Central Bank Watch Overview:

- Rate hike odds are normalizing for the BOE after the November meeting, in which there was a 95%+ chance of a 15-bps hike (which did not occur).

- The ECB has made clear that it doesn’t intend on raising rates anytime soon, but that hasn’t stopped markets from pricing in the first rate hike in mid-2022.

- Retail trader positioningsuggests both EUR/USD and GBP/USD rates have mixed trading biases in the near-term.

Mind the Gap

In this edition of Central Bank Watch, we’ll cover the two major central banks in Europe: the Bank of England and the European Central Bank. Early-November has produced some significant shifts in rates markets, particularly in the wake of the ECB meeting in the final week of October and the BOE meeting last week. The continued evolution of rates markets is likely to have a profound impact on both EUR– and GBP-crosses for the foreseeable future.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Back to Reality for BOE

During October, rates markets turned aggressive towards expectations that the BOE would raise rates soon: starting the month with May 2022 favored for the first rate hike, the BOE meeting last week was greeted by markets pricing in November 2021 as the period most likely to produce the first rate move.

Alas, the BOE disappointed markets by producing the same 7-2 vote that QE and rates should remain unchanged, just like the Monetary Policy Committee did at the September meeting. “The Committee judges that, provided the incoming data, particularly on the labour market, are broadly in line with the central projections in the November Monetary Policy Report, it will be necessary over coming months to increase Bank Rate in order to return CPI inflation sustainably to the 2% target.”

Bank of England Interest Rate Expectations (November 9, 2021) (Table 1)

{kind=link}

Rates markets evaporated in the wake of the non-move by the BOE. Ahead of the November BOE meeting, rates markets were eying last week for a 15-bps rate hike (96% chance). Following the BOE’s disappointment, rates markets are back to discounting February 2022 as the most likely period for when rates will rise (133% chance; 100% of a 15-bps rate hike, 33% chance of a 35-bps rate hike). The next Quarterly Inflation Report (QIR) arrives in February 2022, so rates markets are effectively as aggressive as they can be at present time – a ceiling, of sorts, for the British Pound.

IG Client Sentiment Index: GBP/USD Rate Forecast (November 9, 2021) (Chart 1)

GBP/USD: Retail trader data shows 64.05% of traders are net-long with the ratio of traders long to short at 1.78 to 1. The number of traders net-long is 22.30% lower than yesterday and 11.58% higher from last week, while the number of traders net-short is 23.80% higher than yesterday and 19.90% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests GBP/USD prices may continue to fall.

Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed GBP/USD trading bias.

Market May Be Wrong About ECB

The ECB is among the world’s most dovish major central banks, and based on the commentary from ECB President Christine Lagarde at the October meeting at the end of last month, it doesn’t appear that the central bank will be shifting course anytime soon. Specifically, ECB President Lagarde noted that market pricing was not in line with the ECB’s guidance, a clear suggestion that rates markets were too aggressive in their expectations that the ECB would raise rates in the coming months.

EUROPEAN CENTRAL BANK INTEREST RATE EXPECTATIONS (November 9, 2021) (TABLE 2)

Nevertheless, rates markets remain convinced that the ECB will act on the rates front in mid-2022, even if the head of the ECB says otherwise. According to Eurozone overnight index swaps (OIS), while the ECB won’t change interest rates in the first half of 2022, the ECB is most likely to raise rates in July 2022 (62%). If ECB President Lagarde is correct, however, rates markets are thus wrong and thus any cooling of expectations could prove to be a negative development for the Euro.

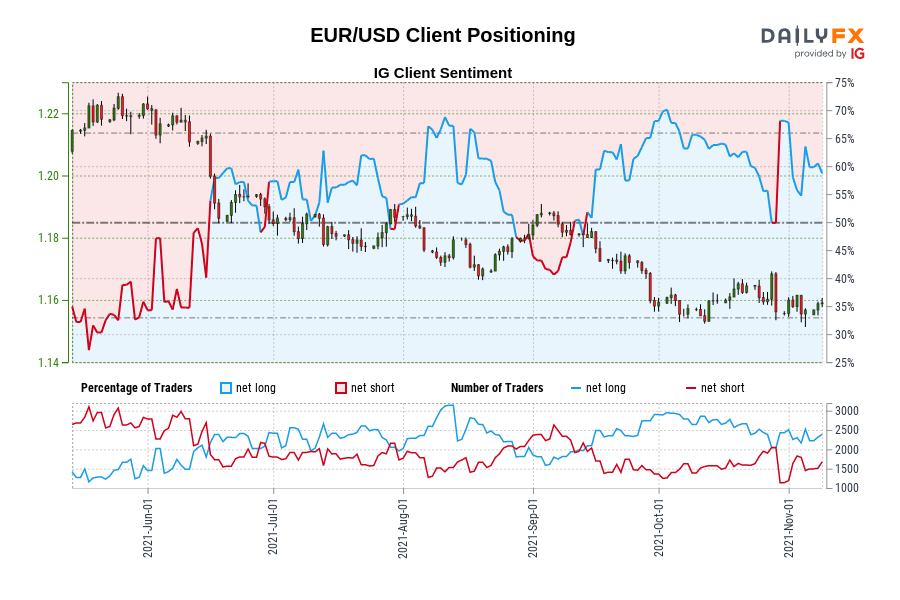

IG Client Sentiment Index: EUR/USD Rate Forecast (November 9, 2021) (Chart 2)

EUR/USD: Retail trader data shows 57.32% of traders are net-long with the ratio of traders long to short at 1.34 to 1. The number of traders net-long is 3.99% lower than yesterday and 7.65% higher from last week, while the number of traders net-short is 11.51% higher than yesterday and 4.22% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests EUR/USD prices may continue to fall.

Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed EUR/USD trading bias.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment