Andrew Burton

Blackrock (NYSE:BLK) is the world’s largest asset manager, with over $8 trillion in assets under management. The company effectively “owns the market” through its family of exchange-traded funds [ETFs], under the “iShares” brand name. Given many analysts have forecast a recession, one would imagine that this gigantic asset manager would be feeling the pain. However, the company recently reported solid financial results for the fourth quarter of 2022, beating both top and bottom-line growth estimates. In this post I’m going to break down these financial results before diving into the valuation, let’s dive in.

Solid Fourth Quarter Financials

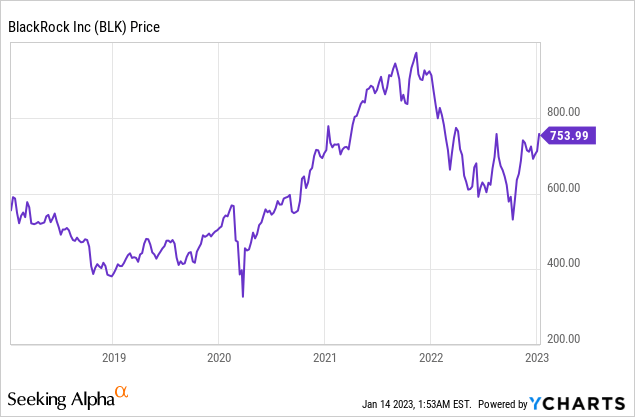

Blackrock reported solid financial results for the fourth quarter of 2022. Revenue was $4.337 billion, which beat analyst expectations by ~$68 million. This was despite declining by $769 million over the year. This was mainly driven by $572 million less in “base fees”. In addition, performance fees were $101 million less, which makes sense due to the poor market performance of 2022. Advisory services also took a hit of $16 million, as many investors are in a state of uncertainty. A positive is quarter over quarter, revenue actually increased by $26 million, driven by better market performance and thus higher performance fees.

Revenue Blackrock (Q4,22 report)

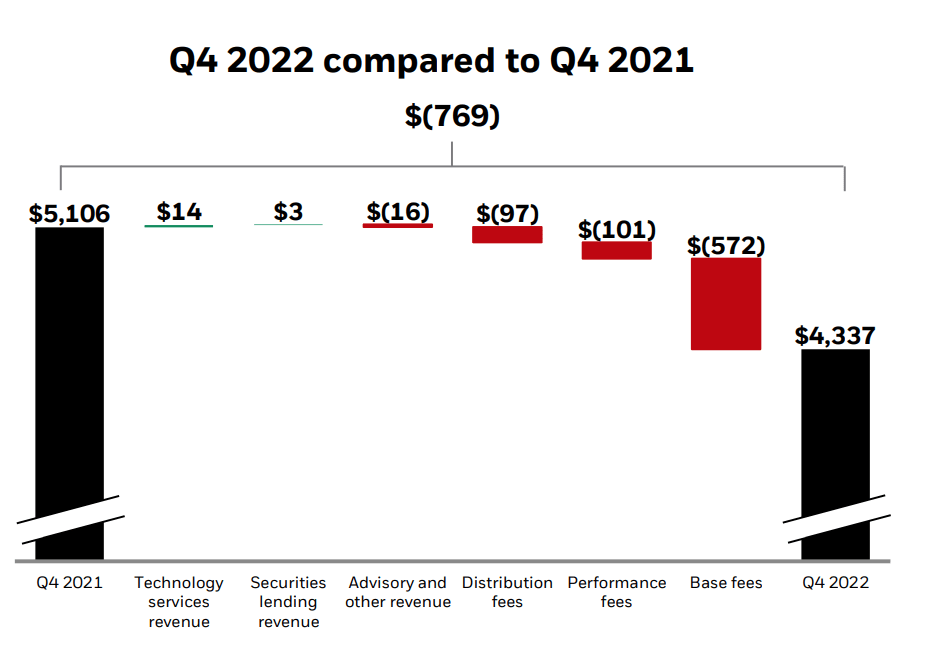

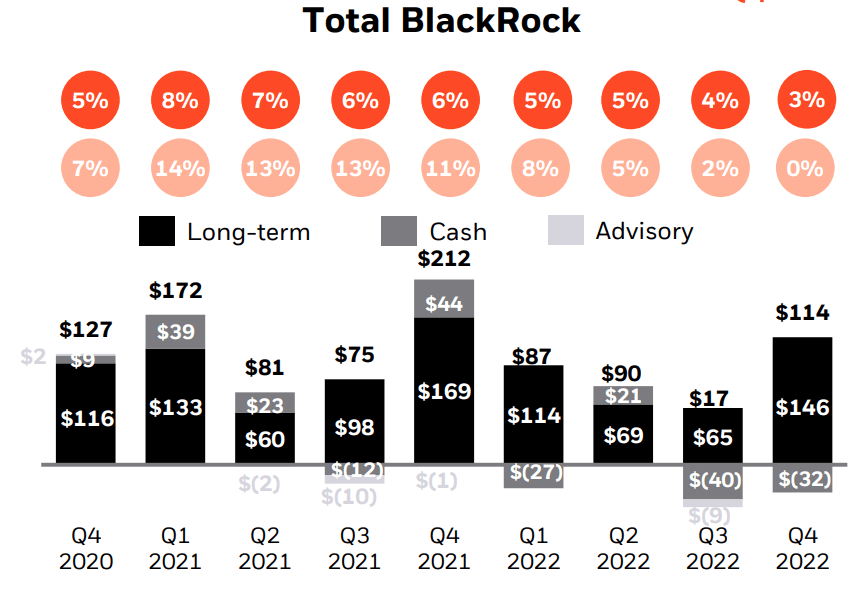

Blackrock reported solid inflows of $308 billion year over year, despite a tough economic backdrop. The fourth quarter reported the largest inflows of the year with $114 billion reported, up from the $17 billion in the third quarter of 2022. This shows investors are seeing value in the market and are starting to put capital to work.

Blackrock Inflows (Q4,22 report)

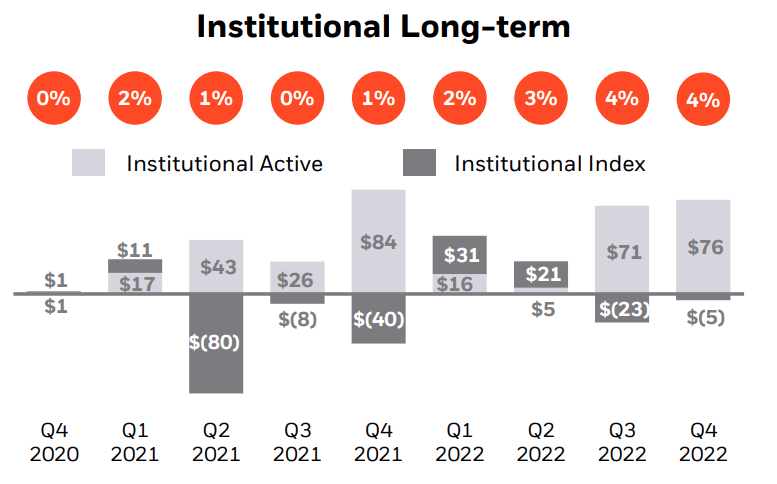

In Q4,2022, the majority ($90 billion) of the $114 billion in net inflows was driven by investments into Blackrock’s leading ETFs. The company offers some of the lowest fee’s in the industry, which entices investors to purchase. For example, the iShares S&P 500 Core ETF has an expense ratio of just 0.03%. This is level with competitor Vanguard which charges an 0.03% expense ratio for its Vanguard S&P 500 ETF, although iShares was cheaper prior. Most active fund managers or “hedge funds” generally charge a “2/20” fee structure, which means a 2% fee on assets and an eye-watering 20% on performance over a benchmark. This makes “passive ETF” investing much more cost-effective, especially given the majority of active fund managers, don’t outperform the market. To beat the market it effectively requires a fund manager to find the “needle in the haystack”, the one or two winning stocks. This is extremely difficult and thus the founder of Vanguard Jack Bogle suggests buying the “entire haystack”. The low fees Blackrock offers are only economical for the business, due to its massive scale ($10 trillion in assets under management), therefore this acts as a barrier to entry against competitors. For large pension funds, institutional investors, and even individual investors, a 0.5% fee difference can make a huge impact on final investing results. By investor type, Institutional investors drove the majority, 66.7% or $76 billion in net inflows, as they aim to take advantage of the low market prices.

Institutional inflows (Q4,22 report)

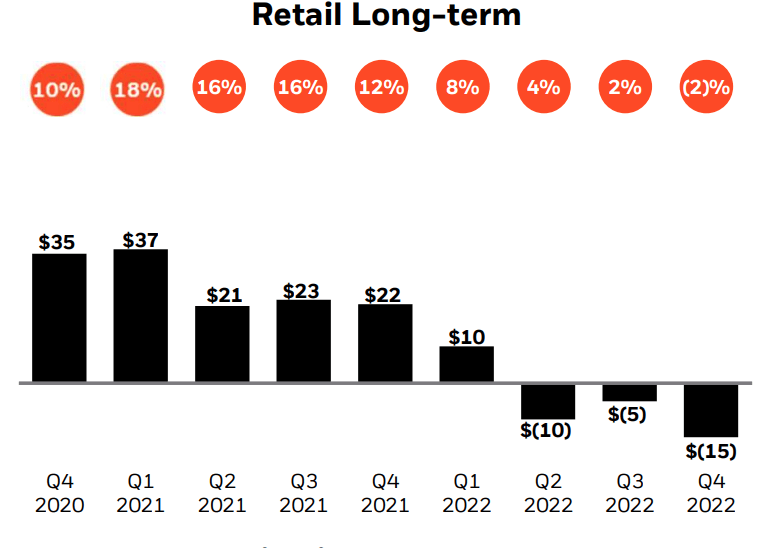

Interestingly enough, retail investors look to be still spooked by the market conditions and this cohort’s net outflows reached negative $15 billion. The average retail investor was extremely active during 2020 and we saw a staggering $35 billion in inflows for Blackrock’s funds in Q4,2020. This was driven by stimulus checks, “free trading” applications and a surge in retail activity. However, I believe this “irrational exuberance” turned a stock market crash into a bubble. We are now feeling the market effects of this and given the high inflation and rising interest rate environment, the average person on the street is feeling the pinch. The psychological impact also plays a key part in retail investor activity, as “fomo” can cause a surge in buying activity like we saw in 2020. However, in 2022 we have seen the opposite, a fear stricken retail investor paralyzed by uncertainty. This is normal and the positive for Blackrock is both economic conditions and the stock market tends to be cyclical. There is an old joke that “financial memory” is relatively “brief” and thus market cyclicality is expected.

Retail outflows (Q4,22 report)

Blackrock reported “record” sales of its Aladdin portfolio management software which increased quarterly revenue by 4% year over year. For the full year, its technology services revenue increased by 7% year over year to a huge $1.4 billion. The company also reported an 8% year-over-year increase in “Average Contract Value”, or ACV, which was a positive.

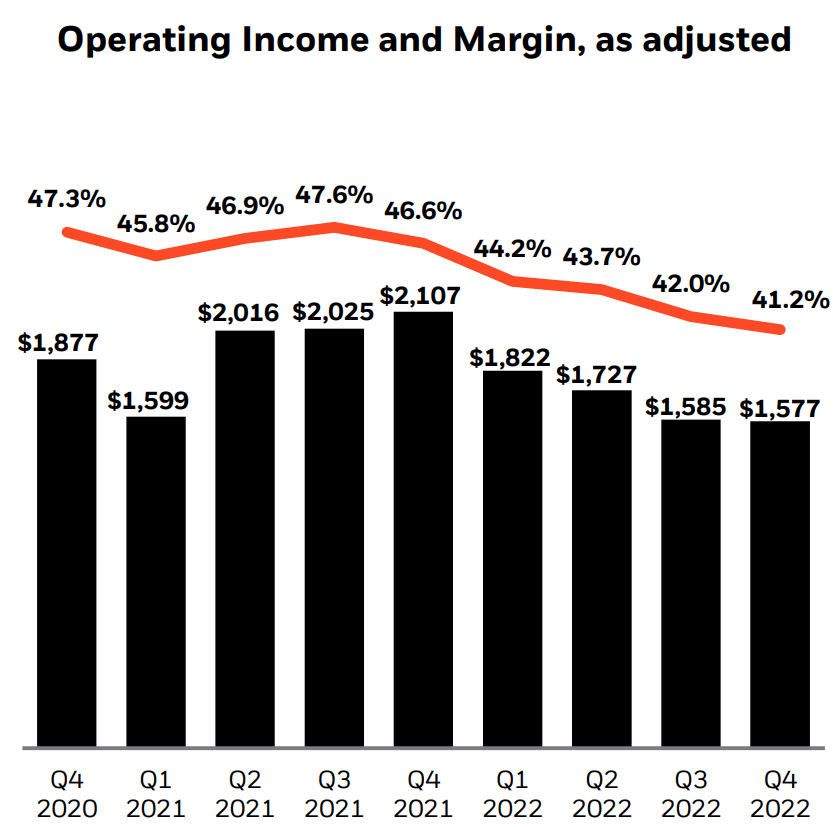

Onto profitability and margins, Blackrock reported earnings per share [EPS] of $8.29, which beat analyst estimates by $0.23, despite declining by 22.46% year over year. Its operating income was $1.577 billion at a 41.2% operating margin. This was lower than the $2.1 billion and 46.6% operating margin reported in Q4,21. Its lower margin was mostly driven by foreign exchange headwinds and a tough market backdrop.

Operating Margin (Q3,22 report)

A positive is Blackrock has been focusing on reducing its “discretionary expenses”. The company reported 4% in total expenses, which was related to lower employee compensation expenses, driven by lower performance fees and operating income. Blackrock has also recently announced it has slashed 500 jobs, which of course is not great for the individuals but will of course help with expense management moving forward. Although this news made headlines I think it’s a good idea to “zoom out'” and keep perspective. Blackrock employs approximately 18,000 people, thus this cut is only ~2.5% of its total. Blackrock’s employee count is also still ~5% higher than last year. In addition, this move was part of a “restructuring” which actually cost the company ~$91 million in severance and related costs. Therefore the company should have a leaner cost structure moving forward, once these costs are absorbed.

Blackrock has a solid balance sheet with cash and short-term investments of $6.5 billion. The company does have a fairly high total debt of $8.4 billion, but the majority ($6.59 billion) is long-term debt.

Moving forward I expect Blackrock to focus increasingly on building up its portfolio of “uncorrelated” assets in the market. The “holy grail” of investing is a collection of assets that are “uncorrelated to the general market”. For example, Blackrock recently announced an agreement to form “Gigapower”, a joint venture AT&T. This will basically allow Blackrock and AT&T to build/own digital infrastructure such as fiber optic networks, for the internet as assets. I personally think this is a fantastic strategy, as I believe the “internet” is really the next major utility after water and electricity. Therefore whoever owns the assets effectively has a toll road on global communications.

Advanced Valuation

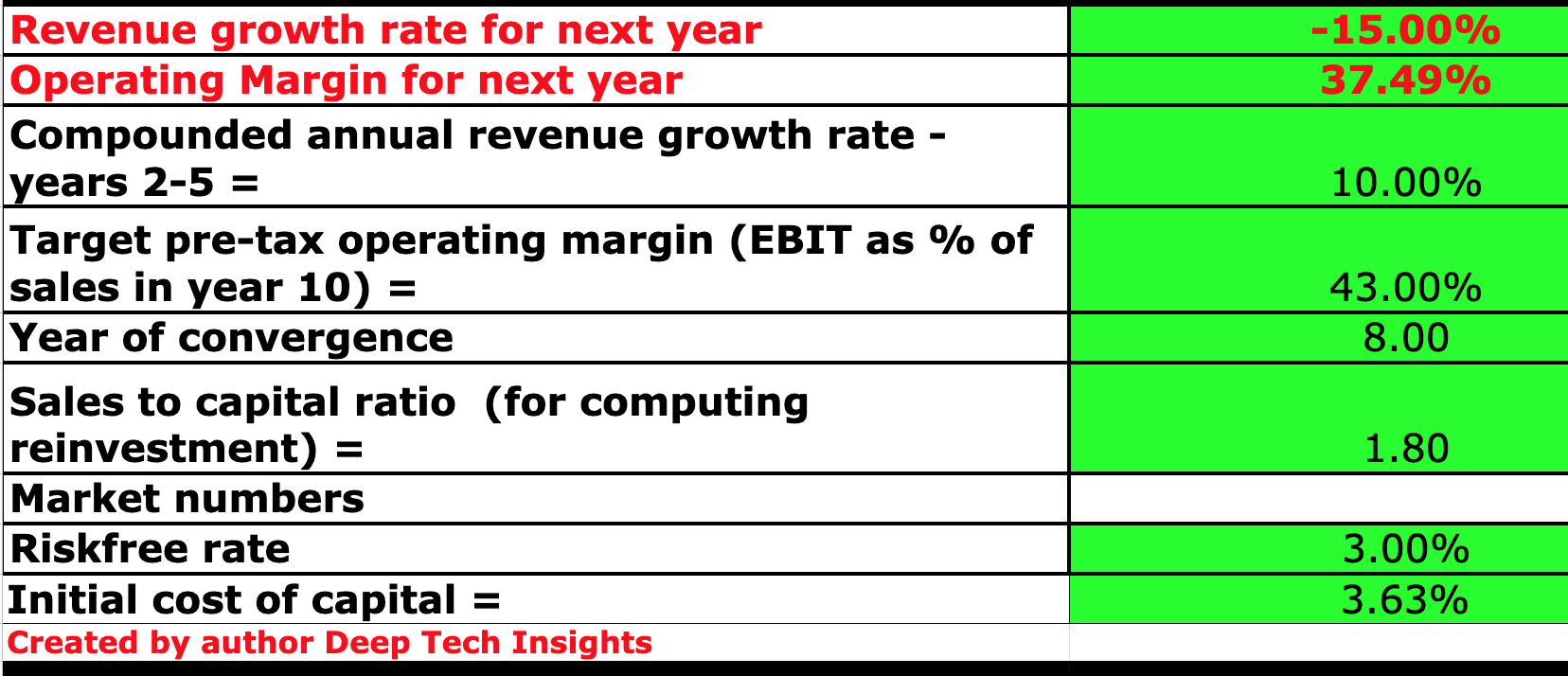

Valuing Blackrock is fairly challenging as this is a gigantic complex company. However, I have plugged its latest financials into my discounted cash flow model. I have forecast negative 15% revenue growth for next year, which I expect to be driven by the forecasted recession, which could cause greater retail investor outflows, as many people “sell at the bottom”. The positive is in years 2 to 5, I have forecast 10% revenue per year which is aligned with pre-pandemic levels and assuming a cyclical rebound in the economy.

Blackrock stock valuation 1 (created by author Deep Tech Insight)

I have also forecast an improvement in the operating margin to 43% over the next 8 years. I expect this to increase as performance fees are likely to improve given improving economic conditions.

Blackrock stock valuation 2 (created by author Deep Tech Insights)

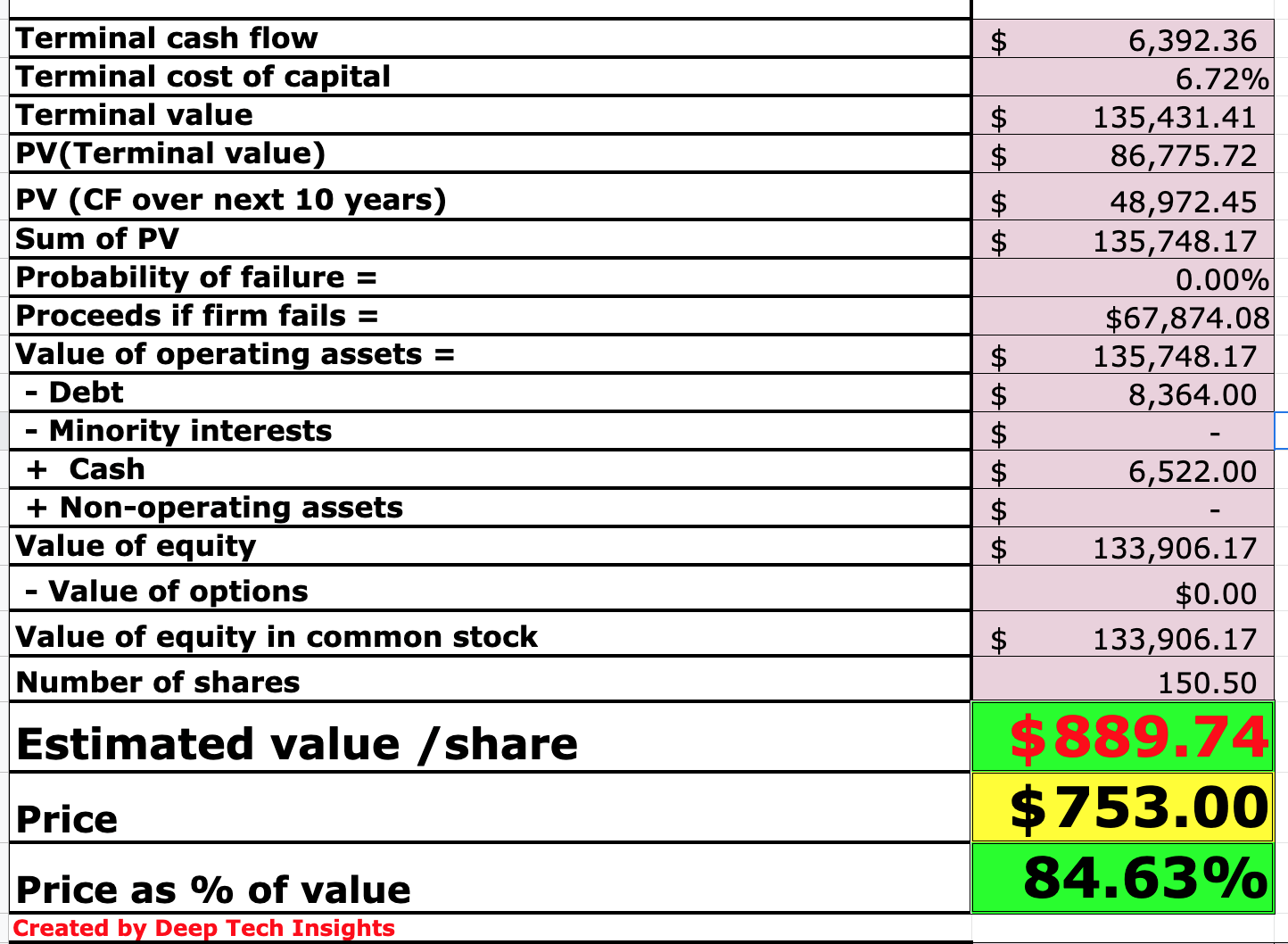

Given these factors, I get a fair value of $889 per share, therefore the stock is ~15% undervalued intrinsically at $753 per share.

Risk

Recession/market conditions: Many analysts have forecast a recession in 2023, therefore I expect continued outflows by the retail investor due to the aforementioned high inflation and rising interest rate environment.

Final Thoughts

Blackrock is an investment industry titan, which has a strong market position with its scale acting as a competitive advantage. The company is currently facing temporary headwinds, due to the economic environment. However, despite this, the company has still beaten its financial estimates. I believe its alternative investments in areas such as fiber optics is a solid strategy, given the investor demand for “uncorrelated assets”. Its stock is undervalued intrinsically and thus it could be a great long-term investment.

Be the first to comment