Ekaterina Markelova/iStock via Getty Images

Bioceres Crop Solutions Corp. (NASDAQ:BIOX) is a company that offers crop productivity solutions, and operates in three segments: crop protection, seed & integrated products, and crop nutrition.

Between the last three to four years BIOX has twice traded for prolonged periods of time in a tight range, struggling to break out. From the latter part of February 2019 through early 2021, it traded in a range of the low $4s to about $7.00 per share, before finally breaking out and jumping to a much higher trading range of approximately $11.00 per share to about $15.50 per share from early April 2021, to where it stands today, trading at a little over $14.00 per share as I write.

Including the acquisition of and ongoing integration of Pro Farm into the business, the excellent collaboration deal it has with Syngenta, and the potential of its drought resistant HB4 crops, it appears the company may be strongly positioned to make another sustainable, upward move in its share price in 2023 and further out.

In this article we’ll look at some of its recent earnings numbers, and how each of the catalysts above could boost the performance of the company.

Latest numbers

As I share the numbers below, keep in mind they now include the numbers from the merger with Pro Farm.

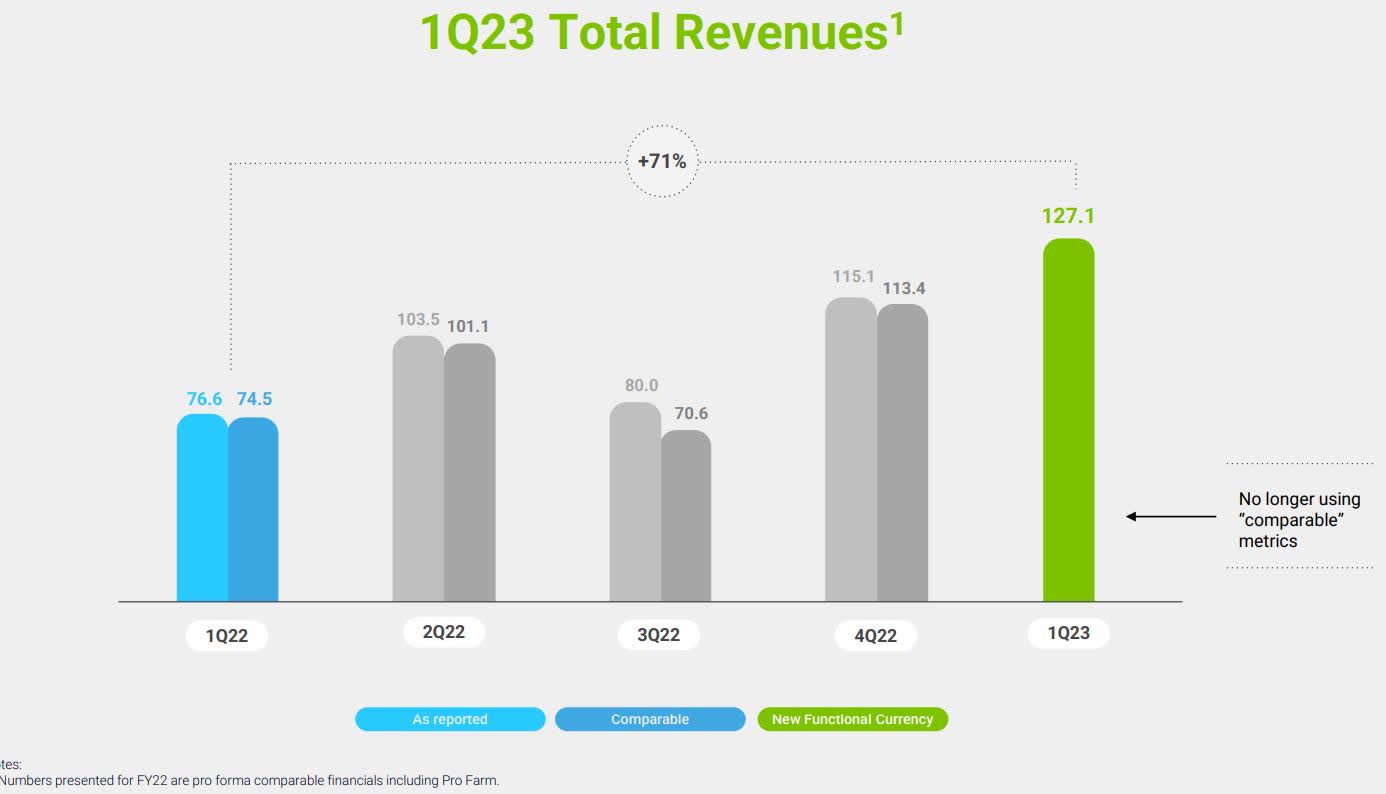

Fiscal first quarter revenue of 2023 was $127 million, up from the $67 million in revenue generated in the first fiscal quarter of 2022.

Company Presentation

Gross profit was $57.4 million, up from the $29 million in gross profit in the first fiscal quarter of 2022.

Operating profit in the quarter was $17 million, a gain of about $7 million from the $10 million operating profit year-over-year.

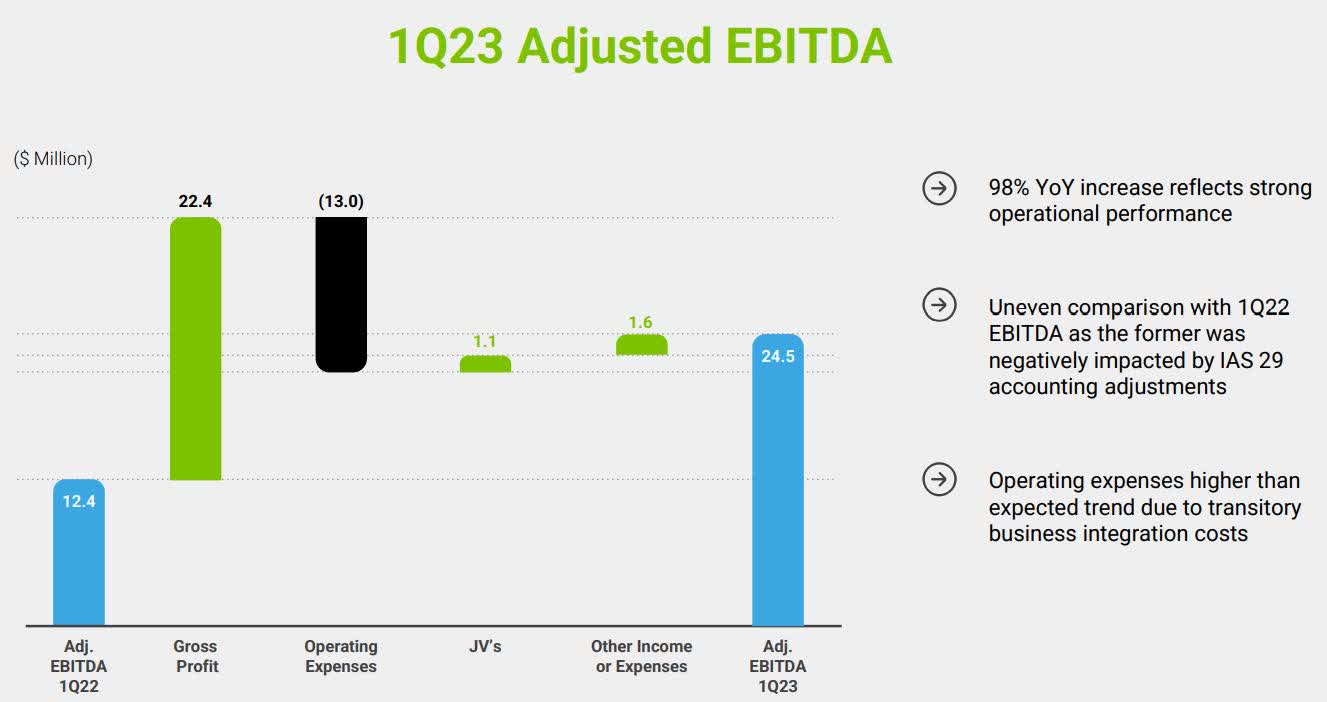

Adjusted EBITDA in the reporting period reached a record $24.5 million. That was about double the $12.4 million in adjusted EBITDA recorded in the first fiscal quarter of 2022.

Company Presentation

The merger with Pro Farm put downward pressure on adjusted EBITDA, but management said that over the next couple of quarters it cost synergies should result in Pro Farm becoming a positive contributor to adjusted EBITDA by the end of fiscal 2023. Pro Farm recorded full-year EBITDA of (-$14.6 million) in full-year 2022. With the drag on its adjusted EBITDA from Pro Farm and still being able to produce record numbers, the company is optimistic concerning it outlook for profitability in the first fiscal half of 2023.

Company Presentation

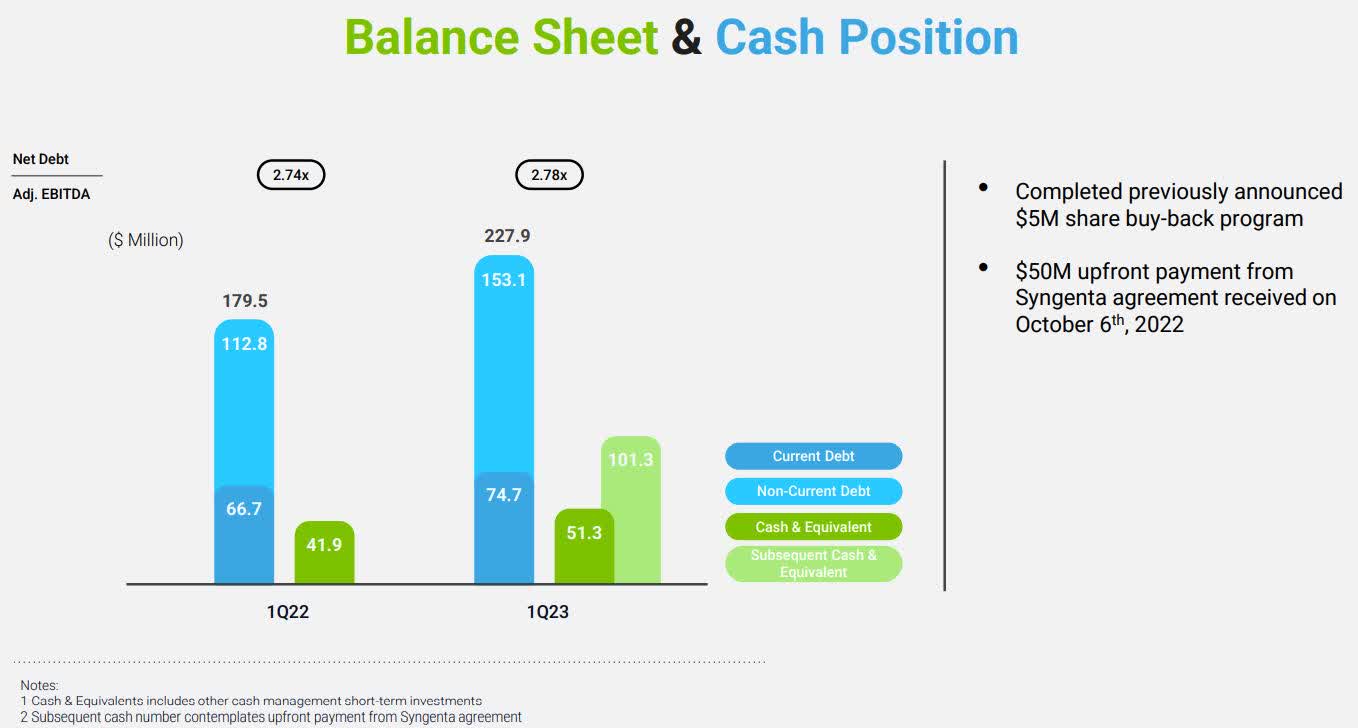

At the end of the quarter BIOX had cash and cash equivalents of $47.4 million, up just shy of $14 million from the prior quarter. Total debt at the end of the quarter was $228 million. The increase in debt was related primarily to financing agreements from the Pro Farm merger, including paying down existing financial obligations of the company and providing working capital while boosting its cash position.

HB4 crops

Company Presentation

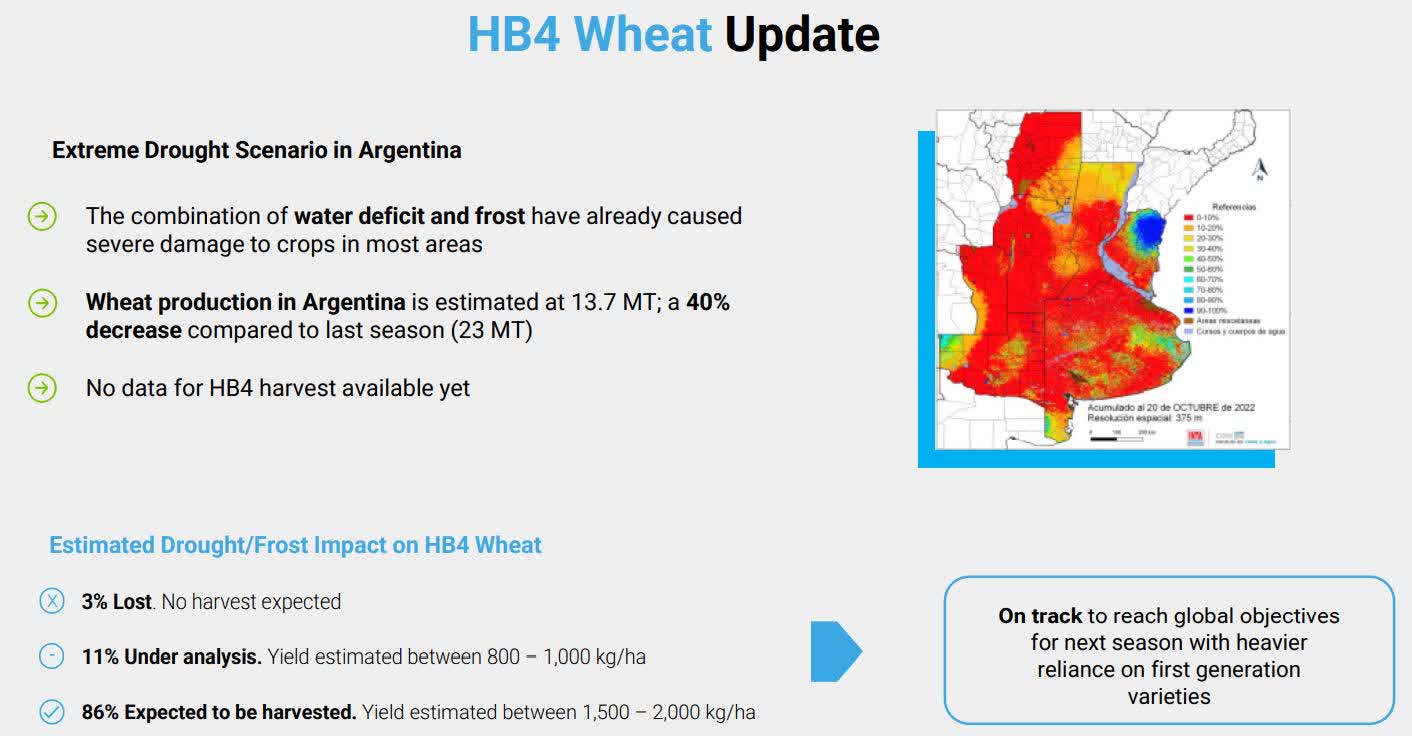

HB4 crops are drought tolerant solutions resistant to dry weather conditions. The company is currently growing HB4 wheat and soy crops, with its current focus on Argentina because of it being the growing season in that hemisphere.

Even though HB4 wheat is drought resistant, it doesn’t fully protect crops in extreme drought conditions, which is now faced in Argentina. For that reason, the company expects a smaller harvest than it would have had under more optimal conditions. In the next earnings call the company will provide more data on the outcomes of that harvest. This is actually a potentially good thing for the company over the long term, as it’ll provide a comparison against competitors that provided wheat in the past that didn’t have the resistant capabilities of BIOX’s HB4 wheat.

The company also continues to scale its HB4 soy breeding and multiplication in Argentina and Brazil.

As far as contributions to the company, HB4 wheat is expected to add $15 million to $20 million of EBITDA in fiscal 2024 and soy is projected to add $20 million to $25 million of EBITDA by fiscal year 2025.

Concerning wheat, because of the drought, that is likely to generate lower numbers in the first two fiscal quarters of 2023.

BIOX does sell a conventional, non-HB4 system in Argentina, which is a top-selling brand in the country, so it’ll be able to have side-by-side comparison with the two systems in regard to yields under drought conditions. This should provide stark differences between the two, and show the superior results of HB4 wheat, which in turn should drive sales up.

Company Presentation

The company has also recently received clearance from South Africa in regard to HB4 wheat and soy.

HB4 crops are a long-term game, and if the company is able to execute on its EBITDA guidance, they’re going to be a strong tailwind for the company in the years ahead, and potentially more so if it continues to expand its global footprint.

One last thing to consider with wheat in particular is the conflict between Russian and Ukraine has resulted in the world looking for alternative supplies of wheat, and that could be a strong catalyst for BIOX as it grows that part of its business as food security increasingly becomes a global concern.

Syngenta

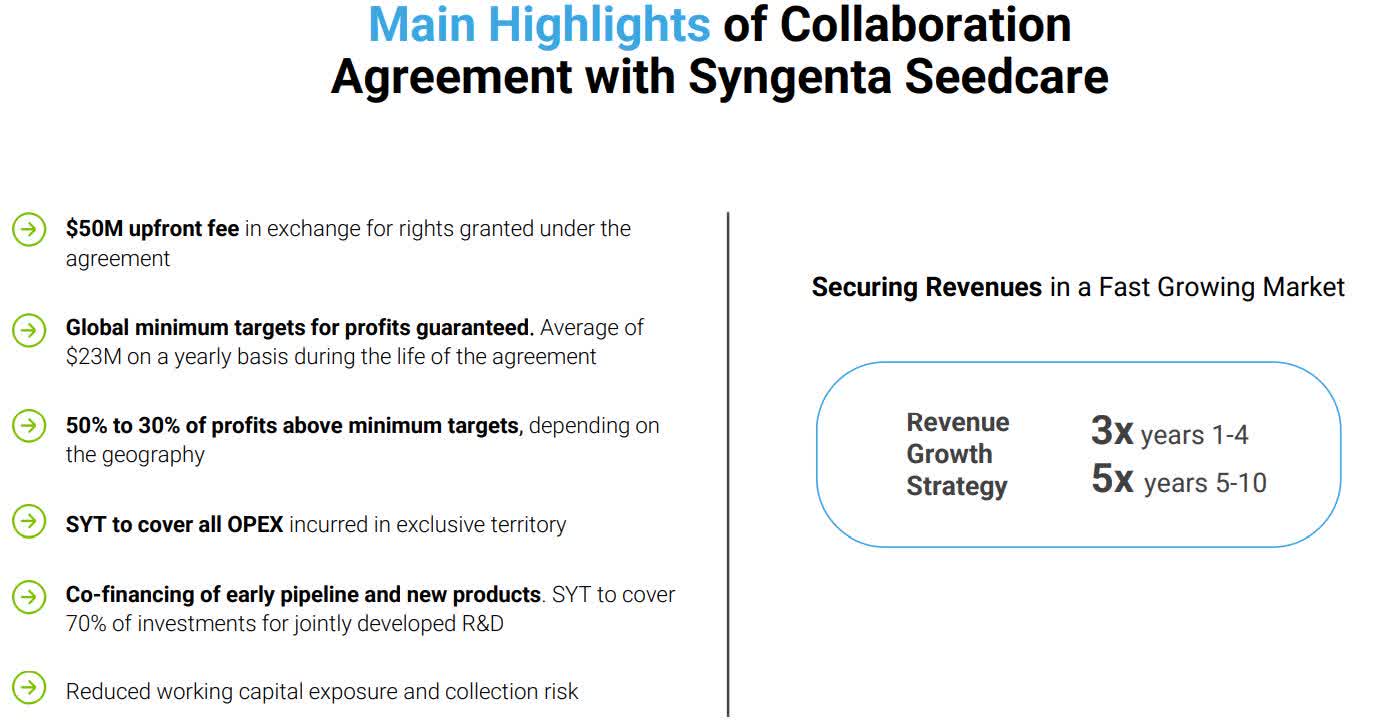

In the near and long term, the collaboration with Syngenta Seedcare is probably the strongest catalyst for growth the company now has at its disposal. The seed care market is estimated to be between $4 billion to $5 billion with biologicals representing 20 percent of that. One third of the penetration comes from inoculants, which is what BIOX is competing in. The company estimates biologicals will reach $1.6 billion in the segment by the end of the decade, and management believes it’s going to be the winner in capturing much of that growth.

That was the major impetus behind entering into the collaboration with Syngenta Seedcare. The companies have already been working together in Argentina, but what the deal does is provide the opportunity to expand internationally. Based upon the success of the two companies in Argentina, where, together, they’ve taken the first position in its “inoculants, bio fungicides and Syngenta molecules for a long time.”

In this venture the two companies, at this time, are focusing solely on inoculants over the 10-year duration of the deal. BIOX is providing the product while Syngenta provides capital, and sales and marketing.

The company said it has “secured minimum profits that average $23 million on a per year basis over the life of the agreement.” Along with that it received an upfront fee of $50 million in exchange for right granted in the deal. The minimum profits noted above is not the only benefit BIOX will receive from the agreement, it will also receive from 30 percent to 50 percent in incremental profits based upon specific geography and specific years.

Syngenta is also providing 70 percent of the capital for R&D “for early pipeline products and new products that we may opt to develop jointly within this framework.”

Management was clear on the fact that it hasn’t sold its inoculants business to Syngenta but has entered into the agreement in order to make its inoculants business far more relevant over the next decade.

I has retained the rights to use inoculants in its HB4 farming program.

By any measure this is a great opportunity for BIOX, and presumably it has a good chance of expanding across other parts of the company once the results of the deal are clearly evident.

This will accelerate its footprint in markets like Australia, China, Europe, and the U.S., where it currently doesn’t have a footprint. If it can do this in the one product category it has chosen to work with Syngenta in, again, the potential to expand it to other products presents a terrific, long-term opportunity for BIOX.

But even as the deal stands today, I see it as a no-brainer as far as the positive impact it’s going to have on the long-term performance of the company.

Company Presentation

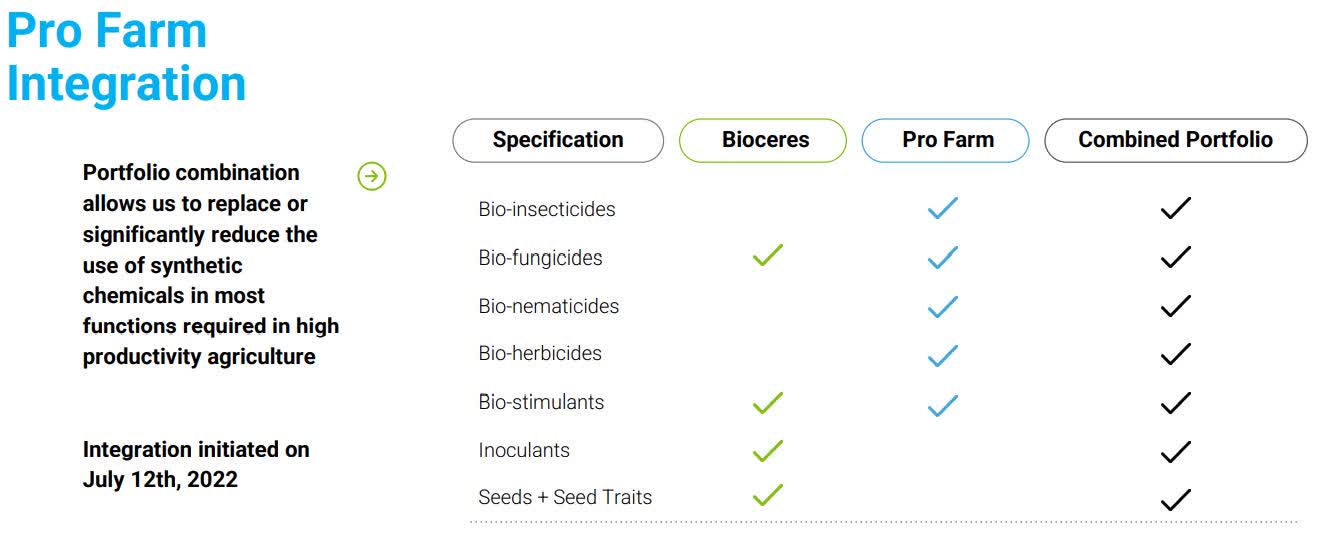

Pro Farm

I already mentioned the merger with Pro Farm earlier in the article and how it will temporarily have a negative impact on EBITDA, which is expected to be remedied in 2023.

What Pro Farm adds to BIOX is expertise in Bio-insecticides, Bio-nematicides, and Bio-herbicides. It also complements existing categories like Bio-fungicides and Bio-stimulants. Combined, they offer a far more comprehensive solution to end users.

Pro Farm also has an R&D department that will strengthen BIOX’s R&D results.

Company Presentation

Conclusion

Company Presentation

Taking into consideration the various moves BIOX has recently made, its future growth potential is much higher than it was last year at this time.

Not only has it added Pro Farm to its business, but it has entered into a deal with Syngenta that will provide a predictable revenue stream over the next 10 years, but also has the potential to add much more depending on timing and geography.

Add to that the advancements it’s making with its HM4 wheat and soy, which will without a doubt expand to other markets in the future, and you have a solid narrative for a long-term growth story that I think is close to taking off to the next level, based upon the share price movement of BIOX, which doesn’t appear to have priced it all in yet.

This assumes it continues to perform well in the other parts of the business.

Be the first to comment