Stephen Brashear/Getty Images News

Boeing (NYSE:BA) reported its fourth quarter and full year 2022 results on Wednesday before the opening bell. In response to the earnings release, shares trade down 3.3% in pre-market trading. Previously, I provided an earnings preview for Boeing’s fourth quarter results. In my view, the analyst estimates were on the high side and after the significant run up in Boeing’s stock prices by the end of 2022 that could create a scenario in which some profit taking could occur. In this report, I will be analyzing the results as well as any guidance and comment that management has provided.

Boeing Earnings Fall Short

As I pointed out, the estimates for Boeing were extremely high both on top and bottom line. Analysts were expecting earnings per share of $0.29 and revenues of $19.88 billion and the whisper numbers were $20 billion for revenues and $0.56 in core earnings per share. Boeing ended up reporting $19.98 billion in revenues which was higher than the $19.88 billion estimated though Seeking Alpha reports the consensus revenue estimate at $20.1 billion indicating a $120 million shortfall. Earnings per share were -$1.75 indicating that earnings well short by $1.95 to $2.04 per share.

Interesting to note is that while I already noted that expectations were too high, even the significantly lower expectations that I had were too high. Ideally, when making projections on earnings you hope you’re right and that’s not the case this time. Still, there’s a lot of value in coming up with earnings previews and estimates. On this platform as well as outside of this platform, I’m the only one who does not just provide revenue and earnings estimates but I show how my estimates are put together. So, I provide much deeper insights than other platforms or parties do and that provides readers with deeper insights for a company as complex as Boeing. This also allows me to assess where Boeing meets, exceeds or in this case fell short of expectations which I will do in this report.

My median estimate was $19.8 billion and earnings of $0.08 (out of a range of -0.08 to $0.23), so when assessing the difference I will be using the median estimate even though the low-end of my estimates is much close to what Boeing reported.

Boeing Results: Falling Short In Each Segment

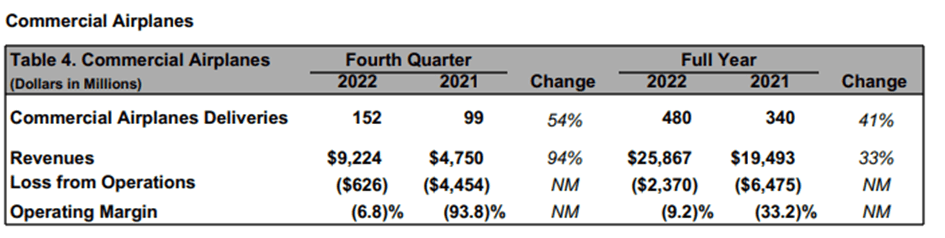

Boeing

Boeing reported revenues of $9.2 billion, whereas I anticipated revenues of $9.5 billion that provides a significant difference but it should be kept in mind that actual sales prices are public so even a thing seemingly as simple as estimating revenues can be difficult. When revisiting the delivery numbers for the quarter, it seems that Boeing 787 revenues were 10% lower than anticipated which could be related to customer compensations.

Boeing realized a loss of $626 million which was $176 million higher than our most positive scenario and around $120 million worse than our low-end estimate. Boeing cited abnormal production costs and R&D for the 6.8% loss margin. Boeing’s 10Q which is not immediately available should provide us with some insight on where the differences were caused. If those costs were in line with what I had modeled, there could be a bigger issue for Boeing namely accounting profits on the Boeing 737 MAX being 3.25 percentage points lower than modeled which is something that would carry forward. From what I can see now, the abnormal production costs for the Boeing 787 were higher than modeled.

Either way, the steeper loss at BCA already accounts for $0.25 out of the $1.83 shortfall either driven by program margins or period expenses. In its earnings release, Boeing reaffirmed plans to increase production to 50 aircraft per month for the Boeing 737 MAX by 2025-2026 and on the Boeing 787 production is going up to five per month by the end of this year, a bit later than earlier expected, and eventually toward 10 aircraft per month. So, while Q4 loss at BCA was a bit steeper than anticipated, the production rate increase planning remains intact.

On China, it seems that Boeing paused the remarketing effort as there seems to be some progress in getting the MAX back in the air in China. The wording during the call was not completely clear, but it was suggested it takes six months to get the aircraft in China back in the air and from there, there could be opportunities to deliver new aircraft.

