da-kuk

Thesis

BlackRock Enhanced International Dividend Trust (NYSE:BGY) is an equity focused closed end fund. The fund has current income as its primary objective, and as per its literature:

Under normal circumstances, the Fund invests at least 80% of its net assets in dividend-paying equity securities issued by non-U.S. companies. The Fund may invest in securities of companies of any market capitalization, but intends to invest primarily in securities of large capitalization companies. Under normal market conditions, the Fund generally intends to write covered call and put options with respect to approximately 30% to 45% of its total assets, although this percentage may vary from time to time with market conditions.

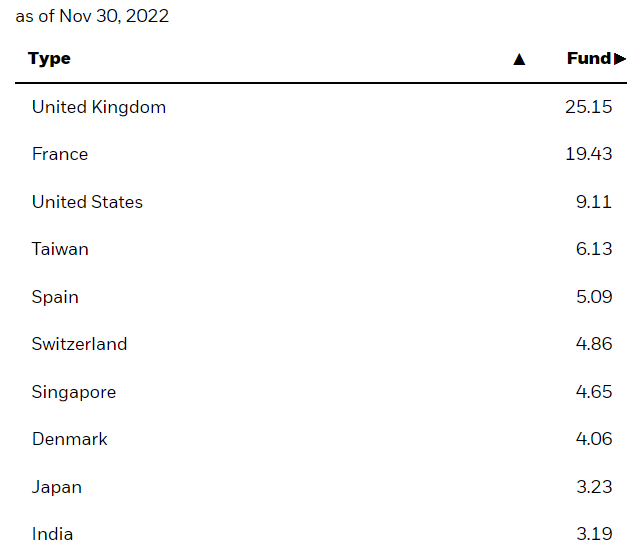

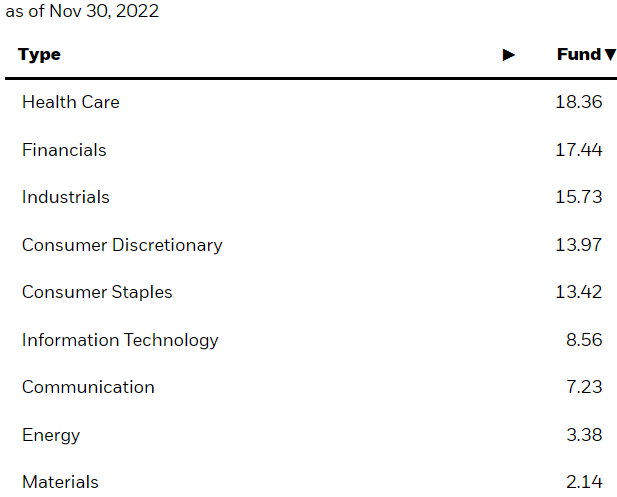

Currently the fund is defensive being overweight the healthcare sector. From a geographic standpoint the U.K and France are the highest exposures. Around 40% of the portfolio is currently overwritten with single name covered calls. We like this strategy in a down market since it will be able to generate income when stocks decline and volatility increases.

The CEF is a well run, large capitalization stock vehicle. It does what it is supposed to in terms of utilizing implied volatility and covered calls to generate a total return in a down market. The CEF has a total return profile that is in line with a generic ETF in the space, namely the Vanguard International High Dividend Yield ETF (VYMI). With monthly dividend distributions the CEF is checking all the right boxes – it transforms international equity market returns into monthly dividends with a performance that equates a generic ETF in the space. We would like to see outperformance, but we cannot always get what we want, plus there is the issue with management fees coming out of the fund.

So from a structure/wrapper perspective BGY checks all the boxes. However, from an asset class perspective, total returns are fairly muted here, with annualized total returns at only 5%. The international large cap market seems to have severely trailed the U.S. one, and BGY will not be able to get around that.

BGY Analytics

AUM: $0.5 bil

Discount to NAV: -13.5%

Z-Stat: -1.66

Yield: 8%

St Dev: 14.6

Sharpe Ratio: 0.2

BGY Holdings

The vast majority of the portfolio is from equities outside of the U.S.:

Countries (Fund Fact Sheet)

The fund has a defensive stance, being overweight health-care names:

Sectors (Fund Fact Sheet)

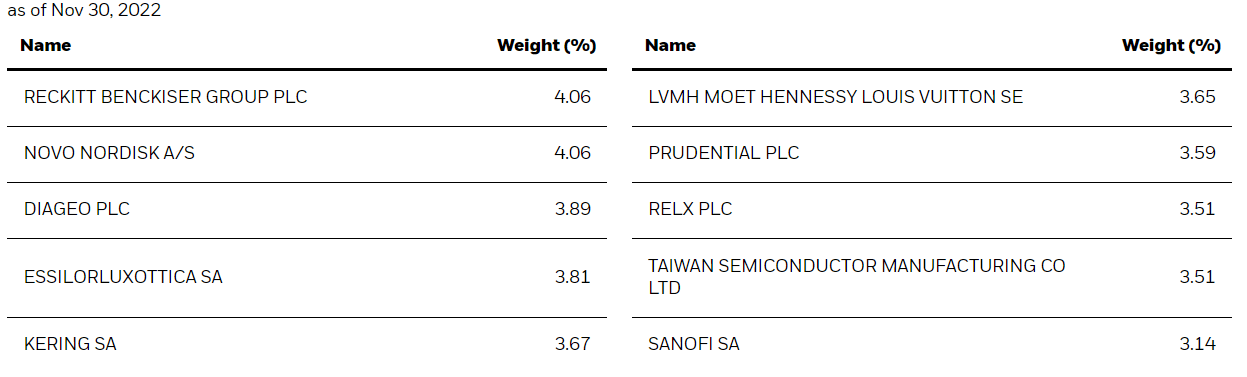

As of the writing of this article, the top names in the portfolio are:

Top Names (Fact Sheet)

Currently around 40% of the portfolio has covered calls written against it:

Portfolio Details (Fund Fact Sheet)

Covered calls are a smart way to generate income in a down market. We like the fact the fund is utilizing this feature. The CEF pursues the single stock option avenue, not the index covered call writing.

BGY Performance

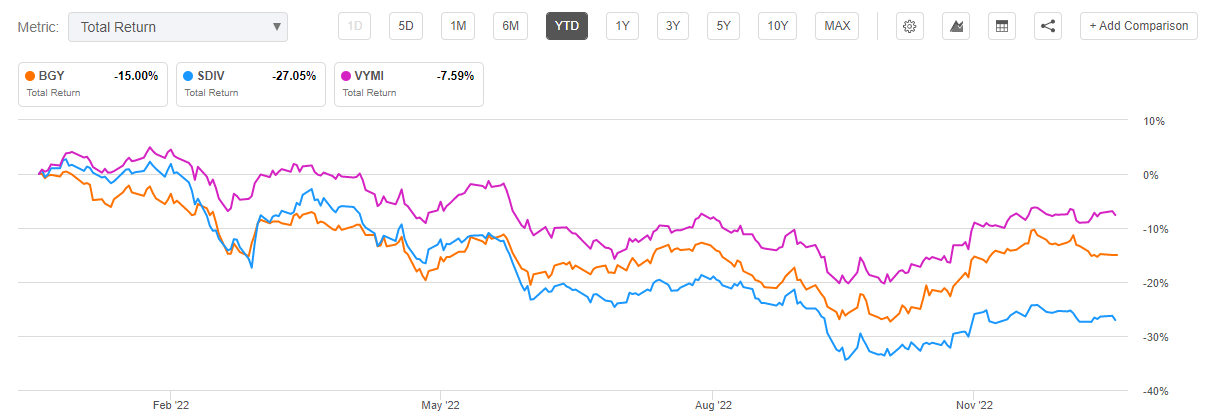

The fund is down -15% year to date, outperforming the S&P 500, but underperforming a similarly focused ETF, namely the Vanguard International High Dividend Yield ETF:

Total Return (Seeking Alpha)

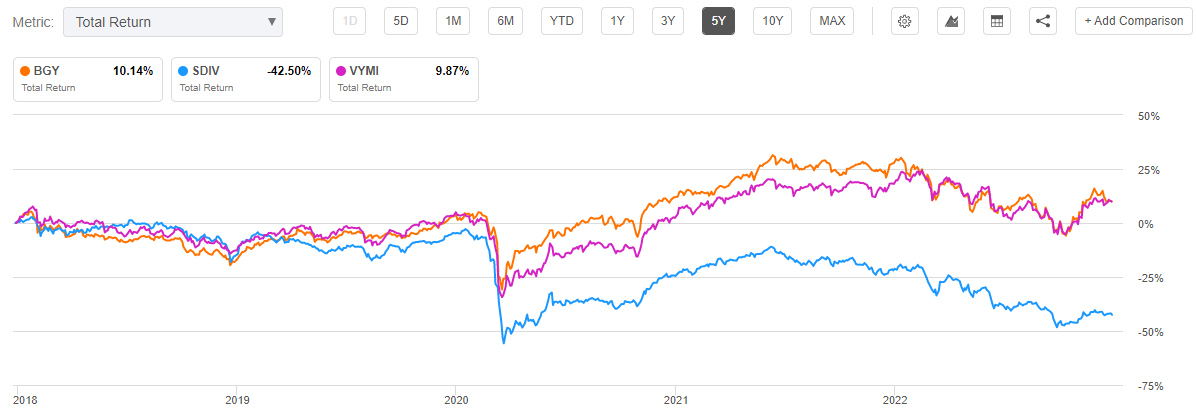

On a 5-year basis the two have almost an identical total return:

Total Return (Seeking Alpha)

We can observe that BGY actually outperformed VYMI during the 2020-2022 period, which is a positive for the fund. We want to see actively managed structures like CEFs outperform simple ETFs in the asset class.

