jetcityimage

Strong Prices Enable More Investment

Much has happened in the energy industry since Bernard Looney took over as the CEO of BP (NYSE:BP) and rolled out the company’s new strategy in 2020 to shift more focus to low-carbon energy sources. The ending of Covid-19 mobility restrictions around the world has caused energy demand to bounce back toward pre-pandemic levels. Russia’s invasion of Ukraine and the West’s response reconfigured global energy supply chains, particularly natural gas supply to Europe. Both of these shocks disrupted the energy balance much faster than they could be mitigated by renewable energy sources, regardless of Europe’s green ambitions.

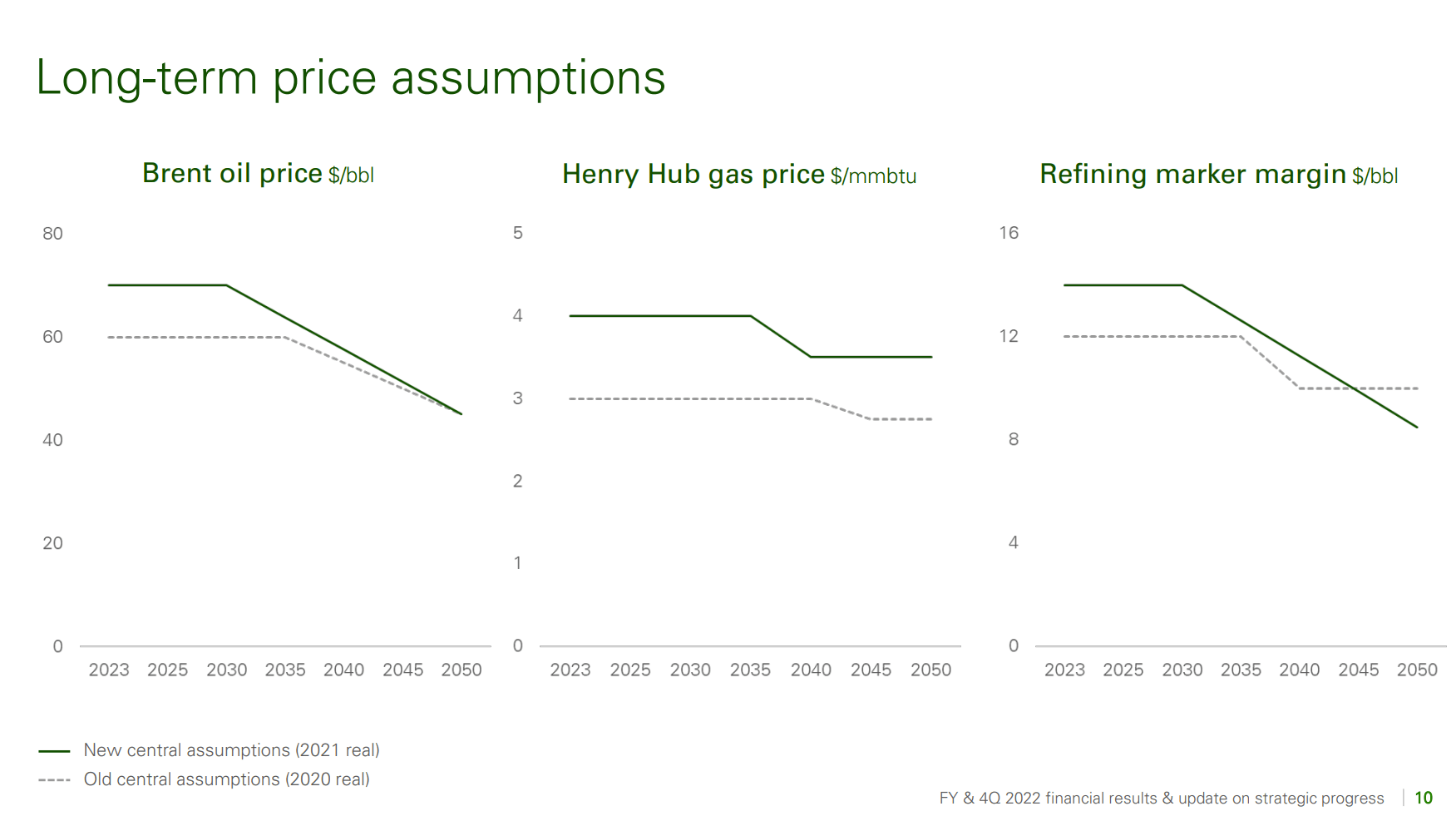

BP management began recognizing this last year as they started referring to the “energy trilemma”, meaning energy needs to be cleaner, but also available and affordable. With this recognition, the company has also shifted to a higher for longer planning price set. In the company’s 4Q and FY 2022 results, BP has raised its long term price assumptions for Brent crude to $70/bbl from $60, Henry Hub natural gas to $4/mmbtu from $3, and refining marker margin to $14/bbl from $12.

