Editor’s note: Seeking Alpha is proud to welcome Bay Area Ideas as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Alex Wong

Thesis

Despite large headwinds in the last few quarters, I believe the long-term growth story of Blackstone Inc. (NYSE:BX), the world’s largest alternative asset manager, is still highly intact. Amid market turbulence, Blackstone recorded a relatively weak investment performance in Q3 2022 but was still able to grow its total AUM by 30% YOY to a record $951 billion. The recent investment of $4 billion by the University of California into the Blackstone REIT has restored confidence amid redemption curbs. In my view, with near-term headwinds/uncertainties and a premium valuation, Blackstone’s stock will struggle to outperform in the near term but the company’s future is still very bright as there does not seem to be any long-term reversal in alternative management trends. I believe Blackstone is a buy in any major pullback in 2023.

Third Quarter 2022 Earnings

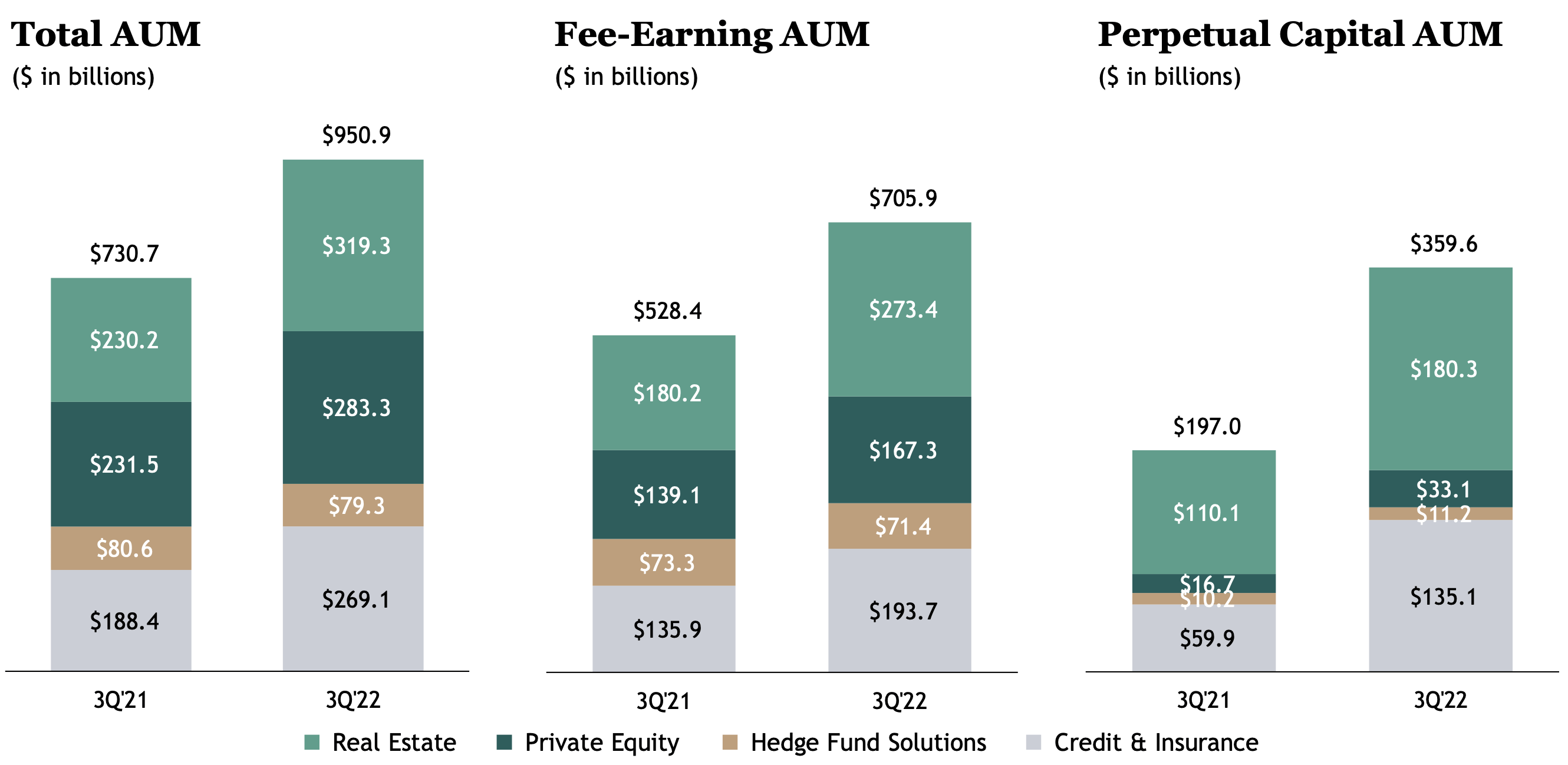

In its third quarter earnings release in October, Blackstone reported promising results despite also showing difficulties in some of its investments as interest rates continued to rise. In my view, the attractiveness of Blackstone’s funds did not seem to be an issue in 2022. They had a fee-earning AUM of $705.9 billion in Q3, up 34% YOY. Perpetual capital grew to $359.6 billion, which was a 83% YOY increase. This is very significant as perpetual capital has allowed Blackstone to make longer-term commitments that were previously impossible. Blackstone reported $44.8 billion in inflows in 3Q22 and $337.8 billion in the LTM period. It is clear that Blackstone is still attracting clients despite the headwinds.

Blackstone Q3 2022 Earnings Blackstone Q3 2022 Earnings

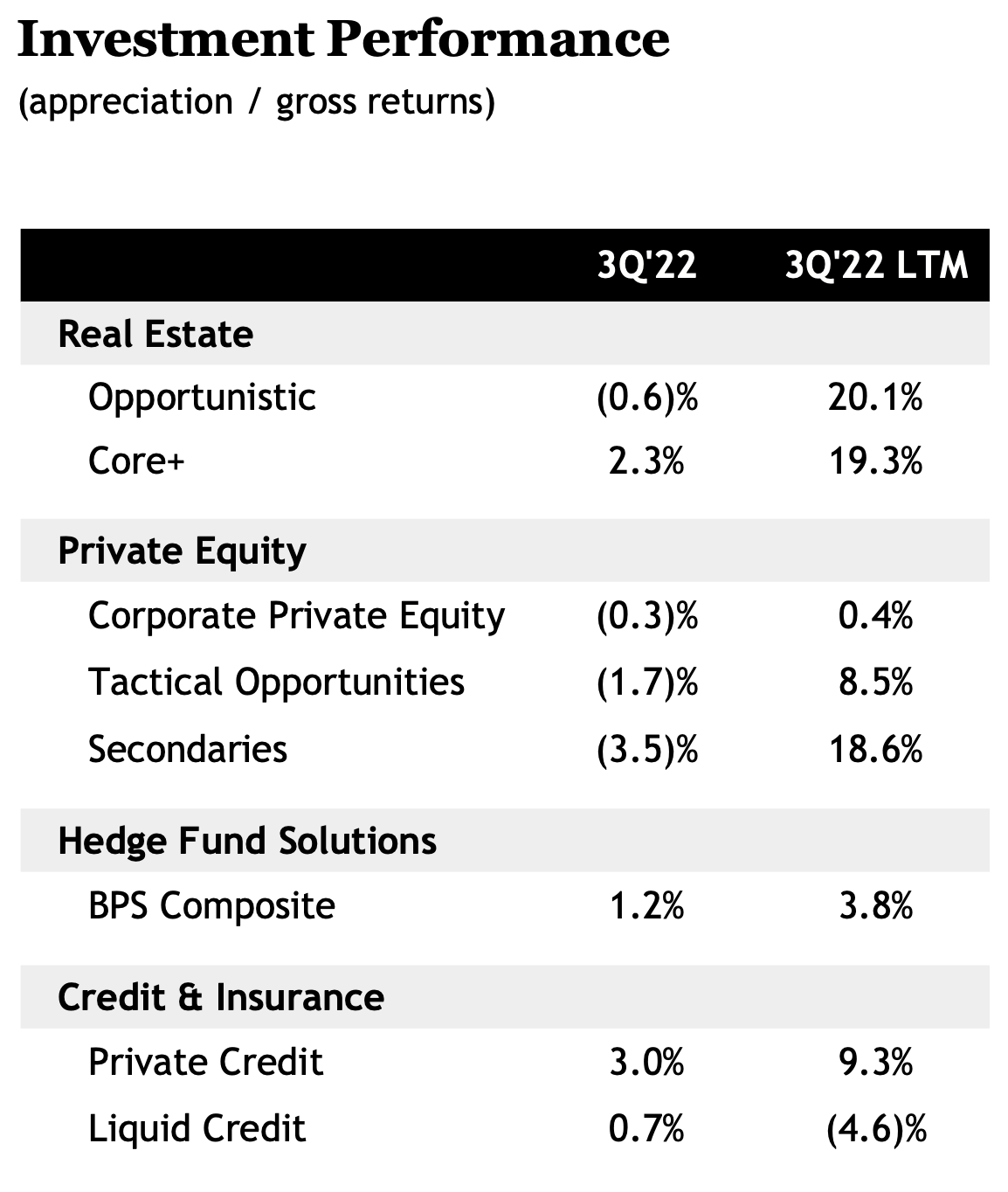

Blackstone’s fee-related earnings also showed very strong results. Total fee-related earnings grew by 51% YOY in Q3 and the Q3 YTD figure showed 50% growth YOY. However, net realization income plunged 61% YOY in Q3 despite showing 28% YOY growth for the YTD period. Blackstone also had a lackluster third quarter in terms of its investment performance. Overall, the company had weak quarterly returns and was mainly focused on capital preservation rather than gains. The largest losses occurred in its Private Equity category while the largest gains were in its Private Credit category. This reflects that interest rates are weighing on equity asset classes while boosting its credit segment. However, for the LTM, Blackstone was still able to generate mainly positive returns across asset classes. It is clear that despite its difficulties in its investments, Blackstone is still generating large amounts of revenue through its fees. According to my analysis, the weakness in Blackstone’s earnings is mainly the result of interest rates weighing on asset prices rather than any company-specific issues.