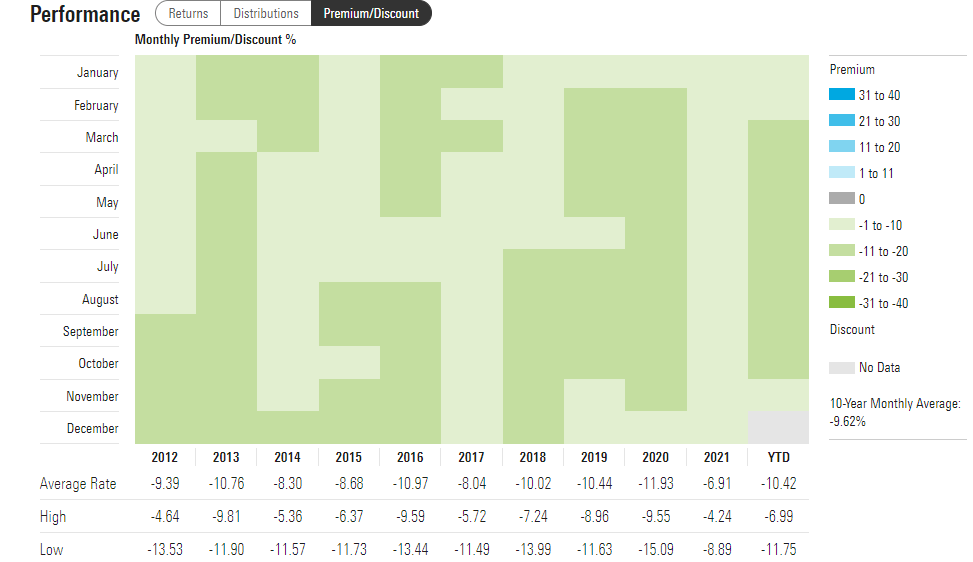

Premium / Discount to NAV

The fund has always traded at a discount to NAV:

Premium/Discount (Morningstar)

We can see that in the past decade the CEF never moved to a premium to NAV. At the moment the fund’s discount is closing in on historic wide levels. We can see from the above chart that the widest levels occurred in 2020 when it moved to -15%.

Distribution

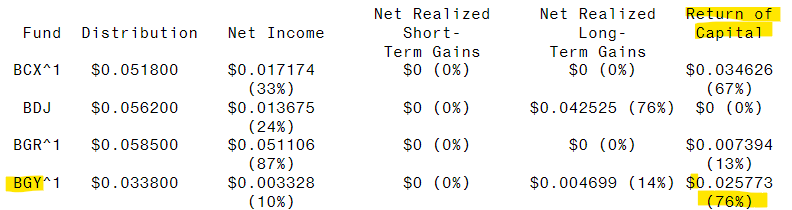

Given the poor equities performance in the past year, the CEF is now utilizing a very high amount of ROC to sustain the distribution:

Distributions (Section 19a)

As of the latest distribution date the return of capital amount utilized is 76%. That is a very high figure, and we expect that amount to persist as long as international equities do not generate any capital gains. Cash disbursed by equity CEFs does not come from thin air – it is received either via stock dividends or from selling equities that have generated capital gains.

Conclusion

BlackRock Enhanced International Dividend Trust is an equity focused closed end fund. The CEF invests in dividend paying international stocks with an option overlay. From a geographic standpoint, the UK and France are currently the highest exposures. From a sectoral standpoint, healthcare and financials represent the largest concentrations. The CEF checks all the right boxes from a structure perspective, having a similar performance as a vanilla ETF in the space, and transforming international equity capital gains into monthly dividends. The fund’s current dividend yield of 8% is not supported, with the latest Section 19a notice showing a 76% return of capital utilization. This is to be expected, given equity market underperformance in 2022. Long-term, though, the fund should be thought of as a 5% annualized total return vehicle, given the relative modest performance in the chosen asset class, namely dividend paying international large caps. BGY is correctly utilizing all the tools at its disposal to create an efficient structure, but the underlying asset class does not help. Holders in the name should expect a much brighter 2023 as equities will recover in the second half. New money looking at the space should expect much more modest long-term annualized total returns when compared to the U.S. equity sector.

Be the first to comment