Andrew Burton

And there you have it, folks, a potential turnaround for BlackRock’s (NYSE:BLK) stock after a triumphant fourth-quarter earnings report that saw it stroll past revenue estimates by $70 million while delivering an earnings-per-share beat of 86 cents.

Although BlackRock’s year-over-year results have softened, Friday’s Q4 earnings beat provides a potential inflection point to the company’s stock, which has drawn down by approximately 15% in the last year.

Here’s why we believe BlackRock and its stock alike could reroute in 2023.

BlackRock Q4 Earnings Review

First, let us start off by reviewing a few of the key events that occurred during BlackRock’s fourth quarter.

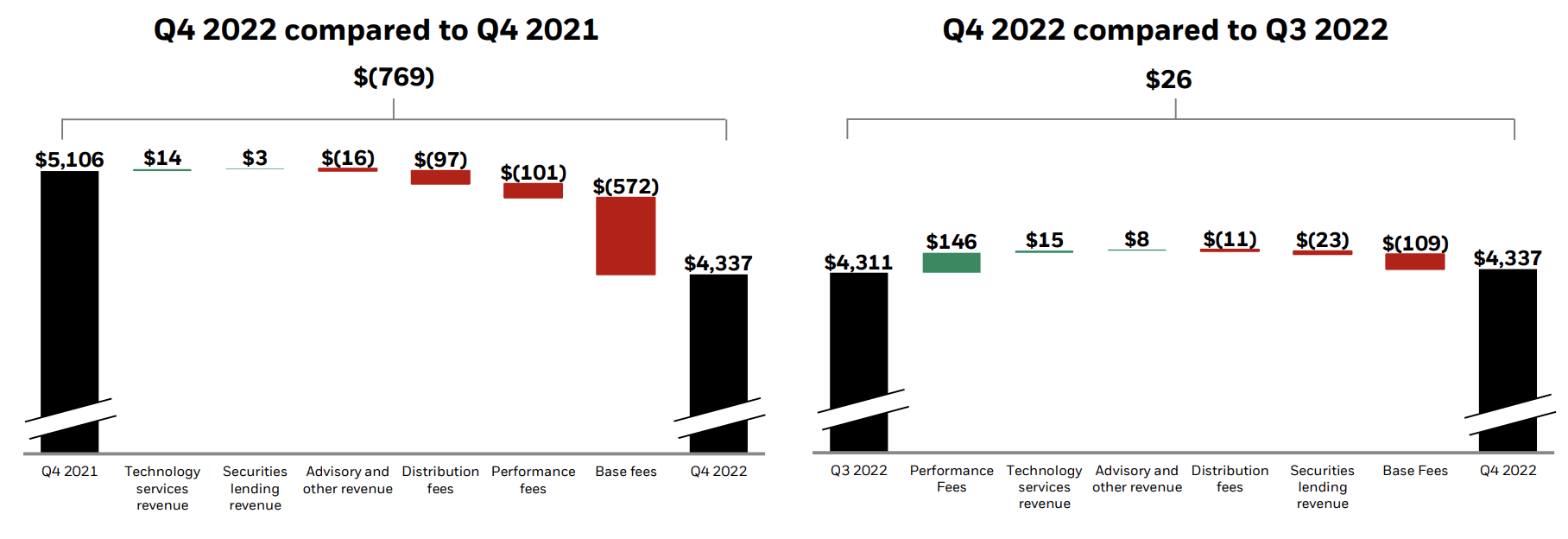

The company’s revenue from base fees retraced during the past year amid a slump in global financial market activity. In BlackRock’s case, much of the business unit’s backdrop was induced by lower securities lending revenue, which in turn forced lower entry rates. However, we see a sharp recovery in 2023 as monetary policies (and FX rates combined) are starting to illustrate consistency. Moreover, harder entry-level pricing could be possible, given a potential financial market recovery.

Revenue Breakdown (BlackRock)

Furthermore, BlackRock’s private market activities are in balance. The company’s liquid activities gained significantly, allowing for a 42% surge in performance fees. This could resume and might be assisted by recovering illiquid activities. However, there’s an argument that unfavorable capital structures could slow the growth of AUM (assets under management).

An interesting talking point is BlackRock’s 7% year-over-year increase in direct fund expenses, primarily due to lower index AUM. Investors should note that higher Q4 direct fund expenses are often normal due to seasonal rebate recognition.

The company’s product launch costs rose by 2% year-over-year, primarily driven by upgraded technology and innovation.

Lastly, BlackRock incurred a $191 million delayed compensation expense in its fourth quarter, which was backed out (of the firm’s financial statements) to adjust for non-core items.

It is perhaps trivial; however, we believe BlackRock’s prospects hinge on investors’ appetite. The firm’s business model is top-heavy, with fee reliance, correlating its operating cash flows with both public and private market investor sentiment.

The business’ profit margins and per-share value is extraordinarily attractive from an investors’ vantage point. This played a big hand in our decision to exercise a long-term bullish call on the firm (and its stock) as it displays resilience during trying economic periods.

BlackRock

Key Earnings Metrics

BlackRock’s history of earnings-per-share target beats indicates that it is an earnings momentum stock. Thus, providing prospects of stock price momentum. The momentum anomaly is a renowned quantitative concept in today’s financial markets, and continued earnings beats could send BlackRock’s stock into a cross-sectional momentum frenzy.

Seeking Alpha

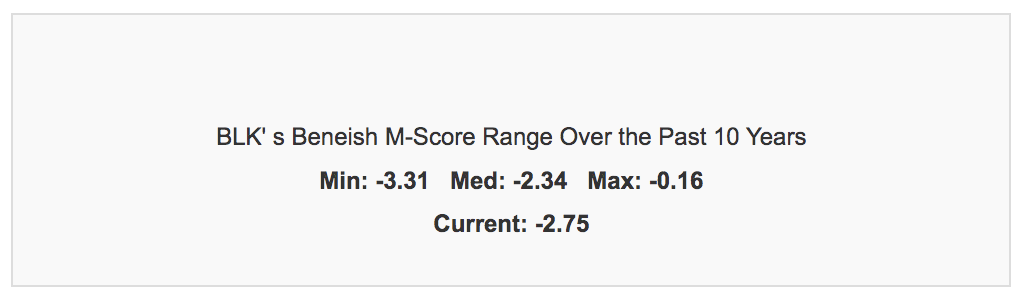

Retrospective data reveals that BlackRock is a conservative earnings recognition firm. Its midpoint Beneish M-score of -2.34 indicates that BlackRock rarely recognizes income statement line items prematurely. Therefore, likely phasing out earnings crash risk, which should be considered a positive by investors.

Beneish M-score (GuruFocus)

Valuation & Dividends

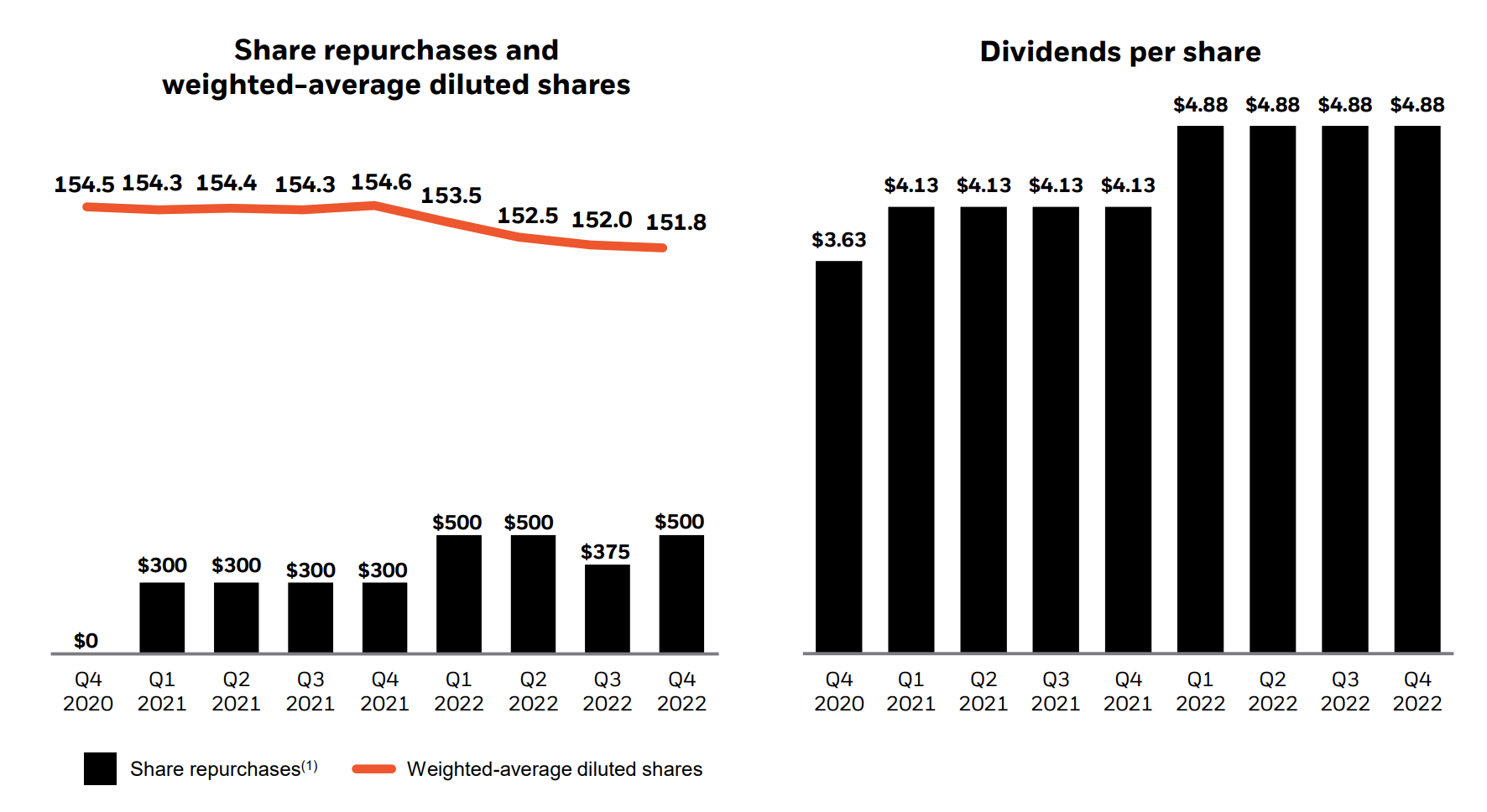

Although BlackRock’s weighted diluted EPS is trending downwards, the firm’s share repurchases remain lucrative, with another $500 million being executed in Q4, which speaks volumes given the uncertain economic climate.

Furthermore, although no distribution increases were made, the stock’s dividends per share are steady, with an approximate yield of 2.6%, providing investors with lucrative carry returns. We believe the stock’s dividend profile will remain consistent as BlackRock hosts robust operating cash flows.

BlackRock

Our relative valuation implies that BlackRock’s stock is in fair value territory. Given its latest EPS, the stock’s price-to-earnings ratio is at approximately 21.15x, which is slightly above its cyclical midpoint (19.52x GAAP). Although the result means that relative value risk can’t be denied, we don’t see this as a huge issue, as BlackRock’s stock has a history of elevated price multiples.

Risks

As previously mentioned, BlackRock is highly reliant on base fees. Therefore, the zeitgeist among private and public market investors will likely dictate its future operating performance. Market participants could remain subdued during 2023 as fears of a recession loom.

Furthermore, a market-based analysis suggests that BlackRock’s stock could be unfavorable among investors in today’s risk-off environment as its beta coefficient (1.28) stretches beyond that of a risk-off asset. We aren’t sure whether investors will have the appetite for high beta assets until tangible evidence of an interest rate pivot surfaces.

Concluding Thoughts

BlackRock’s fourth-quarter earnings beat could re-route its stock after its significant drawdown in 2022. Despite waning public and private markets, the company managed to navigate risks during its fourth quarter to provide its shareholders with additional residual value. Even though the stock hosts elevated valuation multiples, BlackRock’s robust profit margins and its consistent dividend profile offer investors much hope of steady value creation.

Be the first to comment