Floriana

The BlackRock Innovation & Growth Trust (NYSE:BIGZ) is a venture capital fund wrapped in a CEF structure offering investors exposure to pre-IPO investments that are typically not available to retail investors. It also pays an attractive 12.3% current yield funded through return of capital.

During equity bull markets, pre-IPO venture investments can add significant returns to a portfolio, as early stage companies can seek exits via sales to other companies or IPOs to the public markets. Unfortunately, the IPO market is currently in a deep freeze and large technology companies are more concerned with cutting costs than acquiring startups. I would stay away from the BIGZ fund until the market environment improves and exits become viable again.

Fund Overview

The BlackRock Innovation & Growth Trust is a closed-end fund (“CEF”) that primarily invests in small to mid-capitalization companies the investment manager deems to be ‘innovative’.

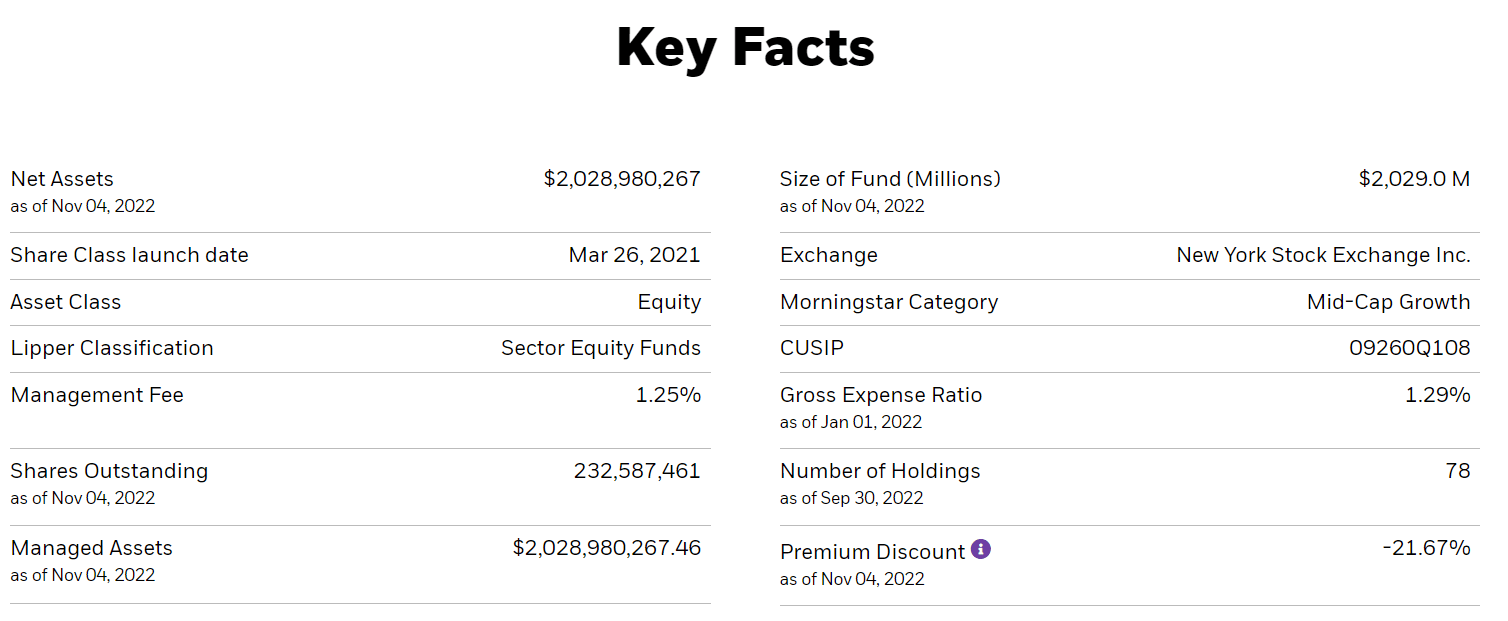

The fund has over $2 billion in assets and is trading at a steep 21% discount to NAV (Figure 1).

Figure 1 – BIGZ key facts (blackrock.com)

Strategy

The BIGZ fund’s investment objective is to provide total return through a combination of income, current gains, and long-term capital appreciation. To achieve its investment objective, the fund will primarily invest in companies that have introduced or are looking to introduce a new product or service that can potentially change their respective marketplace. The fund also writes call options on investment holdings to generate current income.

Portfolio Holdings

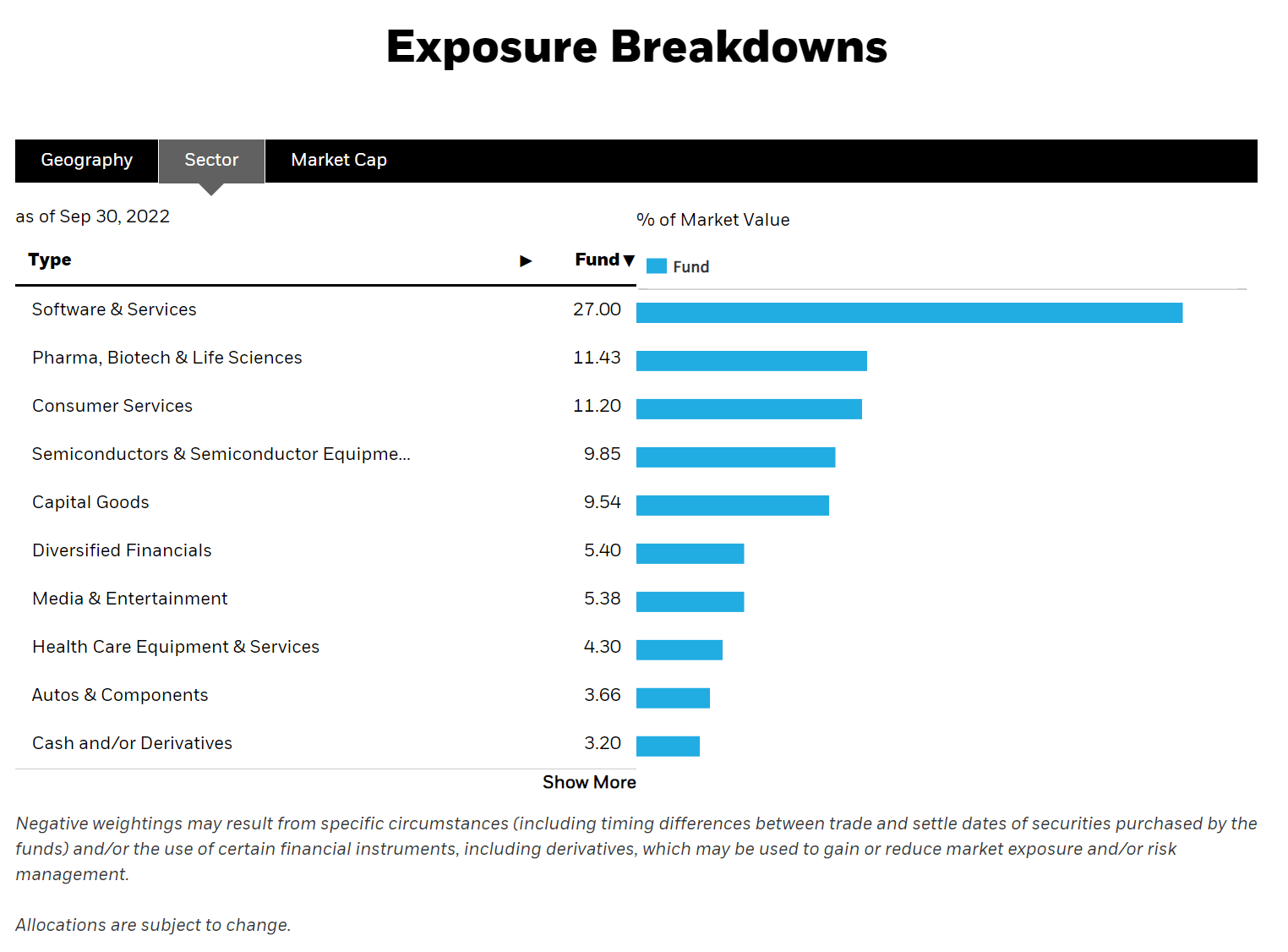

As the fund is aiming to invest in innovative companies, its portfolio holdings resemble that of a ‘technology’ or ‘growth’ fund, with large allocations to software (27.0%), biotech (11.4%), consumer services (11.2%), and semiconductors (9.9%).

Figure 2 – BIGZ fund sector exposure (blackrock.com)

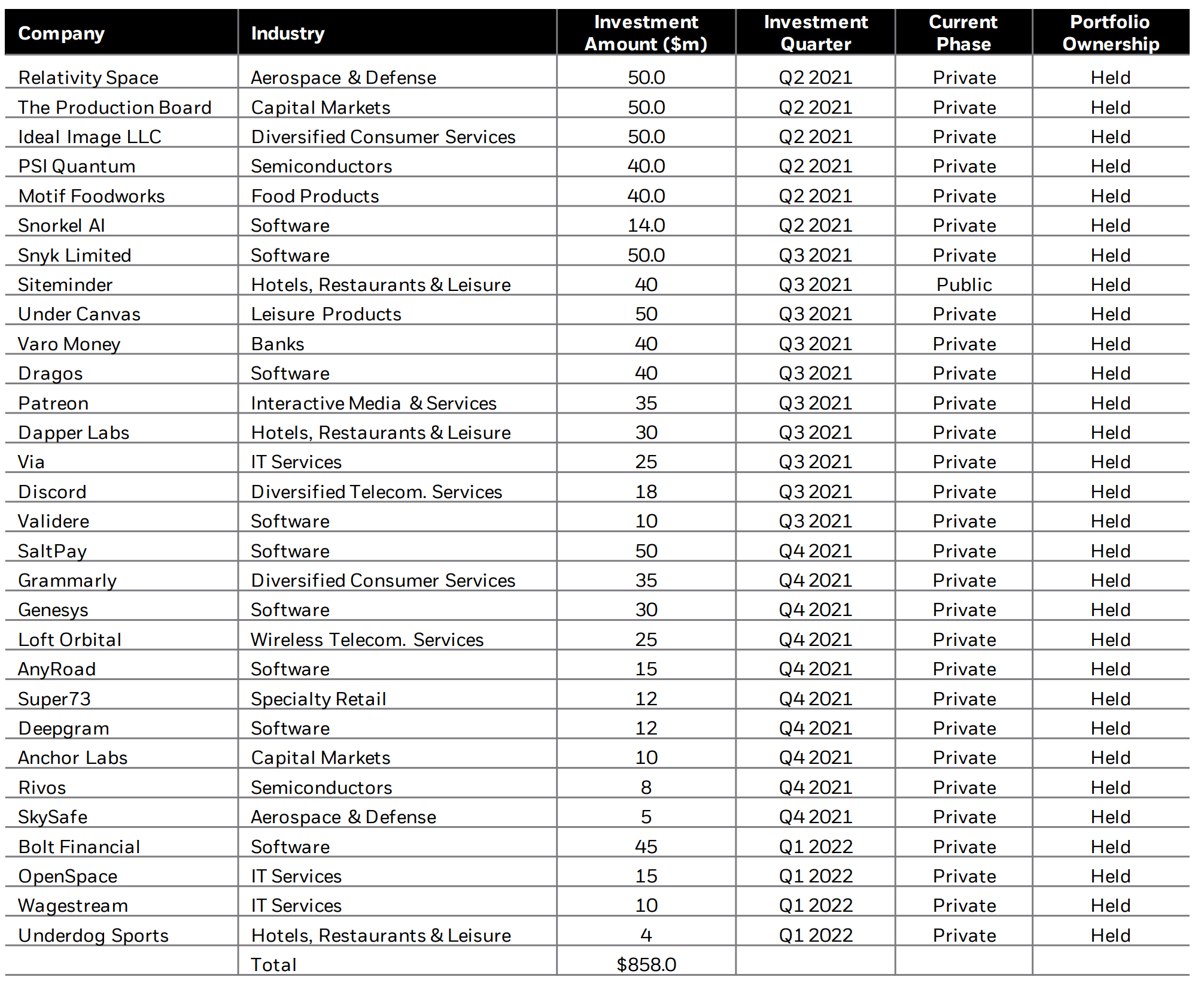

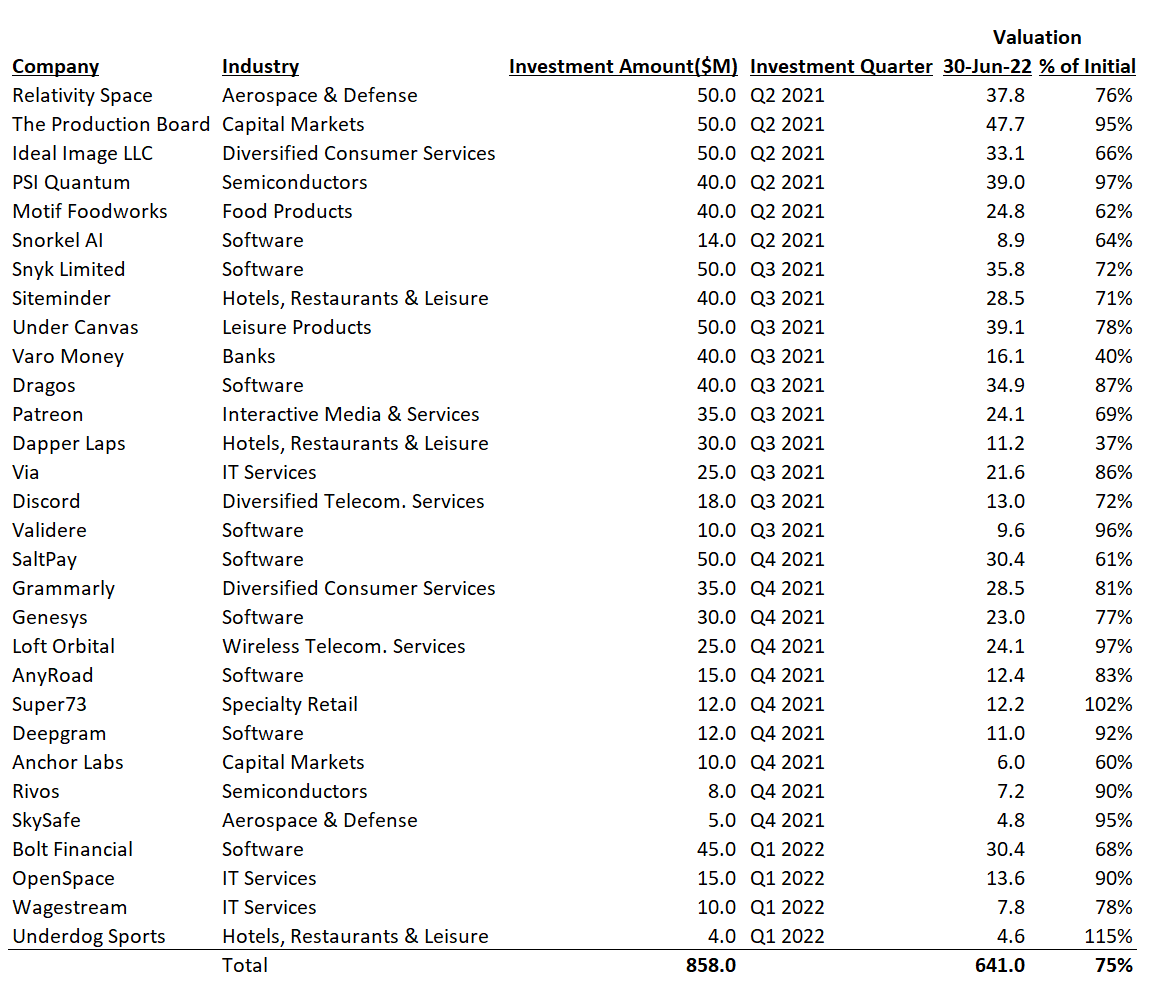

Another feature of the BIGZ fund is its large weight to private investments. The fund aims to invest up to 25% of assets into private investments. As of the end of Q2/2022, the fund’s allocation in privates was 27.4%, as the value of the public investments fell. In total, the fund invested $858 million across 29 privates as of June 30, 2022 (Figure 3).

Figure 3 – BIGZ private investments (blackrock.com)

