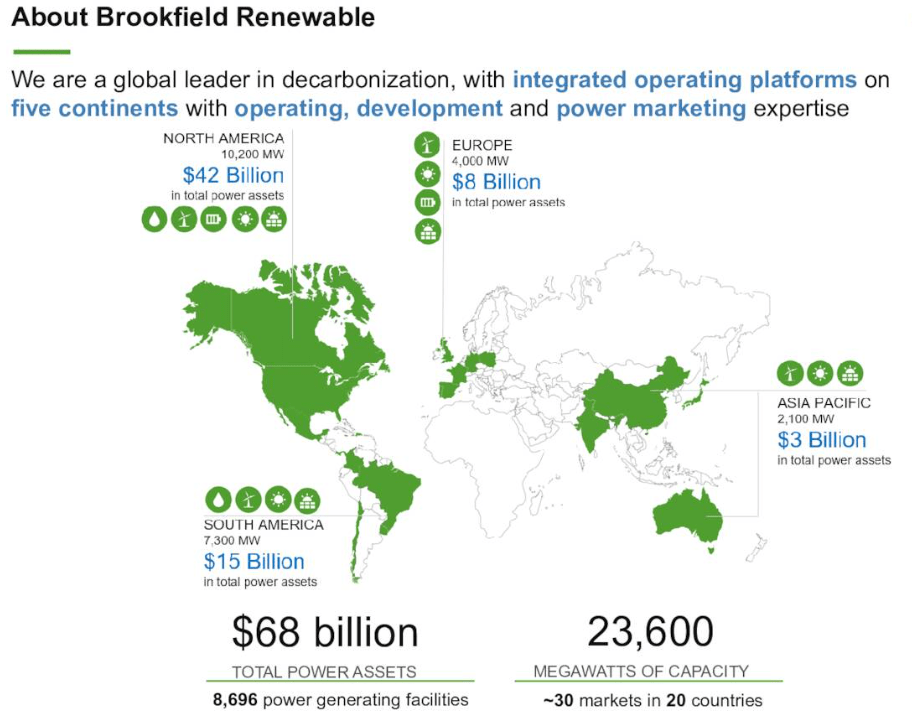

Brookfield Renewable Partners L.P. is the industry leader in publicly traded producers of electricity from renewables and other low-carbon power sources. In addition to utility-scale wind and solar projects and dozens of hydroelectric dams across the world, BEP is also an active investor in more cutting-edge technologies like hydrogen fuels and carbon capture.

BEP Q3 2022 Presentation

As the industry leader in this space, BEP is often the go-to provider of green electricity for utilities, corporations, universities, and government agencies around the world. Here’s how BEP’s customers break down by type:

- Power authorities (government utilities): 44%

- Distribution companies (private utilities): 21%

- Commercial & industrial users: 20%

- Brookfield: 15%.

BEP’s industry-leading status is a big reason why BEP’s development pipeline of future projects currently sits at 102 gigawatts, more than 4x larger than its operational portfolio of 23.6 GW.

Around half of BEP’s energy production comes from hydroelectric dams, which act as a complementary diversifier for the growing portfolio of wind, solar, and battery storage assets.

At the same time, BEP’s strong cost of capital and partnership with Brookfield Asset Management (BAM) allows the company to expand its low-carbon portfolio at a rapid pace. This portfolio expansion translates into profit (measured by funds from operations or “FFO”) growth. In the third quarter, BEP delivered 15% growth in both FFO per share and normalized FFO per share.

