Serenethos

Blink Charging (NASDAQ:BLNK) shares have fallen more than 54% since mid-September, after warning of near-term risks stemming from a need to raise cash and a challenging path to profitability. Blink has just raised ~$100 million from a $12/share equity offering, slightly easing concerns even though more cash will be needed. However, positive underlying trends are surfacing — strong gross profit growth, decreasing levels of SBC, and a significant boost to manufacturing capacity. Let’s dive in to see if BLNK stock is worth a second look near $10, after falling over 30% in just over a week.

Cash Concerns Slightly Eased

From the most recent Q3 report, Blink’s cash position sat at ~$57 million, a razor-thin balance. Cash burn during the quarter averaged about $9 million per month, suggesting a six-month runway, hence the need for a capital raise.

Through fiscal 2022, Blink has burned through about $117 million, or an average of about $13 million per month — this includes the recent cash and stock acquisition of SemaConnect, financed with $80 million cash and $120 million in stock.

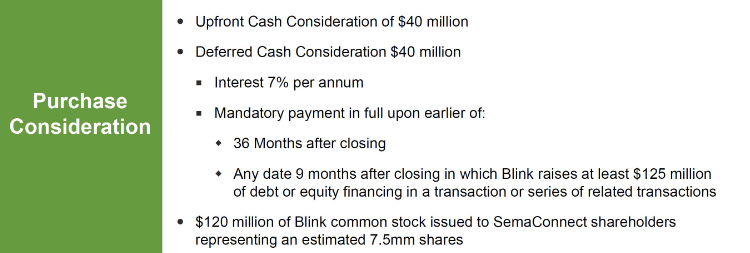

The one key consideration from this $100 million equity offering — and why it was limited to $100 million and not higher — is that it saves Blink from paying the deferred $40 million to SemaConnect. Under the terms of the deal, Blink owes the final $40 million after either 3 years, or if it raises more than $125 million within 9 months of the deal closing.

Blink Charging

Essentially, Blink’s $100 million capital looks like a strategic move to ensure the company has enough cash to surpass that 9 month obligation (late March), after which it can raise a larger sum. While the capital raise eases concerns about Blink’s razor thin cash, taking its estimated cash as of February 2023 to $112 million (accounting for cash burn), Blink is still likely to need more cash before year-end.

Strong Underlying Metrics

Even with another cash raise and further dilution likely in 2023, Blink’s fundamentals and underlying metrics are showing signs of improvement.

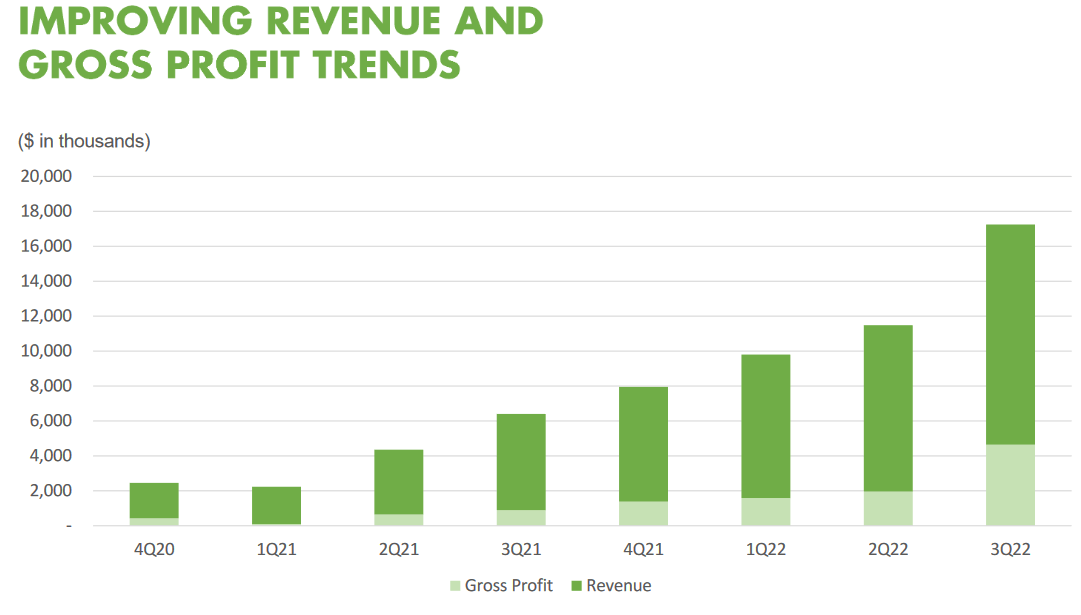

Blink has recorded substantial increases in gross profit as gross profit margin has expanded significantly. Although revenues and gross profit still remain at a small scale, the pace of growth suggests further gains ahead. Operating leverage does not look to be on the table just yet, even as operating expenses are dropped to 6.1x gross profit for Q3, compared to over 9x for 1H.

Blink Charging

Gross profit jumped substantially in Q3, reaching about $4.8 million, at a gross profit margin of 27.7%. Q3’s gross profit has contributed 57% of fiscal 2022’s gross profit to date, showing that Blink’s expansion and recent acquisitions are aiding revenue growth, gross profit growth, and gross profit margin.

Take a comparison to fiscal 2021 — gross profit in Q3 ’21 was just $892k, at a 13.9% margin; in the nine-month period, Blink only recorded $1.46 million in gross profit at an 11.3% margin. On a y/y basis, Blink has doubled its gross margin for the quarter, and nearly doubled it for the nine-month period. With revenue growth expected to be in the region of 65% to 70% for fiscal 2023 towards $100 million, maintaining a gross profit margin of ~24% for the year would see gross profit totaling ~$24 million.

Other signs of strength in Blink’s fundamentals include decreasing levels of SBC.

Although Blink has diluted shareholders to a large degree via the SemaConnect acquisition (about 17.5% ownership went to Sema) and the recent equity offering (8.33 million plus 1.25 million over-allotment), SBC is decreasing, unlike peers like ChargePoint (CHPT) where SBC is increasing.

For fiscal Q3, Blink’s SBC expenses decreased 22.4% to $4.8 million, and for the nine-month period, decreased 24.1% to $7.8 million — Blink incurred a majority of its YTD SBC expense in Q3.

Most growth stocks tend to incur increasing levels of SBC, utilizing it for employee retention and acquisition. While SBC is beneficial from that standpoint, companies are able to show adjusted profitability on a non-GAAP basis by excluding SBC; however, these companies are wildly unprofitable when accounting for SBC, such as MongoDB (MDB).

In Blink’s case, SBC may not be as attractive to employees as shares are diluted and as share price falls, but showing decreasing levels of SBC as growth scales significantly demonstrates that Blink could be on a quicker pathway to GAAP profitability once operating leverage kicks in, given that it is not heavily spending in SBC.

Valuation Comparable To CHPT

In the low $10/share range, Blink trades at fairly similar levels to rival and EV charging leader ChargePoint.

With estimated revenues of $100 million, Blink trades at approximately 5.6x EV/revenues, slightly above ChargePoint’s ~4.9x forward EV/revenue multiple. Both are projected to record losses for the upcoming fiscal year, with profitability not in sight until at least 2025. Compare this to EVgo’s nearly 12x EV/revenue multiple, it’s evident the market is valuing Blink and ChargePoint as the outright leaders in the space, with revenues and scale to show.

For Blink, the main downside stems from its need for cash. The strategic cash raise of $100 million prevents Blink from having to pay out its deferred payment to SemaConnect while offering another two to three quarters of runway before more cash will likely be needed. This dilutive risk is probably the largest headwind to shares at the $10 range, as valuation has dipped comparably to ChargePoint.

Blink also benefits from increasing ASPs, from ~$1,010 in Q1 to $1,560 in Q2 to $1,705 in Q3. Combining that ASP growth with the ability to scale production to at least 30,000 units to 50,000 units annually opens the doors for accelerated revenue growth over the next two to three years. With EV market growth expected to benefit significantly from the IRA and from a flood of new models hitting the market over the next few years, the tailwinds are all in place for Blink to capture a multi-year growth runway.

Outlook

Blink’s shares have fallen nearly a third in just over a week as the market pulled back and as the equity offering negatively impacted shares. In the low-$10 range, Blink is valued comparatively to ChargePoint, and is showing positive signs within ASP growth, boosting revenues as manufacturing capacity is set to expand, while gross profit growth is increasingly strong. SBC expense is also decreasing, and if this trend continues, Blink could be on a fast track to profitability once operating leverage arises, likely by 2025. Shares are worth another look at $10, but are not fully a convincing buy yet due to the risks to dilution ahead this year.

Be the first to comment