Blackstone Q3 2022 Earnings

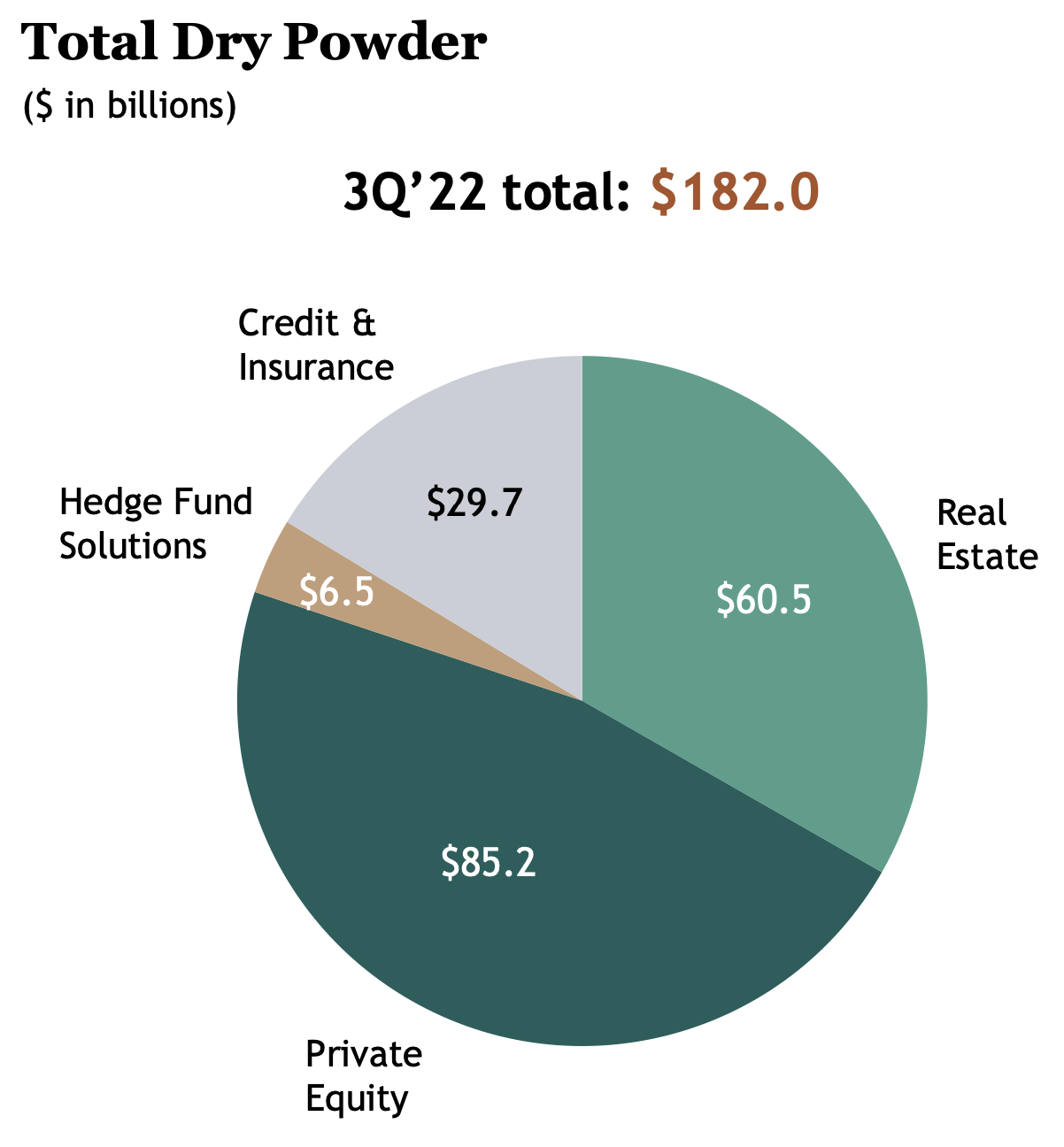

While their investment performance has suffered, Blackstone still remains highly committed on long-term returns. During the market turbulence in 2022, Blackstone has not shied away from making investments for clients. In fact, they deployed $31.3 billion of capital in the third quarter and $167.6 billion in the LTM period. In particular, in the third quarter they deployed capital of $11.2 billion in Real Estate, $7.6 billion in Private Equity, and $12.3 billion in Credit/Insurance. Blackstone has been capitalizing by making investments in a market plagued with fear. In addition, the company also holds $182 billion in dry powder. With large amounts of dry powder concentrated in real estate and private equity, Blackstone is in great position to take advantage of potential weakness in these asset classes in the coming quarters. My view is that, amid large amounts of uncertainty in 2023 with regards to economic growth and interest rates, markets may continue to see weakness and Blackstone is ready to make more quality investments as opportunities present themselves.

Overall, in its most recent earnings report, Blackstone showed that near-term headwinds are continuing to plague its investment returns, particularly in their riskier asset classes. Net realization income continued to be weighed on while fee-related earnings have been much more resilient. In terms of segment performance, Real Estate and Credit/Insurance were the outperformers while Private Equity and Hedge Fund Solutions lagged. Despite the turmoil in Real Estate, Blackstone managed to show a Q3 7% YOY increase in the segment’s distributable earnings. It had high fee-related earnings growth of 62% YOY in Q3 while net realization income plunged 54% YOY during the quarter. The Credit/Insurance segment also showed strong results likely driven by interest rate hikes with segment distributable earnings up 176% YOY for the quarter. The Private Equity and Hedge Fund Solutions segments showed weakness as a result of the sell-off in risk assets throughout 2022.