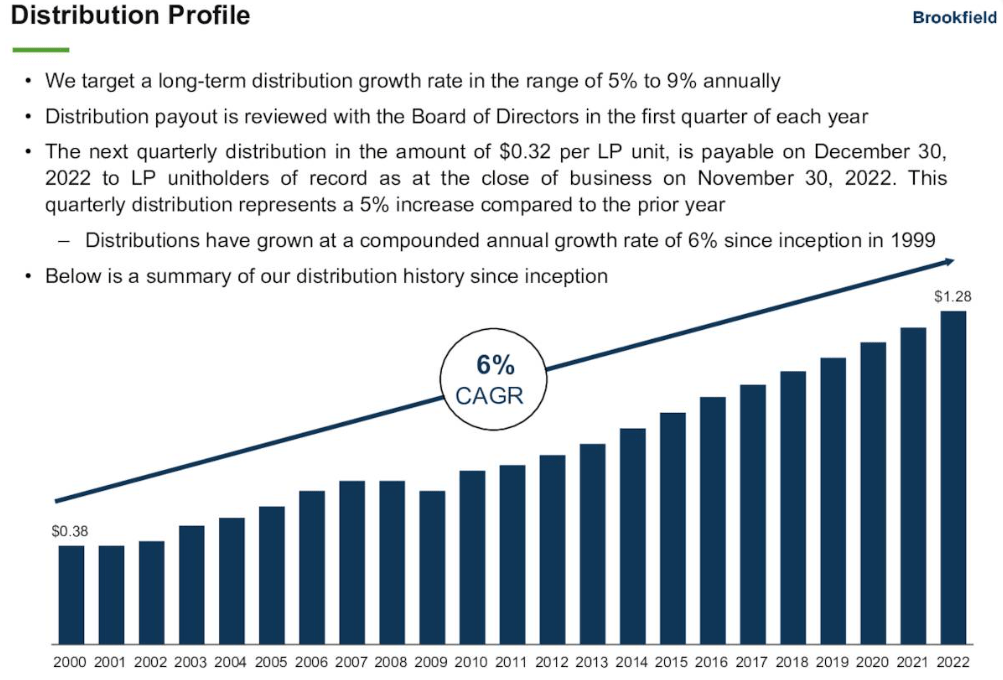

Historically, the company has grown FFO per share at a pace of around 10% per year while growing its distribution at a rate of 6% annually.

BEP Q3 2022 Presentation

Year to date, BEP has had a payout ratio of 79% based on FFO, 70% based on normalized FFO, and 93% based on cash available for distribution (“CAFD”).

While CAFD comes closest to a true free cash flow metric, it isn’t perfect. For instance, it includes amortization of wind and solar assets. These assets will eventually wear out and require replacement, of course, but the amortization of this eventual cost is a non-cash charge that reduces CAFD and therefore pushes up the CAFD payout ratio. Amortization of wind and solar assets amounted to about 16% of FFO in the first nine months of 2022.

Perhaps the most impressive feature of BEP is its BBB+ rated balance sheet.

Debt to total capitalization is relatively low at 38%, and 97% of debt features fixed interest rates. Meanwhile, 92% of this debt is in the form of non-recourse, project-level loans. These loans are similar in many ways to a real estate mortgage wherein recourse in the case of a default is remission of ownership to the lender and nothing more.

The average term to maturity of BEP’s debt (both non-recourse and unsecured, corporate loans) sits at 12 years. The average interest rate on non-recourse debt is 5.1%, which is up from 4.2% at the end of 2021. Rising interest rates are the primary headwind for BEP right now, but the relatively long duration to maturity of most of its debt greatly helps to mitigate this headwind.

BEP also enjoys strong liquidity of $3.5 billion, including $665 million in cash and liquid investments. This offers plenty of dry powder with which to continue funding acquisitions as well as its massive development pipeline.

Down nearly 20% YTD and trading at a price to normalized FFO of around 16x as well as a dividend yield of 4.7%, BEP is a great company (indeed, an industry leader) trading at a reasonable price.

Enterprise Products Partners L.P. (EPD)

EPD is one of the largest and strongest midstream energy infrastructure owners in the United States. The master limited partnership (yes, it produces a K-1 form for tax accounting) is particularly focused on natural gas and natural gas liquids (“NGLs”), which are critical inputs for a number of uses and products such as plastics.

EPD has an extensive network of pipelines stretching across the country as well as a wide variety of storage, processing, and exportation facilities along the Gulf Coast.

EPD November 2022 Presentation

Many of the most successful, long-term-oriented companies in the world are family businesses, and many others have significant alignments of interests through high insider ownership. EPD enjoys both, and this plays no small part in the company’s impressive total returns over time.

Roughly 1/3rd of the company’s units outstanding are owned by management and board members. And the Chair of the Board, Randa Duncan, is the daughter of the company’s founder, Dan Duncan.

EPD has an excellent history of capital allocation, both in terms of shareholder returns and investment decisions made by management.

Evidence of this is EPD’s average return on invested capital (“ROIC”) of 12% over the last decade. ROIC has dropped to as “low” as 10% in 2016 and risen to as high as 13% in several years, including 2022 year-to-date. This high and consistent ROIC metric demonstrates both quality and consistency in management’s investments over long periods of time.

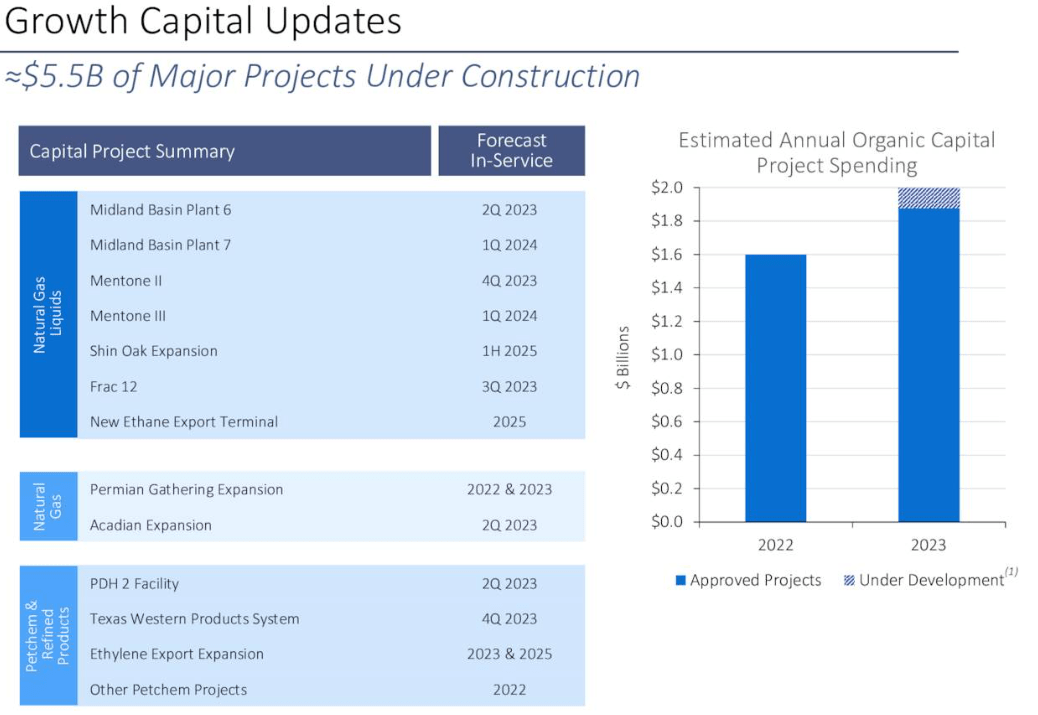

Speaking of investments, EPD still has plenty of opportunities to put money to work in building pipelines or other midstream infrastructure assets. In total, EPD estimates $3.6 billion in growth capital spending in 2022 and 2023, with a little more of that coming in 2023 than in 2022.

EPD Q3 2022 Presentation

As you can see above, EPD has several projects expected to come into service next year. In light of the productivity in the Midland and Permian basins, where EPD has a strong presence, these projects are likely to maintain the company’s excellent ROIC track record.

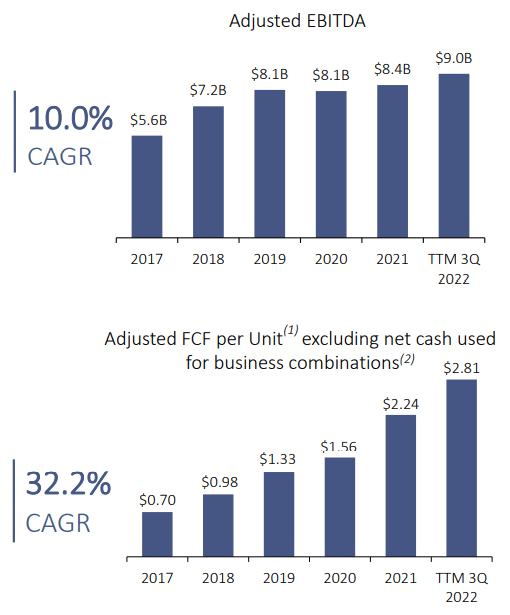

Over the last five years, EPD’s prudent capital allocation has generated strong results in the form of double-digit EBITDA and free cash flow growth:

EPD November 2022 Presentation

Meanwhile, the investment-grade balance sheet is as strong as ever, sporting a leverage ratio of 3.1x, which is under the company’s target of 3.25x to 3.5x.

And while BEP’s weighted average term to maturity of 12 years is impressive, EPD’s weighted average term to maturity of 19.7 years is even better. Though about $1.2 billion in debt is maturing in 2023, EPD has ample liquidity of around $3.5 billion to handle it if refinancing proves prohibitively expensive.

Moreover, EPD is virtually a gusher of cash. In Q3 alone, EPD generated $1.5 billion in adjusted FCF. This depth and consistency of cash flow creates lots of optionality concerning debt maturities.

It also provides substantial protection to EPD’s 7.7%-yielding dividend. The MLP has low payout ratio of 56% based on cash flow from operations and 70% based on free cash flow. This allows EPD to self-fund most if not all of its growth projects while leaving some cash available to buy back units.

The recent dividend hike represents 5.6% YoY growth and marks 24 years of consecutive distribution per share growth. Over the last 24 years, EPD has grown its DPS at a CAGR of 7%. Though dividend growth slowed in recent years, dividend raises of 3-5% per year on top of a 7.7% yield makes for an extremely attractive income investment opportunity.

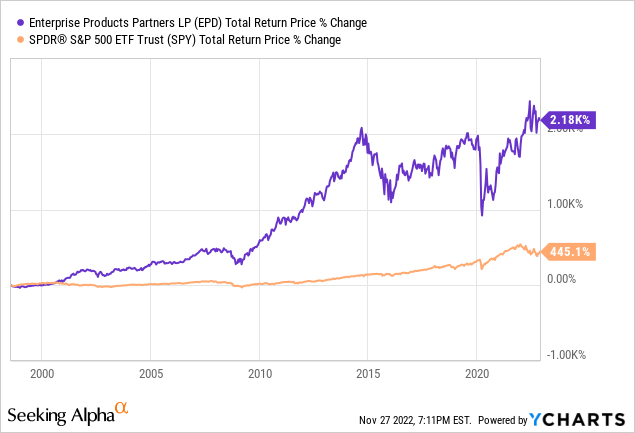

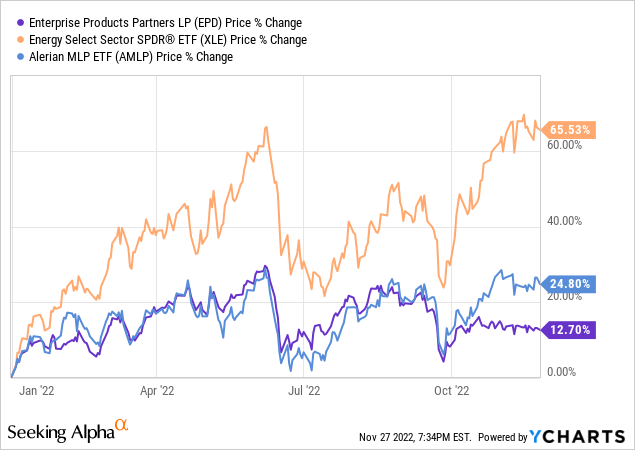

Remarkably, despite EPD’s blue-chip and industry-leading status, EPD has underperformed both the broader energy sector (XLE) and midstream oil & gas MLPs (AMLP) so far this year:

This strikes us as a great opportunity to buy this high-yielding, industry-leading midstream energy giant.

Bottom Line

Regardless of politics, we believe the world will need to take an “all of the above” approach to energy in order to meet the consumption demands of the future. While renewable energy production will grow rapidly from here, renewables lack the capacity to provide for both the growth in energy demand and the entire current level of demand.

At High Yield Investor, we see great, high-yielding, dividend-growing investment opportunities in both spaces. And today, investors have the opportunity to pick up shares in industry leaders in each field – BEP in the area of renewables and EPD in the area of midstream oil & gas.

Be the first to comment