The Good Brigade

Thesis

Boston Beer Company (NYSE:NYSE:SAM) is a stock that has disappointed investors and we believe the stock will continue to do so due to its weak position in the market and unfavorable financial performance. We believe that there are other stocks in the industry that would be better investments at this time.

Company Overview

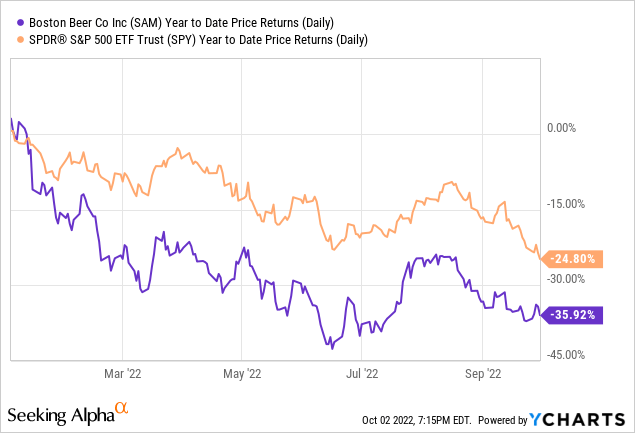

Boston Beer Company is a U.S. beverage company that sells numerous drinks, such as Samuel Adams, Rebel IPA, Angry Orchard, and Truly Hard Seltzer. In aggregate, Boston Beer Company has a production volume of 8.5 million barrels but in terms of brand prestige, the company is well behind bigger industry peers, as in 2021, the company ranked 9th place out of 50 brewing companies. This is well behind competitors such as Anheuser-Busch (BUD), Molson Coors (TAP), and Heineken (OTCQX:HEINY). Boston Beer Company has underperformed the market year-to-date, with a decline of -35.92% compared to S&P 500’s decline of -24.80%. The company as of the time of this writing has a market capitalization of $3.98 billion.

Weak Brands and High Competition

The competition in the beer market is fierce, and often times brand and marketing provides the competitive advantage for incumbents. In addition, recently there have been new companies and brands to compete with the incumbent players like Boston Beer Company, most notably seltzer brands like White Claw and various third-party craft beer brands. Such a shift in the market place shows changes in consumer preference away from traditional beers, and recent market movements by big players have been reflective of that. Boston Beer Company has launched Truly to compete against White Claw, and a host of other hard seltzer drinks launched by other beer companies. For traditional beer, Boston Beer Company is behind some of its competitors, and numerous rankings and surveys of beer brands show that Boston Beer Company brands are lagging behind other brands. For example, in this report from 2019, none of the 31 “top” beer brands in America listed a brand from the Boston Beer Company. Meanwhile, Molson Coors and Anheuser-Busch dominated the rankings, showing that these two companies had more popular and favorable brands compared to Boston Beer Company.

Boston Beer Co. Images

Unfavorable Performance

In the Q2 earnings release, one major concern we saw was the worse-than-expected decline in the Truly brand having a major impact on other key metrics, such as depletions. Management tried to sound upbeat by discussing the launch of new products like Twisted Tea and Hard Mountain Dew, but given the large size of the Truly brand in the portfolio, we believe the decline in that segment to be concerning. Overall, the company was able to increase its net revenue in Q2 at only a 2.2% clip, which is far below the YoY inflation and the 3 to 5% price increases during that same time frame. The deteriorating margins should be bad news for investors.

Limited Shareholder Value Return

Unlike other companies in the industry such as Molson Coors or Anheuser-Busch, Boston Beer Co. does not have many shareholder return programs. Boston Beer currently does not pay a dividend and has not bought back shares since 2018. As a result of the lack of these programs, we believe that the company’s stock price has a weak floor and can have major downsides if investors lose further confidence in the stock. Furthermore, given that competitors have had better history of shareholder returns through dividends and buybacks, we find that there are other stocks in the industry that can be more defensive in nature.

Unfavorable Peer Valuation

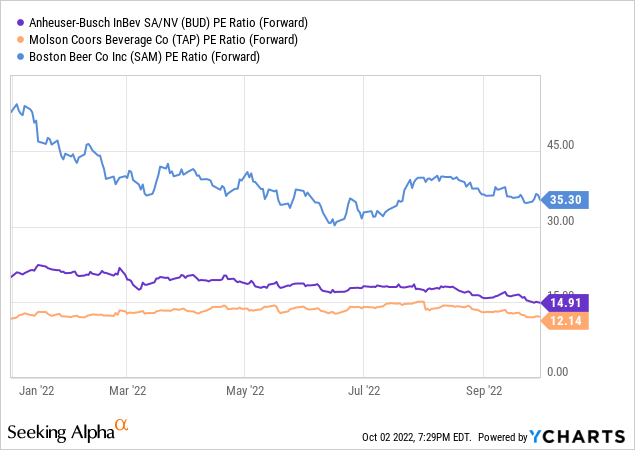

Boston Beer Company also has a high valuation when compared to some of its bigger peers. Currently, the company trades at a 35.30x forward P/E ratio, which is more than double the valuation of Anheuser-Busch and triple the valuation of Molson Coors Beverage Company. Given that the competitors have stronger brands, bigger scale, and good shareholder-friendly policies, we believe that Boston Beer Company’s valuation is very expensive at the moment. Furthermore, the company lowered its 2022 Non-GAAP EPS from a range of $11.00 to $16.00 to a range of $6.00 to $11.00 which is a significant reduction in guidance. We believe such a deterioration in guidance should be reflected in a lower earnings multiple to account for deteriorating business performance, and thus we believe that the current valuation is too expensive based on the fundamentals.

Risks

Downside Risks

Similar to other consumer discretionary companies, we believe that Boston Beer Company will be impacted by a drop in U.S. consumer sentiment and consumption. If the Federal Reserve continues to tighten monetary conditions and cause a steep recession, Boston Beer Company will see its sales and profits decline further. In addition, as yields rise, valuation multiples could be contracted further, especially for a high multiple stock like Boston Beer Company.

Upside Risks

We find the upside risks for the company to be limited as the short interest ratio is below the 10% threshold, and there doesn’t appear to be any indicators of oversold conditions based on valuation level. We believe that the stock price may change and valuation to expand if the company were to see a turnaround in its business performance in the next quarter.

Conclusion

Boston Beer Company is a stock that we believe should be avoided given the high valuations and the unfavorable market position against bigger incumbents and new brands/entrants in the market place. We believe such pressures are being shown through its financial performance, and as a result, unless the company starts to show signs of major financial growth as a result of changing consumer preferences or new product launches, we believe that the stock will not be a good investment for the foreseeable future.

Be the first to comment