hapabapa

Introduction

If it wasn’t for the 9th ranked number of Phase 3 clinical trials, Bristol Myers Squibb (NYSE:BMY) may have ended up leading my recent pipeline analysis of the top 10 pharmaceutical companies. While Swiss competitors Novartis (NVS) and Roche (OTCQX:RHHBY) score slightly higher, addressing the best US-based player is important when considering foreign exchange rates. Despite a strong USD, BMY is performing well over the past 12 months, particularly when focusing on R&D and profitability. The current issue is that BMY has a small P3 clinical trial base, and this reduces the opportunity in the short-run. However, as the data suggests, the growth issue over the next few years may be negated by all the other positive indicators. Therefore, BMY remains a superior choice in Large Cap Pharma.

Pipeline Analysis Results

When considering valuation, Bristol Myers scored third out of 10 large cap competitors, with an average rank per metric of 3.8/10. Above them was Novartis in first and Roche in second, while Pfizer (PFE) and Merck (MRK) were in fourth and fifth. Despite high ranks in 2 metrics, BMY was very consistent, ranking top 3 across the rest of the data points. The data is summarized in the bullets below.

-

Phase 3 trials: 25 – rank 9

-

Phase 2 trials: 48 – rank 3

-

R/D Expense / Revenues (%): 22 – rank 2

-

Levered Free Cash Flow Margin (%): 22 – rank 2

-

Price / R&D Expense: 16x – rank 1

-

Price / FCF: 24x – 6th

Past and Present

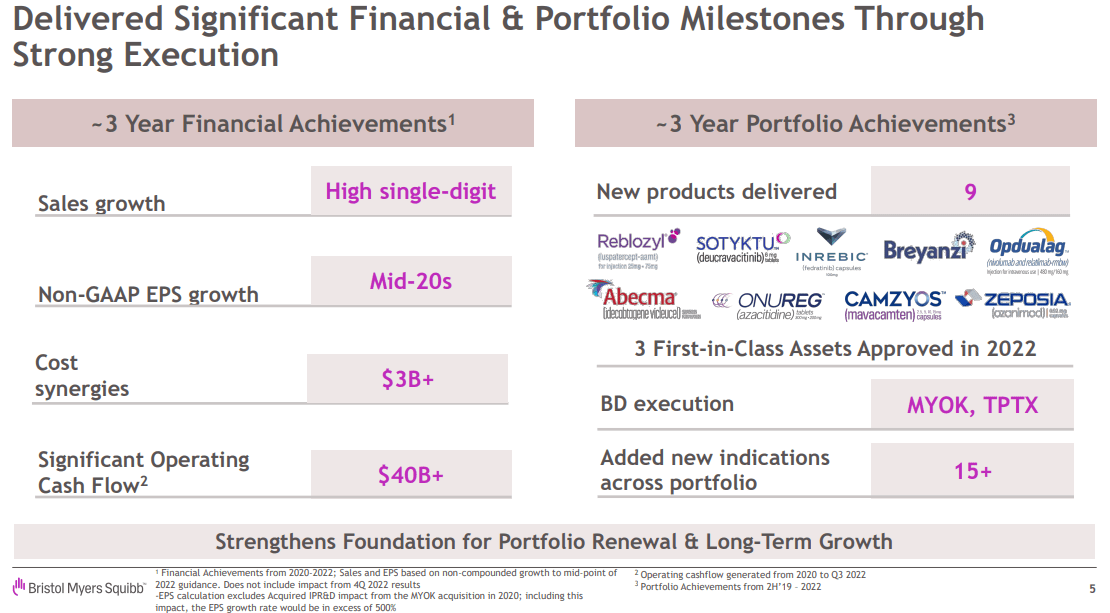

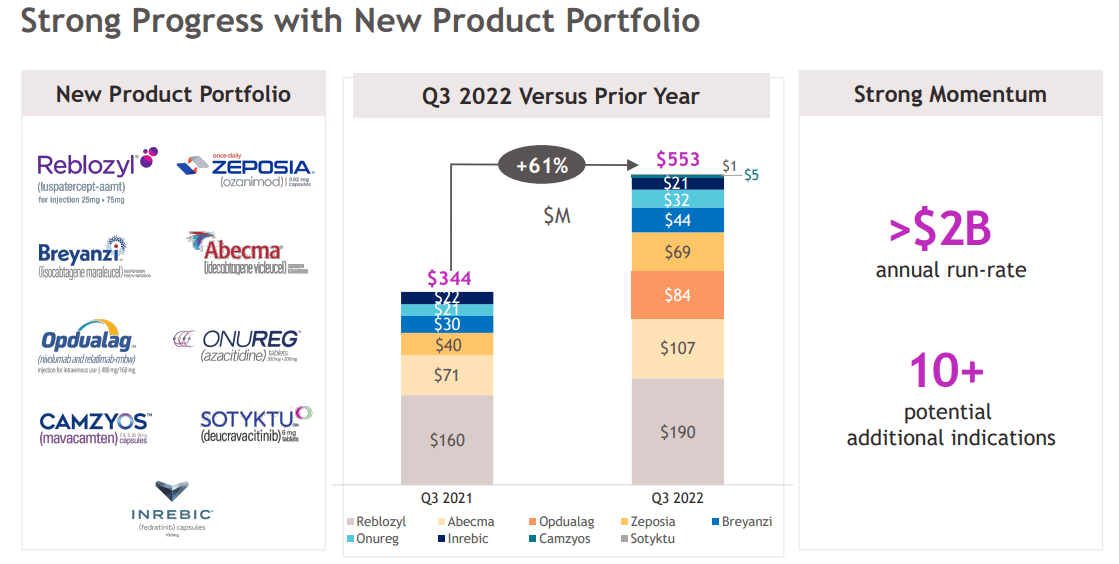

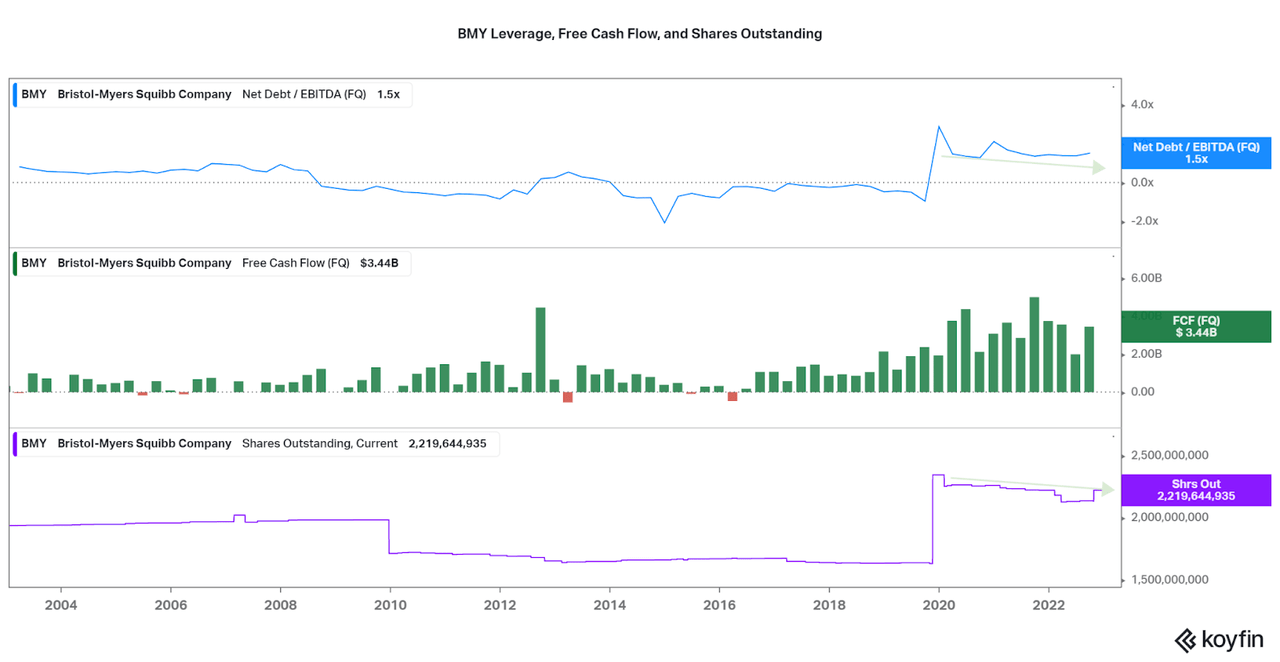

Bristol Myers Squibb has positioned themselves well in early 2023 thanks to leveraging the success of three main therapies, Revlimid (currently fighting off generics), Eliquis (shared with Pfizer), and Opdivo. However, all three blockbusters are aging, facing competition and replacement soon. Now, thanks to many years of profit generating, approximately $40 billion in operating cash flow over the past three years, has allowed BMY to establish the third-largest Phase 2 trial base. Investors can even be happy with short-term performance (2023-30) as over the past three years, BMY has released 9 new therapies across a wide range of treatment areas and technologies.

Also of importance, the success cannot be attributed to internal R&D alone, as BMY acquired Celgene in 2019. Investors can consider BMY’s $74 billion acquisition a success, as cash flows and R&D expenses are best in class. With capable management providing synergies across both the biotech and pharma units, I believe the future is bright. For the next few years, look to the current recent approvals to be the new cash flow generators, and then the large P2 clinical asset base will move to replace those. This is the power of a strong pipeline in providing a transparent outlook.

BMY JP Morgan Healthcare Conference 2023 Presentation BMY JP Morgan Healthcare Conference 2023 Presentation

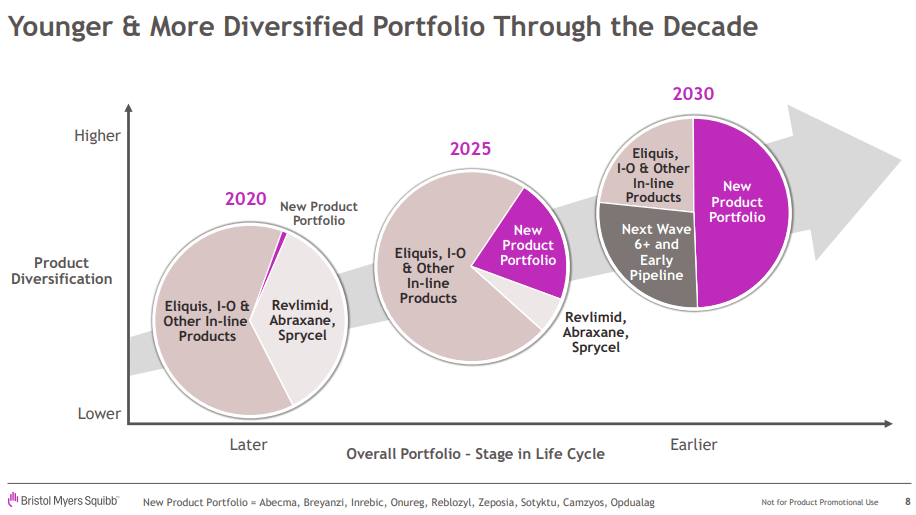

One of the best aspects of Bristol Myers’ clinical pipeline is that they have a diversified focus, rather than a focus on blockbuster therapies in a single area, unlike peers such as Novo Nordisk (NVO). Thankfully, this is reflected in the analysis and was able to single BMY out as a leader, and NVO in last place. This does not mean other companies will outperform or not, but that BMY is safe, stable, and predictable. When investing in pharmas, that is far more important than total return.

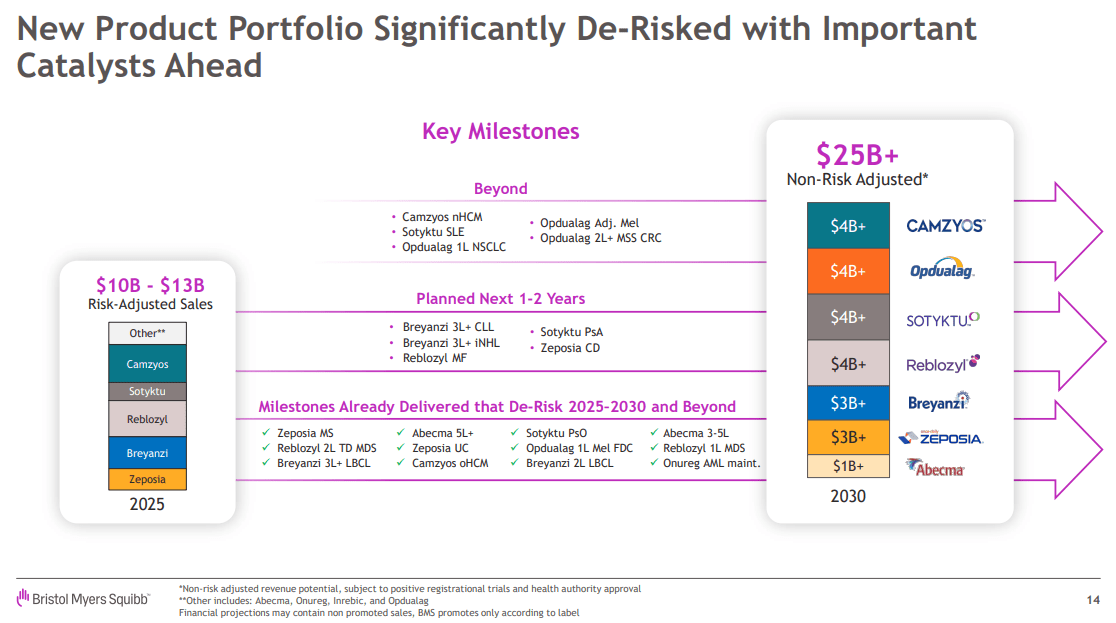

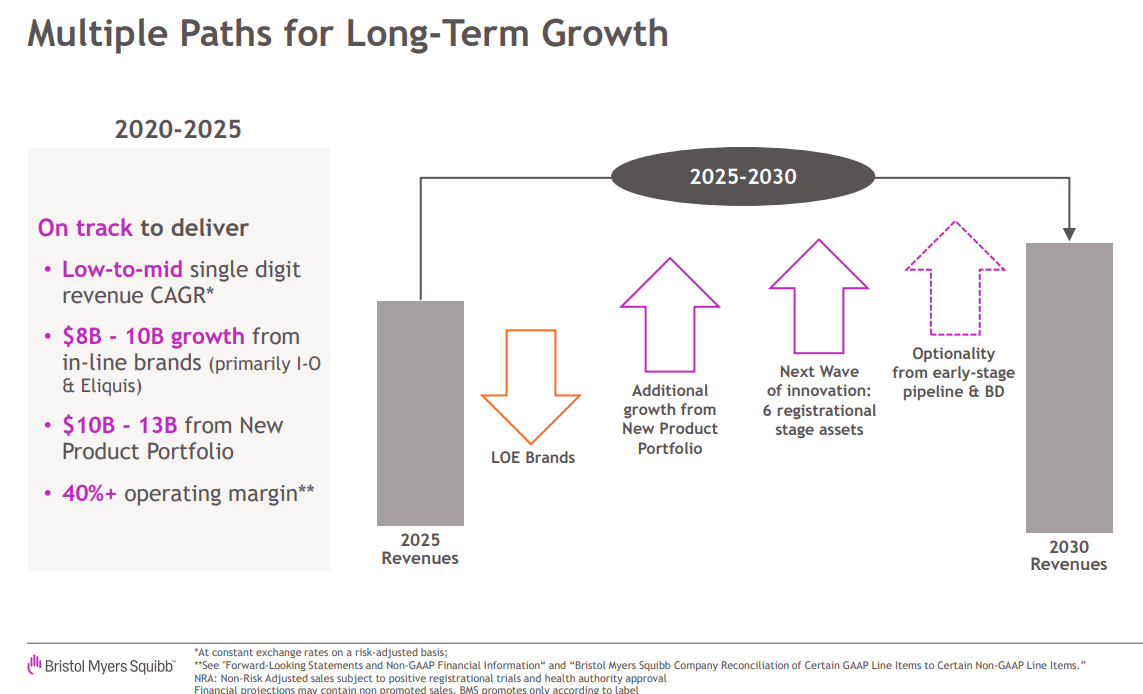

The Power of the Pipeline

Bringing a drug from the research phase to full approval can take over 10 years. Therefore, the pipeline is a great future indicator to use for pharmas. In the case of BMY, 2030 revenues are expected to be dominated by the approvals of the past five years, not the current P3 or P2 therapies. Management currently expects the asset approved asset base to create $25 billion in revenues (not risk adjusted) by 2030. Don’t forget that current blockbusters Opdivo and Eliquis are not set for patent expiration until 2026-28. The multi-billion in revenues from these two therapies alone are not even included in current financial outlook.

BMY JP Morgan Healthcare Conference 2023 Presentation

Financial Implications

The $25 billion in revenues from approvals over the past 3 years is expected to amount to ~50% of total revenues upon maturity, with current P2 and P3 trials accounting for up to an additional 25%. This means total revenues should be around $50 billion, or 8% more than the trailing 12 months of revenues. I believe these figures are quite conservative, as expanded indications in Opdivo and Eliquis may extend the life cycle of these blockbusters past patent expiration in 2026-8. Also, generics may take a while to enter the market and BMY can adjust pricing accordingly.

Also, with inflation and economies around the world remaining stubbornly strong despite higher interest rates, it may be viable to expect higher drug pricing in the future. This suggests that the 8% growth over 7 years may be far below the actual revenues, allowing for upside. However, it is important that revenue growth will not be the major determinant of future returns, as high profitability can lead to inorganic growth, earnings growth, buybacks, and an increased dividend. With the pipeline data suggesting there will be plenty of assets to monetize in the years to come, I expect profitable outcomes with an investment in Bristol Myers Squibb.

BMY JP Morgan Healthcare Conference 2023 Presentation BMY JP Morgan Healthcare Conference 2023 Presentation Koyfin

Valuation

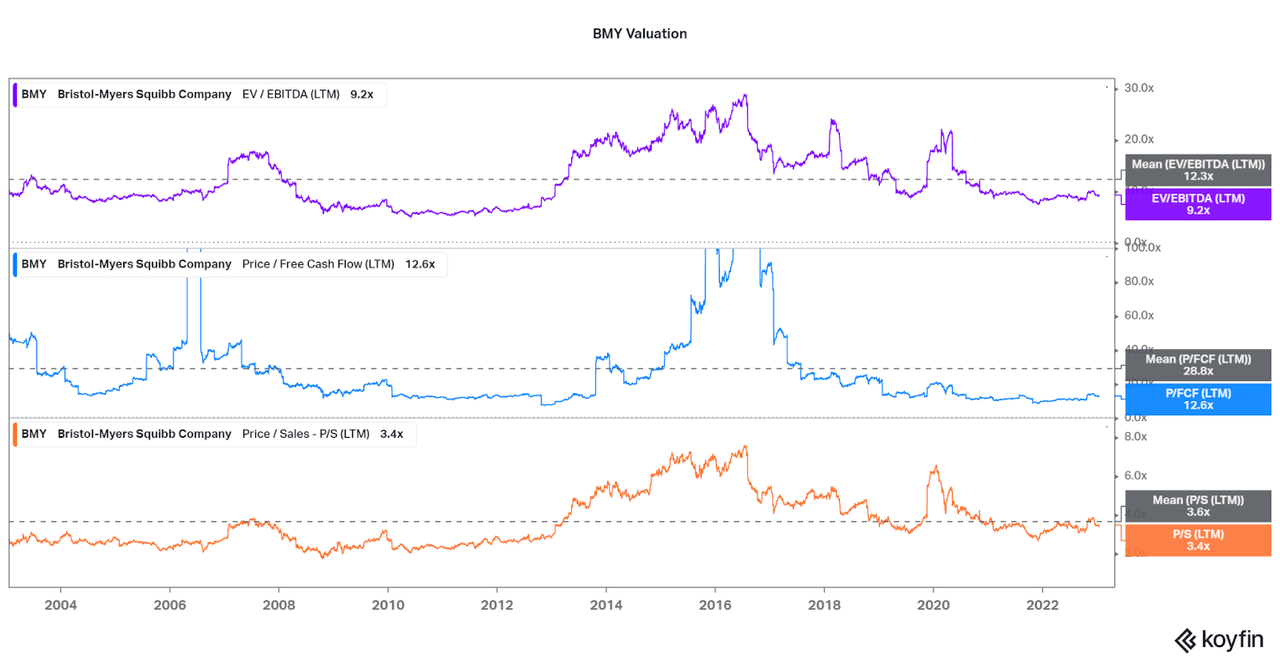

In my pipeline analysis, BMY ranked first in terms of Price / R&D Expenses and third for Price / Free Cash Flow. Therefore, considering all the other pipeline data, my analysis indicates BMY is a good value proposition at the moment compared to peers. However, we should also take into consideration the current valuation from a historical standpoint. To do so, I created a chart highlighting Bristol Myers’ mean P/E, EV/EBITDA, and P/S. In all three metrics, BMY is currently at a below average valuation. With most other healthcare names at peak valuations, it is clear BMY still offers a viable entry point at the moment.

Koyfin

Conclusion

Bristol Myers Squibb looks to be the US’s best opportunity in Big Pharma. There are risks though, mostly surrounding the small P3 trial base focusing on indication expansions, a strong USD hurting sales, and various litigation battles, which may suppress the share price at various points in the coming years. However, the underlying pipeline of multiple current approvals and the early stage pipeline offer a positive outlook for the company despite shifts in sentiment.

With the valuation now below 20-year mean levels, I believe it is ok to continue adding shares on a recurring basis. If the valuation rises above those mean valuation levels, then I would begin to hold. With such positive outlook, I would hesitate to trim even if the valuation rises significantly, although I will update if this occurs.

Also, I find the likelihood of an excessive valuation to be low due to the lack of reliance on a singular therapy or treatment area for cash flows, unlike other pharmaceuticals. Therefore, enjoy adding shares at a low valuation over the next few years and then reap the benefit from the consistency in the long run.

Thanks for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment