Wirestock/iStock Editorial via Getty Images

Years ago, The Boeing Company (NYSE:BA) was the market darling. The company could do nothing wrong, or, well, it seemed that way. Following two crises with the Boeing 737 MAX and Boeing 787, and ongoing problems on other programs, things obviously look completely different for Boeing. Nevertheless, shares of Boeing have had a nice run higher, and in this report, I want to discuss why.

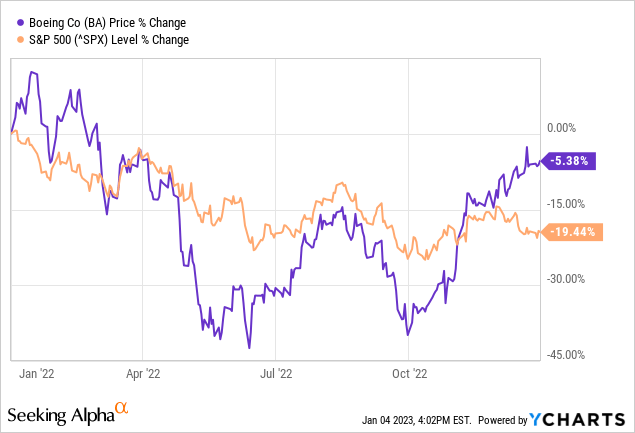

Boeing Stock Lost In 2022

One thing to keep in mind is something that a lot of people might not be aware of, and that is that even though there has been a lot of bullish momentum for Boeing lately, the stock actually lost altitude in 2022. In 2022, Boeing stock lost 5.4% of its value. Is that bad? Maybe it is. That really depends on your expectations for Boeing in 2022. However, we do see that the broader markets were down 19.4%. So, I would say that Boeing shedding some of its value was not completely unexpected.

Why Boeing Stock Lost Value

So, the market was down in 2022 just like Boeing, which partially indicates that some of the factors driving down Boeing’s share prices are the same factors that drove down the stock market.

Those factors are really the common themes in 2022, namely:

- Inflation

- Labor costs

- Supply chain issues

- Recession

- Geopolitical tension.

The big fear in 2022 has been inflation driven by higher energy costs exacerbated by supply chain issues. The result is that day-to-day living has become more expensive, which puts pressure on consumer spending and that of course sparks concerns on the health of the economy with a recession as a possible outcome. The Fed started hiking interest rates to battle inflation, which does not do anything good for consumer and business spending. For the stock market, it also means that investing in it became a bit less appealing.

We see the same things hurting Boeing, even though together with airlines they have not observed softening in demand for air travel and aircraft. In fact, demand for commercial aircraft is higher than it has been in the past years, but that didn’t materialize fully, particularly due to supply chain issues that Boeing experiences down the chain and which gives them an extremely difficult time stabilizing production rates. There also is the angle of geopolitical tension,

The aforementioned factors are some that are applicable to many companies today, not just to aerospace companies or corporations but also to small businesses. There also is a set of elements specific to Boeing that drove down its share prices in 2022. Boeing started last year announcing a multi-billion dollar write-off on the Dreamliner program. It was not a huge surprise, as I had been anticipating this since 2021, but obviously this put pressure on Boeing share price performance.

Boeing

The bigger pressure to the stock came in April, as Boeing disclosed that it no longer was aiming for 500 deliveries in the year because the Chinese market remained closed for the Boeing 737 MAX, meaning that a significant unwind in inventories that was expected would not materialize. Furthermore, Boeing 777X costs would grow by another $1.5 billion as the program was further delayed and the company decided to halt production. Along with that, the non-performance of Boeing’s defense unit became painfully clear as fixed-price contracts started to bite Boeing back:

- Costs on the VC-25B (Presidential Aircraft) program grew by $660 million.

- Costs on the T-7A Red Hawk trainer jet grew by $367 million.

- Costs on the KC-46A program grew another $165 million.

- Costs on the MQ-25 tanker drone grew by $78 million.

The cost growth on those defense programs showed the risk infusion of those contracts that Boeing won years ago, but are now not returning value to the business due to a combination of ongoing delays and the high-cost environment.

The disappointing results on commercial programs as well as defense programs made investors question whether 2022 was the year of the big Boeing turnaround as they had hoped for.

For the second quarter, things did not get better for Boeing. Deliveries on the Boeing 737 MAX program remained underwhelming, and an anticipated rate increase to 38 Boeing 737 MAX aircraft per month got out of sight due to engine shortages driven by shortages of forging technologies required for the engines. This was partially driven by the situation with Russia, and the number of expected Boeing 737 MAX deliveries was brought down to 400. Cost growth on the defense programs also continued, with a significant cost addition of $2.8 billion in a major de-risk move on the defense platforms.

So, in terms of performance, there was extremely little to cheer about for the majority of 2022. Measuring performance from the day before one earnings date to the other, Boeing shares lost 18.2% from the Q4 2021 release to the Q1 2022 release, and another 6.7% in line with market performance from the Q1 2022 release to the Q2 2022 release and 6% from Q2 to Q3.

So, Boeing’s stock from earnings to earnings did not do great, and it was clear why. Defense programs attracted billions of dollars in cost growth and commercial aircraft program were generally trending up, but with some delays on recovery and cost growth on the wide body programs.

Boeing Stock Price Booms

From its lows by the end of September, shares of Boeing rose strongly, with a 57.3% gain compared to a 7% gain for the stock markets. You could wonder why that is the case, since the financial results did not give much reason to be upbeat about Boeing. In terms of the financials, there was one huge plus, and that was the cash flow which hit $2.9 billion in the third quarter. Boeing would expand its gain on further projections for its free cash flow in later years.

What marked a big reversal for Boeing was the fact that the company decided to remarket some aircraft initially built for China. Boeing has been waiting for years now to get those aircraft delivered to China, but geopolitical tensions and the COVID-19 situation in China delayed or even halted any significant progress to reintroduce the MAX in China. Boeing ultimately ran out of patience and started remarketing the jets, which sent a strong message to China. It also showed how strong the demand environment for jets actually is, which puts more confidence in Boeing’s ability to price the aircraft right. Who will eventually “win” this strongarming battle remains to be seen, but Boeing made a bold move to send a message to China which could count on support from investors.

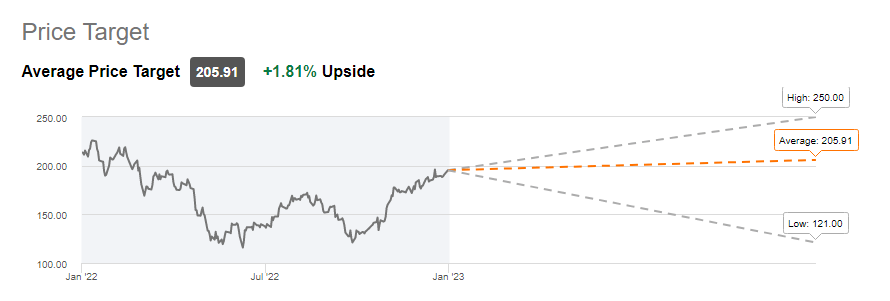

Wall Street price target Boeing (Seeking Alpa)

Furthermore, the plan that Boeing presented during its Investor Day was promising and followed by a necessary reorganization of the Defense segment. For the full year 2022, Boeing expects to be cash flow positive, with up to $2 billion in cash generated and $3 billion to $5 billion in 2023 with projections of returning to $10 billion in free cash flow by 2025-2026. For me, that was reason enough to put a $240 price target on Boeing’s shares granted they are able to execute on their projections. With a share price projection of $240, my projection is significantly higher than what Wall Street analysts are expecting, but I also have to note that since I marked shares of Boeing a buy in May 2022, the stock has surged over 60%.

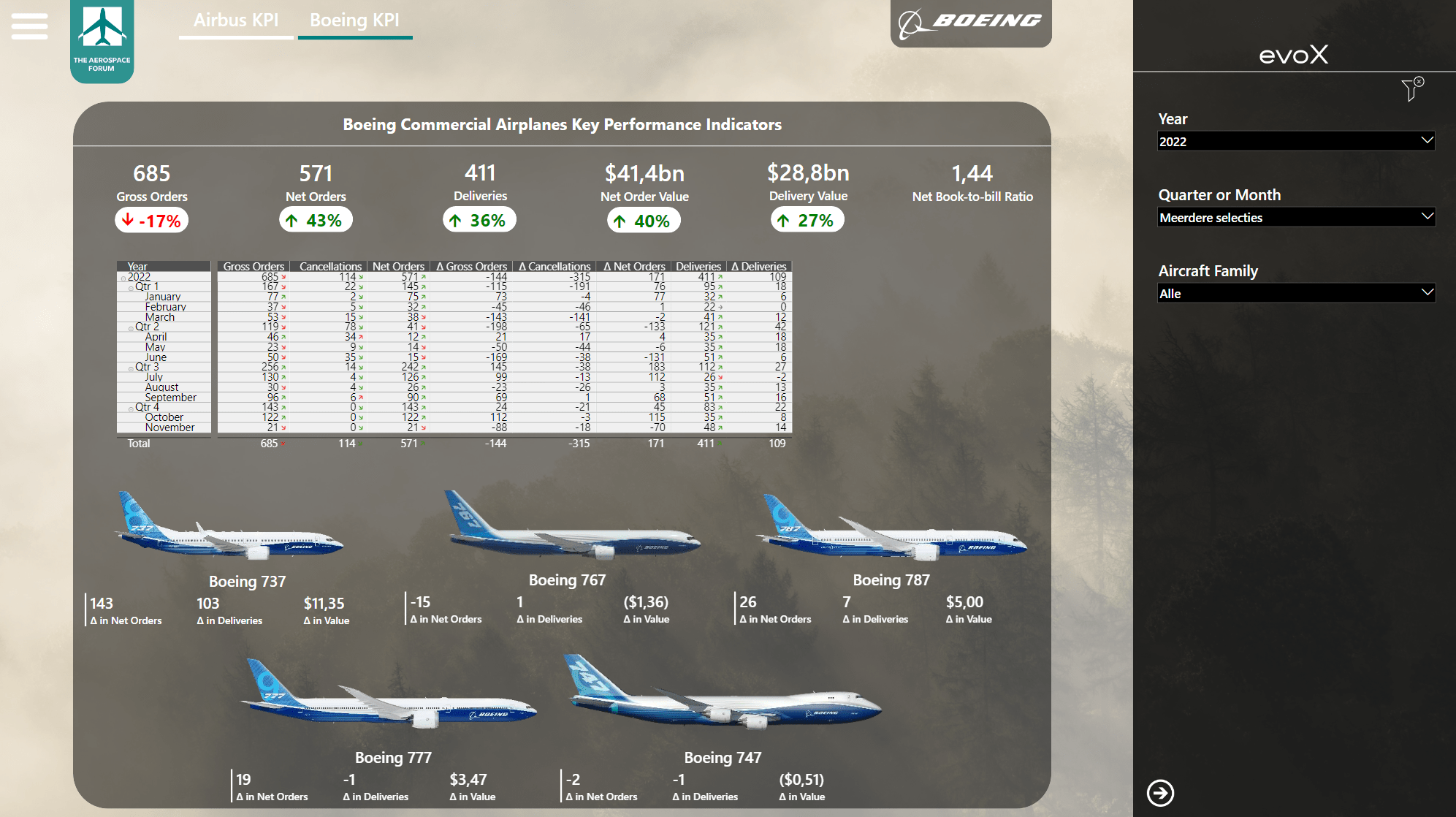

Boeing KPI Commercial Aircraft (The Aerospace Forum)

So, we have most definitely seen some bad elements, primarily in Defense, wide body cost pressures, and a slow MAX recovery. However, the fact remains that with the MAX and Boeing 787 back in the game, things are developing in positive directions. We don’t have the data from Boeing yet for December, but looking at the January-November period we see that things have materially improved for Boeing. Gross orders are down 17% and with demand being higher than in the years before you could wonder why. The reason is that last year we saw a lot of cancellations, which were than offset by the same company placing a new order. So, it was really a zero-sum game that boosted gross orders.

A better metric to look at is the net orders, which are up 43%. United Airlines’ agreement for up to 300 aircraft is not part of this overview, since the announcement occurred in December, but it is one of the orders that also showed the continued appetite for Boeing 737 MAX and Boeing 787 aircraft. This proved the doomsayers on Boeing’s key programs wrong. In line with net orders being up, the net order value is up 40% while deliveries are up 36%, while delivery value is up 27%. So, we most definitely are seeing what is supporting the major improvement in cash flows, and in 2023 we should see the full-year effect of that.

Conclusion: Boeing Is A Buy Even Without It Firing On All Cylinders

I continue to believe that The Boeing Company is a buy even if it is not firing on all cylinders. The recovery in MAX deliveries is rather slow, and Defense programs have provided a drag on earnings and cash flow, and that will be the case for 2023 as well. However, even with that in place, the improvement that we do see and should be seeing on an annualized scale this year should propel The Boeing Company stock price even higher, even after the big 60% surge we saw in late 2022.

Be the first to comment