Leon Neal

Thesis

I have previously pointed out that BP (NYSE:BP) stock could be undervalued by as much as 80%. Although BP stock is slowly approaching a more reasonable valuation, the company’s strong Q3 results support a bullish thesis and more upside. Notably, BP management provided confident commentary, implying that the profit boom can continue even at lower oil prices.

On the backdrop of a strong outlook going into 2023, despite macroeconomic challenges, I raise my EPS expectations for BP through 2025, and I now calculate a base case target price of $66.55/share, as compared to $52.72 prior.

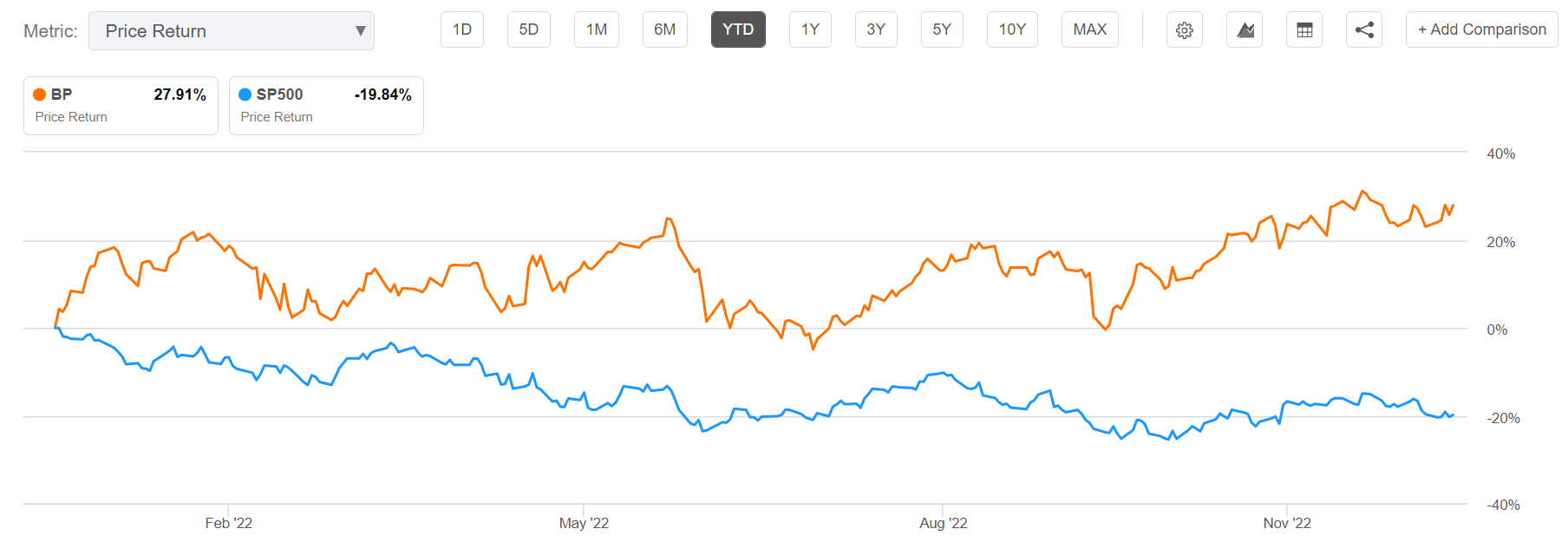

For reference, BP stock us up approximately 28% YTD, as compared to a loss of almost 20% for the S&P 500 (SPY).

Seeking Alpha

Strong Q3 Results Support Bullish Thesis

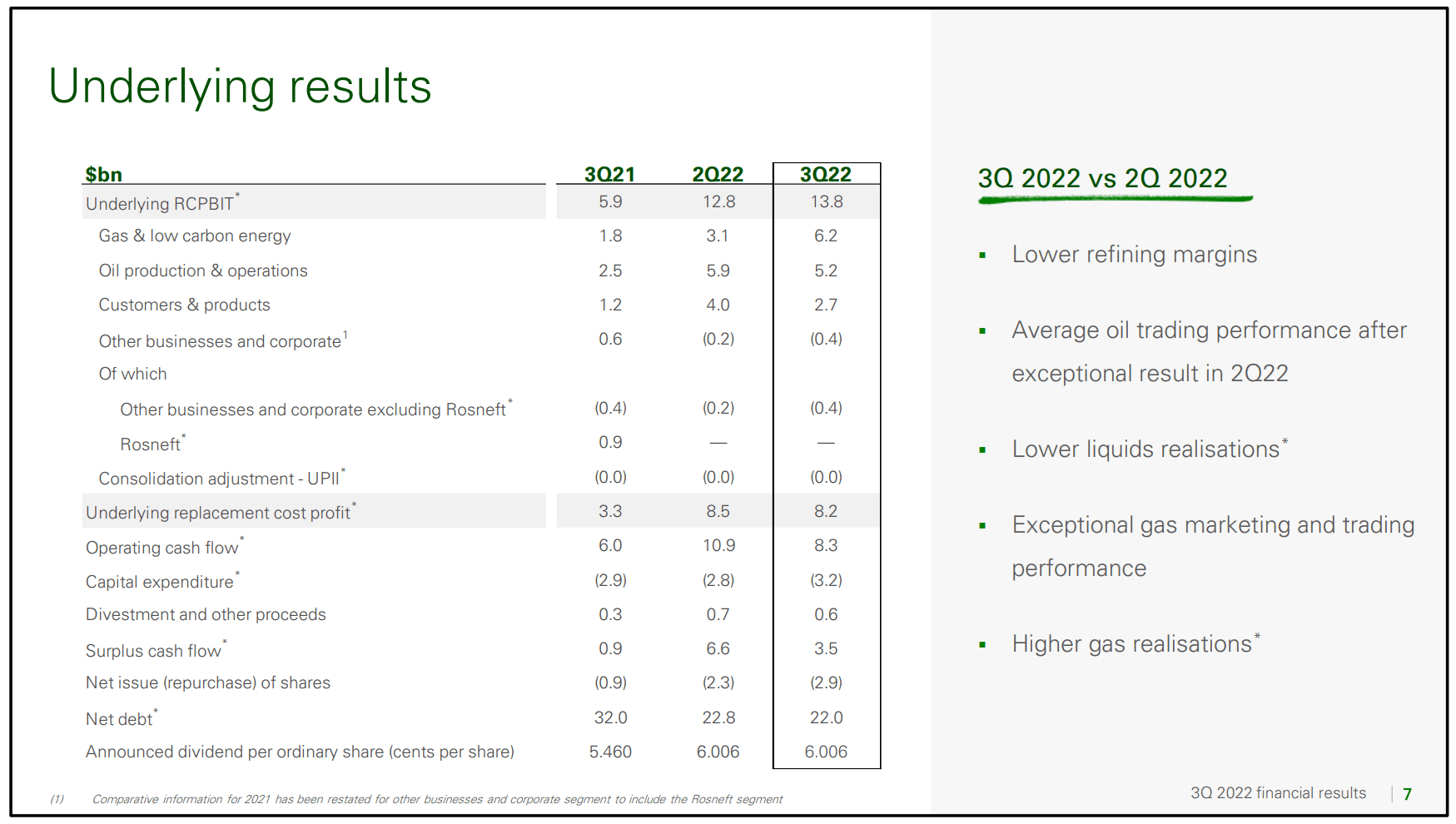

During the period from July to end of September, BP generated total group revenues of approximately $54.5 billion, which compares to $35.8 billion of revenues for the same period one year earlier (52% year over year growth).

Although BP recorded a net loss of $2.2 billion for the September quarter, the negative headline number was mainly due to an accounting formality relating to contract pricing for natural gas futures. On an adjusted basis, BP income more than doubled in Q3 2022 as compared to the same period one year earlier, growing to about $8.15 billion – which is only slightly below the record $8.5 billion achieved in Q2 2022.

Reflecting on a strong Q3 period, Bernard Looney, BP’s CEO commented:

This quarter’s results reflect us continuing to perform while transforming. We remain focused on helping to solve the energy trilemma – secure, affordable and lower carbon energy. We are providing the oil and gas the world needs today – while at the same time – investing to accelerate the energy transition. Our agreement on Archaea Energy is the most recent step in our strategic transformation of BP

BP Q3 2022 Results

Likely Strong Profitability Also At Weaker Oil Prices

Investing in oil producing assets is also a bet on the underlying fossil fuel/ energy prices. And fossil fuel/ energy prices remain supportive.

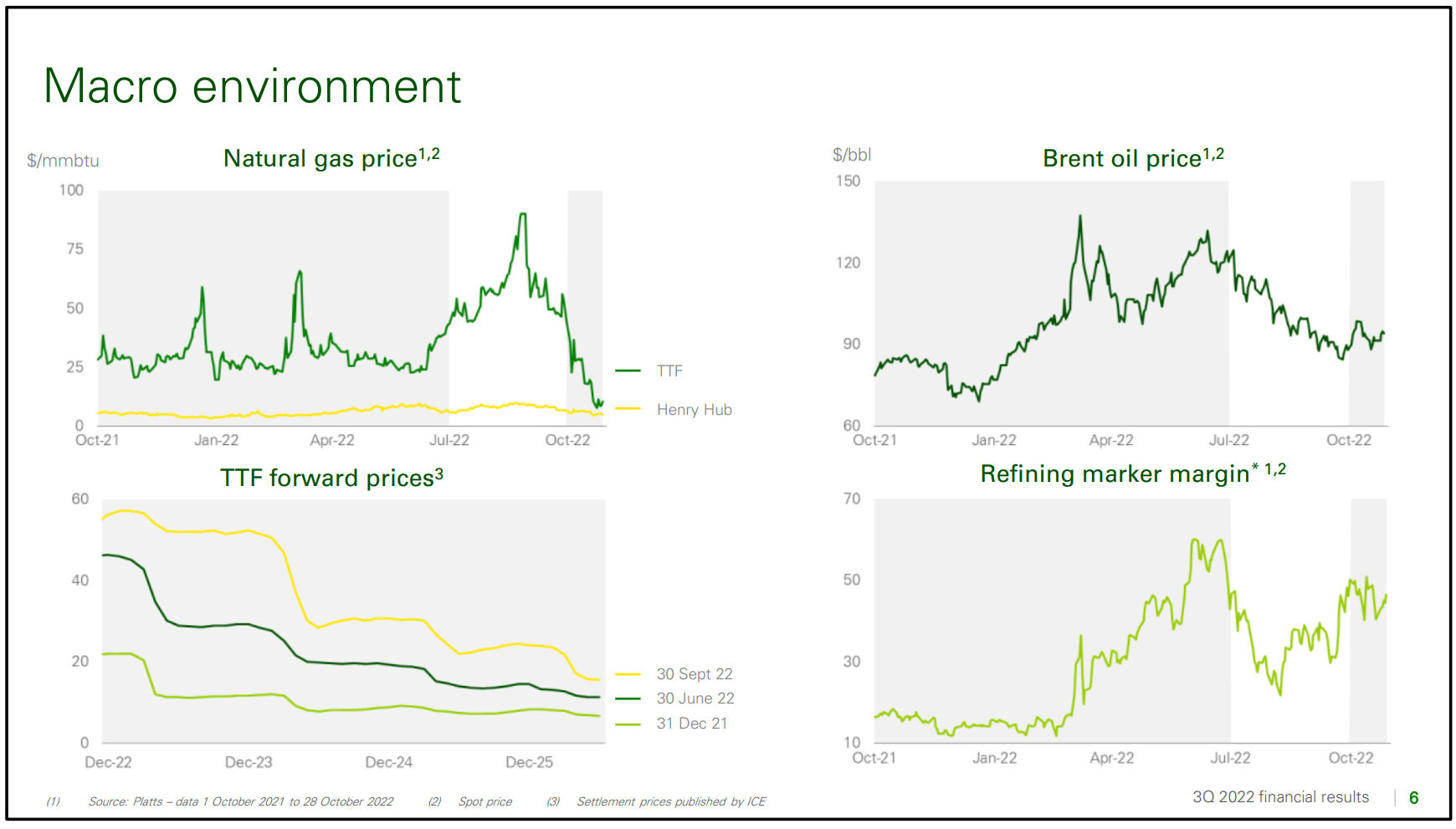

On the backdrop of surging energy prices, BP has enjoyed exceptional profitability in the past few quarters. And although natural gas and oil prices have already started to trade down towards more long-term sustainable levels, which I see around $60/ barrel, BP will likely continue to see strong profitability going forward.

BP Q3 2022 Results

Together with Q3 2022 results, BP provided confident commentary about the outlook for energy prices going into Q4 – expecting elevated oil and natural gas prices, as well as refining margins. It is thus likely that BP will deliver strong – near record – results also in Q4 and early 2023.

Looking ahead to the fourth quarter, we expect gas prices to remain elevated and volatile with the outlook heavily dependent on Russian pipeline flows and the severity of the Northern Hemisphere winter.

Moving to oil prices. During the third quarter, Brent averaged $101 per barrel, down from $114 per barrel in the second quarter. This reflected increased uncertainty around the economic outlook and the continued COVID-related lockdowns in China. Despite this uncertainty, we expect oil prices to remain elevated in the fourth quarter given the backdrop of low inventory levels, OPEC+ supply cuts, limited supply growth and uncertainty around Russian exports.

Turning to refining. Global margins decreased to average around $35.50 per barrel during the third quarter, and are expected to remain at elevated levels during the fourth quarter due to lower stocks and sanctioning of Russian crude and product.

But even if energy prices would depreciate further, the British oil major would enjoy attractive operating cash flows as long as the brent reference remains above $60/barrel.

Looking ahead, on average, based on BP’s current forecasts, BP continues to expect to have capacity for an annual increase in the dividend per ordinary share of around 4% through 2025 at around $60 per barrel Brent and subject to the board’s discretion each quarter.

And as long as the brent reference remains above $40/barrel, BP would operate cash neutral. According to the company:

[cash neutrality] is underpinned by an average 2021-5 cash balance point of around $40 per barrel Brent, $11 per barrel RMM and $3 per mmBtu Henry Hub (all 2020 real).

Attractive Investor Payouts

One key argument why BP stock is such an attractive investment is anchored on super attractive investor payouts. Given strong profitability, investors should consider that for the trailing twelve months, BP has distributed approximately $12.86 billion to shareholders, $4.35 billion of dividends and $8.51 billion of share buybacks – which implies an equity yield of more than 12% based on a $106 billion market capitalization. Notably, this is approximately x3 the yield an investor would enjoy from investing in 10 year US treasuries.

Seeking Alpha

In Q3 alone, BP has distributed almost $4 billion to shareholders – of which $1.14 billion and $2,.88 billion worth of buybacks. The company also announced a further $2.5 billion of share buybacks.

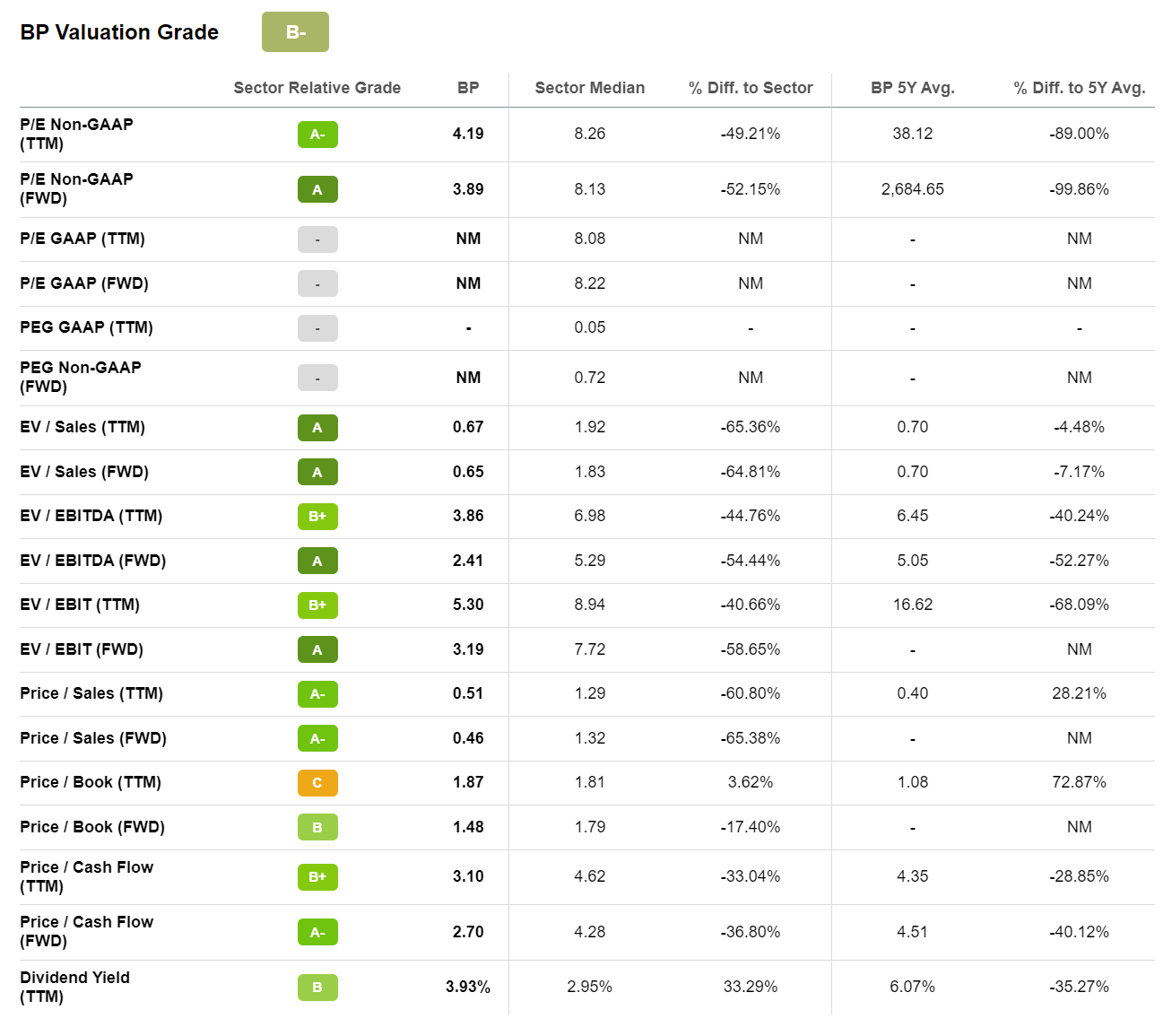

Valuation Too Cheap To Ignore

BP stock is clearly valued attractively – currently trading at a one year forward P/E of x3.9, a P/B of x1.5 and a P/S of 0.46. For reference, these multiples imply a discount to the sector median of 52%, 17% and 65% respectively.

Seeking Alpha

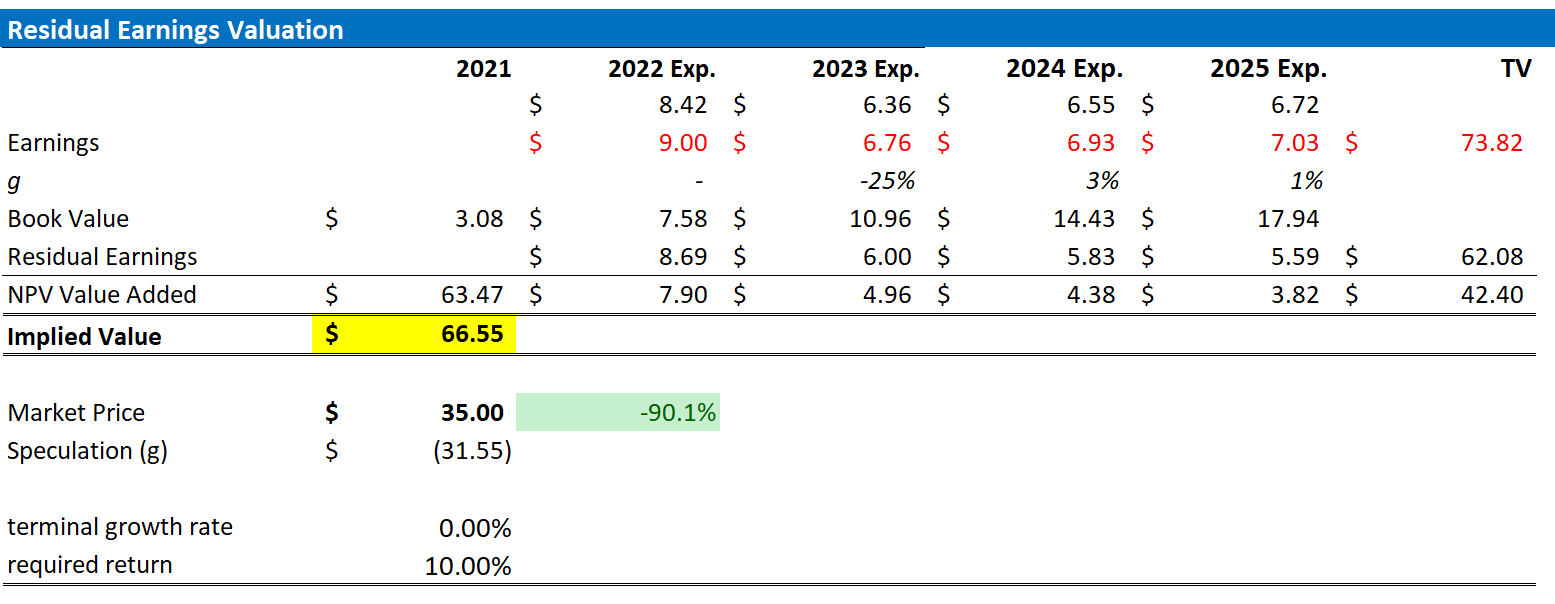

Residual Earnings Model

On the backdrop of a strong Q3 2022 and confident management commentary going into Q4 2022, I slight raise my EPS expectations for BP through 2025. However, I continue to anchor on a 10% cost of equity and a 0% terminal growth rate.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price for BP of $66.55, as compared to $52.72 prior.

Author’s Assumptions and Calculations

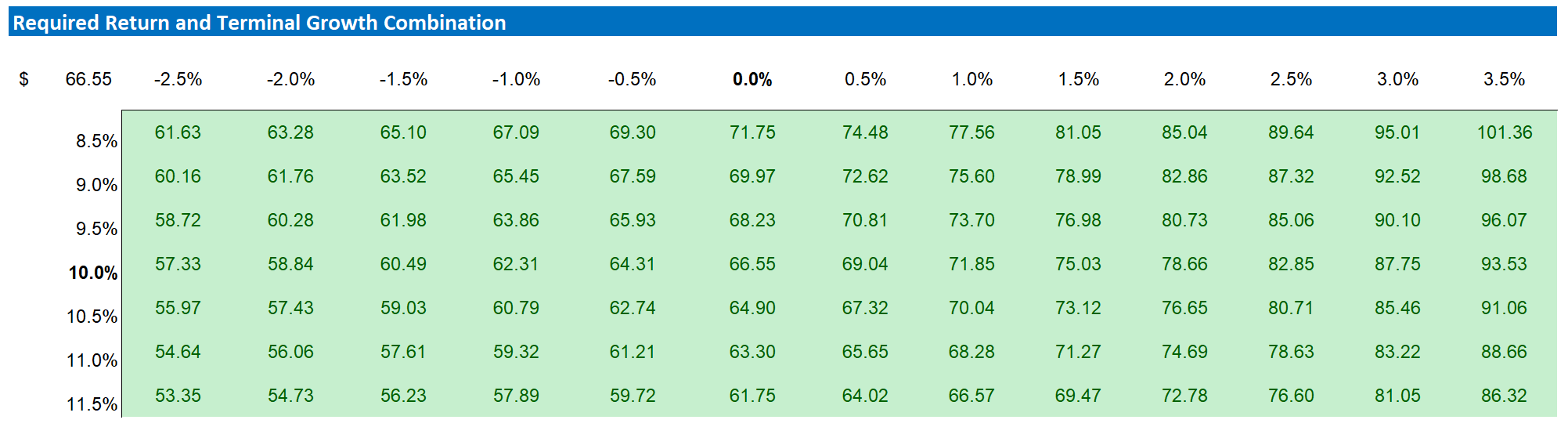

Below is also the updated sensitivity table.

Author’s Assumptions and Calculations

Risks To My Thesis

As I see it, there has been no major risk-updated since I have last covered BP stock. Thus, I would like to highlight what I have written before:

… investors should note that I assume a sustainable oil price of about $60/barrel. While this might seem bearish for some readers, others might argue that the fair value for oil is much lower.

As the 2020 COVID-19 induced sell-off has shown, oil can even trade at negative price-levels. If oil would break considerably below $60/share and does not recover within a sensible time-period, the bull thesis for BP would break.

Conclusion

Anchored on a strong Q3 reporting and confident management commentary, I remain bullish on BP stock. In my opinion, a 12% TTM equity yield (buybacks and dividends) and a x3.9 P/E multiple are simply too attractive to ignore.

According to my analysis, which I base on a residual earnings model, BP stock should be fairly priced at around $66.55/share. Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment