Introduction

The brutal selloff across the oil and gas industry following the combination of an OPEC oil price war and coronavirus pandemic has been very tough on BP (BP), with their share price more than halving in one month. The selloff has reached such a significant extent that their current share price now sits well below even the depths following their Gulf of Mexico oil spill disaster. Whilst their share price is almost certainly going to remain highly volatile for quite a while longer, the current share price offers investors a very attractive investment opportunity that still offers immense upside potential, even if their dividend payments are completely suspended for years.

Valuation Assumptions

The most important assumption underpinning the valuation is that they take the necessary decisions to ensure they can emerge on the other side of this oil price crash without having conducted any value destructive equity raisings. Given they entered this downturn with a safe but still elevated level of leverage as analysed in my previous article, it seems quite possible that they will be forced to reduce their dividend. Given their sheer will to sustain their dividend payments during the 2015-2016 oil price crash, I believe that they will only reduce their dividend payments as a last resort, especially since they are already discussing reducing capital expenditure.

The other main assumption was that the world continues to transition away from hydrocarbons in the same current path and thus provides decades for them to manage these changing times before it threatens their business model. Whilst they have already begun making investments to transition their earnings away from traditional hydrocarbons, these still require time to ramp up sufficiently.

Valuation Scenario

Due to the turmoil and uncertainties facing the oil and gas industry, along with the aforementioned short- to medium-term future of their cherished dividend payments, the goal was to ensure that any investment could be easily justified with very conservative future scenarios. The primary scenario envisioned is the most bearish one where this oil price cash lasts for approximately two years, with oil prices stuck firmly below $40 per barrel the entire time, before staging a slow recovery to average in the mid $50 per barrel range. This foresees their quarterly dividend being completely suspended for the next three years, before being half and then fully reinstated in the fourth and fifth years, respectively, after which it grows at 2.50% annually for ten years before remaining unchanged perpetually into the future. This provides a very conservative baseline valuation that many investors would consider the worst case scenario in the short term. The dividends are summarized in the table included below:

![]()

Image Source: Author.

Meanwhile, the secondary scenario provided a basic middle of the road scenario whereby oil prices recover within one year, although they still remain permanently subdued at the levels seen throughout most of 2017 through 2019. When this is combined with their push to deleverage, their quarterly dividend remains unchanged perpetually into the future at $0.63 per share or $2.52 per share on an annual basis.

Finally, the tertiary scenario is the most bullish scenario envisioned where oil prices recover to their 2017 through 2019 levels by the end of 2020. Due to this faster recovery, their leverage does not increase as significantly as the previous scenarios and thus they are able to provide more modest dividend increases. This scenario foresees their quarterly dividend remaining unchanged at $0.63 per share or $2.52 per share on an annual basis for the next three years, before growing at 2.50% annually for ten years and then remaining unchanged perpetually into the future. The dividends are summarized in the table included below:

![]()

Valuation Technique

The primary valuations used a standard discounted dividend model, with their cost of equity being estimated with the Capital Asset Pricing Model. Whilst this model is not perfect, it still provides enough accuracy for the purpose of this analysis. This model produced a cost of equity of 7.90% with the following inputs, a risk free rate of 1.16% (10 Year U.S. Treasury), a 60 month Beta of 1.05 (SA) and an expected market return of 7.50%. Meanwhile, the additional valuation consideration provides a relative valuation across several differing metrics that focus on different aspects and approaches.

Valuation Results

The primary valuation returned a result of $28.84, which is 69.65% higher than their current share price of $17.00 as of the time of writing. Meanwhile, the secondary valuation and tertiary valuation returned results of $31.90 and $36.99, respectively, which are 87.65% and 117.59% higher than their current share price as of the time of writing. These results all indicate that regardless of whether my bullish or bearish scenarios eventuate, their shareholders are still well positioned to see very attractive upside potential. To provide additional context, based upon this valuation approach, they would have to reduce their dividend by 46.70% to only $1.343 per share and never provide any increases again to justify their current share price. This seems highly unlikely to eventuate as they can structurally support their current dividend payments outside of crisis conditions, which further indicates that their shares are currently undervalued.

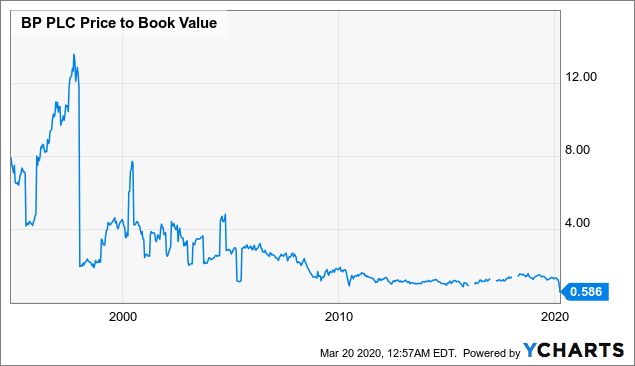

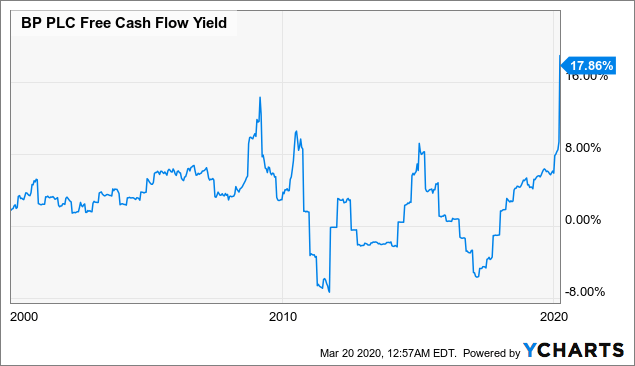

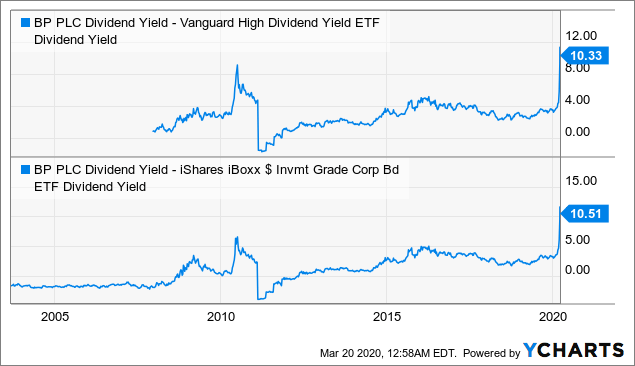

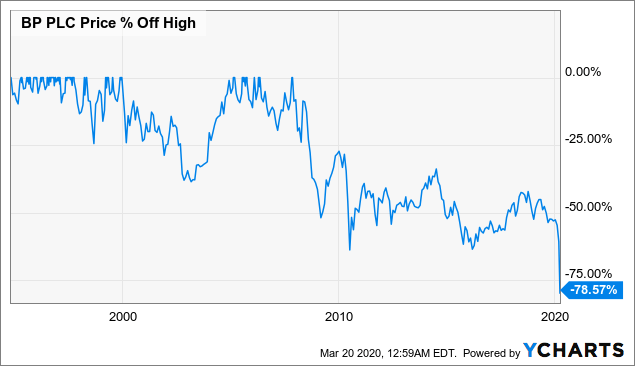

The additional valuation consideration provides further food for thought by simply comparing several relative valuation metrics. The first two graphs compare their current price to book ratio and free cash flow yield to that of their historical results. Meanwhile, the third graph compares the spread between their dividend yield and that of other alternative sources of income. All of these results clearly further indicate that their shares are currently the cheapest on the records that extend for decades into the past. The final graph clearly shows that this current crash has pushed their current drawdown to the largest since their ADRs listed decades ago in the 1990s.

Data by YCharts

Data by YCharts Data by YCharts

Data by YCharts Data by YCharts

Data by YCharts Data by YCharts

Data by YCharts

Additional Thoughts

Even though I find exploring different quantitative valuations quite interesting, when a situation such as this one eventuates, I believe that an investment can also be easily justified with a basic qualitative approach. I believe that an investor should consider their shares a very attractive investment opportunity at the moment if they answer yes to each of these three questions:

One – Do you believe that global economic activity will recover from this coronavirus crisis within the next three years?

Two – Do you believe that during this period of time, Brent oil prices will increase as the market rebalances and thus at least average around the mid-$50 per barrel range in the future?

Three – Do you believe that they will take the appropriate decisions to avoid any value destructive equity raisings and thus be capable of reinstating their current dividend in the future if temporarily suspended?

If an investor answered yes to all three of these questions, then their current share price offers a very attractive opportunity to lock in a yield on cost of almost 15% as of the time of writing. Even though it may be reduced or suspended in the coming year due to the turmoil currently rocking financial markets, it will one day be reinstated as there is nothing structurally wrong with their company.

Conclusion

Given the sheer value offered by their shares at the moment as well as the ease of justifying an investment, I believe that changing my rating from neutral to very bullish is appropriate. I believe that they will continue fighting to maintain their dividend for a while longer and possibly even make it through this latest crash without any reductions. Even if this does not eventuate and they are forced to completely suspend their dividend payments, they should still be reinstated in the coming years. Since I firmly stand behind this viewpoint, I have recently further increased my investment in their shares.

Disclosure: I am/we are long BP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment