JamesBrey

Dear readers/followers,

Blackstone Mortgage Trust (NYSE:BXMT) reported their Q4 results on Feb 8, 2023, and although they reported solid earnings and beat estimates, the market sold off by around 8%, likely because investors got spooked by a large increase in the CECL reserve (current expected credit losses) and focused too much on the negatives. I believe the market has overreacted, creating an attractive entry point for anyone not yet invested in BXMT stock.

Why should you be interested in this stock? Well, for starters, it has a dividend yield of 10.8%. And I know, yields above 8% are risky and will get cut eventually, right? Well, maybe not this time unless, of course, unless things get a lot worse. The company is actually in a pretty good shape and on top of that is undervalued compared to peers.

Blackstone Mortgage Trust

This is a mortgage REIT (mREIT), this means that the company’s sole business is underwriting loans for real estate. BXMT focuses on commercial real estate, which is riskier than residential real estate, but also enables the company to earn superior yield on their portfolio. The good thing is that the company focuses on quality rather than quantity.

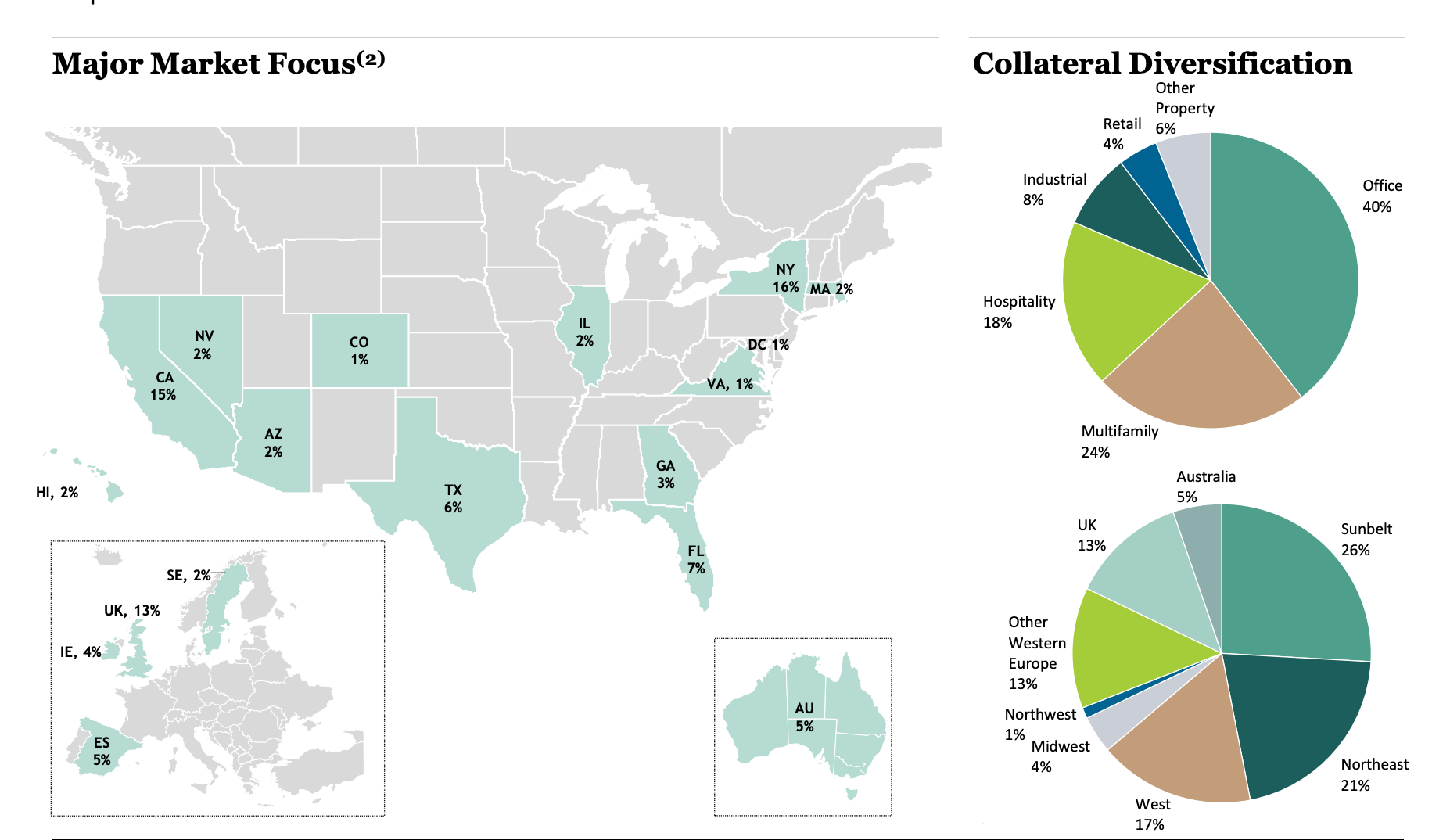

Its $26.8 Billion portfolio currently consist of 203 loans on institutional quality assets, mainly across the US (69%) with some exposure to Europe and Australia. The portfolio is heavily weighted towards offices (40%). The allocation to offices is also arguably what has scared investors away, although BXMT has done a good job of explaining in their Q4 presentation that the vast majority of the office portfolio consists of loans on newly constructed or substantially renovated assets with LTV below 65%. 4- and 5-rated offices (which are most likely to struggle with high vacancies) only account for 5% of the portfolio, and there are substantial CECL reserves in place for those (more on this later). I also find reassuring that in 2022 they had a 100% interest collection, despite a 400bp+ increase in U.S. short rates.

BXMT Q4 2022 Report

2022 results

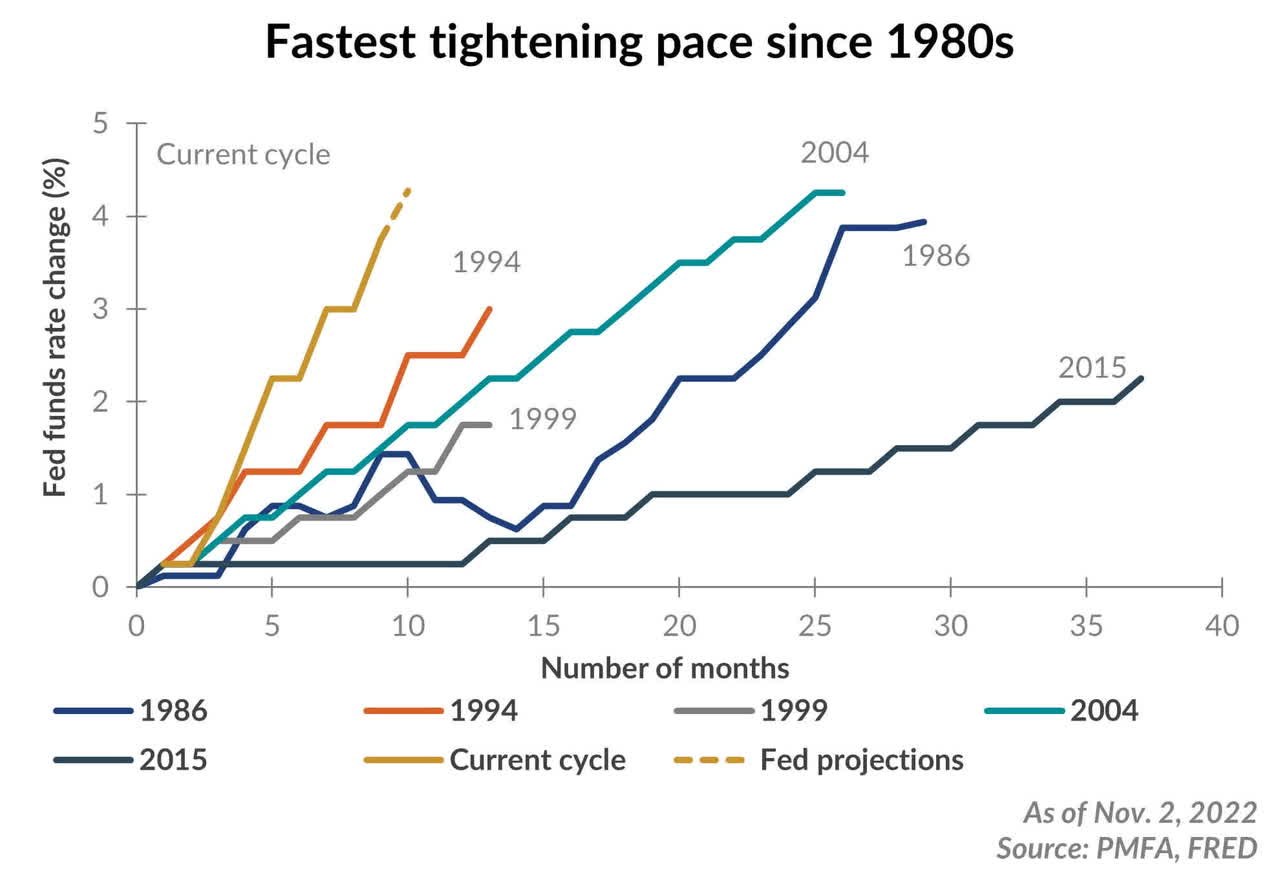

In 2022 the Federal Reserve raised interest rates by over 4% in an effort to fight inflation, resulting in the fastest hiking cycle in modern history. And since BXMT is a mortgage REIT, their results are primarily driven by interest rates. In particular, higher interest rates significantly increase their earnings, because 100% of their loans are floating rate, therefore allowing the company to charge higher interest on their loans. This is great, but it comes with a ‘but.’ Higher rates also put a lot of pressure on the economy as a whole, and especially on the heavily indebted real estate sector. With a slowing economy and increasing rates leading to higher interest payments, some borrowers will simply not be able to keep paying and will default on their payments. This is especially worrisome on distressed assets that have high vacancy (such as old office buildings).

FRED

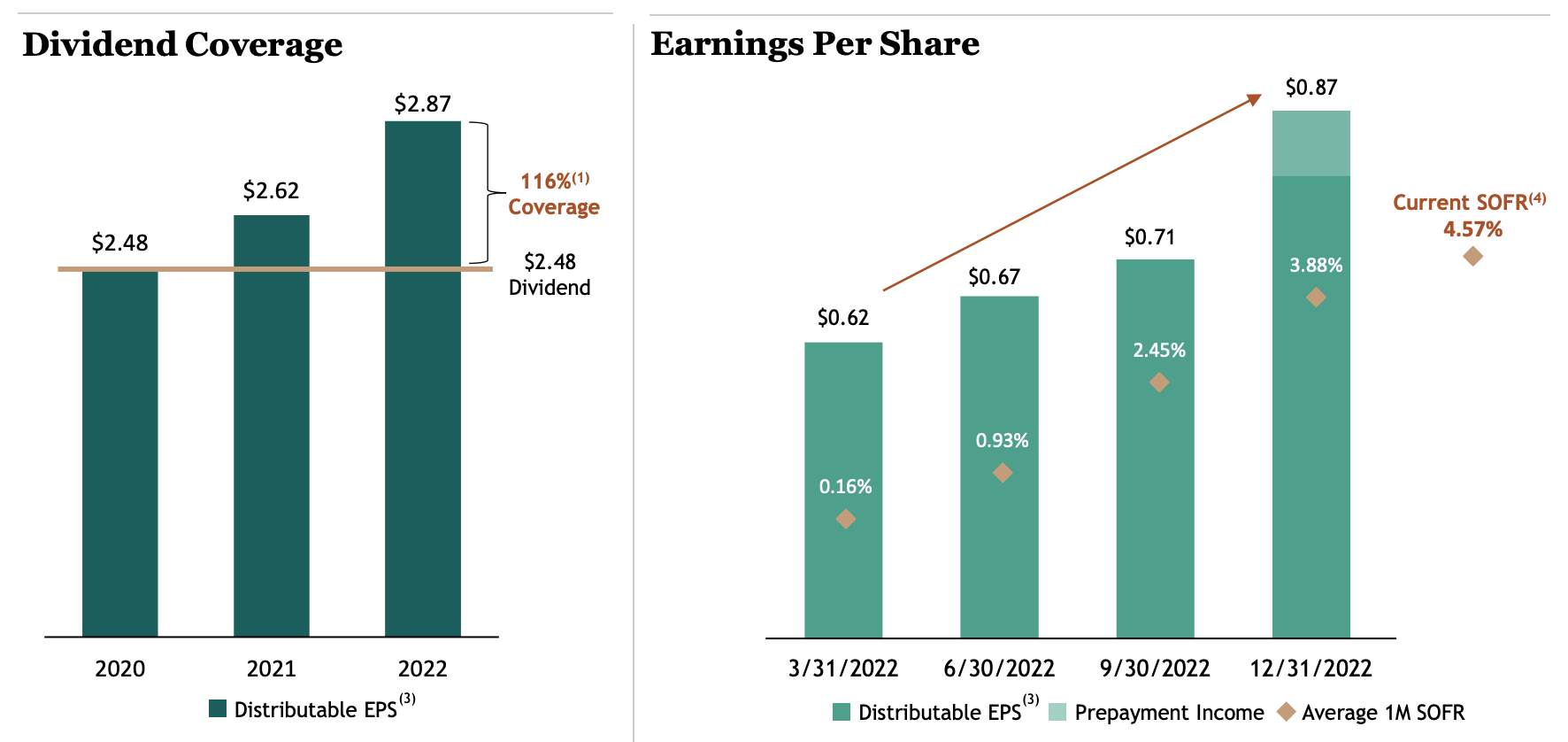

In terms of earnings, the company has done great in 2022, generating a 9.5% YoY growth in distributable earnings, supporting robust full year dividend coverage of 116%. The dividend coverage has been significantly higher in 2022 compared to prior years, allowing the company to retain $66 million of excess distributable earnings. Earnings have accelerated over the course of the year, driven by increasing rates (see SOFR below – secure overnight financing rate).

BXMT Q4 2022 Report

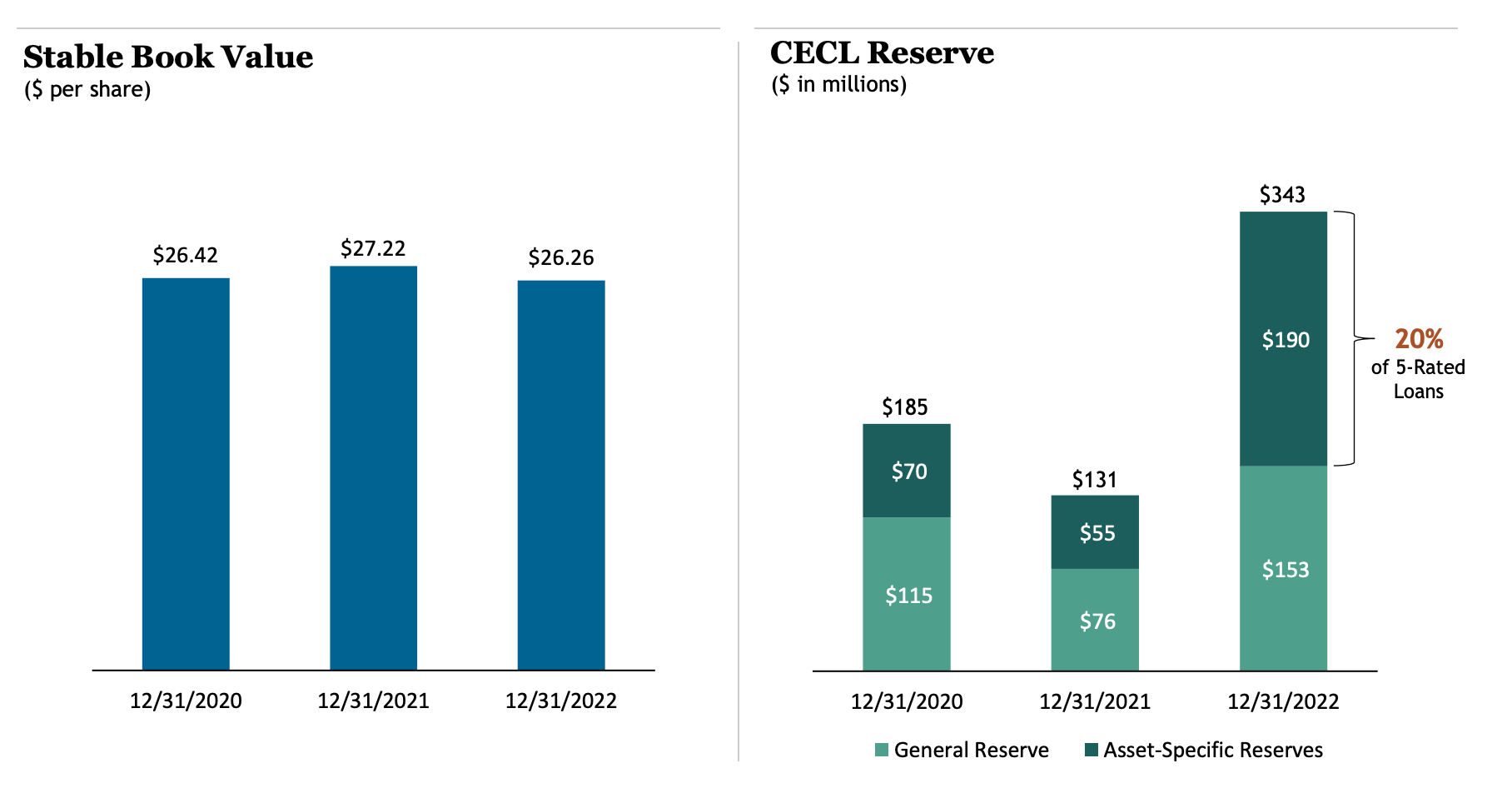

Throughout 2022 the company has increased its CECL reserve by 161% compared to the year prior. In Q4 alone, the reserve increased by $1.10 per share. This increase was done to be able to cover up to 20% of 5-rated loans in case of default. Understandably, this scared investors, as it may indicate that the company expects trouble going forward. I’d argue though that it could just as well mean that management doesn’t necessarily see problems coming, but given the extraordinary earnings results of this year, they simply want to hedge a little and perhaps lower the expectations going forward. Either way, this increase in CECL reserve combined with $66 million of excess distributable earnings resulted in a decrease of book value of 3.5% to $26.26 per share. It’s worth noting, that the book value doesn’t get market-to-market (as BXMT’s assets are not publicly traded), but rather is confirmed each quarter by external valuers.

BXMT Q4 2022 Report

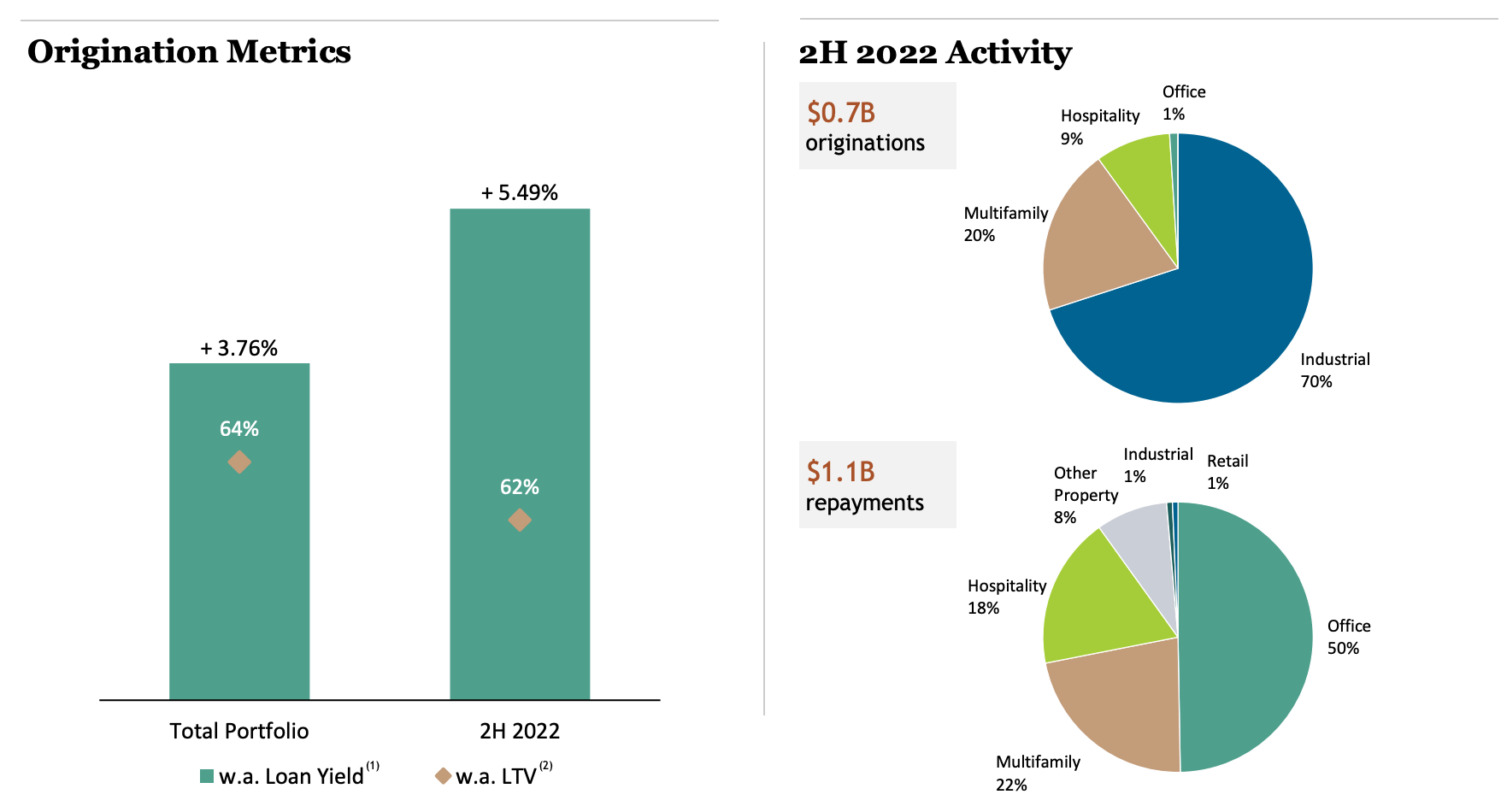

Recent originations and repayment reiterate the focus on quality as the company puts more emphasis on valuation, leading to lower LTV of new originations and shifts away from riskier assets. Lending conditions have changed drastically between the first and second half of 2022 (due to much higher rates in the second half). This has understandably helped the company get higher yields on their loans (5.49% in H2 2022 vs overall average of 3.76%), but notably these new loans have also been underwritten at a lower LTV. In H2 2022, BXMT mainly gave out new loans for industrial projects while mainly closing loans for office projects. Although the annual turnover accounted for only 7% of the portfolio, this shows their focus to move away from offices and into safer asset classes.

BXMT Q4 2022 Report

Valuation

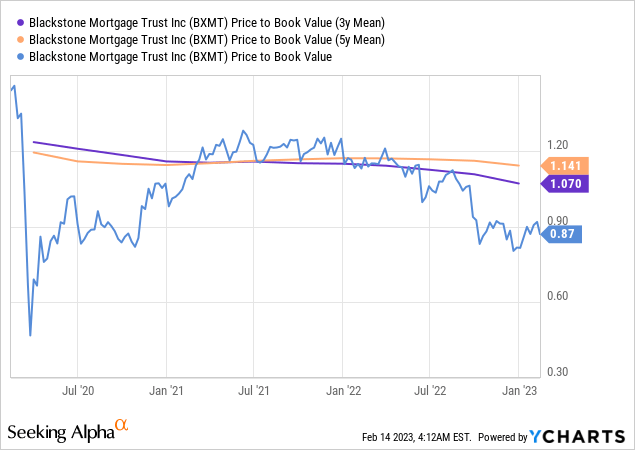

The best way to value an mREIT is to look at its P/BV. The company currently trades at $22.80 per share, which represents P/BV of 0.87x. Any value below 1.0x indicates that a company is trading at a discount. In the case of BXMT, this is reinforced by the fact that book value was actually revised down in 2022 as the CECL reserve was increased.

The current multiple is also below the 3-year and 5-year average multiple of 1.07x and 1.14x, respectively. That means there’s a 26% upside when the stock returns to it historical average P/BV of 1.10x. This gives an indicative PT of $29.00 per share, but I am not planning to sell at that price, not with the 10.8% dividend yield.

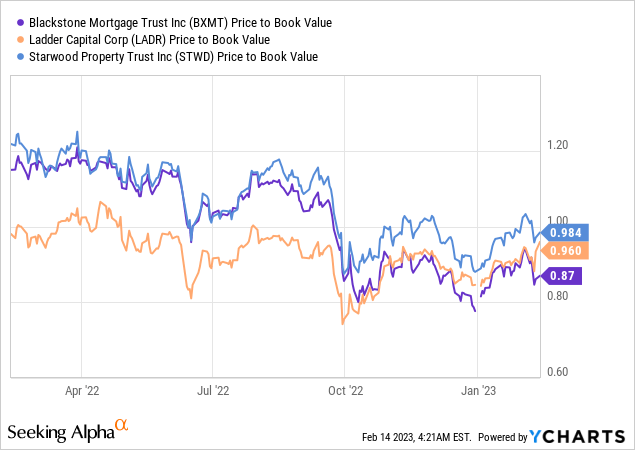

When compared to peers, BXMT also seems undervalued, as both Starwood Property Trust (STWD) and Ladder Capital (LADR) are trading at P/BV multiples close to 1.0x. This confirms that the stock probably has some upside in addition to a great dividend yield.

Verdict

Rising interest rates have been a double edged sword for BXMT – they drove very strong earnings results in 2022, but also caused the company to increase the expected credit loss reserve (‘CECL’) in anticipation of some of its 5-rated loans struggling. The market has mainly focused on the negatives and punished the stock accordingly. The company now trades at a discount respective to its historical P/BV average multiple as well as peers and given the quality of the portfolio, I don’t think this discount is justified. There is a 20%+ upside to normalized levels in addition to an almost 11% dividend yield that has historically been covered by distributable earnings.

I rate BXMT as a “Buy” here at $22.80 per share and might add to my position, which has a basis around $23.50.

Be the first to comment