hrui

Broadwind (NASDAQ:BWEN) used to be a somewhat fairly valued company with some risks that could lead it to bankruptcy; however, after the massive rally provoked by the new tower order they received worth $175 million extended itself for too long than is acceptable, Broadwind has become a highly risky investment worth either avoiding or shorting.

Recap

Broadwind announced a few days ago a massive wind tower order worth around $175 million. Ever since the announcement, Broadwind was on a relentless rise to highs not seen since the days of the meme stock mania. As of the weekly closing on January 13th, Broadwind stood at $5.60 with a slight post-market decline of 1 cent.

Current Chart of Broadwind (Yahoo! Finance)

While I must ask if the order is as “transformative” as the company says, I am afraid that off the bat I’ll skip on Broadwind after such a massive rally like this. The rally has exceeded analyst estimates and has gone beyond fundamentals and would likely remain unsustainable. Besides that, the case for now is that Broadwind will have to prove that the order is as transformational as they claim before I can consider this company a buy.

Company Description

Broadwind manufactures various components needed to assemble certain structures. The most centric and likely known types of components to investors are the wind tower components, such as the ones needed to fulfil the new order.

However, Broadwind seems to be more than just wind towers, according to their latest 10-K filing. They have three segments: Heavy Fabrications, Gearing and Industrial Solutions.

To put briefly, Heavy Fabrications consists of manufacturing large and complicated structures. Gearing manufactures gears and gearboxes for various purposes and Industrial Solutions provides various types of services such as supply chain solutions, inventory management, kitting and assembly services and such.

The main focus of this article will be their Heavy Fabrications segment; however, it may be possible that part of their financial results will be affected by the other two segments.

Tower Order Details

The full announcement explains that the full order will be completed by 2024. That means that the company expects to complete this order in two years, dividing the total value of the order by two, meaning that it should be reasonable to expect it to provide around $87.5 million in revenue. Considering the company’s current trailing twelve months (ttm) revenue of $162 million, and assuming that revenue before the announcement was to be expected, it’s reasonable to expect that revenue for 2023 could reach $250 million.

Sounds like attractive numbers, right? Well, I would be careful. The company has been showing inefficiency in making a profit, and so if Broadwind also fails to make a profit from this improved source of revenue, then the current market reaction might not last enough to justify buying the stock at this moment.

The order reflects the current strategy the company has, which is to increase the amount of money their current business partners spend on their orders organically. I also must note the next point, that the order would secure around 50% of their tower manufacturing capabilities in those two years.

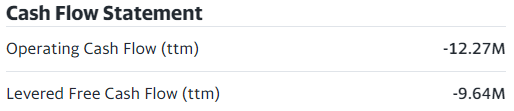

If the company desires to increase their wallet share of their current business partners, then they may need to start reorganizing their manufacturing capabilities and expenditures so that they at least make a profit, if not have positive Operating Cash Flow

Yahoo! Finance

Case in point, if they cannot generate cash, then in reality they won’t be able to expand very much. Considering that the tower order will use about half of their production capacities, this could limit how many new orders they can reasonably fill.

And apparently, the order will double their current backlog. While having a backlog may sound good, it might have some questionable implications. For one, the company could already be using its full capacity, or they don’t have enough capacity to meet their demand.

Finally, the order will be applicable for the Inflation Reduction Act (IRA), which means that the order will allow the company to receive certain tax credits, which help with their full profitability.

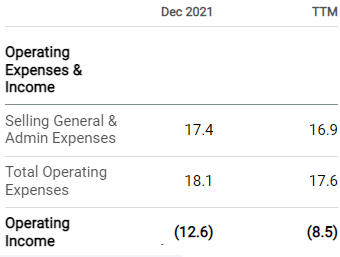

BWEN’s Operating Expenses and Margin (Seeking Alpha)

Except… they aren’t making a profit on the operating side…? Their EBITDA isn’t showing any better signs so I have to wonder what sort of improvement is the company talking about when it comes to margins, if all the “improvements” might as well either already exist or not have any effect, as looking at the income statement displayed here at Seeking Alpha already shows they have effectively paid zero taxes in the last four years.

I don’t know, but so far, the transaction is a massive “good for them” when it comes to raising hopes of being able to make it out alive, but when it comes to being transformational, it’s so far not living up to the hype, in my opinion. The only thing that is transformational about the order is the exceptionally large receipt, which should help their financials.

Balance Sheet

Looking at their latest 10-Q filing, specifically the balance sheet, we can see some things:

Broadwind’s Q3 2022 filing

There seems to be some improvement in their cash reserves compared to 2021, however Broadwind seems to be running on thin ice here. There is some comfort to be had in the company managing to survive an entire year on very little cash, however it does raise a red flag for me.

It also seems to show that they have slightly invested in more property and equipment, which is good, but it does need to translate into more capacity before it can be called a meaningful investment.

They also have plenty of inventory, which they can sell off in a pinch (if it’s not their products but rather the materials to make the products), however I wouldn’t count this in fully.

All in all, though, their total assets have increased, but I do find it risky that Broadwind is running on low cash like this when it struggles to make a profit, let alone bring cash in.

Broadwind’s Q3 2022 filing

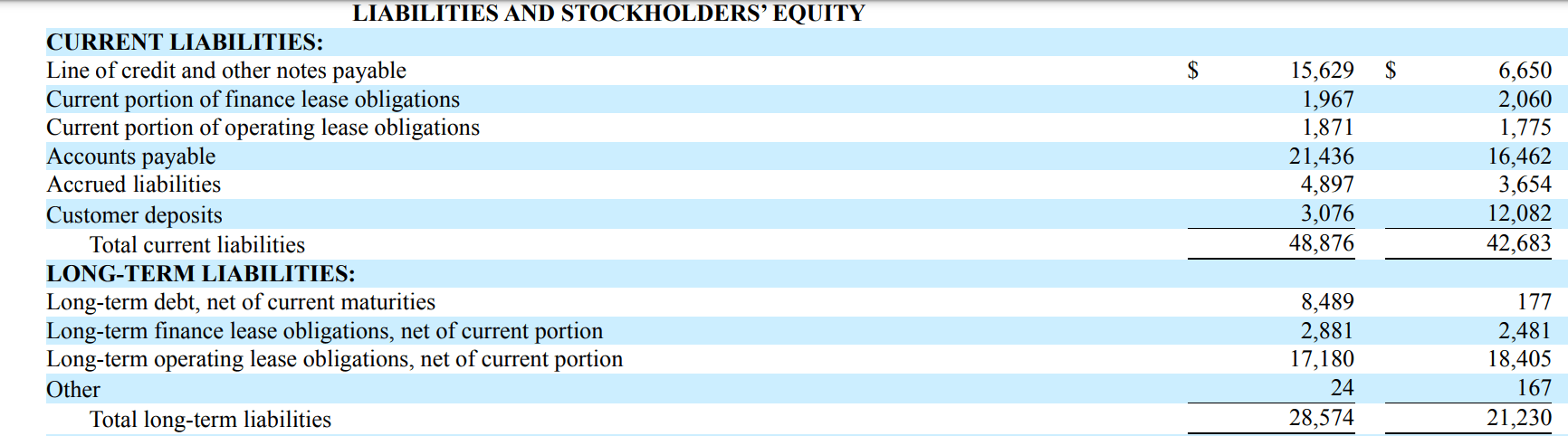

Now, looking at their liabilities page carefully, there’s something strange that can be seen. They have a lot of financial responsibilities pending on the short term that seem to be adding up. If we removed their customer deposits from liabilities entirely (as these simply are deposits for orders, which can be considered unearned revenue), their December 2021 current liabilities would amount to $30.6 million while their September 2022 liabilities would stand at $45.8 million.

This is not looking very good, especially as accounts payable and their line of credit and notes payable sections are the ones mostly driving up their current financial responsibilities. This would likely mean that they are incurring in more debt and purchasing on credit as they don’t have the cash on hand to pay their purchases immediately. While this expands the longevity of their cash reserves, it reinforces the idea that Broadwind is running on thin ice.

The news might as well then open the suspicion that they may be trying to keep their debtors and stockholders as calm as possible while they try their best to bring a profit. For the sake of the company, they better do it, because it seems they may need bankruptcy protection if things suddenly get much worse from here on.

What Caused the Rally?

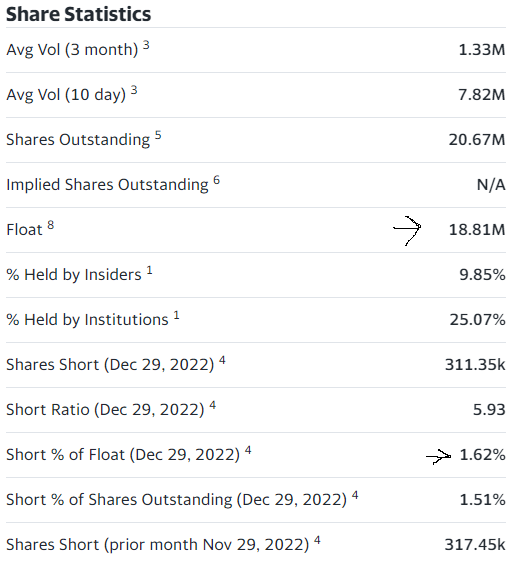

A quick look onto the short interest shows that the rally was not caused by a short squeeze

Share Statistics (Yahoo! Finance)

Before the rally, short interest was relatively low, and the chart showed relative strength in not breaking under $1.50, which has been a stiff resistance for a very long time. This in a psychological sense may tell us that people believe the stock would be unjustifiably undervalued at those levels, as there aren’t many signs that the company would go bankrupt yet.

However, looking into a more market-wide perspective, it seems that Broadwind, may have gapped higher from market makers repricing the stock to account for the improved revenue stream and potential profitability, however Broadwind may have become a target for meme stock traders as has been happening lately in other names such as Bed Bath and Beyond (NASDAQ: BBBY), AMC Entertainment (NYSE: AMC), GameStop (NYSE: GME), Carvana (NYSE: CVNA) and the like.

The small float also allows for extremely high price swings to occur. While volume during the day of the announcement was exceptionally high at 66 million shares – over three times the company’s float – the total volume was still higher than normal during the days after, when volume was 4 million the second day after and 6 million the third day after. I also believe that as limit orders get processed and demand rises at unprecedented rates, the lack of pending sellers at these untouched levels also allows for the stock to easily rise if there’s an unusually high number of buyers, as market orders from eager investors will look for the next lowest possible offer. Market makers wouldn’t be able to cover this demand as the volume is not typical for Broadwind (or alternatively, may capitalize on the unprecedented volume depending on their programming). For reference, normal volume in Broadwind stock stands between 40,000 to 80,000 shares a day.

This also pushes forward the theory that the rally is no longer rooted in fundamentals and investing in Broadwind is now a gamble. If you like gambling, then you probably already know what you’re gonna do, but I honestly am in a decreasing mood for speculation and more for investing soundly.

I highly suggest making your due diligence as I cannot make financial advise and I am simply sharing my thoughts on the stock and the current business prospects. I’ll simply share what Seeking Alpha believes are the company’s peers to give you a starting point, however I don’t forecast I’ll provide coverage on these companies soon.

Sell/Short Thesis

The rally worth over 100% is not rooted in fundamentals anymore. It is currently highly risky to enter a long position as the stock may eventually decline back to more reasonable levels, whether it happens at whatever tomorrow is relevant to you, or in a month or two from writing, or even a year after writing. The only way a price this high can be sustained is through improvements in fundamental areas such as profits, cash flows, cash reserves, shareholder equity, industry outlook, macroeconomic outlook, etc.

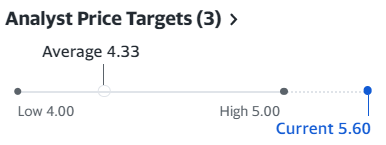

My current expectations are for the stock to return below $3 as it managed to sustain for long periods of time, regardless of more experienced voices placing these price targets for the stock:

Yahoo! Finance

The company has also failed in recent times to make a profit, despite consistent revenues. Their cash flows are also looking problematic as this would represent a potential bankruptcy if cash burn increases pacing due to deteriorating macroenvironment or industry conditions.

Their financial obligations also seem to be catching up to them at a dangerous pace. The increase of accounts payable and payable lines of credit or notes may also imply that the company has been buying on credit more often due to their current inability to buy using their cash reserves, which may be rather dangerous. I should also note that this is the definition of a zombie company.

