pixelfit/E+ via Getty Images

In our previous article on Booking Holdings Inc. (NASDAQ:BKNG) and Airbnb (ABNB) just over a year ago, we estimated BKNG’s fair value at $2400. As time has passed and the BKNG stock has reached its target share price, it’s time to have a look at Booking Holdings Inc. again.

Booking Holdings performed better than expected

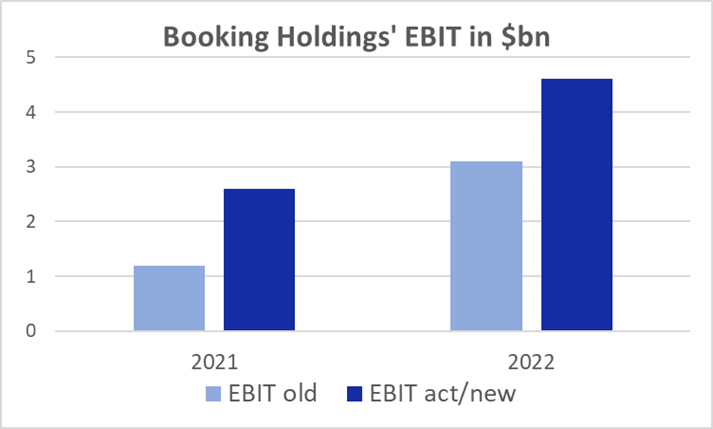

In hindsight, we were somewhat conservative in 2021 in the midst of the COVID-19 pandemic when estimating Bookings’ revenues and profitability resilience. The company has outperformed our forecast, both on revenues and on EBIT.

Booking Holdings Inc. is expected to deliver $16.9bn in 2022 (55% growth y-o-y) and 12% above its 2019 revenues, exceeding our original estimate of $15.6bn. The company has also delivered an impressive 24% EBIT margin in 2021 and almost 29% in 9M22.

In the chart below you can see our original estimates of Booking Holdings Inc. EBIT and actual numbers for the latest estimate.

Author, Booking Holdings Inc.

However, all of those additional profits were wiped out by the unusual items aka one-off expenses, which were booked below EBIT. Therefore, all in all, our estimates were pretty much on spot, especially given that investors are mostly interested in the free cash flow that the company generates.

For example, Booking’s EBIT margin including unusual items for 9M22 constituted 20.8%, in line with our 20% EBIT margin projection for 2022.

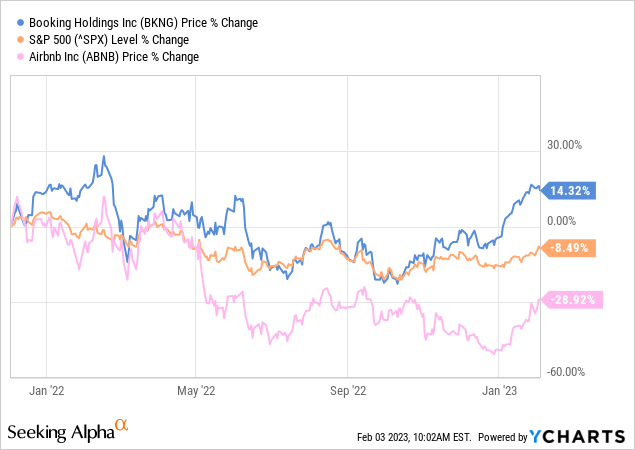

In terms of share price performance, in the time since our previous article BKNG shares outperformed the market by almost 23%, most of the share price surge coming from the past two months.

Steep share price performance in the past months causes some investors to be cautious, however, and we believe that BKNG shares still have some upside potential.

To watch: Booking Holdings Inc. FY2022 earnings release on Feb 23, after markets close.

Major Drivers Behind Booking’s Growth

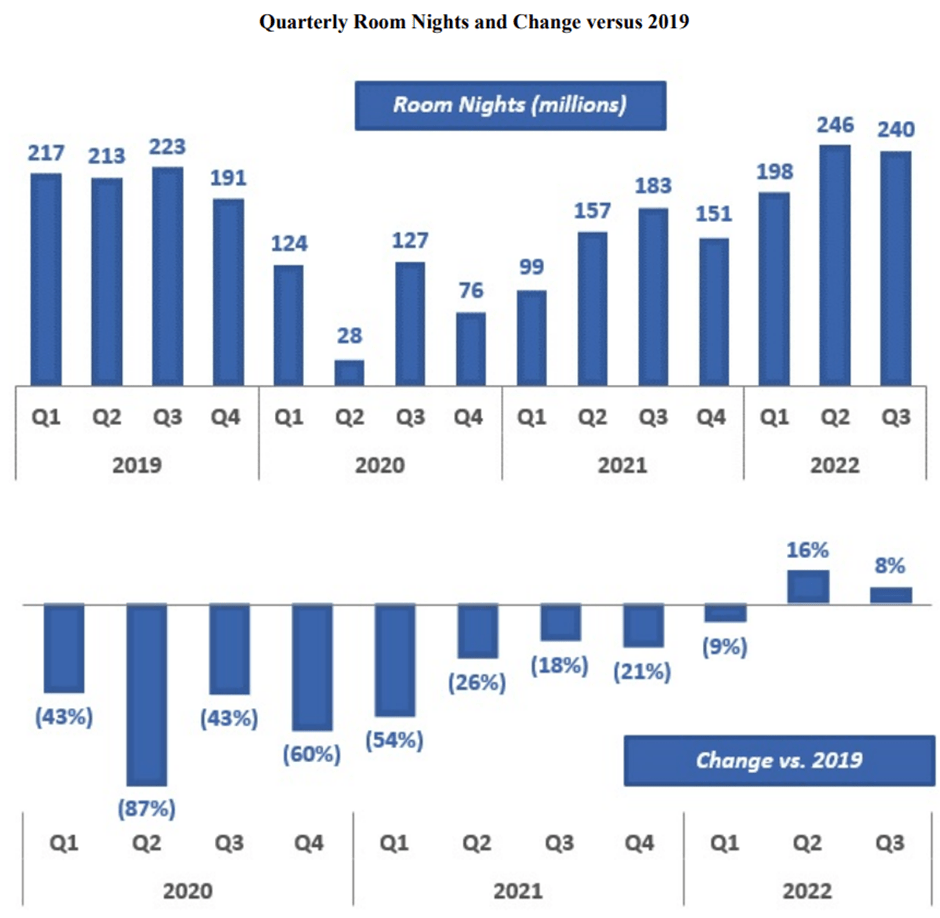

In 2022 Booking Holdings Inc. delivered excellent top line growth both in volume (room night growth) as well as ADR (average daily rate) in their two largest markets – the US and Europe.

You can see in the chart below how the room nights volume recovered in the second half of 2022, exceeding 2019 in Q2 and Q3.

Booking Holdings Inc.

The company so far has not seen any indication that customers move to cheaper accommodation or reduce their length of stay – typical signs of recession. Moreover, according to the management, hoteliers succeed in passing on inflationary pressures onto customers.

Booking Holdings management also shared optimistic news about bookings for the Q1 2023, which should exceed the figures at the end of 2019 for the Q1 2020.

In the medium-term, the company’s management implemented several initiatives to ensure top line and bottom line growth:

- Integrating payments platform – it gave the company an increased ability to merchandize, while reducing friction with customers;

- Developed connected trip – included flights and other services, which can be booked on the platform;

- Increased alternative accommodation inventory.

The payments platform is expected to be break even in 2022 and deliver some profit contribution starting from 2023. As for the flights, according to David Goulden, Booking Holdings’ CFO, in a steady state this business segment would deliver only mid-single-digit EBITDA (in contrast to 30%+ EBITDA in accommodation business). Therefore, despite optimistic revenue growth projections, Booking’s EBIT growth is expected to lag behind, due to lower profitability of new businesses.

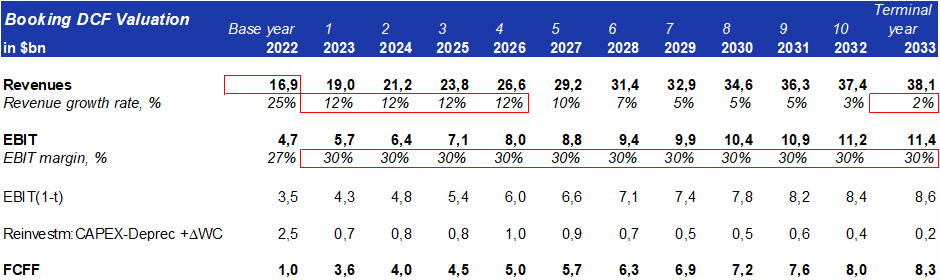

Booking Holdings Inc. DCF Model Update

Revenue growth: prior to the COVID-19 pandemic, Booking Holdings revenue growth has slowed down to low single digits. The company’s management used the past three years to develop new business areas such as integrating payments and offering flights to spur top line revenue growth. Therefore, we remain confident in the projected double-digit growth in the several years, gradually slowing down to 2% terminal growth rate.

EBIT margin: Booking’s fast recovery from COVID-19 travel restrictions as well as historical 35% EBIT margin gives us confidence that the company is able to achieve 30% EBIT margin going forward. The margin is somewhat lower to reflect margin compression from new businesses.

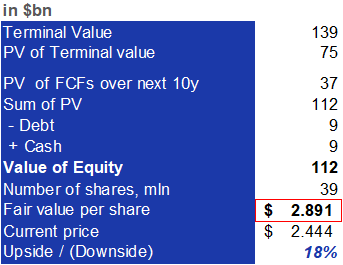

Author

Discount rate: This is the major change in our DCF model (and investor expectations) in the past two years. Now investors can achieve 3.4% return by merely buying 10-year US Treasury bonds, therefore, investing in stock market has to bring at least 5.11% on top (depending on the riskiness or beta of the company).

In our previous DCF model for BKNG we used a discount rate of 6.5%. Now we adjust it to 8% and come up with an estimated fair value of $2900, which suggests 18% upside to the current share price.

Author

Relative Valuation

BKNG is the only company among its peers that enjoys BUY rating from Quant, SA Authors and Wall Street.

Seeking Alpha

When it comes to the P/E ratio, BKNG is one of the cheapest among its peers, second only to Expedia (EXPE). However, the forward P/E of almost 25x is by no means cheap for a maturing company.

Seeking Alpha

Conclusion

Booking Holdings demonstrated strong recovery after the travel restrictions were lifted. The company has defined new ways to grow, which, in the long-term could cause some margin compression.

Our updated valuation of BKNG shares suggests a target price of $2900, offering 18% upside potential to the current share price.

To watch: Booking Holdings Inc. earnings release on Feb 23, after markets close.

Be the first to comment