BP

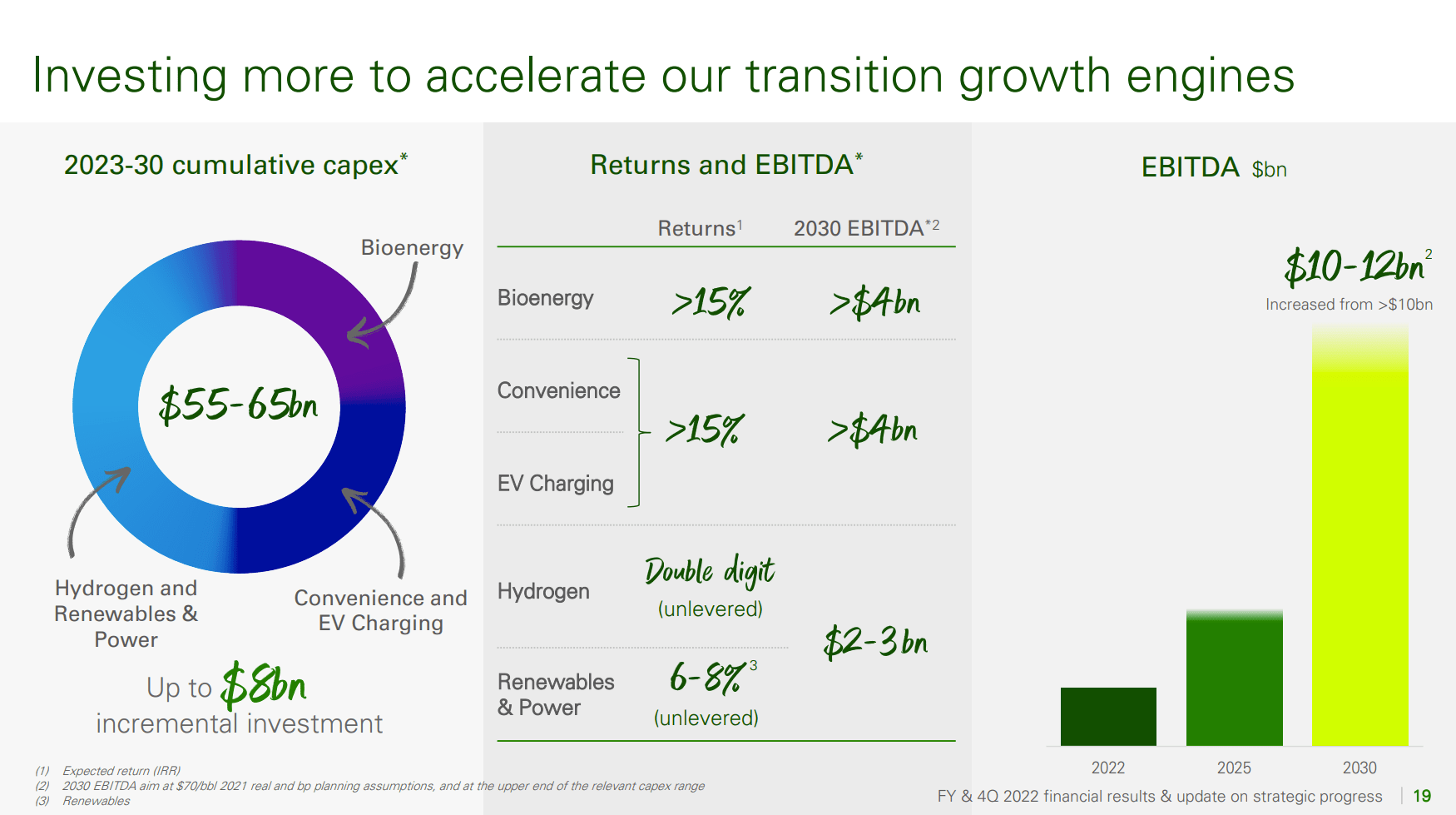

The higher prices result in stronger cash flow for BP, enabling the company to increase the high end of its capital spending plans by $2 billion per year. BP is now targeting $14-$18 billion of capex per year, up from $14-$16 billion in previous plans. The additional capex will be split with $1 billion more spending on hydrocarbons and another $1 billion on low-carbon projects. The company will also be in less of a hurry to divest oil and gas production and will focus its low-carbon efforts on higher-return technologies.

Performing (Better) While Transforming (Slower)

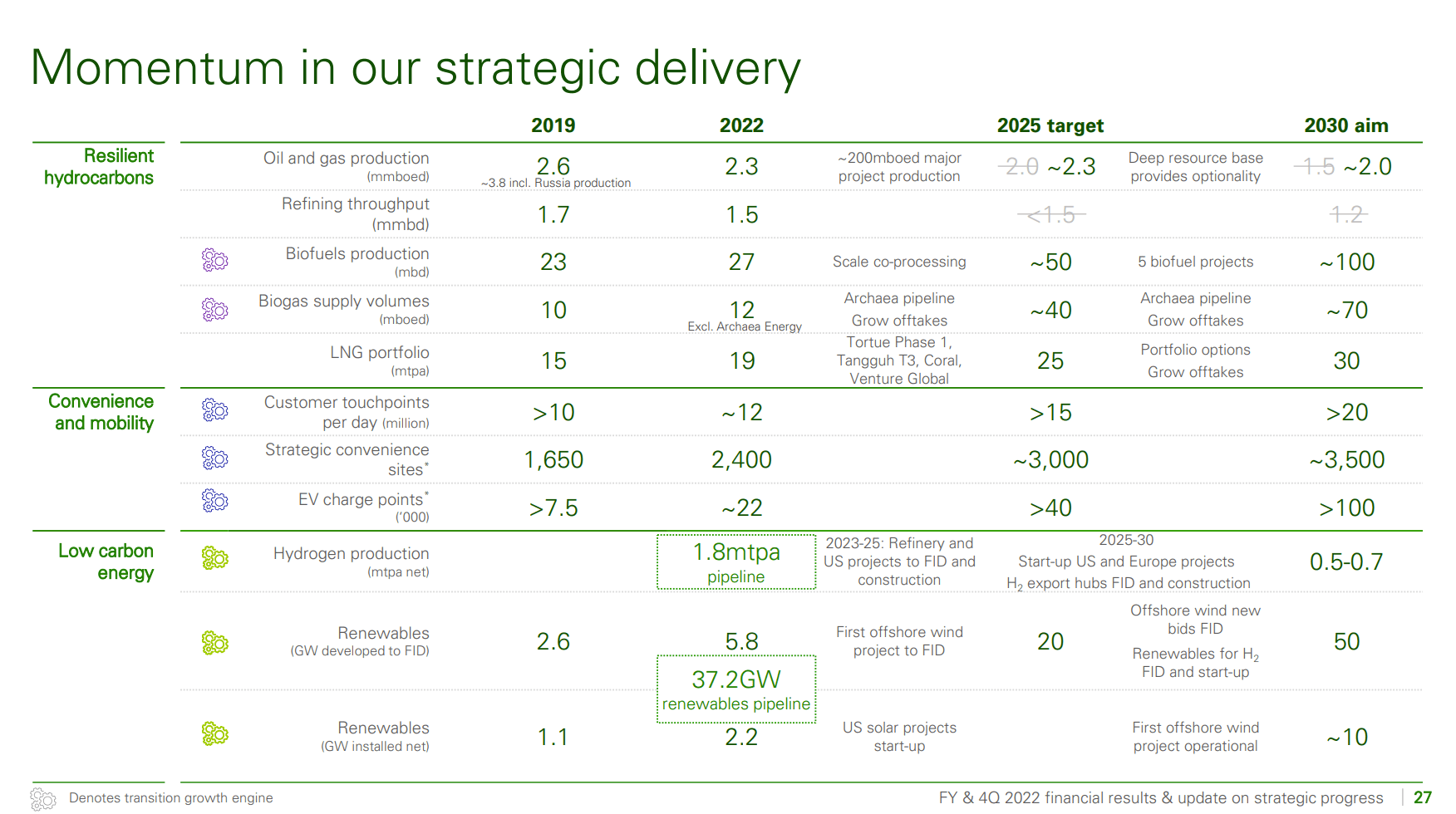

In the week prior to the earnings release, rumors began to circulate that BP would dial back parts of the company’s renewable energy strategy. I never expected management to put it in those terms. That would be Bad Politics. (OK, last one.) The increased commitment to the oil and gas business was refreshing to see, however. The company had been planning to reduce oil and gas production to 1500 mboe/d in 2030 from 2300 in 2022. With this latest strategic update, BP now plans to remain around 2300 mboe/d in 2025 and only cut to 2000 mboe/d by 2030. The company will increase spending $1 billion per year to bring on new production, offsetting base decline. Additionally, the company will slow its divestment plans, only selling off 200 mboe/d total through 2030. Further, the company has removed any reference to plans to cut refining throughput this decade. Finally, BP still plans to increase its LNG sales, hitting 30 mtpa in 2030, double 2019 levels.

BP

On the low carbon side, BP is also increasing its spending by $1 billion per year, but the latest strategy update puts more emphasis on higher-return projects. BP expects 15% returns on Biofuels and EV charging as well as double-digit returns on hydrogen investments. The company will be leveraging its refining assets by using them as sites for liquid biofuels and hydrogen projects, while the retail network of course fits in well with EV charging plans. Renewables such as wind and solar only have an expected return of 6-8% and BP appears to be de-emphasizing these except for what is already in the pipeline. Solar projects in particular now seem limited to the Lightsource BP joint venture, which is expected to be self-funding for any new investments.

BP

With the higher prices and added investments, BP now expects to earn between $51 and $56 billion EBITDA in 2030, about $10-$12 billion more than expected in the last version of the strategy. In the financial model below, I will show how this can be achieved and can produce a 14.6% annual return between now and 2030.