Fair Valuation

I believe that $2 was and is still the fair valuation this company can have given current conditions. I can lay out certain expectations which were already mentioned here in the article:

- Future revenue between $200 – $250 million

- Reasonably expectable earnings of $10 million

- Maintain shareholder equity of $40 million

I could mention future growth over 5, 10 or even 20 years to justify ridiculous valuations, but I don’t believe the company can consistently grow in the current revenue model as it is an “on demand” B2B business that depends on the company receiving tower orders. The fortunate thing is that the company can manipulate the pace of tower order completion to allow for more consistent revenue, however they also have the challenge of making sure they complete their orders in a timely fashion. Because the tower order is expected to be completed in 2024, it is safe to expect annual revenue at a minimum of $87.5 million. Assuming other customers are having their orders completed and revenue recognized with no major declines to their usual annual revenue (about $150 million), it is reasonable to provide this forward-looking revenue number to account for uncertainties.

However, if management believes the tower order is transformational and has good margins (translation: must actually lead to profitability), then I believe that with their current margins and ability to create net profits it should be reasonable to expect a net annual GAAP profit of $10 million.

Their current shares outstanding stand at 20.67 million, as displayed above, and so the current valuation of $2 would lead this company to have a market cap of $41.34 million, approximately. This valuation would be severely expensive if we account for profits alone, standing at around 41x GAAP profits. However, this is why I consider their positive shareholder equity and revenues into my valuation estimates.

If management were to improve their margins enough to exceed expectations and say, double the net profits in comparison to this expectation, then the valuation would then stand at 20.5x. This is an advantage of having high revenues as it allows the company extra room to become more cost efficient.

Additionally, as shareholder equity is, in easy words, the value of the company’s assets after subtracting all liabilities (including debt), then it would be a little extreme to value the company at around $1 or even $1.50, as equity would be quite higher than the market value of the company itself.

This may explain why Broadwind has seen difficulty falling below $1.50 in terms of price action. Even though debt-to-equity is over 100% primarily due to the combination of current debts and longer-term debts, it does not mean that the equity is worthless. As nature of equity, it already has all liabilities accounted for, so debt-to-equity is better used as a metric of the company’s financial solvency (especially in combination with fully liquid cash) than to undermine the company’s equity position.

Because their TTM equity was $48.9 million and my expectation is for it to be at least $40 million, then a valuation of $2 would provide an almost one-to-one relation to their equity, give plenty of room for improvements in fundamentals and as a result of that, possible appreciation after those improvements.

However, at the current valuation of over $5, Broadwind is at risk of a 60% decline should the fair valuation materialize into the stock price.

Risks

I believe that there’s a lot of good news here with the current announcement. I do not fully know all the variables and investors likely don’t either, which means that there may be some pleasant surprises to come in 2023 should the company succeed translating that $87.5 of annual revenue into actual profits.

The company also managed to survive this long with their cash reserves having been in a worse position than it is now, so it’s important to keep this in mind if betting on a bankruptcy.

Additionally, as is often the case with stocks that are turned into meme stocks or dragged into a meme stock mania, price movements are often irrational and even cause more damage to one’s short position than one would want, as is what happened with GameStop almost two years ago. Do consider the smallest chance that Broadwind may ignore fundamentals for even longer and rise beyond $10 as part of the “story” that we’re being sold, if any.

Conclusion

Looking at what was observed so far, it is fair to say that while I would be encouraged by the new tower order, the price movement may have both priced in the order and beyond. The tower order is not as transformational as management says with the current information retrieved. Additionally, I am not looking particularly encouraged by the company’s balance sheet indicating they’re running on thin ice and in a highly risky situation that can get worse with deteriorating conditions. I believe this would be an interesting short if anyone’s brave enough to battle the meme stock traders but as my disclosures would imply, in the near term I would sit in the side-lines until I see some signs of this rally calming down after going on cloud 9 these last few days.

My current price target is rather low, but generous in order to take into account stockholder’s equity, revenues and the possibility of improving conditions in the near term. I rate Broadwind a sell and give it a price target of $2.00, with the possibility of the stock being upgraded to hold if the stock price falls under $3 or the fundamentals improve enough to justify the current $4.40 price tag. Additionally, imply a downgrade to super sell (strong sell) if the rally goes to $6 and beyond.

Be the first to comment