Shares of Bicycle Therapeutics (NASDAQ:BCYC) currently sport a 117% gain in ROTY’s main portfolio (emphasis on needle moving catalysts and accelerating clinical momentum over the next 12 months). It’s also currently our largest position, with the general idea being to let winners run as thesis continues to strengthen.

With the share price depressed ahead of AACR (American Association for Cancer Research) presentation, I felt it was a timely opportunity to bring to the attention of readers ahead of a material milestone for the company.

Chart

Finviz

Figure 1: BCYC weekly chart

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what’s going on. In the weekly chart above, we can see shares uptrend nicely since the beginning of 2020. October results for drug candidate BT8009 caused shares to spike at the triplet meeting last year, but since then they’ve fallen to the 50-day moving average. My initial impression (and a stance I’ve been advocating for some time) is that this represents a buying opportunity ahead of the higher dose results coming at AACR on April 11th.

Overview

Our current thesis in ROTY is as follows:

Bicycle Therapeutics (BCYC)- $1.2B MC, $800M EV (as of March 23rd) is an attractive valuation for this pioneer of the unique Bicycle technology platform. Bicycles are simply better suited for certain indications and targets than prior classical technologies (biologics, small molecules, etc.). For BTCs in oncology, they are able to deliver 5x-6x the payload of ADCs, getting it into tumor cells more efficiently and elimination of all excess renally (leads to better tolerability/safety profile). Management appears to be asking the right questions and relying on data to answer them, moving three oncology candidates forward in the clinic at therapeutically relevant doses and in patient populations enriched for the given target. Some derisking has taken place via proof of concept achieved with positive phase 1 data for Oxurion-partnered Kallikrein inhibitor Bicycle, THR-149. Additionally, BT8009 as a fast follower for Seattle Genetics’ (SGEN) enfortumab vedotin/Padcev looks attractive (improved safety and 4 times the potency). Initial low dose data looks superior (or comparable) to Padcev in a slightly more advanced patient population and safety profile is also significantly improved. Consider that Padcev is thought capable of doing up to $2 billion in relapsed/refractory bladder cancer and over $5 billion in previously untreated patients. A position here is a bet on the Bicycle platform and at least one positive data readout for lead programs as the pipeline progresses. Specifically, I expect promising high dose data (management now intent on pursuing Padcev failures or patients who can’t tolerate the approved ADC drug from Seagen) would move the needle and pave the way for expansion studies (Epha2 also moving into expansion cohorts after promising early responses in UC and ovarian). See my July update piece. Needle-Moving Catalyst=8009 higher dose data AACR in April

Company Presentation

Figure 2:Pipeline

Let’s move onto some of my prior notes, as I hope they’ll help bring readers up to speed on this exciting story.

Excerpt From My September Cantor Notes

At Cantor presentation on September 27th, I appreciated the following (while dated, they provide a sense of how clear and transparent this management team is, enthusiastic without being cheerleaders, simply following where the data leads):

Context was given that Bicycles are 100x smaller than an antibody (and have applications in MANY different areas). The first 3 molecules are designed to deliver high potency toxins into solid tumors- they are also working on the idea of using two pharmacologically different Bicycles conjugated together (one retained in the liver, other activates immune system).

Compared to ADCs, the most differentiating thing is their small molecule nature (100x smaller), ability to readily penetrate into solid tumors (almost instantaneously penetrate into tumor). Short systemic half-life ensures that they disappear from circulation after penetrating tumor and bind to target. The extra Bicycle is eliminated primarily through renal route. They can thus get quite a bit of payload into the tumor despite having relatively small presence of drug in systemic circulation (lends to potentially a greater efficacy and greater tolerability).

Advantage (Corporate Slides)

Figure 3:Bicycles combine advantages of both small molecules and antibodies (Source: corporate presentation)

Regarding BT8009 versus Seagen’s (SGEN) Padcev in Nectin-4, management stated that comparing phase 1 data to registrational results is unfair. The 2016 phase 1 update showing 28% response rate for Padcev was conducted in patients with fewer lines of therapy and obviously ¨we are in a different world today¨ (treating patients with considerably more prior lines of therapy). It’s thus very hard to do direct comparison, so they chose to compare it with comparable phase 1 data. Management states that people will draw their own conclusions from the data- they are hopeful their data will speak for itself. Another thing to keep in mind is that they are still in escalation, so it’s worth looking at when they gave that update it was a selected dose, whereas for Bicycle we need to take into consideration where they are in the trial. When data comes out, they will be very clear on the details to aid in comparison & context. Readout is all comers- bladder is the known indication, but as for other indications that could be interesting where Nectin-4 is expresser, their investigators are very enthusiastic with breast as well as head and neck cancer.They are amending protocol in their study to ensure enrollment of Padcev failures as well– same payload but it’s being delivered in a different way. 8009 is really a penetrant molecule, so it could really be that they are simply reaching parts of the tumor that ADCs don’t reach.

