waleed ahmed/iStock via Getty Images

Bioceres (NASDAQ:BIOX) is an Argentinian manufacturer of agricultural inputs like adjuvants, inoculants and seeds. The company also licenses patents for drought-resistant wheat and soy varieties, and operates a bio-based input segment.

In previous articles from April 2021 and March 2022, I gave a hold rating to Bioceres. My rating was based on the idea that BIOX was not growing fast enough to justify its expensive multiples, and that its aggressive growth strategy was diluting the already profitable part of the business.

Despite the Argentinian stock market more than doubling in the past year, and the generalized boom of commodities, the company’s stock has not moved (the company’s market cap grew 50% because of share issuance).

In this review, with data from 1Q23 and after the merger with Marrone Bio Sciences, I still consider BIOX expensive. The reasons are very similar: growth is either slow or far in the future, which cannot justify the current elevated multiples.

Note: Unless otherwise stated, all information has been obtained from BIOX’s filings with the SEC.

Business description

For a more detailed review, please visit my previous articles, particularly the one from April 2021.

Rizobacter, the engine: Before going public, BIOX acquired Rizobacter, a company with a leading position in adjuvants, inoculants in Argentina, and an interesting position abroad. The company is the profitability engine of BIOX, with a margin on its businesses of about 30%. Its size is around $175 million in revenue and about $50 million in gross profits.

HB4 and the promise of growth: But BIOX is considered a growth company because it licenses part of the patents for HB4 varieties of wheat and soy. These are the first drought tolerant varieties of these crops, with yields that are enhanced between 15% and 20% under drought conditions.

Growth is risky and in the future: One thing is to pay growth multiples for a company that is growing fast at the time, with a proven moat. But BIOX’s HB4 technology has not initiated commercialization yet. Its implementation in the market, success (considering the yield differential is not enormous) and profitability are yet to be seen.

Growth becomes a dangerous mindset: Sometimes companies find out that if they pursue growth, their stocks command a hefty multiple. If growth does not show up fast though, the market gets bored. At this point managers may try to keep juggling, getting further into the mud. BIOX has kept the growth story afloat through a series of dilutive and debt generating acquisitions.

There are also many signals in their financial presentations of promotional investor relations, like mentioning TAM of hundreds of billions in their yearly reports, or showing growth by acquisition in the same place as organic growth.

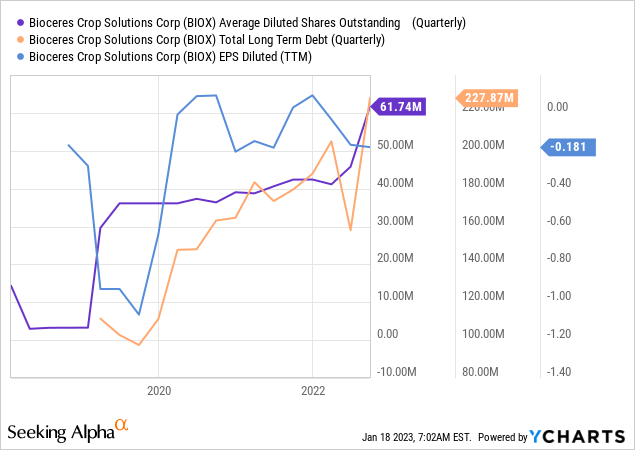

Financially tight: BIOX debt is high and has short maturities, with as much as $75 million maturing this year, and the rest maturing before 2026. If the company has to roll-over in this context, it could increase its interest expenses. The company may also issue shares to recapitalize.

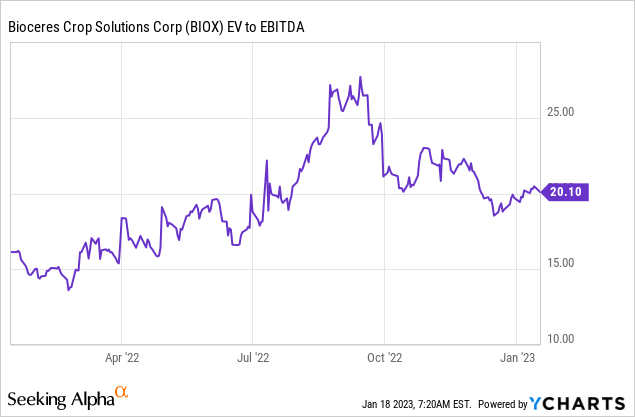

Expensive: On different multiples, either P/E ratio (when earnings are positive) or EV/EBITDA, the company trades at expensive valuations. Of course expensive is relative to the fact that its growth prospects are far in the future and uncertain.

Not so great corporate disclosure and important parent relationships: Bioceres Group (sometimes reported as Bioceres S.A., Our Parent, or Group plc, depending on the report) owns 50% of BIOX shares.

The company is the actual owner of 40% of the patents for HB4, and only grants commercial licensing to BIOX. This is very different from the image that BIOX shows in every presentational material, like below.

BIOX claims that it achieved HB4 technology but it actually licenses it from its parent company (BIOX’s Investors Presentation Dec 2022)

The companies are further intertwined by investments from BIOX in other companies in the group, like Moolec. I also find it strange and confusing that the parent company is called Bioceres as well.

Recent developments

Marrone biosciences merger: BIOX merged with Marrone in July 2022 (previous ticker MBII). Marrone is a growth company specializing in biological solutions for agriculture. It can be thought of as bio-Rizobacter. Of course, its products are not as widely sold and used. The company had negative EBITDA and $45 million of revenue but was merged for approximately $240 million in BIOX shares (a 70% premium on the company’s public price when the merger was announced).

Again, Marrone products may be revolutionary, but only in the distant future and under significant uncertainty. I prefer to leave those very uncertain scenarios to venture capitalists, not to public shareholders.

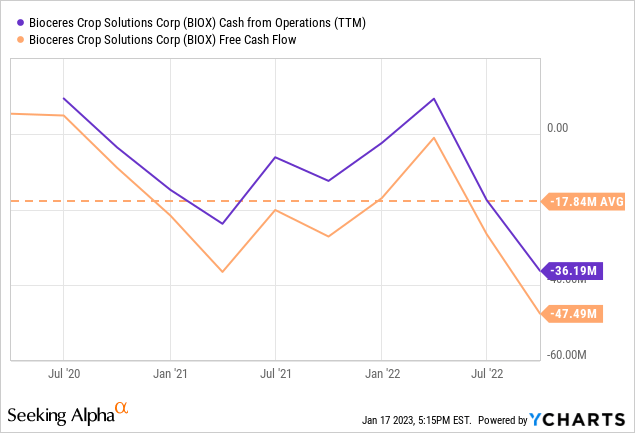

Cash flows continue to deteriorate: With the addition of Marrone, BIOX has increased its requirements for cash, both for working capital and for investment. The problem is that the company has already generated dilution and has to pay $75 million in debts this year. It will have to come up with cash quickly. In fact the company registered a prospectus for the sale of an additional 4.7 million shares in November.

Agreement with Syngenta: BIOX announced an agreement with Syngenta in September, for the exclusive distribution of inoculants, one of Rizobacter’s products ($24 million in revenue in FY22). The agreement guarantees a minimum distribution profit of $230 million over 10 years, a participation of 30% to 50% on ‘profits’ (an undefined term), and a lump payment of $50 million. Given the small size of inoculants, it seems like a good deal, although it could be motivated by a need for cash, considering the $75 million in debts maturing this year.

Even under absurd assumptions BIOX is overvalued: The first and second fiscal quarters (last two calendar quarters) are the strongest for BIOX because Rizobacter sells to Argentinian and Latin American producers during the region’s winter and spring.

Therefore, if we annualize using 1Q23 figures, we are not making BIOX a disadvantage. The company reported profit before income tax of $9 million for the quarter ($12 if we remove transactional costs from Marrone’s merger). The Argentinian tax rate is 35% but BIOX reported a statutory tax of $5.7 million (not effective, statutory) for that period. Even then, we can consider $12 million and 35% tax for $8 million in after tax profits. Multiply this by 4 to find $32 million for the year, against which the company sustains a market cap of $780 million. This means BIOX trades at a high multiple even if adding back expenses, considering the strong quarter as a normal one, and lowering the statutory tax rate.

Mind the non-controlling interest: From the $3.9 million in net income reported for 1Q23, $3.4 million corresponds to non-controlling interests. This is the unconsolidated 20% shareholding base of Rizobacter. What this means is that BIOX is using the remaining profits of Rizobacter to finance its unprofitable growth segments.

Conclusions

I believe BIOX growth prospects are way in the future and uncertain. This means I do not feel confident paying a hefty premium over current earnings for that growth.

To complicate things further, the company seems to be following an aggressive growth strategy, that is risky and dilutes shareholders. I do not believe the opportunity is there to invest in BIOX yet.

Be the first to comment