Returns

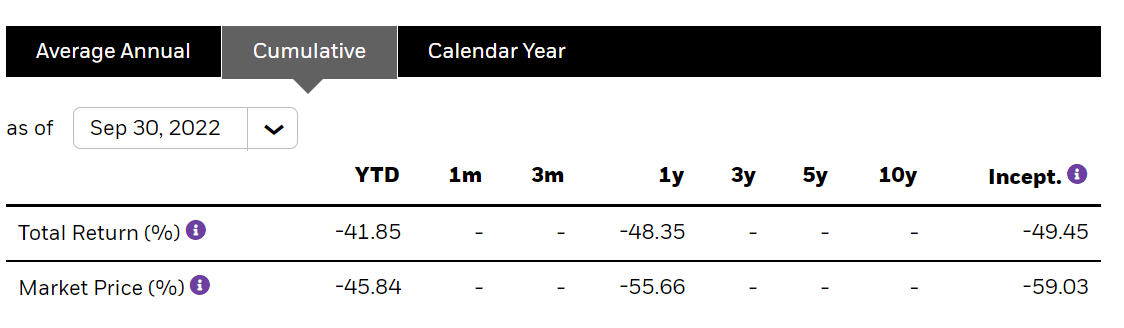

The BIGZ fund was only launched in March 2021, so it has a limited operating history. However, in the short time the fund has been live, it has lost about half its value (on NAV basis, the fund has lost 49.5% since inception), with most of the losses occurring YTD in 2022 (Figure 4).

Figure 4 – BIGZ returns (blackrock.com)

Distribution & Yield

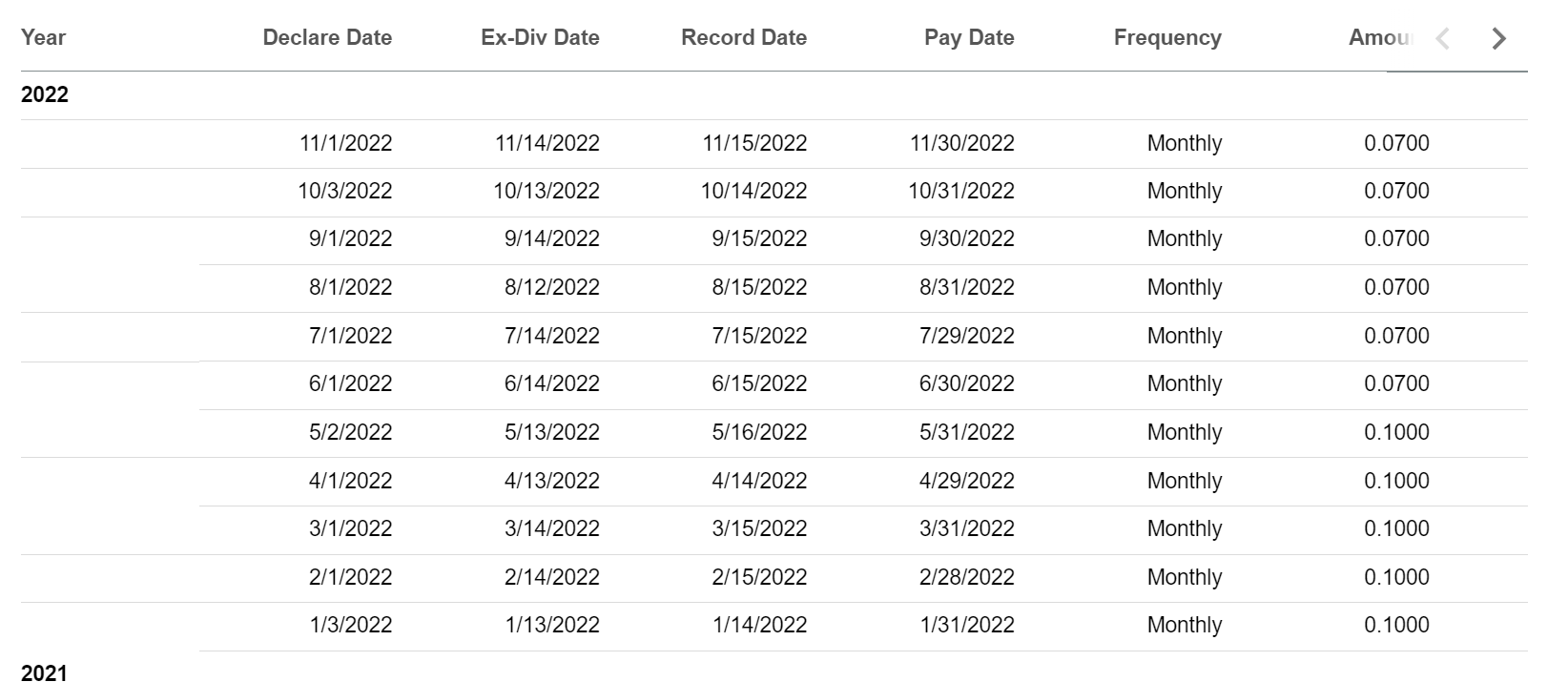

One of the main attractions of the BIGZ fund is its high distribution yield. However, the trailing 12M distribution figure of $1.05 / share is misleading, as the monthly distribution was cut from $0.10 to $0.07 in June 2022 (Figure 5). At the current distribution rate of $0.07 / month, the fund is yielding 12.3% on market price and 9.6% on NAV.