Regarding TICAs, management notes that CD137 responds better to transient activation as opposed to prolonged activation (long lived agonist biology is precisely the wrong way to target this receptor). You have to be able to get into the tumor to activate this target, and they’ve developed a molecule with these key design criteria (highly tumor penetrant, completely dependent on Nectin-4 for activation and has relatively short biological profile). ¨This asset is very distinct from anything else out there¨. Accelerated titration, 3+3 design and investigators are very excited (more than the usual level). Beautiful pharmacodynamic readouts, lots of sampling they can do and again it will be very different from BTCs. ¨We are the only company on the planet with this technology¨.

Corporate Slides

Figure 4:TICA Overview

Biomarker responses will inform where they go with the rest of IO franchise (again, follow the data). The ability to activate the immune system will be very valuable in cases where they don’t respond to the toxin. In other cases, the immune system is compromised and straightforward cell kill makes more sense.

They try to embark on collaborations that allow them to explore the potential of the technology beyond what they can do themselves. This line of thought underpins how they are thinking regarding future partnerships.

Notes On Data At Triple Meeting In October

As for October 7th data readout, what stuck out to me for BT5528 was the 100% ORR (2 of 2 partial responders) in urothelial cancer (this for a target, epha2, that was left for dead). 80% disease control rate was observed in Epha2 positive ovarian cancer patients with 1 partial responder (20% ORR). Context is very important here, as these were patients with median of SEVEN prior lines of therapy (heavily pretreated/very advanced population). On the con side, mild transient neutropenia was observed at 8.5mg/m2 every week and two dose limiting toxicities took place at 10 mg/m2. There were two grade 5 (death) events as well with one being tumor lysis syndrome and the other renal failure caused by GI-related dehydration.

It looks like the company will move forward with either 6.5 or 8.5/m2 every other week dose (we shouldn’t be spooked by adverse events, as that’s the nature of a dose escalation study). Bicycle Therapeutics will move forward with expansion cohorts in urothelial and ovarian cancers as well as a basket cohort (includes HNSCC, NSCLC, gastroesophageal and triple negative breast) in 2022. The trial will enroll up to 56 patients and from there expand enrollment as data merits.

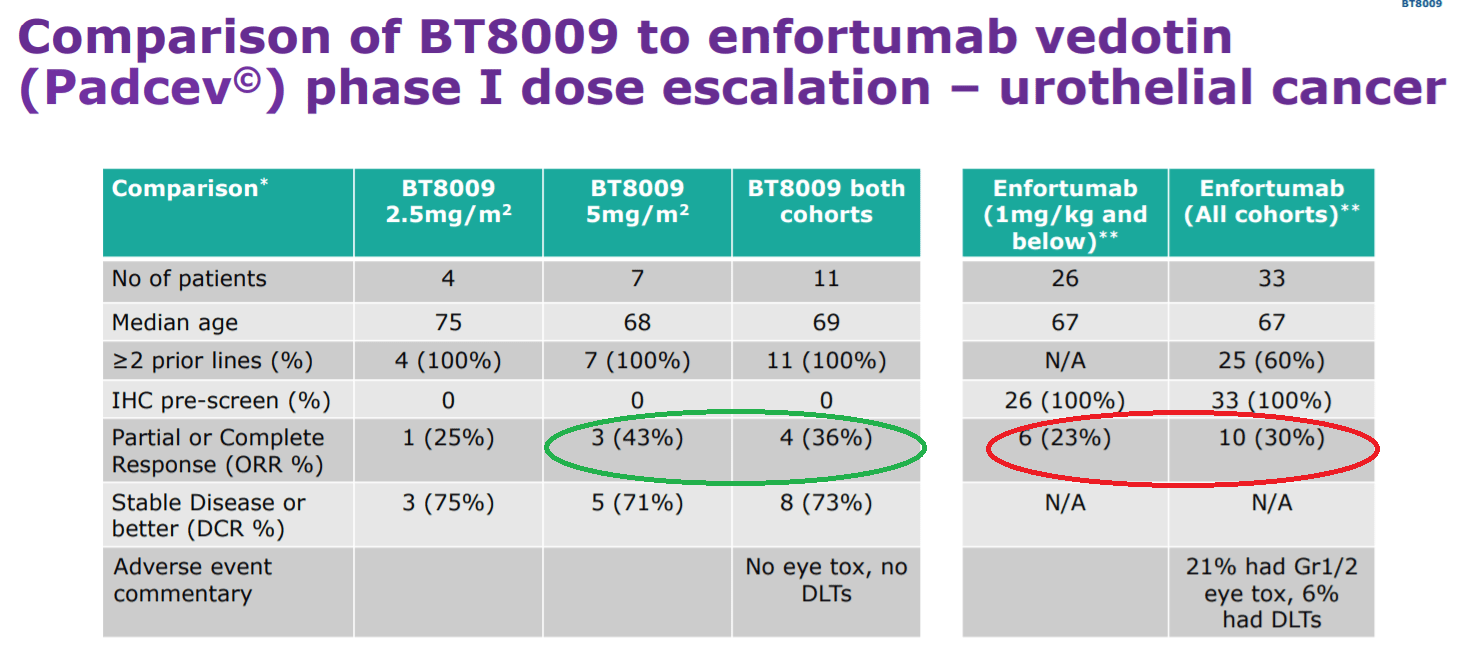

For BT8009 phase 1 dose escalation study, 4 of 11 urothelial cancer patients had partial responses, safety profile looked solid and the bottom line for me was that both early safety (no eye toxicities, no DLTs) and efficacy appeared superior to Seattle Genetics’ Padcev (usual caveats for cross trial comparisons, low N, lack of follow up, etc.). It’s important to note that 43% ORR was achieved at just the 5.0mg/m2 weekly (MID) dose, with 30% ORR for Padcev/enfortumab vedotin in phase 1 being the benchmark to match that up to. ORR for 8009 was 36% when include low dose patients, still respectable. Seattle Genetics’ data from phase 1 for enfortumab vedotin/Padcev was in patients of whom 81% had received prior platinum chemo and 67% received 2 or more prior therapies. Again, Bicycle Therapeutics achieved better ORR in a more advanced population.

Corporate Slides

Figure 5:BT8009 Padcev cross trial comparison

I’m very much looking forward to the 7.5mg/m2 weekly and every other week cohorts reporting data next year. It’s a good sign that new sites continue to open (14 trial sites active globally, up to 21 will be online by the end of this year).

As for the conference call, I highly suggest listening to get your own feel for the data. Here are a few takeaways for me:

CEO joined company 6 years ago, saw revolutionary technology with limitless potential to deliver new class of molecules that could change the way we treat disease. Partnerships are set to maximize value of the platform outside the area of oncology. They have delivered on all of their milestones over the years (consistency).

BT5528 (Epha2) showcased the platform’s ability to reach a target unachievable with antibody based approach. Predecessor MedImmune’s MEDI-547 (ADC) caused clots in 5 of 6 patients. 5528 preclinically did not show these clotting problems. 3+3 dose escalation study, they felt comfortable with no hints of clotting so the criteria was changed to enroll patients with enhanced Epha2 expression. They will go into cohort expansion and consider PD-1 combinations as well. Trial had 21 patients in it- particularly notable is 7 prior therapies (ranging from 1 to 16), which is very high (patients less likely to respond, terribly sick).

Regarding adverse events for BT5528, they had a reasonable degree of neutropenia (attributed to payload), zero bleeding disorders, zero conjunctival disorders, zero cutaneous events, zero neuropathy as well. One patient came on the trial with neuropathy and his neuropathy got better (remarkable). They also saw a Grade 5 tumor lysis syndrome, worthwhile noting that in solid tumors this is a very severe thing to happen. They also had a Grade 5 event with patient went into acute renal failure, went home and got severely dehydrated. At the 8.5mg/m2 stage none of those patients had a DLT, but physicians did say a number of them had grade 3 or 4 neutropenia (not lasting enough to be DLT), some additional gastrointestinal discomfort (nothing to write home about but they decided it wouldn’t be wise to go any higher). They started exploring 8.5mg/m2 every other week and 6.5mg/m2 every week. Last week they came out of safety committee, they are very excited about exploring 6.5mg/m2 every other week.