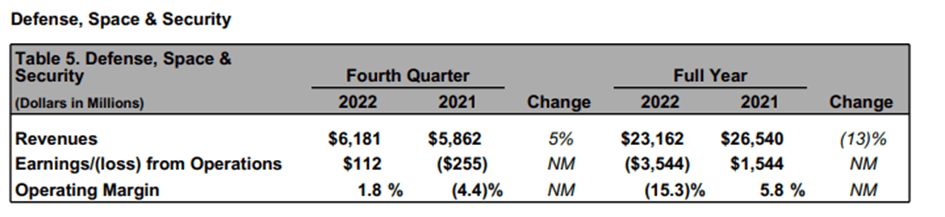

Boeing

Where Boeing really did disappoint is Defense, Space & Security. It hardly should come as a surprise by now that this segment fails quarter after quarter. I had revenues modeled at $6.0 billion meaning that Boeing beat expectations by $181 million. However, segment profits estimated at $600 million did not compare favorably to the $112 million that Boeing reported. Boeing cited continued operational impact of labour instability and supply chain disruption as a reason for the poor results. However, at this point it is more important for the company to provide some insights in whether this is a low single-digit margin business going forward or a 10% margin business any time soon. I had modeled margins at 10% which was way too ambitious causing a $0.70 shortfall in earnings per share. Boeing did share that sequentially things should improve but that something that will likely take a while so, I’d think that this year BDS is more a 3% margin business rather than a >10% margin business. So, half of the shortfall can already be explained by performance at the commercial aircraft unit as well as the defense unit.

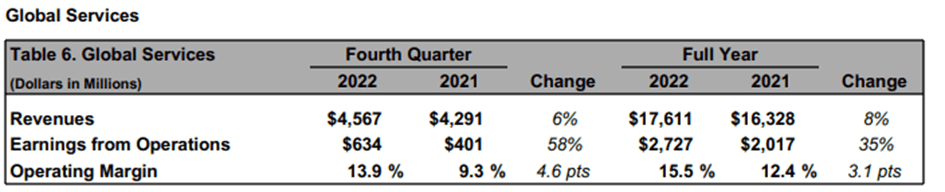

Boeing

Services revenues beat my expectations at the mid-point by $317 million but its margins fell short by a percentage point leading to earnings in line with expectations. So, nothing noteworthy there.

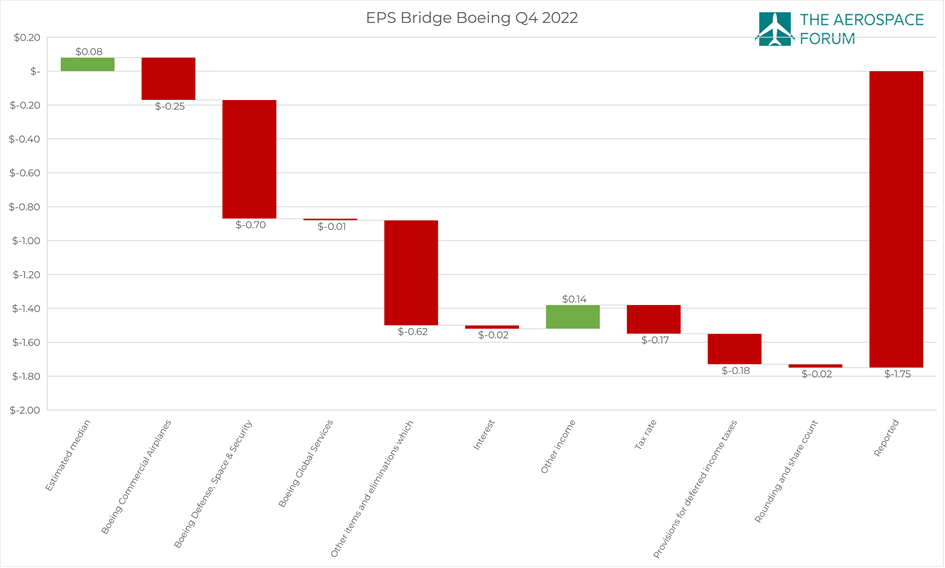

Overall, the operational shortfall was more or less contained within BCA and BDS accounting for $0.95 cents of the $1.75 shortfall and $0.01 for BGS. Boeing Capital Corporation earnings were in line with expectations. So, there still is a $0.80 shortfall in earnings per share that needs to be explained. The bulk of the shortfall comes from other items and eliminations which came in at $785 million while $345 million was estimated driven $0.62 of the shortfall while FAS/CAS service adjustments were $12 million higher than anticipated and another $0.02 per share came from higher interest expenses. Other income was higher than expected providing a $0.14 tailwind while the effective tax rate provided a $0.17 cent headwind plus $0.18 cents higher adjustments to translate GAAP to core earnings per share driven by provisions for deferred income taxes.

EPS Bridge (Boeing)

The big advantage of making your own model is that you can assess where the differences compared to the estimates occur and what we see is that basically all operational segments performed worse than expected while other items such as eliminations and provisions were also higher. Overall, it was not a pretty quarter from earnings perspective.

Liquidity and Outlook Are Good

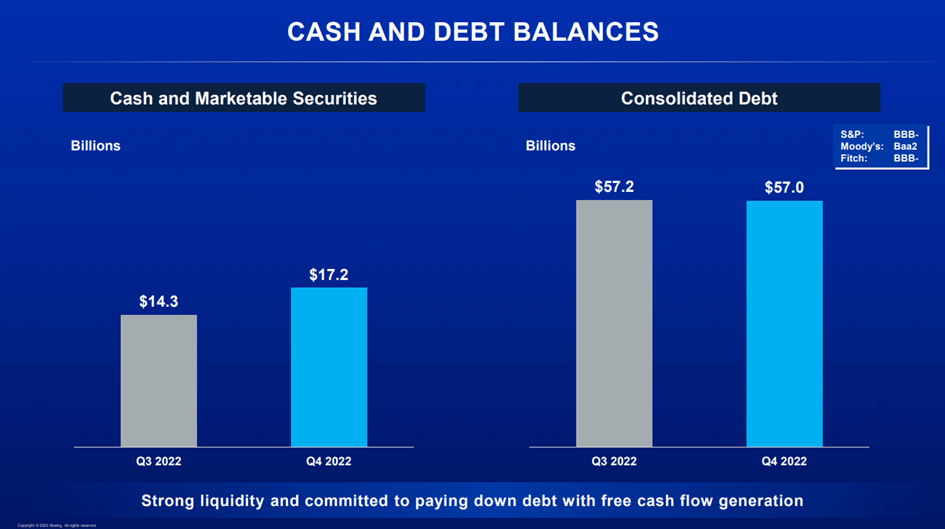

Cash and debt balances (Boeing)

While earnings are important, I believe looking at free cash flow provides more value at times because some charges impacting earnings are non-cash items and some programs do generate cash which is not reflected in the earnings statements. During the quarter operating free cash flow WAS $3.5 billion which is a $2,741 billion improvement year-over-year while free cash flow was $3.131 billion or a $2.637 billion improvement. With that free cash flow came in higher than earlier guided. Consolidated debt remained flat which is not extremely surprising given that the cash generation for Boeing happened in the second half of the year and the first quarter of the year tends to be the lowest for cash flow. So, directly applying positive free cash flow to reduce debt is not the most prudent thing to do but eventually the cash will be used for that purpose. We also saw the cash position increase by roughly $3 billion, meaning that Boeing’s net debt position did improve and we just have to wait until they use that cash to start burning that debt down. The net debt position improved to $39.8 billion from $42.9 billion in the previous quarter. Compared to the start of the year, Boeing’s net debt went up but that is driven by the cash burn in the first half of the year.

For 2023, Boeing guided for free cash flow of $3 billion to $5 billion and I believe that the company should be aiming for the higher end of that range or else it’s a somewhat soft year-over-year improvement in absolute terms. The first quarter is naturally the weakest quarter of the month and as a result the company expects to produce a loss during the quarter and burn cash. Furthermore the company expects cash burn at BDS to continue while services and commercial aircraft will be providing the bulk of the cash driven by continued services strength, 400-450 Boeing 737 MAX deliveries and 70 to 80 Dreamliner deliveries. In that regard we don’t see anything that Boeing did not tell us in November during the Investor Day.

Conclusion: Mixed Results, Outlook Good

As I’m wrapping up this report shares of Boeing are trading down 1% and I would say that is a pretty timid market reaction as I had expected that investors would be taking profits on an earnings miss. The fact that the stock is trading down by a percent indicates that there is some profit taking but nothing spectacular and maybe that is how you can describe Boeing’s Q4 earnings: Not spectacular, while the upside for Boeing Commercial Airplanes remains.

Be the first to comment