Since this earnings report back in October, headwinds for the asset management industry have continued or even strengthened. With the Fed continuing to hold a hawkish stance, 2023 may be a continuation of what 2022 had to offer. I therefore believe Blackstone’s weak investment performance will likely continue amid market uncertainty. However, make no mistake, Blackstone is focusing on the long term and its growth story over that timeframe appears still intact, with strong AUM growth and deployment of capital even amid turbulent markets.

Redemption Concerns

Early in December, it was reported that Blackstone had to limit withdrawals at its $69 billion REIT. It happened as a result of redemptions hitting the preset limits. Further questions were raised as it was reported that Blackstone’s REIT may have been slow to adjust valuations to market prices causing investors to cash out investments at prices higher than the market. Of course, this is a worrying sign and the stock plummeted as a result of this news. In my view, fears were likely overblown as it was discovered that most of the redeeming investors were located in the Asia-Pacific and they needed liquidity as a result of China’s uncertainty and the Asian market volatility. Again, this was an event that was driven mainly by external factors and does not reflect that Blackstone has fundamental issues. Just days later, however, it was reported that the withdrawal limit was hit at Blackstone’s $50 billion Credit Fund. It was the first time this had ever happened at this fund but the company still allowed clients to cash out. Both of these events have no doubt dented both client and investor confidence in the company. It is clear that Blackstone is facing many headwinds over the near term.

After these two reports, Blackstone had to delay the launch of a new private equity fund. The company was reportedly preparing to launch the Blackstone Private Equity Strategies Fund but will now wait until financial market conditions improve. I believe this will delay Blackstone’s growth plans and lower its fee-related earning projections. Through these news reports, it is shown that the fundamental business of Blackstone remains very strong while external factors and headwinds are hampering its business in the short term and causing it to have to delay its growth plans.

Lastly, Blackstone is already rebounding from the REIT redemption report with significant inflows. Approximately two weeks ago, the University of California announced that it would invest $4 billion into the Blackstone REIT. Clearly, despite all the fear and pessimism around Blackstone, it is still attracting clients. While there has been widespread fear over Blackstone’s funds, I believe the core business is still functioning robustly.

Valuation

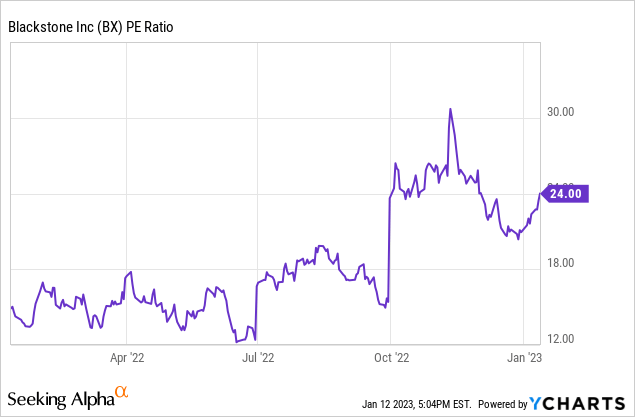

At current levels, the PE ratio of Blackstone is at around 24. As shown in the graph below, it remains elevated relative to levels in the last 12 months. With continuing concerns of a 2023 recession and the uncertainty in the path of interest rates, in my view, Blackstone is still valued quite richly at current levels. The forward PE ratio seems to be showing more moderation in its valuation but 2023 earnings estimates are still highly uncertain amid the economic backdrop.

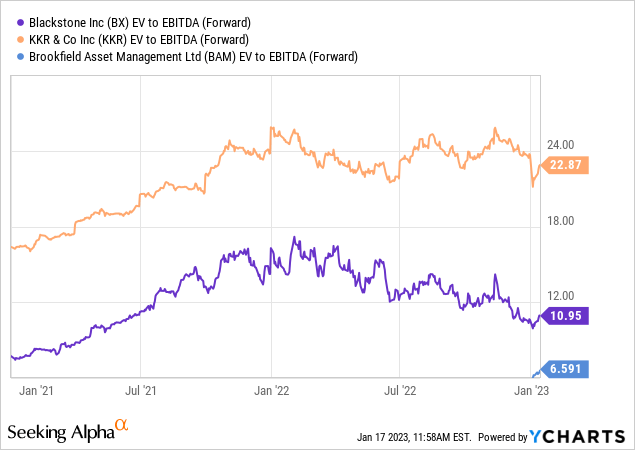

As shown below, in terms of the forward EV/EBITDA ratio, Blackstone’s valuation is in between that of competitors KKR & Co. Inc (KKR) and Brookfield Asset Management Ltd (BAM). Blackstone is valued significantly cheaper than KKR but still valued at a premium relative to BAM. In term of its own history, Blackstone’s forward EV/EBITDA is well off its 2022 peak but it is still elevated when compared with levels seen in the first half of 2021. In H1 2021, financial conditions were much looser and overall investor sentiment was much better than it is currently. Therefore, I believe that even though Blackstone’s valuation has pulled back significantly, it is still quite richly valued given market conditions. With the newly spun-off BAM trading at 6.591 forward EV/EBITDA and Blackstone having traded at around 7.5 forward EV/EBITDA in January 2021, I expect Blackstone’s forward EV/EBITDA to compress to similar levels in a 2023 pullback. Keep in mind that as 2024 approaches, earnings estimates may have upward revisions as uncertainties are resolved and that may help to lower the ratio. In my view, given uncertainty and market conditions, Blackstone has room to fall to a forward EV/EBITDA in the 7-8 range. At that point, the BXC stock would be fairly valued. According to my analysis, this would be an opportunity for long-term investors as they would then be buying a premium company at a fair price.

Risks

Despite the growth story being intact currently, I believe there are risk factors that could derail Blackstone’s future. First, the redemptions so far have had a limited impact on Blackstone’s business. However, if market volatility continues into 2023 or longer, investors may continue to be on the hunt for liquidity. Therefore, Blackstone may continue to be hit with similar redemptions in the upcoming months. If there is continuous demand for redemptions, Blackstone’s business model will be under pressure as they potentially will have to forgo good investment opportunities to ensure they have enough liquidity to meet client redemptions. If enough redemptions occur, Blackstone may be even forced to sell profitable assets in order to meet redemption demands. My view is that this scenario could fundamentally impact Blackstone’s usual strategy of investing client capital in long-term high-return assets.

Another major risk is the Fed. Although inflation seems to be on a declining trend, the Fed’s stance is still quite hawkish. Although there are hopes that there will be rate cuts as we head into second half of 2023, there is a risk that the Fed may have to hold rates higher for longer in order to truly hold inflation near their 2% target. If so, Blackstone’s investments will be put under pressure for far longer than expected and longer-term underperformance in their investments may cause clients to reevaluate their commitments to the company. This scenario could also hamper their growth over the next few years.

That said, I believe that at this moment both of these risks are not likely to occur as there is no evidence that redemptions are getting out of hand or that inflation will remain high beyond 2024.

Conclusion

Blackstone’s fundamental business is rock solid. Its most recent earnings report shows that they are attracting clients even amid market uncertainty. In fact, it can be argued that traditional market volatility has accelerated the adoption of alternative investments. Their fee-related earnings are showing significant growth even though investment performance has been hampered by interest rates. They are making investments when others are fearful as they are deploying capital in many different areas of their business. They also have lots of dry powder which will keep them ready to pounce on opportunities as they present themselves. According to my analysis, Blackstone’s long-term growth story is robust but the near-term is much more uncertain. With fund redemptions weakening investor confidence, Blackstone is delaying the launch of some products. However, these redemptions happened mainly due to external factors, and Blackstone’s fundamental business remains unaffected. In fact, the University of California’s recent investment has already started to restore investor confidence. Despite so many recent struggles, Blackstone’s stock valuation has remained relatively expensive. While it is getting more reasonable, I believe Blackstone’s valuation remains quite rich. Therefore, Blackstone is currently a hold in my view but any major pullback in 2023 will be a great buying opportunity for long-horizon investors. While the short term may have more pain to come for Blackstone, its future is still as bright as ever.

Be the first to comment