Leon Neal

Article Thesis

BP (NYSE:BP)(OTCPK:BPAQF) reported its fourth quarter earnings results on Tuesday morning. While the company isn’t as growth-heavy as supermajor peers such as Exxon Mobil (XOM), BP still seems quite attractive. The company combines ongoing net debt reduction with substantial shareholder returns, which includes a just-announced dividend increase, and BP’s shares are pretty inexpensive today.

What Happened?

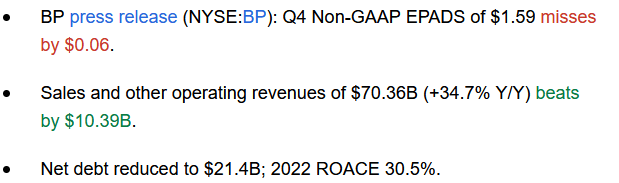

BP reported its Q4 results on Tuesday morning. The headline numbers, as reported by Seeking Alpha, include the following:

Seeking Alpha

The company was slightly less profitable than forecasted, but earnings per ADS nevertheless came in at a run rate level of ~$6.40. That’s highly compelling for a company that has an ADS price of just $35.

Revenue was up by more than one-third, as higher oil and gas prices helped boost sales. At the same time, higher volumes due to the recovery from the pandemic, which still had a more pronounced effect in late 2021, helped BP as well. Of course, higher revenues went hand in hand with some cost increases, as worker compensation grew, while all kinds of materials that BP needs to run its assets became more expensive as well due to the ongoing global inflation phenomenon. Last but not least, higher crude oil prices impact BP’s costs for its refining business, where crude oil is an input cost.

Nevertheless, underlying replacement cost profit, which is equal to adjusted net profit, rose by an attractive 18% year-over-year, to $4.8 billion, or more than $19 billion on an annualized level. Even better, BP’s earnings per share and earnings per ADS rose by 29% year-over-year. The discrepancy in the profit growth rate on a company-wide basis is explained by BP’s share repurchases, which have lowered the share count substantially, which resulted in a nice boost to its per-share and per-ADS profits.

Using Cash Flows To Shareholders’ Benefit

This buyback spending was the result of BP’s capital allocation strategy that pursues several ways to generate shareholder value. Since BP is generating vast cash flows and since it isn’t investing as much in new exploration and production compared to peers such as XOM, it makes sense for the company to have a logical strategy in place for how to use its free cash flows.

During the fourth quarter, BP generated operating cash flows of $13.6 billion. That’s not overly reflective of the general cash flow generation potential, however, as cash flows benefitted from working capital movements during the period, while working capital movements were a headwind in the previous quarter. During all of 2022, BP generated operating cash flows of $41 billion, or a little more than $10 billion per quarter, which seems like a better proxy for BP’s cash flow generation power in the foreseeable future versus the abnormally high level seen in Q4. The price for Brent crude oil was slightly higher at the beginning of 2023 versus the beginning of 2022, thus the two quarters could be more or less comparable. It is, of course, not guaranteed that 2023 will experience a mid-year oil price jump comparable to what we have seen in 2022, thus 2023 could be a worse year profit and cash flow wise overall. But even if profits and cash flows were to come in ~20% below last year’s level, that would still make for operating cash flows of $33 billion, or more than $8 billion per quarter.

BP spent $16 billion on capital expenditures last year for a free cash flow generation of $25 billion. BP has guided towards capital expenditures of $17 billion this year, including inorganic expenditures, i.e. M&A spending. This could result in free cash flows of around $16 billion in the scenario laid out above, where operating cash flows decline by 20% this year. If operating cash flows were to remain stable, the capital expenditure guidance implies that BP will generate free cash flows of $24 billion this year. BP is currently trading with a market capitalization of ~$100 billion — even a $16 billion free cash flow result for the current year would thus make for a pretty attractive mid-teens free cash flow yield. That is not available from Exxon Mobil and Chevron (CVX), as those are generating heavy free cash flows as well, but since they are trading at significantly higher valuations.

In 2022, BP has used its free cash flows for several purposes. First, the company used some of its available cash for reducing its debt position — the net debt load declined by $9 billion, from $30.6 billion to $21.4 billion. During the fourth quarter, BP’s net debt declined by $600 million. This made BP’s Gearing, which is calculated by dividing net debt by total equity, drop to 20.5%, down 480 base points year-over-year. With a net debt position of around $20 billion and a trailing twelve-month EBITDA of $61 billion, BP has a very solid balance sheet already, as its leverage ratio (net debt to EBITDA) stands at just 0.3. Still, the company plans to reduce its net debt further, which is not a bad idea as this has several advantages:

– At a constant enterprise value, lower net debt would translate into a higher market capitalization, one could thus say that net debt reduction moves value from debt holders to equity holders.

– Declining debt levels will translate into lower interest expenses, all else equal. This, in turn, will be beneficial for earnings and cash flows.

– Lower net debt levels make the company a less risky investment, as BP is better-prepared for any potential crisis the stronger its balance sheet is.

BP has stated that it seeks to use around 40% of this year’s surplus cash flows for net debt reduction. Surplus cash flows are defined as operating cash flows and proceeds from asset sales minus capital expenditures, dividends, and the portion of share repurchases that are needed to offset dilution. In 2022, surplus cash flows totaled $19.3 billion, or close to $5 billion per quarter. If we assume that operating cash flows will decline by 20% this year, as laid out above, surplus cash flow for 2023 would be around $11 billion, or $3 billion per quarter. If 40% of that is used for net debt reduction, BP would end the year with a net debt position of around $16 billion, versus $20.4 billion today.

And BP would still have $7 billion or so left over for share repurchases, as dividends are already accounted for in the surplus cash flow number. In other words, BP could buy back around 7% of its common shares this year even in a somewhat bearish scenario where lower oil prices result in a major 20% hit to its cash generation capacity. A 7% buyback pace would still be better than what is available from many other oil companies, however. It is important to note that BP has reduced its share count by 8.5% in 2022, using end-of-period numbers on December 31 of 2021 and 2022, respectively. Since another $2.75 billion in buybacks have been authorized for the current quarter alone (close to 3%), the 7% buyback estimate for the current year could turn out too conservative.

Looking at BP’s dividend, there’s some good news for shareholders as well: The company has hiked the payout by 10%, to $0.3966 per ADS, which pencils out to a dividend yield of 4.5% with BP trading at $35 (per ADS). That’s a higher yield compared to what is available from supermajor peers such as XOM or CVX, and yet, BP also offers a higher dividend growth rate. BP’s strategy of buying back shares in order to keep the per-share dividend growing while keeping the total dividend payment more or less flat has worked very well in 2022. Per-share dividends have been hiked by 10%, but on a company-wide basis, dividends have only grown by 1%, as the rest was offset by buybacks. If BP keeps buying back shares at a meaningful pace going forward, which seems likely, the company should be able to deliver sizeable dividend growth in the coming years as well, even while keeping the company-wide dividend more or less flat.

Takeaway

BP had a pretty solid quarter: Net debt declined, buybacks shrank the share count, cash flows were strong, and BP also hiked its dividend by an attractive 10%. Not everyone likes BP’s strategy of pursuing some green/renewable investments, but from what we see today, the company has not at all forgotten about its shareholders — they get a great shareholder yield.

Since BP is trading at a pretty low valuation — the forward EV/EBITDA multiple is just 2.8 — it’s definitely possible that BP will experience some multiple expansion tailwinds going forward, although that is not guaranteed, of course. Overall, BP looks very solid right here, and if oil prices remain stable or rise during 2023, BP could be a good investment. If oil prices were to fall substantially, e.g. when we get a deep recession (which seems unlikely to me), BP’s shares would likely fall, but that also holds true for its peers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment