Jonathan Kitchen

Investment Rate

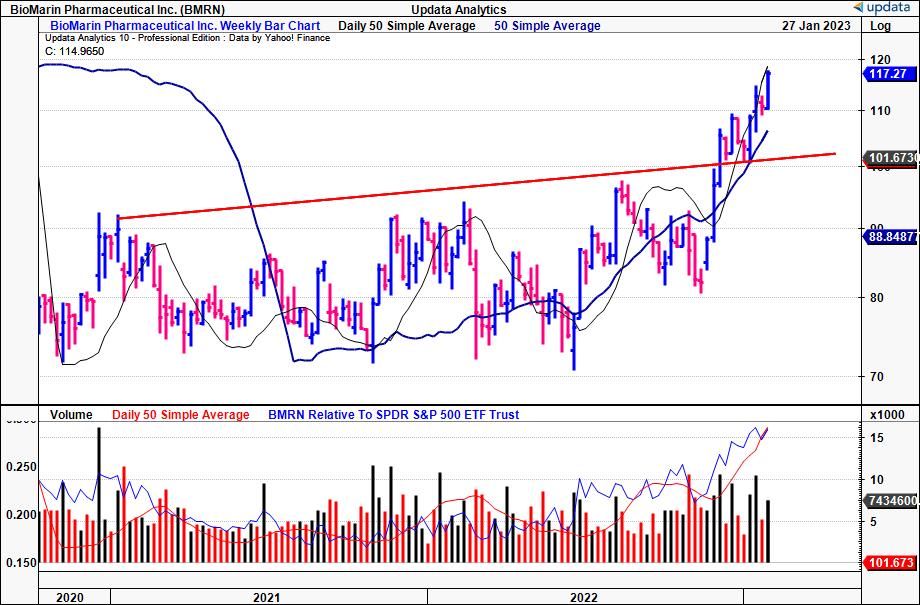

Shares of BioMarin Pharmaceutical Inc. (NASDAQ:BMRN) have broken out of a 2-year congestion in November FY22′ and are now tracing toward multi-year highs [Exhibit 1]. Driving the upside was the FDA’s decision not to hold an advisory committee meeting regarding approval of BMRN’s Roctavian label. The company had made the resubmission back in August after it was initially rejected in FY20′.

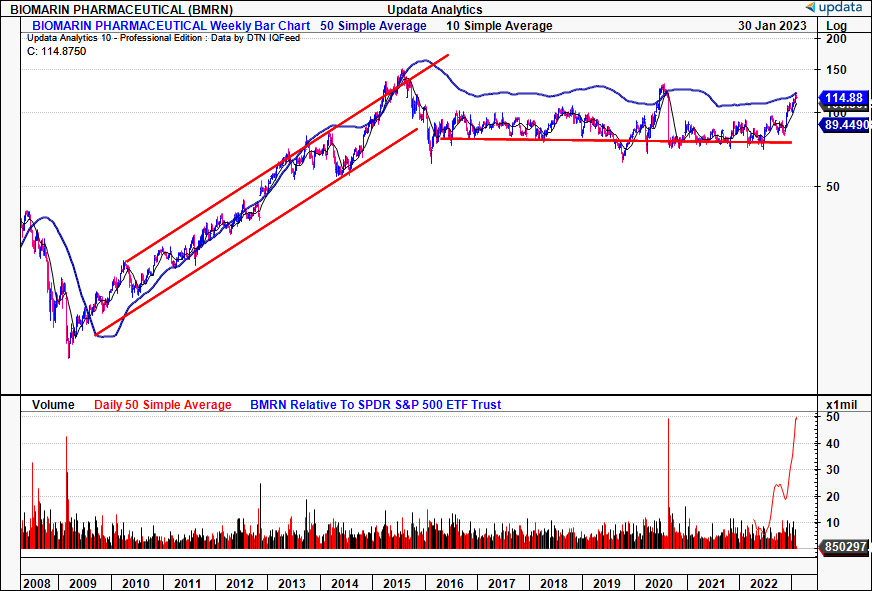

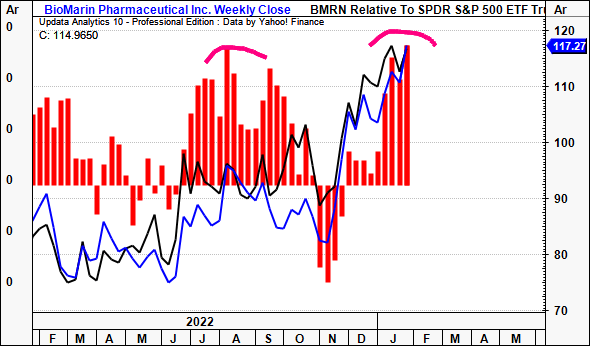

Zooming out over a longer-time frame, BMRN has been a lacklustre listed investment for equity holders from 2015–date [Exhibit 2]. There’s plenty of explanation for this, as we’ll show today, hence, approval of Roctavian is quintessential as a catalyst to extend the BMRN rally into periods to come. At present, there’s scope to harvest some tactical alpha for those speculating on late-stage pharmaceutical assets may find value in this name. Net-net, we rate BMRN a speculative buy, seeking $162 as a tactical allocation over the coming 6-12 months.

Note: It is essential to read the “risks” section located at the end of this report. The entire investment thesis is built on the assumption Roctavian will continue advancing towards FDA approval. Should this not occur, or any setbacks occur, our thesis is completely nullified. Once again, kindly read the “risks” section located at the end of this report.

Exhibit 1. Recent breakout above long-term resistance [weekly bars, log scale]

Data: Updata

Exhibit 2. BMRN long-term stock performance [weekly bars, log scale]

Data: Updata

Expensive growth, or lack thereof, for BMRN

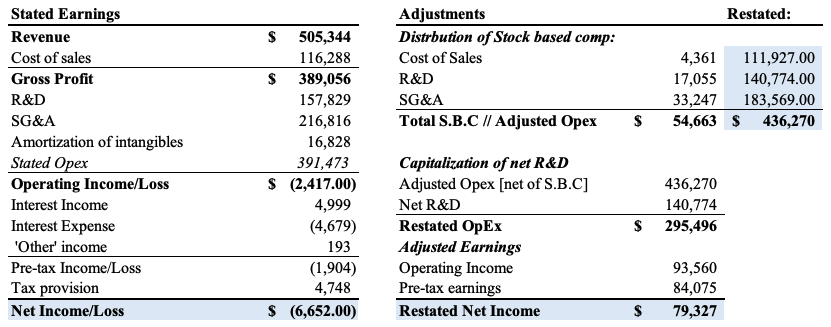

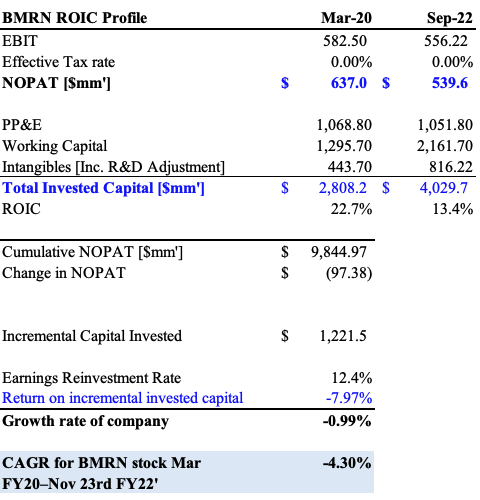

In order to gauge an accurate reflection of the company’s operating performance we first have to make some adjustments. First, the company distributes its stock based compensation (“SBC”) across 3 expenditure segments [cost of sales, R&D, SG&A respectively]. Using its Q3 FY22′ numbers to illustrate, the company booked $391mm in stated OpEx, on a quarterly operating loss of $2.4mm and net loss of $6.65mm. However, it also recognized $54.6mm in SBC for the period, shown in Exhibit 3. We need to adjust for SBC as equity holders as it is a transfer of wealth from common stock holders to employees of the company. Doing so, we restate OpEx to $436mm.

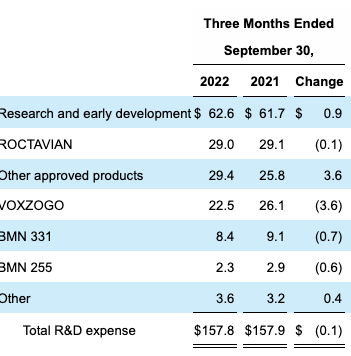

Moreover, R&D is more of an investment for a pharmaceutical company versus an operating expense. We need to capitalize R&D as an amortizable investment to gauge how much it has invested over each rolling period in this analysis. You can see the Q3 FY22 R&D breakdown in Exhibit 4. As we do this, OpEx is restated as $295.5mm, leading to an adjusted operating income of $93mm, and adjusted earnings of $79mm. As seen, the accounting profit that’s presented in BMRN’s earnings presents a vastly different image of the company’s profitability.

Exhibit 3. Restated operating income and earnings after capitalizing R&D and removing SBC

Data: Author, using data from BMRN SEC Filings

Exhibit 4. BMRN R&D Breakdown, Q3 FY22

Data: BMRN Q3 FY22 10-Q

We perform these same adjustments over the last 12 rolling TTM periods for BMRN to get a more reflective set of statements to work from. We then adjust for the tax provision it recorded over these periods, noting the tax benefit it has received over each period as well. From the March FY20–September FY22′ period [rolling TTM figures], it recognizes a cumulative $9.4Bn in NOPAT. It clipped $539mm on NOPAT over the TTM to September 2022, a decrease of over $97mm over the FY20–22′ period [Exhibit 5]. It invested $1.22Bn to generate this loss, meaning its R&D efforts have yet to pull-through just yet – not surprising seeing it’s latest efforts to have Roctavian approved. As a result, growth has been stagnant, coinciding with a 4.3% geometric decline in share price over this period to 23 November FY22′, the day before the Roctavian update was posted.

Exhibit 5.

Data: Author, using data from BMRN SEC Filings

These points in mind, we believe it’s essential for BMRN to have Roctavian move through FDA approval to be successfully commercialized. There’s scope for this to occur, setting up a potential play for those speculating on late-stage clinical assets in this space.

Where to next for BMRN?

I haven’t delved into the mechanism of action for Roctavian, or the underlying pathogenesis and pathophysiology of Haemophilia A, the condition it is indicated for. For a detailed explanation of Haemophilia, the treatment market, and more, check out our deep dive on uniQure (QURE) from December that covers all of this in intensive detail [read the publication here]. Moreover, you can read more on Roctavian’s mechanism of action from BRMN here.

Research conducted by Mckinsey & Co (2017) illustrated that investors reward companies that focus on creating new products or services to fuel their revenue growth. In biotech and pharmaceuticals, we’ve found it is also the prospect of new products/drugs that is accretive to equity returns. Such is the case for BMRN with Roctavian – investors have bid the stock up the page with heavy inflows since the news was announced [Exhibit 6]. On this point, the company’s dominant R&D into the segment could very well pull through to long-term upside for shareholders.

Exhibit 6. Money flows into BMRN equity since Roctavian announcement

Data: Updata

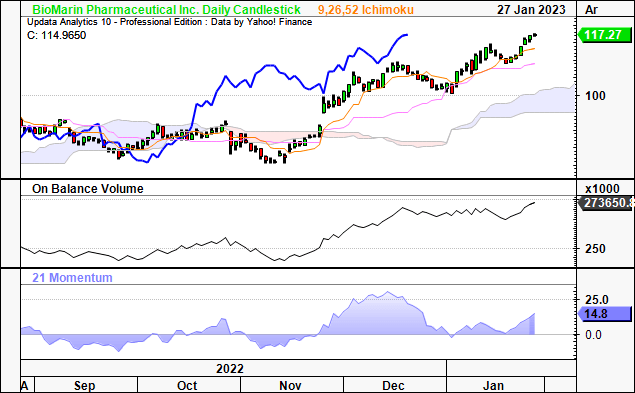

We’ve pared back our exposure to late-stage pipeline assets in FY23′ in-line instead lifting our risk appetite for highly profitable names within the space. That’s not to say that BMRN can’t extend its rally. It is trading well above cloud support, with all systems suggesting the rate of change is set to continue for the time being.

Exhibit 7. Bullish momentum still in situ, long-term buyers evident with technical signs indicating further upside ahead.

Data: Updata

As such, we have upside targets to $162, after the $114 target was recently taken out with confidence [Exhibit 8]. On this basis, we rate BMRN a speculative buy, looking to play the potential for Roctavian’s approval over the coming 6 months.

Exhibit 8. Upside targets to $162

Data: Updata

In short

I’ll finish by saying this buy call isn’t one based off strong company fundamentals, or a macro-thematic to gain exposure too. Investors reward the development of new products, even the prospect of new products in biotech/pharmaceuticals investing. Hence, this is a speculative play to harvest tactical alpha from the market’s generosity to BMRN as it builds momentum around Roctavian, aiming to exit within the next 6-12 months, earlier if necessary, as a risk control.

Risks: The major risk to a buy thesis here is that Roctavian fails in the FDA approval process. This would almost certainly result in heavy supply from sellers and drive the stock south, by estimation. Hence, investors should be comfortable in accepting the fact that Roctavian may not successfully be approved, and make an informed decision on this before any investment. Once again, should it not be approved – or is even delayed somewhat – our entire speculative play here is nullified. I cannot stress this enough. We’ve already identified the risks in BMRN’s business model, in that it has struggled to grow post-tax earnings these past few years, even when adjusted for R&D and others. In that case, there’s not much for the stock to fall back on in the short-term, especially on fundamentals. Therefore, in order for this trade to play out, we need positive updates for Roctavian.

Nonetheless, there’s scope for its approval, setting up a potential play for those speculating on late-stage clinical assets in this space. We therefore rate BMRN a speculative buy, seeking a 38% initial price return at a $162 objective. We’re buying 100 shares. If it rallies to this mark, we will be reconsidering the position, and looking to take a percentage of profits to cover, if not exiting entirely. We will also exit the trade entirely if the stock pulls back another 12% from the entry point of $114. Net-net, rate buy.

Be the first to comment