Financial Model

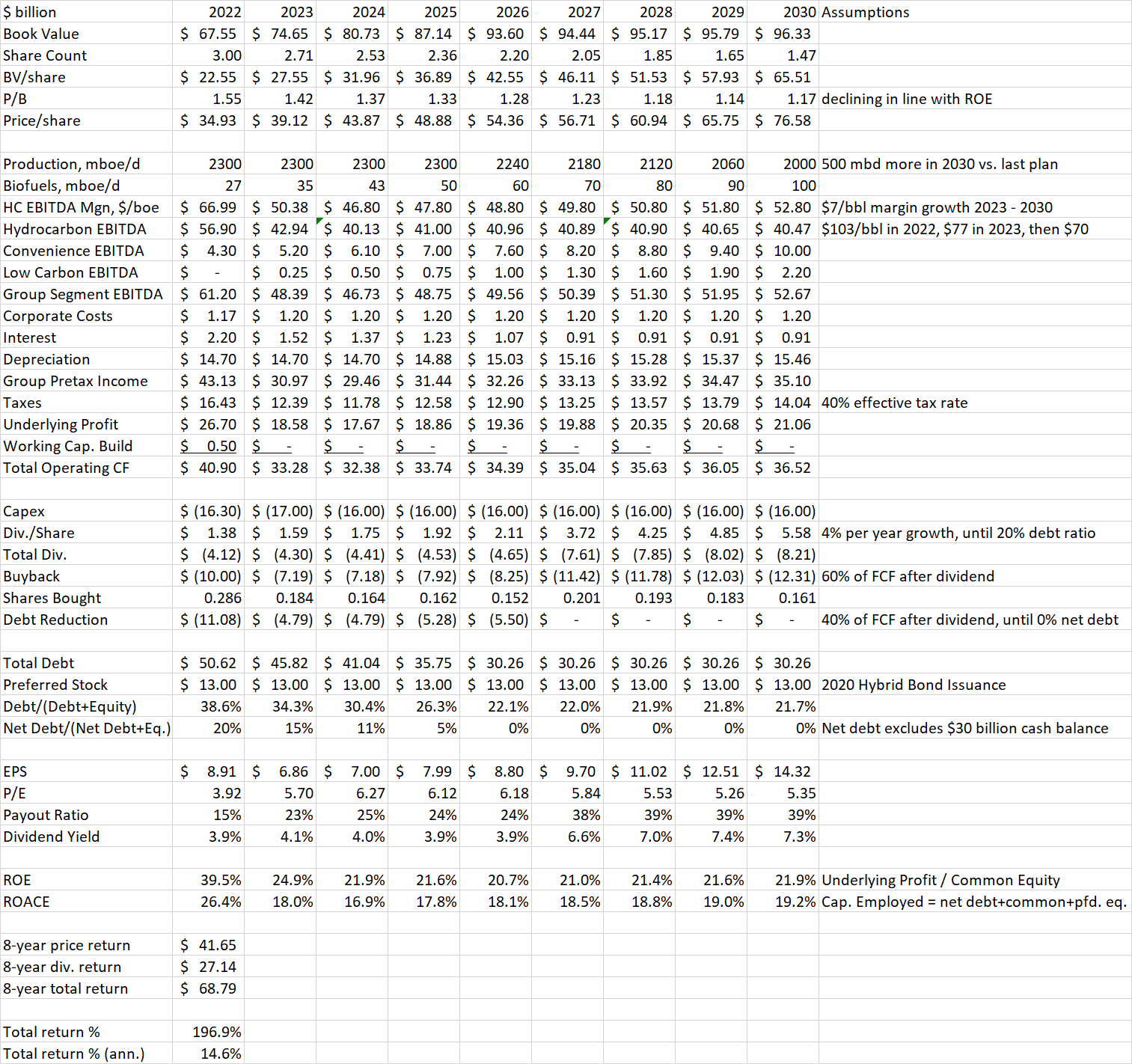

I have updated the model used in previous articles. The model looks at EBITDA from the three sources BP breaks out in its strategy slide – hydrocarbon production, convenience and mobility, and low carbon energy. For 2023, I am using BP’s stated assumption of $77/bbl Brent, switching to $70 for the remaining years out to 2030.

Hydrocarbon EBITDA/boe at a given crude price increases by the company’s forecasted 20% over the 2022-23 period. The values in the model reflect both this margin expansion as well as the changes in crude price. We see that hydrocarbon EBITDA holds steady around $40 billion/year between 2024 and 2030 as improving margins offset the declining production. Convenience and Low Carbon EBITDA are little changed from the last model.

The model then translates total EBITDA to operating cash flow and net income. Capex has been increased to $17 billion in 2023 and $16 billion per year between 2024 and 2030. Depreciation increases slightly every year starting in 2024 due to the increased asset base. Effective tax rate has been increased to 40% due to the removal of lower-tax Rosneft from the mix. Interest expense is assumed to be 3% of debt, which is calculated based on cash generation and debt payoff each year.

Because of the rapidly declining share count at this price set due to buybacks, I have increased the annual dividend raise assumption to 10% from 4%. This is in line with the actual dividend raise in 2023 vs. 2022. The declining share count allows the total dollars of dividends paid to grow less than 4% per year even as the dividend per share increases at 10%. Free cash flow after dividends is split 60% to buybacks and 40% to debt reduction until net debt/(net debt+equity) ratio gets to around 0%, which would happen in 2027. Net debt assumes the company keeps $30 billion of cash on the balance sheet, in line with the last two years. In 2028, 40% of FCF goes to dividends, resulting in a large step-up in the dividend.

The model calculates a book value for the company each year by adding net income minus dividends and buybacks. It also calculates a share count from the buyback value. Finally, I estimate a price/book value for the company correlated to return on equity levels. This allows the share price to be estimated.

Author Spreadsheet

The results show that BP stock price more than doubles by 2030 to $76.58/ADS, an improvement from my last model result. Dividends grow much faster than in my last model. Total return comes out to 14.6% per year annualized. Net debt ratio hitting zero in 2026 allows for a large bump in the dividend in 2027 which would vault it past its pre-pandemic rate of $2.52 annually.

BP still holds about 2.09 billion Rosneft (OTC:RNFTF) shares representing 19.75% of the company. They are restricted from selling these shares on the Moscow Stock Exchange. BP is also entitled to dividends paid in rubles that cannot be transferred out of Russia. Any future resolution to the Russia Ukraine war could produce an unexpected windfall for BP. For now, however, with the outcome impossible to predict, Rosneft and the dividends to which BP is entitled are valued at zero.

Conclusion

BP has recognized the value in maintaining hydrocarbon production and focusing renewable investments where they can earn a decent return. With the planned $70 oil price set and the slower scale-down of oil and gas assets, BP’s earnings power from hydrocarbons looks steady through 2030. Low carbon investments, especially biofuels, EV charging, and hydrogen provide the growth on top of this base across the rest of the decade. Lower-returning wind and solar are still part of the portfolio but are deemphasized.

Beyond 2030, the picture could change if BP decides to continue reducing oil production and implementing more lower-returning projects. This latest strategy update provides some reassurance that the company is responsive to economic signals if the demand for oil and gas is still there. Until then, BP should be able to deliver a total return of 14.6% per year from operations combined with aggressive buybacks and a growing dividend.

Be the first to comment