Ultima_Gaina

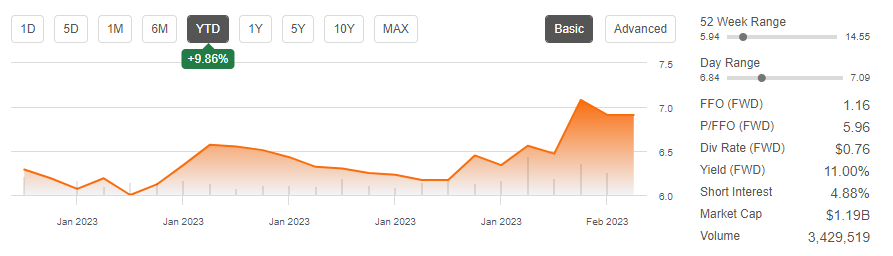

Brandywine Realty Trust (NYSE:BDN), a real estate investment trust (“REIT”) with a core focus in the Philadelphia and Austin, Texas sub-markets, is off to a great start in 2023, with a total YTD return of nearly 10%.

Seeking Alpha – Basic Trading Data Of BDN

And since a prior analysis on the stock, shares are up about 10.5%. This compares favorably to the S&P 500’s (SPY) 7% gains over the same period.

Despite the recent run-up, BDN is still down nearly 50% over the past year. In addition, the stock trades at less than 6x forward earnings with a dividend payout that is currently yielding 11%. For both income investors and those seeking material share price appreciation, recent results are worth further review.

Q4FY22 Earnings Recap

At the end of fiscal 2022, total portfolio occupancy stood at 89.8% or 91% on a leased basis as of January 31, 2023. This compares unfavorably to occupancy and leased rates of 90.8% and 91.8% at the end of Q3 and mid-October, respectively.

In addition, occupancy levels were below company targets of about 90.7%. Driving the miss was a tenant default in their Austin market. This provided a negative contribution to top line levels of approximately 50 basis points (“bps”).

The tenant itself accounted for 65K SF of space in the region, and BDN had been involved in an ongoing dispute with them over the course of the fiscal year.

From a financial perspective, the tenant was fully reserved. Their risk of default, therefore, was already baked into their operating results in prior periods. Looking ahead, BDN does have the space back on the market and is currently in negotiations on about 12K SF of that space.

The default, in addition to other known tenant move outs, also contributed nearly 50% to BDN’s negative absorption of 123K SF for the quarter. This in turn produced a retention rate below their annual run rate, though for the year retention still came in above their guidance of 64%.

Aside from the one tenant default, occupancy held up in their Pennsylvania and Austin portfolios, which together comprise over 90% of their net operating income (“NOI”). Considered together, the two markets were 91.7% occupied and 92.9% leased at year end.

At an occupied rate of 83.6%, however, the Austin market still trails both the Philadelphia Central Business District (“CBD”) and the suburbs, which are occupied at 96% and 92.4%, respectively. Given the inherently greater opportunity embedded in Austin, leasing volumes are likely to be greater there in 2023 than in the Pennsylvania market.

Leasing spreads in the Austin market, however, are expected to come in below their targeted range, which is between 4% to 6% on a cash basis. Their Pennsylvania markets, on the other hand, are expected to come in above the projected range.

In both cases, the mark-to-market is notably lower than current year figures, which came in at 12.5% on a cash basis for the quarter and 10% for the year.

The mark-ups attained in 2022 also came on strong overall leasing volumes. During the quarter, for example, BDN completed 226K SF of signings, 142K of which were attributable to new activity. This brought their yearly total to 1.8M SF, which compares favorably to 2021.

And when singling out their new signing activity, total new signings were above 2021 levels by 11% and on par with pre-pandemic levels achieved in Q4 of 2019.

BDN also remained active in the capital markets. During the quarter, total leverage, as measured by net debt levels in relation to EBITDA, decreased to 7.0x on a non-core basis and 6.2x on a core basis. This is in-line with the midpoint of their guidance range.

They also raised over +$745M in funds via financing activity and the dispositions of two properties, which were completed at cap rates below 6% and generated +$130M in proceeds.

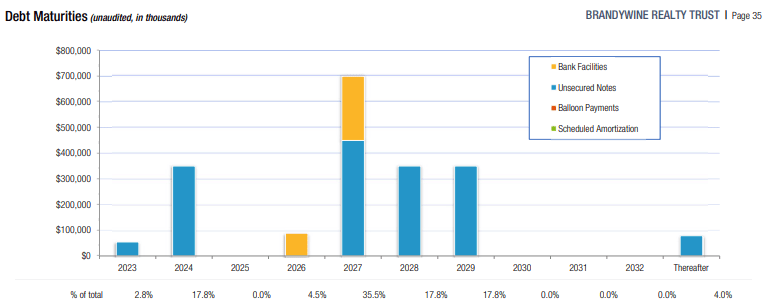

All considered, BDN has full availability on their +$600M unsecured credit line and about +$30M of unrestricted cash on hand. This is paired with an improved debt ladder, which is comprised of 96% fixed-rate debt and limited material maturities until late 2024.

Q4FY22 Investor Supplement – Debt Maturity Schedule

Post-Earnings Insights

BDN was a beneficiary of the turn to quality in 2022. During the year, over 600K SF of their total activity was related to tenants that chose to move up the quality curve, with nearly 60% of their new activity in the quarter attributable to this. Additionally, about 40% of their pipeline in their operating portfolio is related to those seeking higher quality spaces.

Their portfolio of more desirable properties also contributed favorably to touring volume. In Q4, physical tours were up 50% on a sequential basis and 12% YOY. On a full-year basis, total tour volume amounted to 1.2M SF.

Tenant expansions also continue to outweigh contractions by a ratio of nearly 2.5:1.

Despite a robust pipeline, portfolio metrics were hindered by the default of a tenant in their Austin market. While this was largely to blame for lower occupancy levels, it is not an area of concern, as the overall portfolio remains well occupied in their primary Southeastern Pennsylvania markets. Furthermore, there is significant upside embedded in their Austin market, much of which will likely be realized over the coming years as ongoing developments continue to deliver.

In addition, BDN has an increasing stake in the Life Sciences market, which has enormous potential over the coming years. In their development pipeline, for example, 30% of their wholly-owned development is attributable to the industry. Combined with their joint activities, the pipeline is weighted over 40% to Life Sciences at full cost.

This increasing exposure level does warrant a reassessment in the stock’s current valuation, which continues to trade at a cap and pricing multiple that is disconnected with their operating performance. For income investors, the upside potential would be in addition to a reoccurring dividend payout that is presently yielding 11% at current pricing.

Initiating a position for the dividend alone, however, may prove to be unwise, as coverage is uncomfortably tight heading into 2023. In addition, the yield is well above those offered by their peers. One west coast peer, Douglas Emmett (DEI), for example, recently cut their dividend in favor of a repurchase plan. Other peers within the sector have also trimmed their dividends in response to current market dynamics.

Given the disconnect in BDN’s share price relative to the valuations fetched by recent dispositions, it wouldn’t be surprising if BDN followed in the footsteps of DEI with a reallocation of capital from dividends to repurchases.

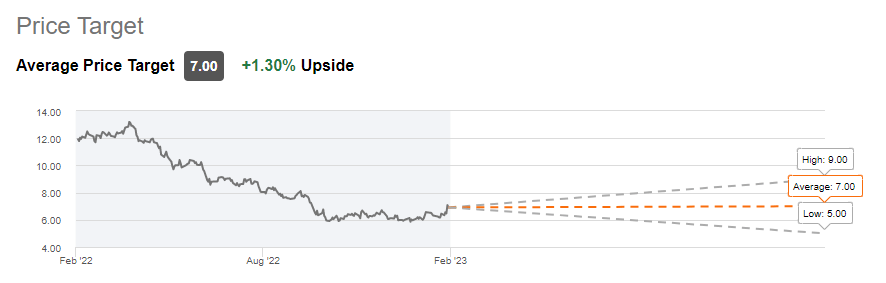

The risks pertaining to their current payout, however, are offset by the upside potential in the shares. At an implied cap rate of over 10%, BDN trades significantly out of range to the sub 6% rates earned on their recent dispositions. Still, it doesn’t appear Wall Street is as bullish on the valuation, as current targets imply shares are essentially fairly valued.

Seeking Alpha – Consensus Price Target Of BDN

While shares may continue to head higher in 2023, the threat of a dividend cut will continue to loom due to tight coverage levels, greater debt servicing costs, and yield disparity to related peers. And any cut would likely result in shares giving back some or all of their YTD gains. For investors seeking new positioning, BDN is one that is best left on the watchlist.

Be the first to comment