Drew Angerer/Getty Images News

Warren Buffett once gave the only three ways that a smart person can go broke, stating:

There’s only three ways that a smart person can go broke…liquor, ladies, and leverage.

While the financial risks associated with the first two “L’s” provided by Mr. Buffett are beyond the scope of Seeking Alpha articles, we will dive into the third “L” in this article to discuss why we don’t buy most Closed-End Funds (i.e., CEFs).

The Dangers Of Leverage

First of all, let’s discuss what Mr. Buffett meant when he said that “leverage” was so dangerous to a smart person. For context, let’s look at some of his other quotes on the subject:

You really don’t need leverage in this world much. If you’re smart, you’re going to make a lot of money without borrowing

Here Warren Buffett is stating the basic principle that you do not need to use debt to get rich if you are intelligent. All debt does is increase your risk, while if you are a smart person, you are going to make a lot of money either way.

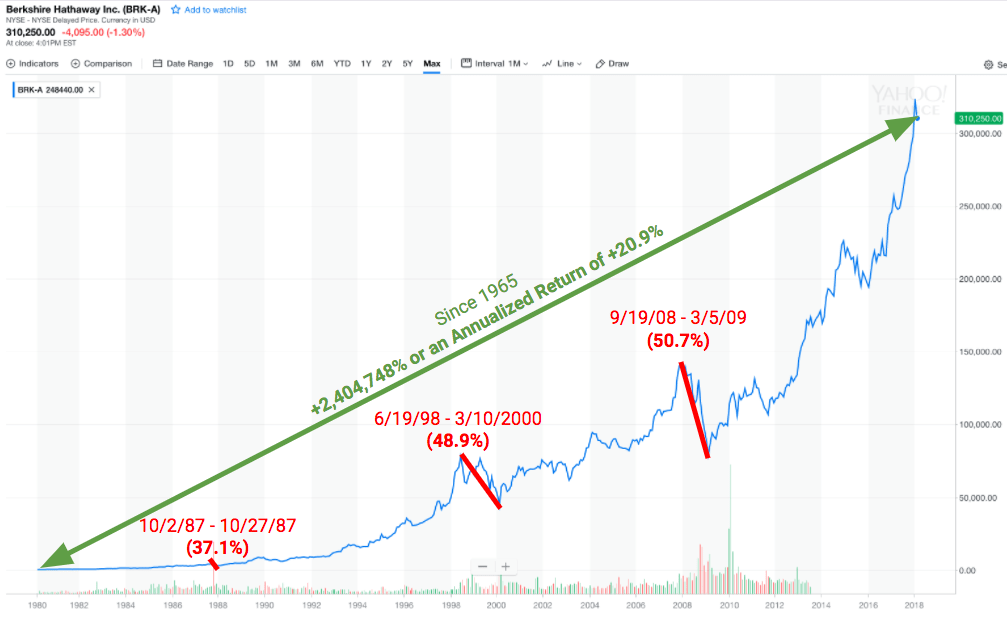

As a clear example, if you were smart enough to invest in Berkshire Hathaway stock (BRK.A)(BRK.B) decades ago and hold for the long-term, you would have made a lot of money without having to borrow any money as – since 1965 – the stock has average 20% annualized total returns. Even just investing in it over the past decade would have increased your wealth by nearly 4.5x.

At the same time, however, Mr. Buffett has credited much of his success to the float generated by his insurance businesses at Berkshire which is a sort of free leverage. Additionally, his company and/or subsidiaries have also taken out long-term debt. Is he talking out both sides of his mouth here, or is there more to what he is getting at?

First and foremost, the general principle that he is addressing is that it is very important to avoid the risk of bankruptcy, so even if you do use a little leverage here and there, make sure it is used very prudently with permanent downside risks carefully mitigated. He does this at Berkshire by keeping a cash hoard of tens of billions of dollars to ensure that Berkshire can always meet its insurance and other obligations.

Additionally, his 2019 letter to Berkshire shareholders contains an even more specific answer about the worst kind of debt for stock market investors to have: margin debt. In his letter he stated:

[When it comes to margin debt,] even if your borrowings are small and your positions aren’t immediately threatened by the plunging market, your mind may well become rattled by scary headlines and breathless commentary. And an unsettled mind will not make good decisions.

This is because when you take on margin debt, your stock holdings are used as collateral. That means that when stocks decline and you are holding a lot of margin debt, your risk of a margin call dramatically increases. At a bare minimum, this means that you will not be able to take advantage of the sell-off and buy the dip. However, in a true market crash, this will often mean that you will be forced to sell at a steep loss and possibly even get entirely wiped out.

To bring the earlier example full circle of how much wealth simply buying and holding BRK.A/BRK.B stock without using any debt has brought investors, we can look at what would have happened if investors had bought that stock using margin.

Over the course of its illustrious history under Warren Buffett, Berkshire stock has seen its stock plunge five separate times:

- down 59% in 1973-1975

- down 37% in 1987

- down 49% in 1998-2000

- down 51% in 2008-2009

- down 26% in 2020

If you had heavily leveraged your Berkshire shares during any of those periods, you would have at a minimum been forced to face a margin call and in the more severe downturns, you would likely have been forced to sell many of your shares at a loss or even gotten completely wiped out.

Berkshire Sell-Offs (The 3 L’s: Liquor, ladies and leverage (medium.com))

As he went on to write:

There is simply no telling how far stocks can fall in a short period…For the last 53 years, the company has built value by reinvesting its earnings and letting compound interest work its magic…The light at any time can go from green to red without pausing at yellow,” he observed.

By using margin leverage, investors run the risk of interrupting the power of compounding and setting themselves back so far that it might be impossible to ever catch up to the broad market indexes like the S&P 500 (SPY), Dow Jones Industrial Average (DIA), or Nasdaq (QQQ), much less a fantastic long-term compounder like BRK.A/BRK.B.

Why We Don’t Buy CEFs

The natural extension of this lesson is that we always look to avoid using margin leverage whenever we invest, regardless of how attractive it looks. One of the areas where we see this most often is in the CEF space.

One of the big allures of CEFs is that they typically offer similar diversification to what is commonly found in ETFs and mutual funds, except that they often trade at substantial discounts and premiums to their net asset values. This means that actively managed portfolios can trade in and out of CEFs to arbitrage these discounts and premiums.

In so doing, they can theoretically achieve superior risk-reward by enjoying the same risk mitigation afforded ETFs and mutual funds via diversification while achieving greater reward potential by purchasing at discounts to NAV and selling once that discount is narrowed or even turns into a premium to NAV.

Furthermore, CEFs often boast very attractive dividend/distribution yields – sometimes far better than what is typically offered by ETFs and mutual funds – so retirees find them to be rewarding income investments as well. However, while we acknowledge that some CEFs have done quite well over lengthy periods of time and have provided a lucrative combination of income and total returns to investors, many times investors overlook a key risk to holding these funds: they often employ a lot of margin leverage.

If you go on popular CEF screening website CEF Connect right now, you will see that many funds that offer very attractive distribution yields – many of whom even trade at large discounts – also carry massive amounts of margin leverage. Here is what I see, doing a basic search without any filters:

| Ticker | EFFECTIVELEVERAGE % | DISTRIBUTIONRATE | DISTRIBUTIONFREQUENCY | DISCOUNT /PREMIUM |

|---|---|---|---|---|

| GLQ | 44.37% | 11.87% | Monthly | 1.38% |

| CPZ | 44.01% | 8.40% | Monthly | -7.80% |

| GLU | 36.53% | 6.18% | Monthly | -3.00% |

| GGT | 33.03% | 9.54% | Quarterly | 25.10% |

| 32.36% | 4.53% | Quarterly | -13.80% | |

| 30.81% | 9.37% | Quarterly | 1.29% | |

| 30.04% | 7.79% | Monthly | -9.83% | |

| BANX | 28.42% | 7.17% | Quarterly | 1.83% |

| JRS | 28.12% | 7.04% | Quarterly | -6.75% |

| SZC | 27.94% | 5.75% | Monthly | -20.44% |

| MGU | 27.83% | 4.75% | Monthly | -17.05% |

| GUT | 27.11% | 8.31% | Monthly | 69.09% |

| EMO | 26.37% | 7.17% | Quarterly | -20.95% |

| SRV | 26.33% | 5.17% | Monthly | -19.49% |

| MFD | 26.20% | 8.04% | Quarterly | -9.22% |

| UTF | 25.94% | 6.52% | Monthly | -0.12% |

| SMM | 24.86% | 4.29% | Quarterly | -14.84% |

| RNP | 24.67% | 6.20% | Monthly | -3.48% |

| KMF | 24.19% | 6.70% | Quarterly | -20.83% |

| GRX | 24.03% | 4.68% | Quarterly | -12.98% |

| KYN | 23.64% | 7.68% | Quarterly | -15.87% |

| DNP | 23.59% | 6.57% | Monthly | 14.24% |

| CTR | 23.14% | 7.17% | Quarterly | -21.47% |

| FDEU | 23.06% | 5.68% | Monthly | -13.68% |

| RQI | 22.53% | 5.68% | Monthly | -1.86% |

| NRO | 22.37% | 7.61% | Monthly | -3.91% |

| GAB | 22.29% | 8.49% | Quarterly | 15.71% |

| IGR | 22.10% | 7.89% | Monthly | -5.78% |

| TYG | 21.41% | 8.36% | Quarterly | -18.42% |

| FEN | 19.50% | 7.46% | Quarterly | 0.12% |

| UTG | 19.42% | 6.67% | Monthly | -1.33% |

| GNT | 19.11% | 6.41% | Monthly | -13.94% |

| FEI | 18.94% | 7.33% | Monthly | -13.53% |

| NTG | 18.85% | 8.22% | Quarterly | -18.51% |

| TTP | 18.82% | 8.16% | Quarterly | -17.51% |

| ETG | 18.62% | 7.55% | Monthly | -2.55% |

| THQ | 18.41% | 6.03% | Monthly | -7.22% |

| FPL | 18.33% | 7.15% | Monthly | -13.60% |

| HIE | 17.91% | 5.15% | Monthly | -9.61% |

| CEN | 17.80% | 5.24% | Quarterly | -15.08% |

| THW | 17.68% | 9.23% | Monthly | 1.40% |

| FIF | 17.62% | 4.95% | Monthly | -14.02% |

| OTCPK:FXBY | 17.41% | 12.99% | Annually | -32.04% |

While most of these CEFs would immediately catch my eye for their huge distribution yields and substantial discounts to NAV, they all have substantial amounts of margin leverage. For example, UTF – a popular Infrastructure fund managed by highly respected Cohen & Steers – currently employs 36% effective leverage. While it pays out a hefty 6.5% monthly distribution and even trades at a slight discount to NAV, its margin debt is potentially a fatal weakness here.

For example, if China were to invade Taiwan tomorrow and the underlying holdings were to crash by a third, the NAV per share in UTF would decline by a whopping 45%, potentially igniting a margin call on the company and forcing it to sell some holdings at a permanent loss. As a result, you as a shareholder would not only suffer immense downside that might rattle you into selling near the bottom (or at least losing some valuable sleep), but would also miss out on some of the potential post-crash recovery since some of your principal was permanently destroyed when shares were sold at the bottom. On top of that, you would almost assuredly face a distribution cut.

This actually happened to the Nuveen Energy MLP Total Return CEF (JMF), which famously had to shut down because it crashed so hard during the market sell-off in 2020. That stock offered a very attractive distribution that was even covered by cash flows and held blue-chip MLPs like Enterprise Products Partners (EPD), MLPX (MLPX), Magellan Midstream Partners (MMP), and Energy Transfer (ET) in high concentration. However, because it held ~30% in margin debt at the time, it suffered an epic crash from which it was unable to recover.

For this reason – as well as the facts that they tend to charge hefty management fees and diversify so broadly to the point of di-worsification – we do not invest in CEFs.

Investor Takeaway

Mr. Buffett’s wisdom on avoiding the perils of margin debt sounds so simple, yet it can be very difficult to follow when starting at juicy distribution yields selling at a discount to NAV.

We ourselves fell into this trap by buying JMF prior to the stock market crash of early 2020 that sunk that investment and turned it into our biggest investing failure of all time.

Today, instead of chasing heavily margined CEF yields, we simply invest in the individual stocks themselves. By building a portfolio of 25-30 high conviction names that include the likes of blue chips EPD and W.P. Carey (WPC) alongside some lesser-known high yield picks like Triton International (TRTN) and FirstEnergy (FE), we have been able to more than double the SPY’s performance since inception of our portfolio while also generating a safe and growing 5%-6% weighted average dividend yield.

We have found that when it comes to investing – as usual – Mr. Buffett knows best. If we patiently invest intelligently in dividend stocks on a value basis, the magic of compounding works quite well for us. Why risk losing it all with margin leverage?

Be the first to comment