As for efficacy of BT5528, they had one formal partial response amongst 8 patients with ovarian cancer. 4 of 5 with Epa2 staining have some degree of tumor shrinkage. More striking (but not surprising) is the two urothelial cancer patients who both had responses after first couple cycles and those responses continue to deepen (one beyond 60% shrinkage level). H-score slide shows correlated with % change according to RECIST (intriguing correlation between intensity of target staining and degree of shrinkage). Investigator states we should carry forward that observation when we think of intensity and depth of staining we get with Nectin.

For BT8009 (Nectin-4), they state that the efficacy exceeds that of enfortumab vedotin (the approved ADC) based on phase 1 results even though patients enrolled in 8009 study were later line and escalation is not complete. Early signs of tolerability indicate differentiation (another validation of Bicycle platform). The data is very early, but they wanted to share it as soon as possible. They are still escalating and looking to do further cohort expansions (including combinations being considered in protocol). They are looking at standard first in human criteria (allowed all bladder cancer patients on trial, but for other tumor types are enriching for Nectin-4 expression). They have 26 patients (urothelial most common amongst them).

Of the 11 patients with urothelial cancer, all had 2 or more therapies (none had 1). This is important because the main comparator at similar stage ASCO 2016 had 40% of patients with 1 prior therapy (Padcev from Seagen).

For 8009 safety profile, excessive bone marrow suppression, some hypertension, some fatigue, nothing that stood out.

¨Mindbending efficacy¨ per management, very much their expectation that tumor reductions will further deepen. One response at the low dose out of 4 patients (37% reduction). Stepping up to 5mg dose, it was very well tolerated and they were seeing 3 out of 7 patients responding (really deep). Even the stable diseases are arguably more response-like than many stable diseases seen in first in human trials. 75% disease control rate at low dose, 71% DCR at 5mg dose.

Management’s intention is to do something different than enfortumab, discover new ways forward (not copying pasting what other people do). They state that if they are not as good as enfortumab, they won’t get very far. But, they are as good and probably even safer. In figure 5 above, they took the 2016 publication for enfortumab to compare to 8009. ORR of 36% compares well to 23% for enfortumab 1mg/kg and below, and to 30% for all cohorts. Management feels that they won’t be seeing degree of neuropathy other agents see (platform readthrough). No eye tox, no DLT.

Speaker states that ¨it’s easily the best solid tumor data response he’s ever seen in a trial he’s been associated with¨. He would have given his left arm to be looking at these kind of results. 89% and 52% shrinkage is observed in patients B and D.

Moving onto readthrough and plans for the platform, they are actively screening against multiple high value tumor targets (both those of current ADCs and those that previously failed). They are also evaluating 3rd generation including DNA-damaging payloads. It’s apparent that Bicycles can direct very effectively to tumors. Believe they will direct other Bicycles to tumors as seen with first TICA (Nectin-4/CD137). Further beyond that in immuno-oncology, they are looking at multiple receptors expressed on NK cells.

As for Q&A, for potential combinations for 5528 and 8009, they think platform lends itself to PD-1 combination (non-overlapping AEs). They want to establish what the monotherapy signal is first (7.5mg/m2 for 5528 is way too intriguing). They are keen to combine with PD-1 and other agents as well.

For 8009, it’s interesting that a couple of bladder patients were below expression threshold (for Seagen’s enfortumab vedotin they were enriching for efficacy with expression cutoff, whereas Bicycle Therapeutics was not).

For 8009, they excluded patients treated with Padcev but are now making protocol amendment (very keen to see what happens in face of patients who fail Padcev).

Other News & Information

In January, the company announced updated results for BT8009 which continue to trend in the right direction. All four responders at low and mid dose have confirmed ongoing RECIST 1.1 responses (signs of durability). Additionally, one mid dose partial response converted into a complete response (100% tumor volume reduction).

An article from Genetic Engineering & Biology News (GEN) highlighted novel cancer treatments and particularly Bicycle Therapeutics’ unique technology and approach. The article also touches on drawbacks of antibody drug conjugates, including:

Too big to effectively penetrate solid tumors

Bind to healthy cells

Can diffuse from targeted cells to harm innocent bystander cells

Release payloads upon being metabolized (injuring liver)

Finally, we are reminded that Bicycles are 100x smaller than antibodies and again the unique benefits we’ve touched on prior (advantages in safety & tolerability, better penetration of solid tumors, etc.).

Management presented at SVB Leerink on February 16th- here are a few nuggets:

For BT8009, they note that Padcev is not available in Europe, so they’ve been enrolling mostly bladder cancer patients (high demand to get into the trial). 8009 delivers 30% more toxin than Padcev per cycle. It’s encouraging the kind of tumor reductions (4 partial responses) they’ve seen so far, along with absence of skin toxicities and January durability update shows responses getting bigger (including PR converting to CR) while tolerability is maintained. Profile is very strong relative to Padcev (¨very excited about what we’re seeing¨).

Bladder cancer landscape is very competitive field, but there’s still a need for better therapies. Management states they would not hesitate to take Padcev if they were a patient, it’s clearly doing great things in patients. However, they were struck by the emergence of tolerability profile for Padcev including French compassionate use program where a number of patient deaths were classified as severe events due to these skin reactions. They still don’t know the cause of these skin reactions, rash then severe complications (is there predisposition, genetic factors, types, etc.)? As a patient, management would be worried about such toxicities and a therapy that comes along without such issues would be highly attractive to patients and doctors.

For 8009, they are keen to get patients who failed Padcev on the study, or those who couldn’t tolerate Padcev or did not respond to it or did ok but no longer working (see how 8009 does in these populations).

BTCs have a long residence time in the tumor and short systemic exposure. Oncology is all about the combination of efficacy AND tolerability (patients keep taking this and taking this). They are seeing good or arguably better efficacy compared to Padcev so far in slightly later stage patients. Tolerability profile is clearly better (caveat for low number of patients).

As for BT8009 in other tumor types, they are focused on finding the recommended phase 2 dose first, then expanding to test full potential in other types of tumors. They want to optimize the dose and understanding of tolerability profile, building out the durability data first.

As for broader implications, they’ve clearly demonstrated for 2 clinical targets that they can differentiate on safety (big deal, as ADC field is full of vulnerabilities and programs that fail due to safety). Bicycles are very amenable to non-internalizing targets (can’t be targeted by ADC players). They can now expand to DNA damaging agents, radioactive elements and other classes in the toxin delivery space. Huge opportunity in immuno-oncology as well.

The big idea here is that Bicycles can target deep into tissue, they don’t know of any other technology that can do what Bicycles can. IO conjugates, radio-conjugates, whatever conjugates you can think of are better suited to Bicycles. Similar applications outside of oncology (Ionis is a first adopter for delivering antisense into CNS and muscle). Several other such opportunities await.

As for the Q4 update, cash position of $438.7 million compared favorably to net loss of just $18 million. We are also reminded that in the 5.0 mg/m2 cohort for BT8009, the patient who initially had 89% tumor reduction now has 100% tumor volume reduction (complete response). Data is still being guided for presentation at a major medical meeting.

For BT5528 (Epha2), expansion cohorts should get underway this year at recommended phase 2 dose of 6.5mg/m2 every other week.

TICA candidate BT7480 dose escalation trial is ongoing.

Lastly, on March 8th the company announced that interim phase 1 results for BT8009 have been selected for oral presentation at AACR (conference call on April 11th at 8:30 AM). 4 additional abstracts have been selected as poster presentations.

Final Thoughts

To conclude, with the usual caveats, we’ve found a differentiated platform technology poised to revolutionize a lucrative space (OTCPK:ADCS) through providing both superior efficacy and safety compared to what’s on the market today.

Additionally, this technology is applicable to many other therapeutic areas (partner Ionis Pharmaceuticals licensed the tech in July to increase delivery capabilities of its LICA medicines, designing one that targets transferrin receptor 1 with aims of improved delivery to cardiac and muscle tissue). Bicycle Therapeutics is focusing its efforts on oncology, and even there the implications are very widespread so management will need to judiciously choose what targets to pursue internally and where they should partner out (in October they expanded the Genentech partnership to pursue novel immuno-oncology therapies).

Clinical momentum continues to accelerate here, as lead BTC candidate BT8009 reports high dose data and moves into expansion cohorts along with their Epha2 candidate (initial TICA data could come later this year as well).

For readers who are interested in the story and have done their due diligence, Bicycle Therapeutics is a Buy and I suggest accumulating at current levels ahead of AACR.

Key risks include disappointing data- if we see significantly more skin or eye toxicity for BT8009 at the higher dose, that would weigh against our thesis of the drug being substantially differentiated versus Padcev. Along the same lines, we’d expect to see even greater efficacy at the higher dose of BT8009, so the stock would take a hit if that’s not the case. The company is well capitalized, but management would not be faulted to raising more funds if share price jumped considerably. Competition in the ADC space is something to keep in mind (finding the right niches for BT8009 to compete with Padcev, knowing which targets to pursue internally and which to partner out).

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment