Scott Olson

The Boeing Company (NYSE:BA) has been defying gravity as the leading aircraft manufacturer’s YTD total return has continued to outperform the S&P 500 (SPY).

BA has recovered remarkably from its September bottom, as astute investors positioned for peak pessimism, even as Boeing faced delays in meeting its deliveries. We updated investors in our previous articles in June and September, encouraging BA investors to ignore the noise and add confidently.

Accordingly, BA rallied nearly 60% through its December highs as investors acclaimed its order book visibility, despite near-term supply chain challenges and inflation headwinds.

With China’s reopening expected to boost outbound travel further, airlines are likely preparing for the robust return of international travel.

Notably, Emirates intends to resume the entire operations of its A380 jets by the end of 2023. In addition, the company indicated in November that it sees the potential for a “tsunami” of bookings from China once its COVID curbs are curtailed.

Therefore, we believe investors who picked BA’s lows in September likely anticipated the potential reopening of China’s economy as the government downgraded its COVID threat status. As such, China has taken a decisive step toward reintegrating with the world.

Notably, it has also lifted quarantine requirements for travelers and also shut down its most stringent requirements that limited aircraft passenger capacity.

Hence, the forward outlook bodes well for Boeing, coupled with the significant shortages of planes due to the rapid recovery in travel demand and fleet replacement. As such, the leading aircraft manufacturers have order book visibility through 2029.

However, the critical issue has always been about timely deliveries, as the recent delivery miss by Airbus (OTCPK:EADSF) demonstrated. Investors should be reminded that a record order book doesn’t necessarily translate to robust delivery execution. Furthermore, “most cash is paid only when planes are delivered.”

As such, we believe the market will likely focus on Boeing’s execution through 2025, as several significant challenges remain unresolved. The global macroeconomic outlook has worsened markedly as we move increasingly close to the most well-telegraphed recession in recent times.

However, we believe BA’s June and September lows have likely contemplated the significant macro headwinds. Hence, investors could be paying more attention to the certification issues of its 737 Max jets.

Importantly, the company recently won a reprieve from lawmakers that exempted Boeing from “a new cockpit requirement” that would have taken effect this week. As such, it has averted a costly redesign that would have exacerbated its certification delay woes.

However, BA hardly moved over the past week, suggesting that the market isn’t too focused on this matter for now.

Hence, we believe the critical driver for a further re-rating would be when Chinese regulators allow Boeing’s 737 Max to return to its skies. Citi telegraphed its optimism in a recent note, suggesting that the Chinese regulators would certify its successful return.

Notwithstanding, the critical question is whether investors’ recent optimism has been baked in, as it snagged a massive order from United Airlines (UAL), to bolster its fleet with 100 Boeing 787 Dreamliners and 100 Boeing 737 Max jets. Hence, UAL and its peers are lifting their optimism in the recovery of international travel, corroborated by the lifting of China’s COVID-zero curbs.

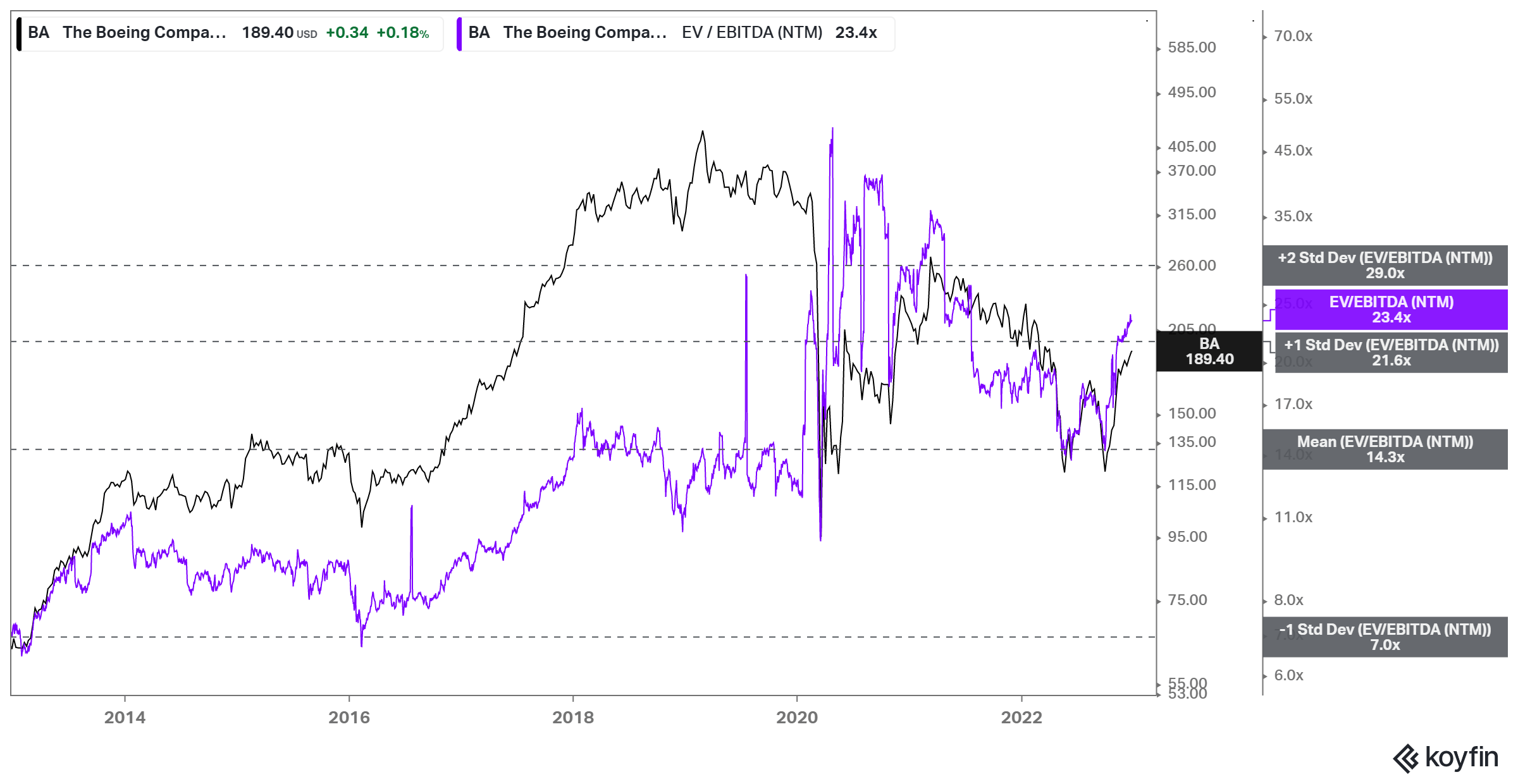

BA NTM EBITDA multiples valuation trend (koyfin)

BA last traded at an NTM EBITDA multiple of 23.4x, well above its 10Y average of 14.3x. It’s also above its peers’ median of 12.4x (according to S&P Cap IQ data).

Hence, it’s pretty clear that the market has likely reflected optimism on Boeing’s earnings projections over the next few years, as it is expected to continue its recovery momentum.

While BA remains nearly 20% below its January highs, investors need to be wary about expecting further upside. We believe BA’s implied FY25 EBITDA multiple of 15.1x at its January highs suggests limited upside from the current levels over the next few years.

Notwithstanding, we gleaned that sellers have not returned in earnest as we previously anticipated. Consequently, BA could continue to consolidate further, even though the medium-term upside is expected to be limited at these levels. Hence, we assessed it more appropriate to move to the sidelines from here.

Rating: Revise to Hold (Previous: Sell)

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment