KE ZHUANG/iStock via Getty Images

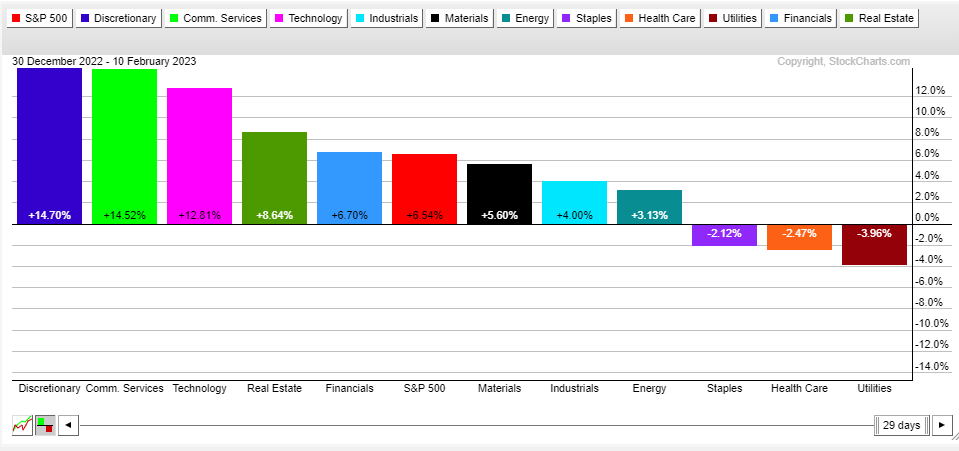

Defensives have declined so far in 2023. Three areas that worked on a relative basis in 2022 – Consumer Staples, Health Care, and Utilities – are all in the red so far this year. Even with a bump back up in yields, long-duration sectors have led the S&P 500. What’s more, with money market yields upward of 4.5% right now, yields in stable utilities suddenly don’t seem as attractive. I also find that the group is not all that cheap considering generally slow growth. We will get a growth update from one firm next week when it reports Q4 results. Are shares of Constellation Energy a buy? Let’s take a look at the valuation and technicals.

Utes Weak in 2023

Stockcharts.com

According to Bank of America Global Research, Constellation Energy Corporation (NASDAQ:CEG) is a competitive generation and retail company that operates the largest US fleet of nuclear and other carbon-free electricity. The company has a 100% carbon-free goal by 2040 for owned assets with a 95% interim goal by 2030. Approximately 90% of the generation output is nuclear or renewables with the assets concentrated in the Mid-Atlantic/Northeast (IL, PA, NJ, MD, & NY). The retail business is the second largest in the US with a 20%+ C&I market share.

The Baltimore-based $27.6 billion market cap Electric Utilities industry company within the Utilities sector does not have positive trailing 12-month GAAP earnings and pays a small 0.7% dividend yield, according to The Wall Street Journal.

Back in November, Consto (as we would call it back when I was a power trader for an energy marketing firm) reported a substantial EPS miss while topping revenue expectations. Shares fell following the report, but then rallied to all-time highs later in the month. Recently, though, the stock has wavered. Higher input costs and labor costs have weighed at times on CEG, but its strong nuclear generation assets help produce solid cash flow.

Rare for utilities, Constellation has ample free cash flow which allows for opportunistic investments and shareholder accretive activities like stock buybacks. What’s more, the firm can benefit from federal reimbursements through production tax credits through its renewables portfolio.

Downside risks include unfavorable regulatory outcomes and weather-related disasters, but the firm’s gen assets performed well during Winter Storm Elliott.

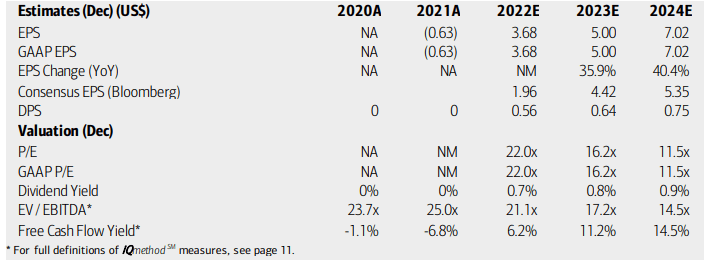

On valuation, analysts at BofA see earnings climbing big in 2023 after a positive earnings year in 2022. Per-share profits are expected to accelerate through next year, too. The Bloomberg consensus forecast is not as optimistic, though. Still, amply FCF should result in not only substantial share repurchases, but also a rising dividend.

With a FCF multiple under 10 this year, the forward P/E of 28 is not crazy, but still high. If CEG can hit $5 of operating EPS, then the stock is only 17x though. With an EV/EBITDA ratio in the mid-teens, however, the overall valuation is not super cheap, but I continue to like it given the growth outlook.

Constellation: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

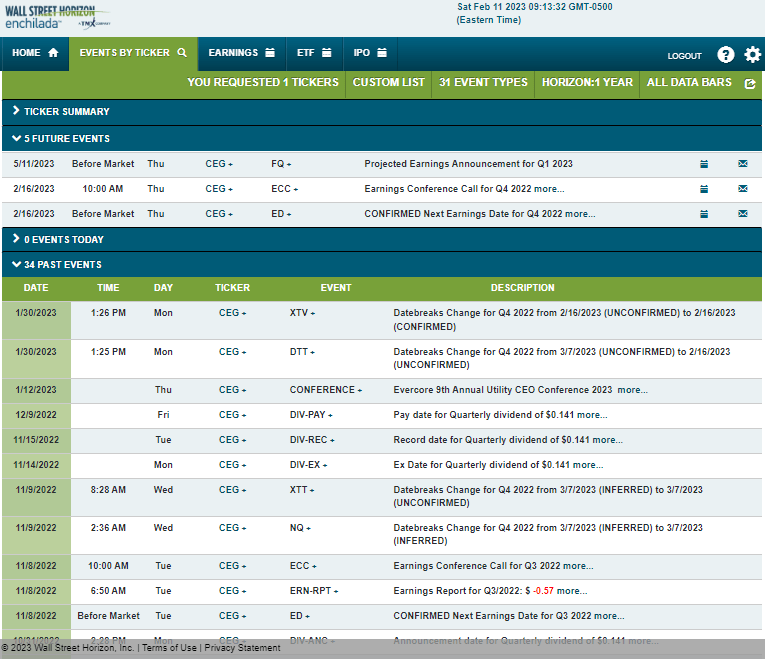

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 earnings date of Thursday, February 16 BMO with a conference call later that morning. You can listen live here. The calendar is light on volatility catalysts aside from the earnings date.

Corporate Event Risk Calendar

Wall Street Horizon

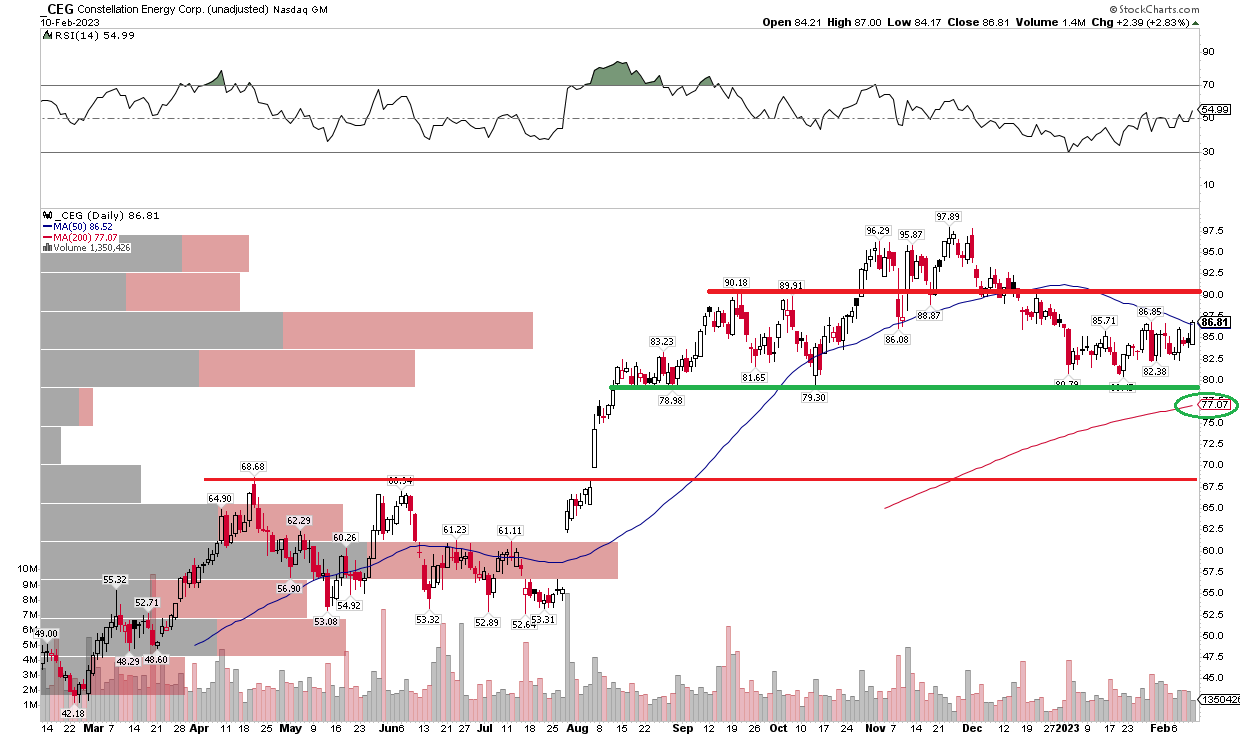

The Technical Take

So, what’s the update on the chart? Notice in the graph below that shares have consolidated big gains notched following positive Inflation Reduction Act news last July and August. CEG rose to its November high, then retreated nearly 20% to hold support around $80. The stock was up big last Friday, closing at a fresh 2023 high. I like a long play here with a stop under $78, but if that area breaks, there is not much air down to the $60s, so a sell-stop order is a good prudent move.

I see near-term resistance around $90, and I will be watching a potential bullish to bearish rounded top reversal pattern – I would like to see CEG rally above $90 to offset that. With a rising 200-day moving average and the stock now back at its falling 50-day, there are signs that the long-term uptrend is at least pausing. I still assert the onus is on the bears to take the stock down.

CEG: $80 to $90 a Key Range

Stockcharts.com

The Bottom Line

CEG continues to be a growth story within a sluggish and somewhat pricey sector. With earnings ahead, a long play near-term looks good while long-term investors should appreciate Constellation’s shareholder-friendly actions and high free cash flow due to its impressive nuclear holdings.

Be the first to comment