Hammad Khan

The Direxion Daily MSCI Brazil Bull 2X Shares (NYSEARCA:BRZU) is a bet on Brazil that gives you some daily leverage on the changes in the underlying index which tracks some of Brazil’s largest shares. While the underlying index has some positives, specific risks to Petrobras (PBR) from political actors could be a headwind for BRZU. Moreover, there are structural risks in the Brazilian market that could cause issues for the whole equity asset class also due to political risks, in particular the new Lula administration. Overall, with leverage being inherent to the BRZU pick and expense ratios being high on account of that, there’s no point of taking a bet that is unlikely to work in the short term. We think the political developments need to be waited out and for the Lula political timbre to be better understood.

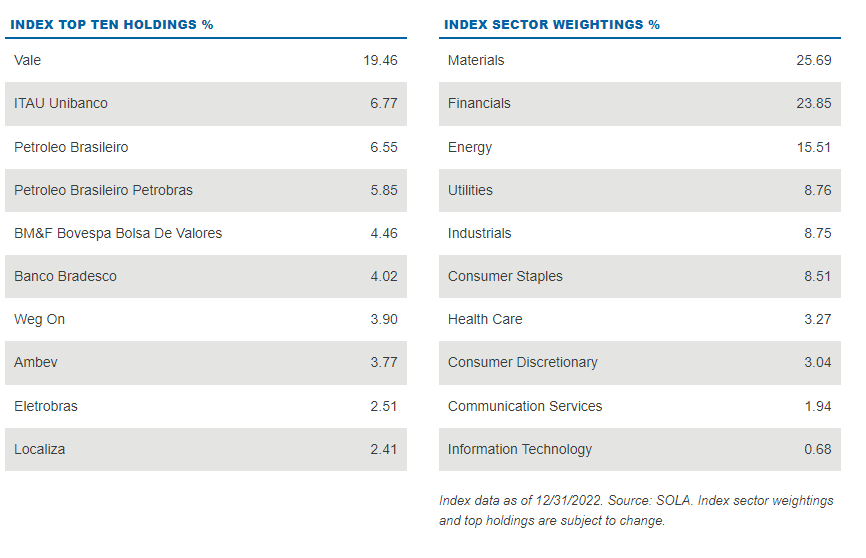

Looking at the BRZU

As said, BRZU tracks its underlying index with 2x leverage. Any daily change in the underlying index’ price, BRZU will replicate that change but with a 2x factor, whether negative or positive. This means you lose money faster, and also means it’s harder to gain it back even with 2x to the upside. So there is a decaying dynamic to the value. You really need to be a bull at the very right time for this to be a wise bet, especially with expense ratios at 1.26%.

The target index has the following as some of its exposures.

Top Holdings (direxion.com)

A lot of substantially government owned entities, and certainly a lot of exposure to Petrobras both through the preferreds and the common stock. There is also quite a lot of banking exposure. Petrobras and banking is not well positioned in the current environment, which already accounts for 35% of the portfolio.

Because of the government control of Petrobras, it can dictate their actions. With a leftist government that has specifically campaigned on getting Petrobras to CAPEX on renewable energy and innovation, it cannot be the cash printing entity that a lot of other E&P companies and full-service oil companies get to be. Moreover, there may be some direct taxes on Petrobras’ windfalls and general business under the Lula administration.

Banking, specifically retail banking and anything that’s levered positively to higher rates, is not in a good position either. Lula is pushing hard against the need to restrict the economy in order to avoid inflation, and even the originators of the current inflation rate targets, not so low at around 3%, are backtracking on that, possibly under political pressure. At any rate, Lula will want to skate on the growth that was prepped after the economy’s 2022 cool-off in order to make political strides and maintain support. Part of allowing inflation to be higher will mean bringing down rates. That will negatively affect banking and insurance business models.

Other Remarks

There are more general concerns too. The election results were protested by Bolsonaro supporters in a manner pretty similar to the apparently insurrectionist movement on January 6th in the US. In a country like Brazil, this is more of a concern. Thankfully, those events are concluded and are no longer a risk, but other threats to political institutions come from Lula. Despite only a recent legislative move to enshrine the independence of the central bank of Brazil in the law, Lula is already on the attack in order to wrangle institutions to support his politically motivated economic policy. This isn’t particularly insidious, but it was important to the financial community that Brazil’s bank was independent, and would not whipsaw on political outcomes, at least not obviously. Lula said in a recent TV interview that he questioned the need for CB autonomy, and with a packed, leftist cabinet of economists, this institution could be under attack.

The consequences were notable. The Real tanked following his remarks, and swap rates rose as questions around the economy suddenly intensified. In general, Brazil has been underperforming on financial markets since Lula won in October, both the currency and its equity market indices. Uncertainty around Brazilian market affects equities too, and therefore BRZU is not well positioned with respect to this political uncertainty.

In general, the markets were very optimistic when Bolsonaro was elected back in the day. It is to be expected that they could now be pessimistic as the government goes from conservative to leftist. BRZU is not the right play when political actors capable of affecting the economy and the financial markets in Brazil have less capitalist considerations.

Be the first to comment