Figure 5 – BIGZ distribution in 2022 (Seeking Alpha)

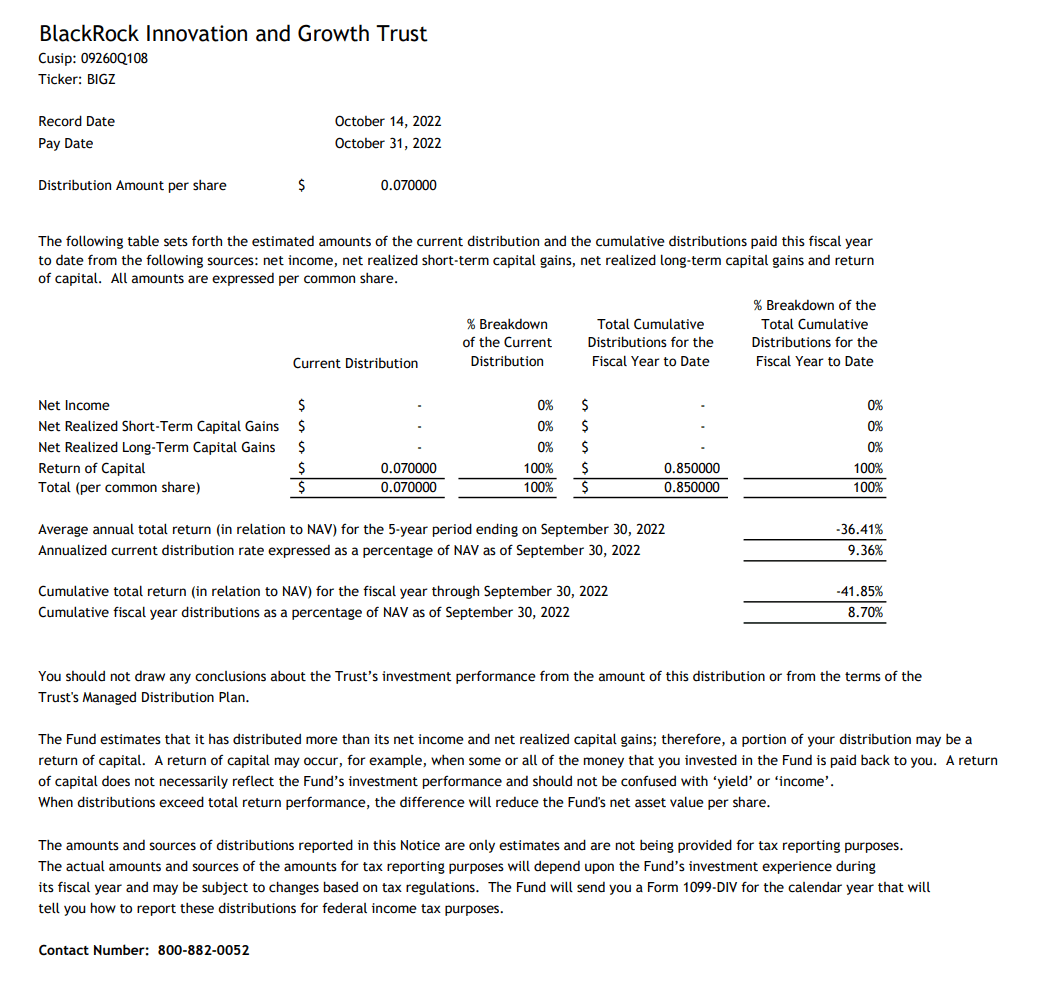

BIGZ’s distribution is funded through return of capital (“ROC”) (Figure 6).

Figure 6 – BIGZ’s distribution is funded through return of capital (blackrock.com)

Fees

The BIGZ fund charges a management fee of 1.25% and has a gross expense ratio of 1.29%.

Private Investments Are High Risk High Reward

As I have written before, pre-IPO private investments can offer phenomenal returns. For example, Sequoia Capital famously turned a $60 million investment in messaging app WhatsApp into $3 billion when the WhatsApp was sold to Facebook in 2014. However, venture capital investing is also fraught with risks, as venture capital returns follow the Pareto principle, where 80% of returns come from 20% of the investments. Often, a venture capital fund will lose money on most of its investments, but 1 or 2 home runs will ‘carry the fund’ and then some. Unfortunately, it is impossible to know beforehand which investment is going to be a winner and which is going to be a loser.

One of the biggest drawbacks to venture capital investing is the unpredictable nature of cash flows and why it is unavailable in a mutual fund / ETF setting. Since most of these investments are in high growth, early stage companies, the investments typically do not pay dividends and rarely have earnings. Instead, venture capital funds rely on ‘exits’, either a sale of the investment to a bigger company like WhatsApp/Facebook, or a public listing (via IPO or SPAC) of the investment, to generate cash flows and returns to investors. The timing of exits is unpredictable, and usually requires a ‘bull market’ environment. Investors in venture capital funds need to have extremely high patience and tolerance for long periods of little to no liquidity.

BIGZ Is A Venture Capital Fund In Disguise

What is interesting with a fund like BIGZ is its attempt to wrap an illiquid venture capital fund into a perpetual ‘closed-end’ fund structure. The CEF structure means that investors in BIGZ cannot redeem their units like in a mutual fund. When investors want their capital back, they sell shares of the fund to someone else, and the capital remains within the fund; there is no forced liquidation of the funds’ investments.

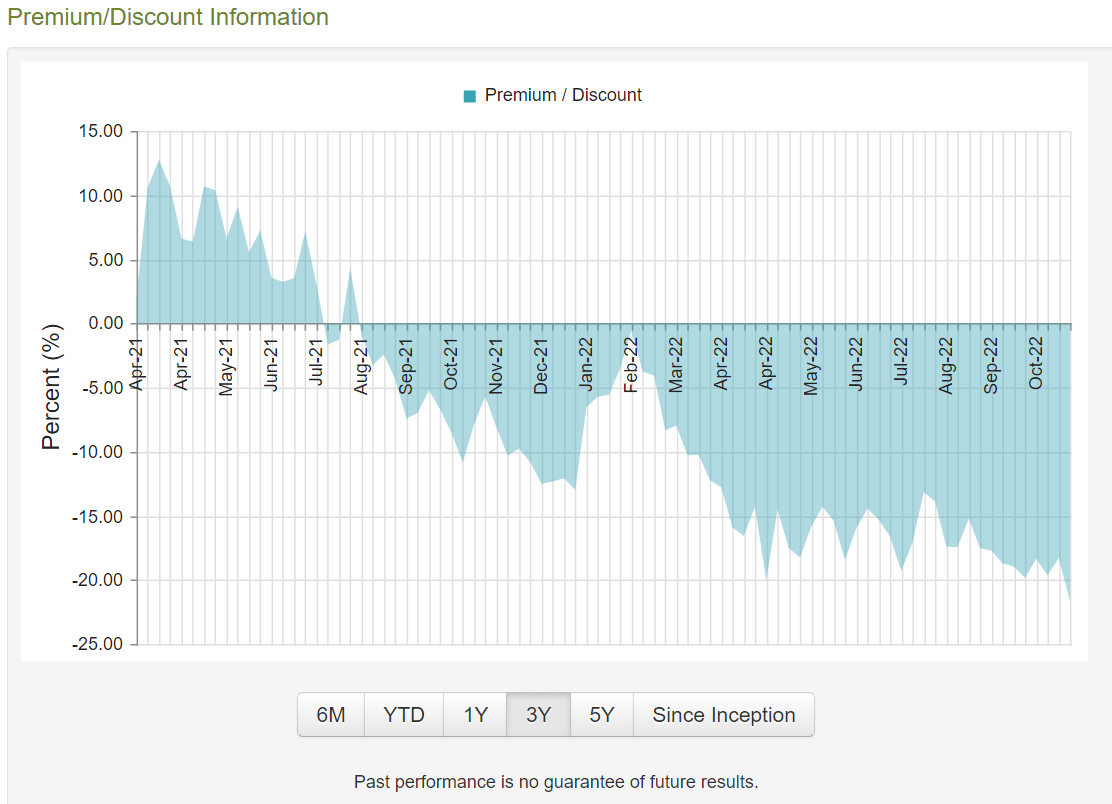

The worst that can happen to a CEF is it trades at a significant discount to the fund’s NAV, as there is no ‘demand’ for the fund’s shares. Currently, the BIGZ fund is trading at a steep 21% discount to NAV (Figure 7).

Figure 7 – BIGZ discount to NAV (cefconnect.com)

The steep discount could also be a sign that fund investors do not trust the mark-to-market valuation of the funds’ private investments. For example, in the BIGZ fund, according to the latest semi-annual report as of June 30, 2022, the private investment portfolio was marked at 75% of the initial investment (Figure 8).

Figure 8 – BIGZ private investments valuation (Author created with data from the semi-annual report to June 30, 2022)

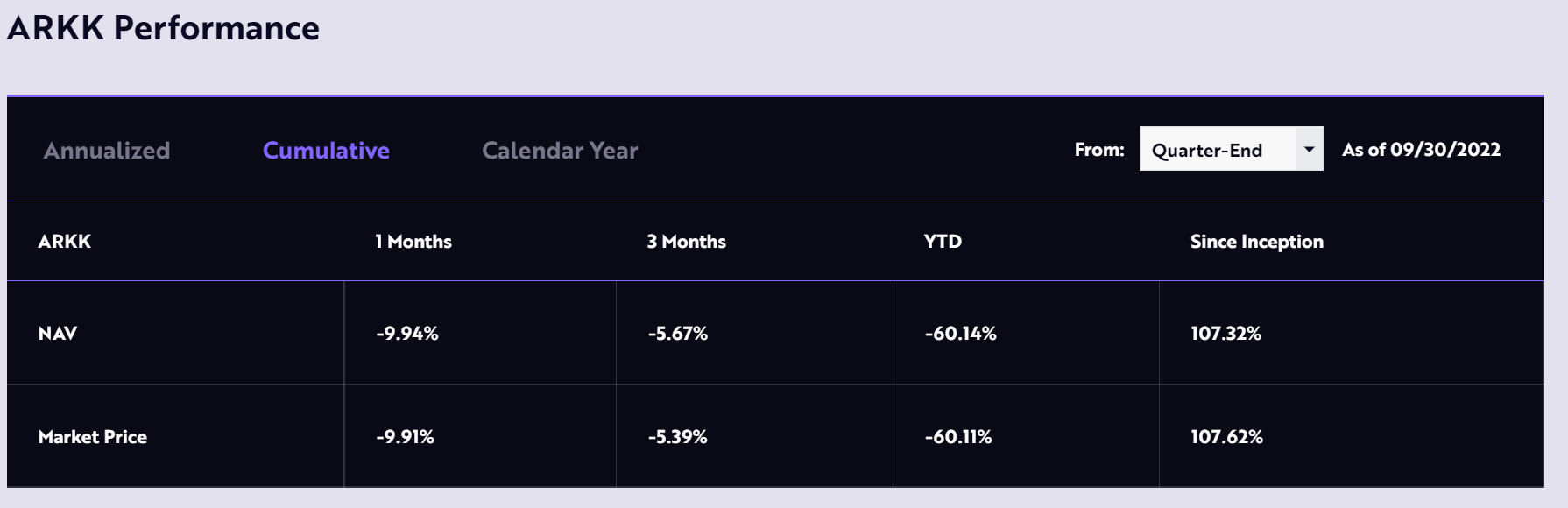

However, we know from tracking public ‘innovation’ fund peers like the ARK Innovation ETF (ARKK) that 2022 has been an abysmal year, with ARKK returning -60.1% YTD to September 30, 2022 (Figure 9).

Figure 9 – ARKK ETF 2022 returns (ark-funds.com)

It is highly improbable that BIGZ, with a 25% weight in private investments that should make it riskier, can outperform the ARKK ETF by almost 20% with a -41.9% YTD return to September 30, 2022. Therefore, sceptical investors have punished the BIGZ fund by marking down its market price by 59.0% YTD (similar to ARKK’s YTD performance).

Conclusion

In conclusion, The BlackRock Innovation and Growth Trust is a venture capital fund in disguise offering investors exposure to venture investments that are typically not available to retail investors. It also pays an attractive 12.3% current yield funded through return of capital.

During equity bull markets, venture investments can add significant returns to a portfolio, as early stage companies can seek exits via sales to other companies or IPOs to the public markets. Unfortunately, the IPO market is currently in a deep freeze and large technology companies are more concerned with cutting costs than acquiring startups. I would stay away from the BIGZ fund until the market environment improves.

Be the first to comment