urzine/iStock via Getty Images Singular Research

Investment thesis

Safe & Green Holdings (NASDAQ:SGBX) develops prefabricated modules for use in safe and sustainable building construction. The Company’s proprietary technology repurposes shipping containers into safe green building blocks to be used for various forms of properties, including residential, office, and commercial.

Safe & Green Holdings offers modular construction with lower costs of capital over traditional construction, enabling developers to increase the number and size of the projects. This cost reduction also leads to a significantly improved internal rate of return (IRR) for developers. Modular construction is typically about 10-20% less expensive per square foot than traditional construction. We believe SBGX provides a viable alternative to traditional construction that is not only greener and quicker but less expensive and longer lasting.

The Company’s ongoing expansion plan (building three new manufacturing facilities) will significantly boost its manufacturing revenue and enable the firm to completely vertically integrate its cost of goods sold, thereby increasing margins. In addition to the construction segment, the focus on expanding the point-of-care testing services beyond COVID-19 opens another larger market vertical. The U.S. point-of-care diagnostic market will reach $11 billion by 2024, according to Safe & Green Holdings Inc.

We believe Safe & Green Holdings has emerged as a company with a diversified revenue stream driven by a growing construction segment as well as an extremely healthy point-of-care solutions opportunity for their medical segment without reliance on COVID testing.

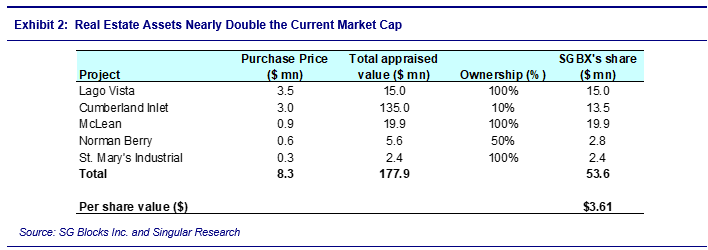

The balance sheet is strong, with minimal debt and $4.4 million in liquidity (cash plus an escrow bond). Our assessed value of SGBX’s real estate portfolio is estimated at $53.6 million (see Exhibit 2), which is more than 2.5x their current market capitalization of $19.6 million. As a result, we believe the share price is undervalued. However, the higher interest rate environment is a headwind in the near term as it is likely to put pressure on real estate and real estate development, but as interest rates decline, we expect demand to return for SGBX’s products and real estate portfolio.

We initiate coverage with a Buy-Long-Term rating and a $6.50 price target.

Real estate assets worth more than the current market cap

Our assessed value of SGBX’s real estate portfolio is estimated at $53.6 million (or $3.61 per share), which is more than 2.5x their current market capitalization of $19.6 million. This portfolio includes SG DevCorp’s four development projects and two industrial facilities. It does not ascribe any value to the Monticello News project as well as two other upcoming industrial facilities (Waldron and McLean).

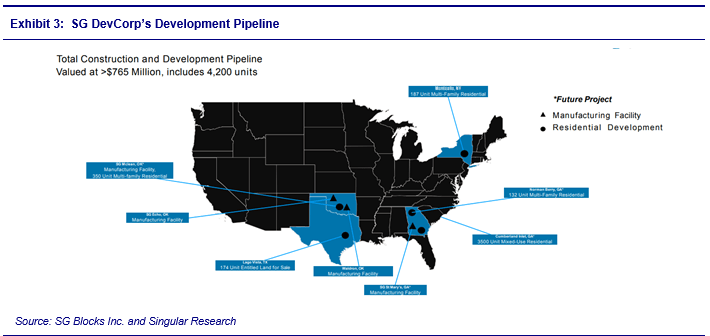

The Company, via its subsidiary SGB DevCorp, owns an interest in five projects currently under development. These include – Monticello News (100% interest), Norman Berry Village (50% stake), Cumberland Inlet (10% stake), Lago Vista (100% interest), and McClean (100% interest). Additionally, there are three manufacturing facilities in their pipeline.

In September 2022, we noted that SGBX had published four land appraisals relating to the Company’s McLean, Norman Berry, and Cumberland properties and the planned St. Mary’s Industrial site located within the St. Mary’s Commerce Park.

SG Blocks Inc. and Singular Research

Vertically integrated business model

SGBX’s business model is vertically integrated with its own in-house module manufacturing facilities as well as its own development projects, which procure modules from their manufacturing facilities. The Company currently owns and operates its main manufacturing campus in Durant, Oklahoma (SG Echo), which provides an internal means of controlling production. In addition, SGBX is building three additional facilities – Waldron (anticipated Q1:23), McClean, Oklahoma (2023), and St. Mary’s, Georgia (2024). These new manufacturing lines, along with their existing facilities, will produce the modules for SGBX’s own development company and its medical segment, which is called Clarity Mobile Venture.

These manufacturing facilities allow SGBX to control the cost of goods sold as well as general manufacturing revenue. Safe & Green Holdings’ current manufacturing pipeline is estimated at $765 million, largely driven by commercial clients and SGB Development Corp (SGB DevCorp). SGB DevCorp’s projects will be constructed using modules built in one of the vertically integrated factories operated by SG Echo. SG DevCorp projects are manufactured at cost plus a 15% margin. This vertical integration means SG can generate both manufacturing revenue and traditional revenues associated with real estate development. These revenue opportunities include sale-leasebacks for factories, developer fees, refinancings, asset sales, operating income from projects, and many others.

SG DevCorp currently has approximately 4,200 residential units in its pipeline. It is targeting to reach 10,000 units in its pipeline, which will provide approximately $1.5 billion in manufacturing revenue over the life of these projects.

SG Blocks Inc. and Singular Research

Investment risks

- Customer concentrations remain a key risk for SGBX. For H1:22, nearly 90% of their revenue was generated from two customers. The loss of business from a significant customer could have an adverse effect on business, financial condition, and cash flow.

- The Company is dependent on the expansion of its manufacturing capacity to keep pace with the demand for modules needed to complete its own real estate development projects. Failure to execute or any delay in the expansion plan could negatively impact its development timelines and could put pressure on financials.

- The decline in Covid-19 testing will adversely impact medical segment sales. However, SGBX has laid out plans to diversify into point-of-care testing for other diseases. There is no guarantee that this diversification will be successful.

- Dilution remains a risk for the firm, given its volatility in earnings and ongoing expansion plans, which will need additional capital. If the Company is unable to generate sufficient cash flow, more equity may be needed for additional capital, which would lead to dilution.

Recent stock action

Since the end of 2021, the stock has moved up significantly. The stock movement is likely due to a couple of items.

- The company released a fairness opinion issued by ValueScope, Inc. on the previously announced spin-off of thirty percent (30%) of its subsidiary, Safe and Green Development Corporation. Based on ValueScope’s opinion, Safe and Green Development has an estimated fair market value of approximately $74.3 million.

- Another possibility is that investors may be jumping back into the stock after harvesting tax losses for the year.

Valuation

We value SGBX using a sum-of-the-parts (SOTP) valuation. We value SGBX (excluding SG DevCorp), which is comprised of the manufacturing and medical segment, using industry peer companies (a Price/Sales multiple) blended with our Discounted Cash Flow (DCF) valuation. The real estate development business (SG DevCorp) is valued based on the fair value assessment of the projects provided by the Company.

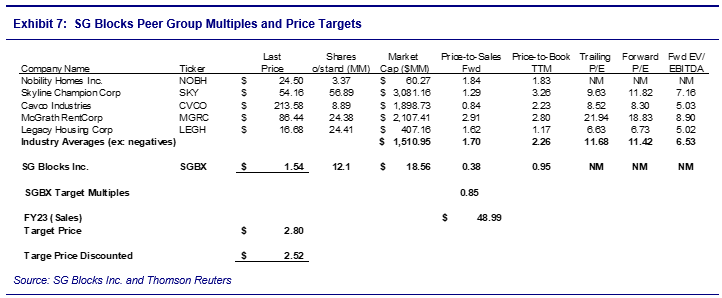

SGBX (excluding SG DevCorp): Our peer group comprises companies involved in providing prefabricated buildings for residential and commercial purposes. We believe these competitors are the closest peer group relevant for SGBX (ex. DevCorp). We value SGBX (ex. DevCorp) at 0.85x 2023 sales, which is a ~50% discount to the peer group given its smaller size, lack of profitability, and early stage of the Company’s ongoing expansion. However, we believe that the discount should further narrow as the Company delivers on its expansion and revenue diversification strategy. This valuation results in a price of $2.80, which is discounted back at our cost of capital (~11%) to arrive at a target price of $2.52.

We weight the other 50% of our target using our Discounted Cash Flow target. Our DCF model uses our forecasted free cash flow to the firm over four years, and then grows EBIT at a 20% rate over years five to seven, 10% over years eight and nine, and 3% thereafter. We apply a weighted average cost of capital of ~11%. Our DCF produces a value of $3.17.

The combination of $2.52 at 50% and $3.17 at 50% results in a weighted average price target of $2.85. Exhibit 7 below summarizes our peer group multiples, while the DCF is included at the end of this report.

SG Blocks Inc. and Thomson Reuters

SG DevCorp: Our assessed value of SGBX’s real estate portfolio is estimated at $53.6 million (or $3.61 per share), as shown in Exhibit 2 earlier in the report.

We add the value of the SGBX (ex. SG DevCorp) and the SG DevCorp business to arrive at the final valuation for SGBX of $6.46, which we then round up to $6.50.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment