Maximusnd

Vanguard Long-Term Bond ETF (NYSEARCA:BLV) is passively managed using the Bloomberg U.S. Long Government/Credit Float Adjusted Index as its beacon aka benchmark. The purpose of this endeavor is to provide its investors high (used loosely as you shall see) current income using highly rated securities. BLV aims to provide unitholders a diversified exposure to the investment grade market in the U.S. It does that by investing treasury, agency, and corporate securities. The BLV ETF uses sampling to select securities from its benchmark index and has tracked the financial results rather well over the years.

Fund Website

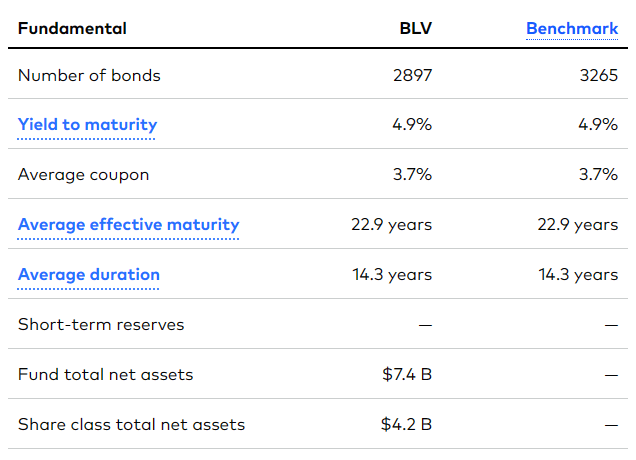

What also helped was its “blink and you missed it” expense ratio of 0.04%. The most recent data available on the fund website is for December 31, 2022 and while slightly stale, provides a glimpse of the ETF’s methodology in action.

Fund Website

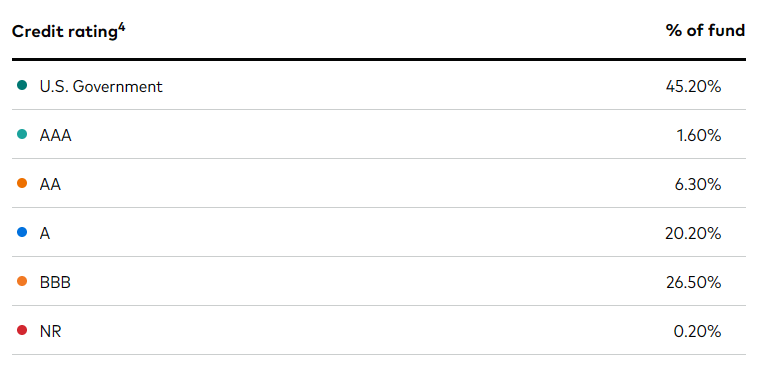

Almost three fourths of the portfolio was invested in A rated securities with treasuries forming the bulk of that.

Fund Website

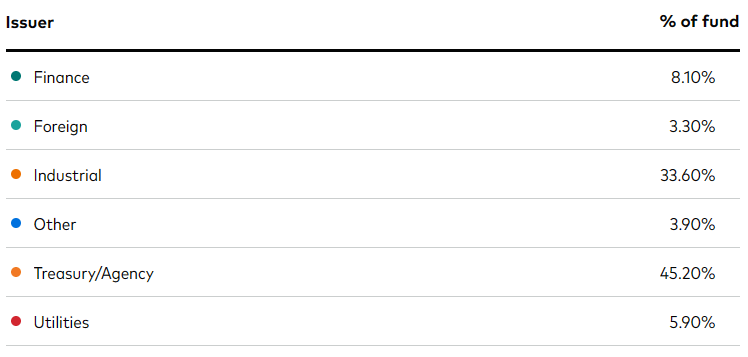

In terms of sector allocations, Industrials were the runner up forming a third of the total portfolio.

Fund Website

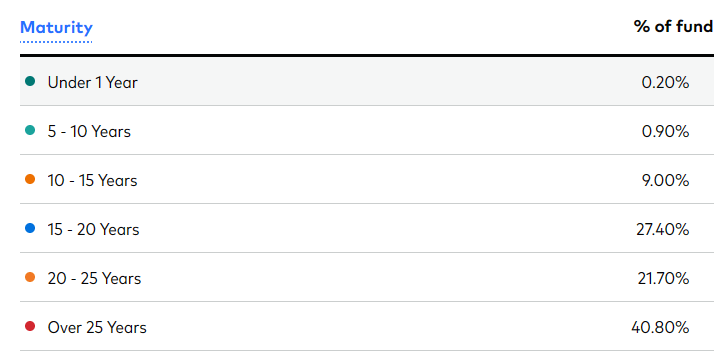

BLV target securities with maturities greater than 10 years, and at the end of 2022 majority of their portfolio matured in twice the target number of years. As a result, collectively the holdings had an average effective maturity of close to 23 years.

Fund Website

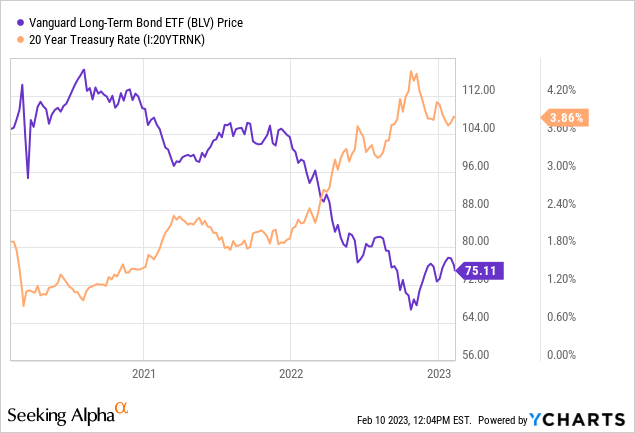

The longer time frame makes the portfolio subject to greater gyrations with the change in interest rates. This is because the existing holdings do not roll off in time to take advantage of the rising rates like we have had in the last year. Investors who buy these ETFs at inopportune times get hit with a double whammy of making relatively less than market rate, alongside the capital loss on them as investors exit for more higher yielding securities. While the effective maturity for BLV is over 20 years, the effective duration which is a measure of its sensitivity to the interest rates was 14.3 years. This means that broadly speaking the portfolio would lose around 14% of its value with every 100 basis points of increase in the comparable interest rates and vice versa. We can see BLV’s price fluctuation in response to the rate changes as an illustration.

We can see above the correlation between the interest rate increases since 2021 and the accompanying stock price decline translate roughly to the 14 year effective duration. Peak to trough the fund lost about 44% with longer term bond yields as represented by the US treasury benchmark yield, rose about 286 basis point. This is not a precise science and factors such as convexity, credit spreads and the duration during the various time periods along the way come into play, but we can get a general idea of how this works with the above exercise.

Yield

While the average coupon of the portfolio holdings was 3.7% at the end of last year, the yield to maturity was close to 5%. The distribution yield based on latest monthly distribution of $0.23426 coupled with the current price of $75.17 is around 3.73%. Over time, the distribution yield will converge with the yield to maturity. Since this is a very long duration fund, it can take some time for the convergence. In other bonds funds like iShares 0-5 Years Investment Grade Corporate Bond ETF (SLQD) or PIMCO Enhanced Short Maturity Active Exchange-Traded Fund (NYSEARCA:MINT), the extremely short duration means that the distribution catches up in a flash. You can see this from our article in August 2022, where we had stated that the yield would be 4% very soon. At the time MINT’s trailing yield was just about 1.66% and a good chunk of the commenters had a hard time with our title. Fast forward to today and we are over 4% at that the August price. With BLV though, you won’t get that 4.9% any time soon. So this can be a deal breaker for many investors who don’t want a bond fund if it will pay such a tiny yield.

Verdict

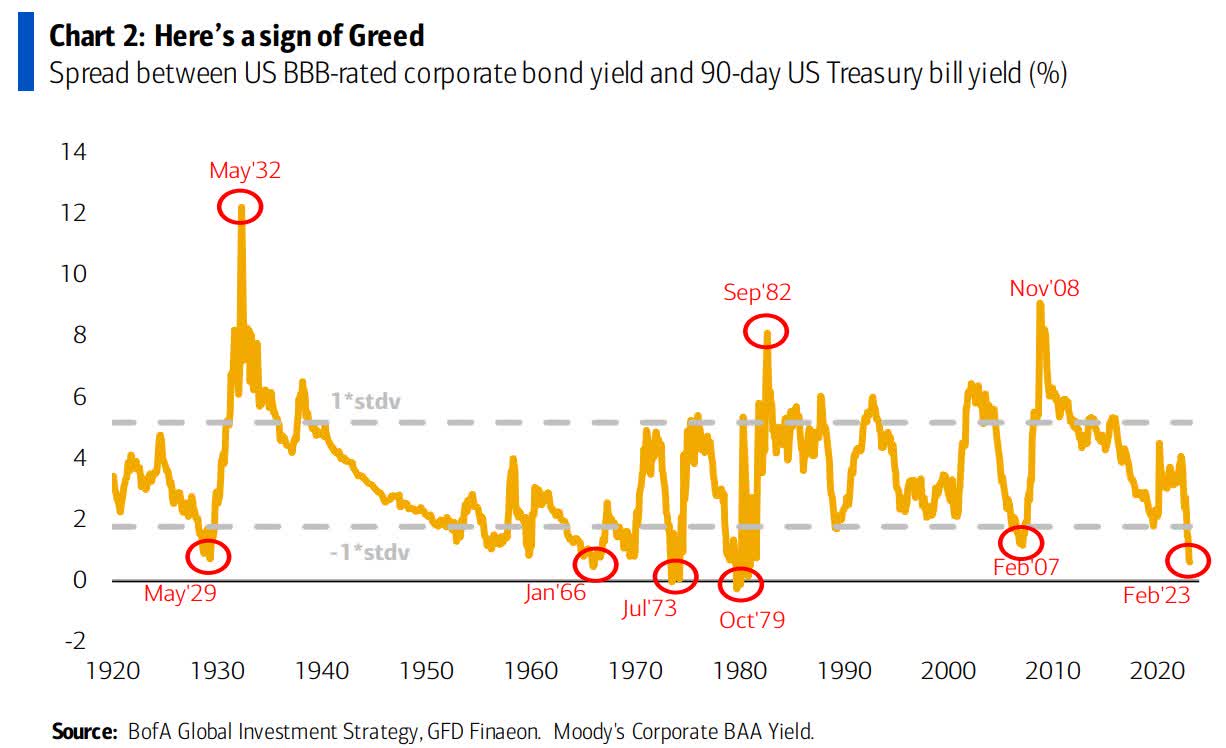

These are not the credit spreads you are looking for.

Bank Of America

The chart is a few days old, but underscores the most important point of all. You are not getting paid to take risk. Yes, the good aspect for BLV is that it holds a lot of Treasuries and corporate sector holdings are low. Even better, we are taking very little risk within the corporate sector by sticking to the top tiers. Nonetheless, the bigger question is why go for any corporate holdings at all? While we are at it, why go for a 3.9% distribution yield when you can get 4.85% in 6 month treasury bills? Yes, the Fed can cut down the line, but the longer term bonds have really priced that outcome to perfection. There is a lot of room for disappointment if the interest rates stay high for long. The long end bonds could get crushed in that scenario. We prefer Treasury Bills and might consider up to a 2 year Treasury note for bonds. But BLV is a no-go for us today.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment