Schroptschop

General Introduction

It is boom time for commodities. Cyclical in nature, the global commodities industry powers world economic growth and has, for many years, played second fiddle to its big brother – global energy. But times are changing. Once the centerpiece of economic expansion, and among the most valuable firms only decades ago, big energy is now starting to fall out of favor.

The likes of Exxon (XOM), Shell (SHEL), and Chevron (CVX) have all collectively become political hot potatoes – at the forefront of public opinion, a realization of environmental shifts, and perhaps political whim to curry favor with voters. In summary, big energy has been socially divisive. Changes in opinion have spawned the electrification of society – whether its automobiles, solar panels, wind farms or the electric grid – new ways are being sought to sustainably drive humanity for generations to come.

Consequently, a new green wave of global change will require copious amounts of nickel, copper, cobalt, graphite, uranium, and iron ore, among others. And in doing so, will play nicely into the hands of global commodities powerhouses the likes of BHP (OTCPK:BHPLF).

It’s a perfect storm – one where society rejects one facet of big industry only to fall headfirst into the throes of the other. Accordingly, huge tailwinds are likely to reap benefits for companies like BHP. Feeding off that change and fueling global growth for years to come, it is hard not to have a bullish outlook on future company prospects.

Bullish. Eyes closed.

Visual Capitalist

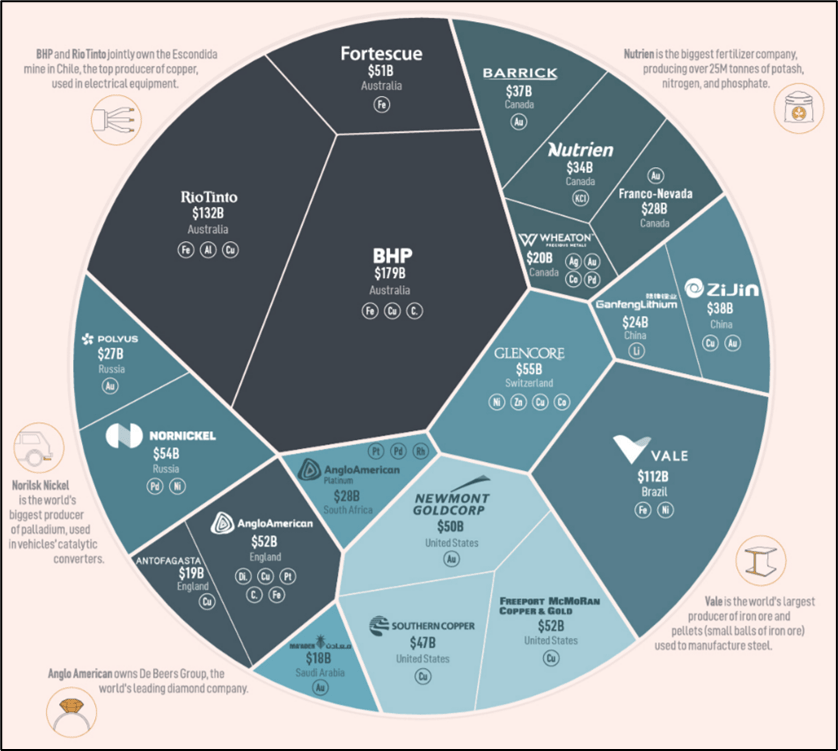

BHP is a 170-year-old global mining titan dwarfing international competition.

Company Overview

BHP is a global mining powerhouse – the biggest player by market capitalization, the Australian mining monster, with a market capitalization of $179B towers above its closest competitors, Rio Tinto ($132B), Vale ($112B) and Glencore ($55B). As the world’s largest player in the global commodities space, the firm remains particularly exposed to both economic headwinds and geo-political volatility with China figuring prominently in its customer base.

Founded in 1851, the company has operating activities in Australia, Europe, China, Japan, India, South Korea, greater Asia, and Latin America. Operations include a portfolio of iron ore, copper, nickel, uranium, silver, zinc, molybdenum, gold, and metallurgical coal mines.

Its activities cover the entire global commodity value chain – from exploration, mining, smelting, refining and project development. Additional activities BHP is involved in includes bulk freight, commodities trading, market support, finance, and administration. World headquarters are located in Melbourne, Australia.

BHP

The company has a balanced asset portfolio – expect growth in nickel and a progressive wind down of coal.

Commodities Portfolio

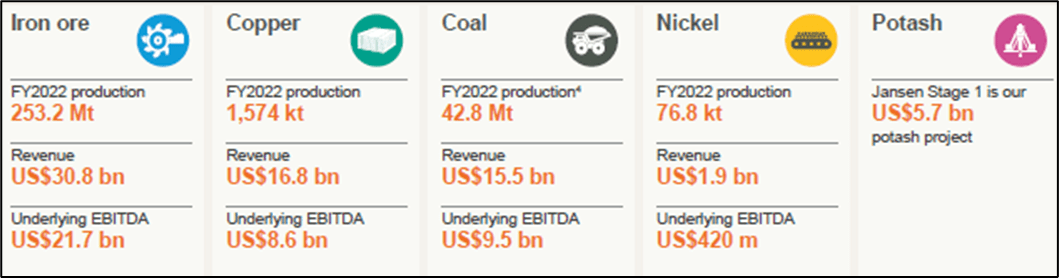

BHP is one of the world’s lowest-cost iron ore producers with its Western Australia Iron Ore (WAIO) operations showcasing high-grade, low emission intensity product. As the new South Flank mine ramps up, the company celebrated record sales volumes FY 2022 on the back of higher commodity prices. The company is among the world’s largest iron ore producers with FY 2022 production hitting ~250Mt and contributing $30B to topline sales.

BHP

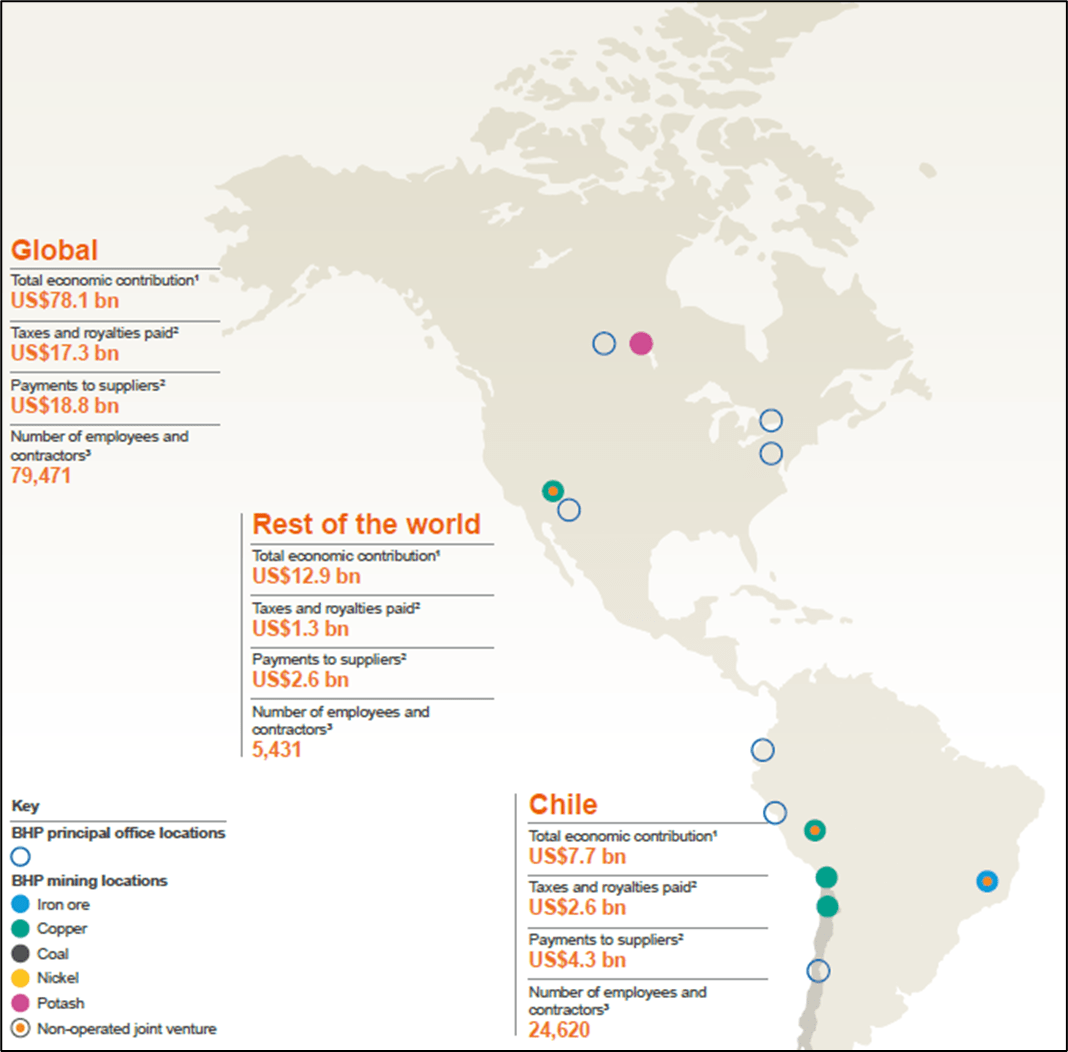

BHP’s Americas operations tout roughly 110,000 contractors & employees, amounting to roughly $100B in total economic contribution. Copper and potash dominate the product line up.

Copper makes up an important part of the company’s portfolio too. BHP holds the world’s largest copper endowment, being a key stakeholder in the Chilean Escondida copper mine. Escondida posted record numbers in 2022 while the firm’s South Australian Olympic Dam asset performed strongly during the back half of the year following major smelter maintenance. The company delivered 1.5Mt of product in 2022, contributing almost $17B to sales.

BHP holds one of the largest potash mines in Canada. Jansen 1 stage 1 is expected to increase BHP’s product diversification ambitions while providing additional growth opportunities. The project tips in on the scales at US $5.7B and is expected to facilitate strategic ambitions to build exposure to the increasingly important fertilizer value chain. The Saskatchewan complex makes up part of Canada’s potash industry which is the biggest in the world.

Metallurgical coal figures in BHP’s commodity line up through its Queensland operations. The company divested its interests in BHP Mitsui Coal (BMC), further focusing efforts on higher-quality product for steelmaking as producers look to optimize blast furnace uptime and reduce emissions intensity. While coal’s importance in the product line up is dwindling, the business unit managed to post $15B in topline sales during FY 2022.

While Nickel‘s contribution to company financials remained marginal, this is likely one of the future growth drivers for generations to come. BHP holds the world’s second largest nickel sulphate endowment globally. The company’s Australia operations achieved first saleable production of nickel sulphate crystals for lithium-ion battery production. The company continues to seek additional nickel resources through exploration, acquisition, partnerships & early-stage entry.

BHP

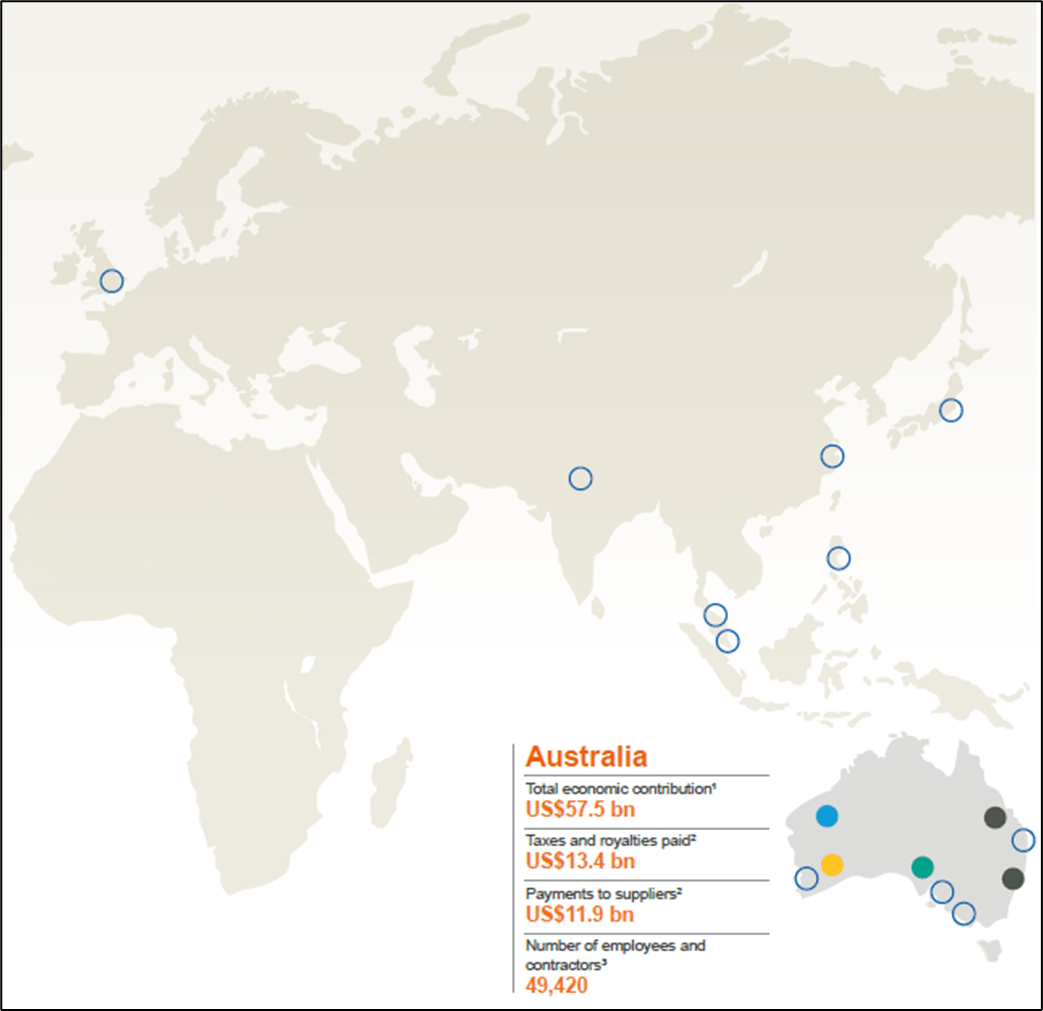

Australia is the company’s home ground with approximately 50,000 direct & indirect employees. Iron ore, copper and coal are heavy focal points.

Financials

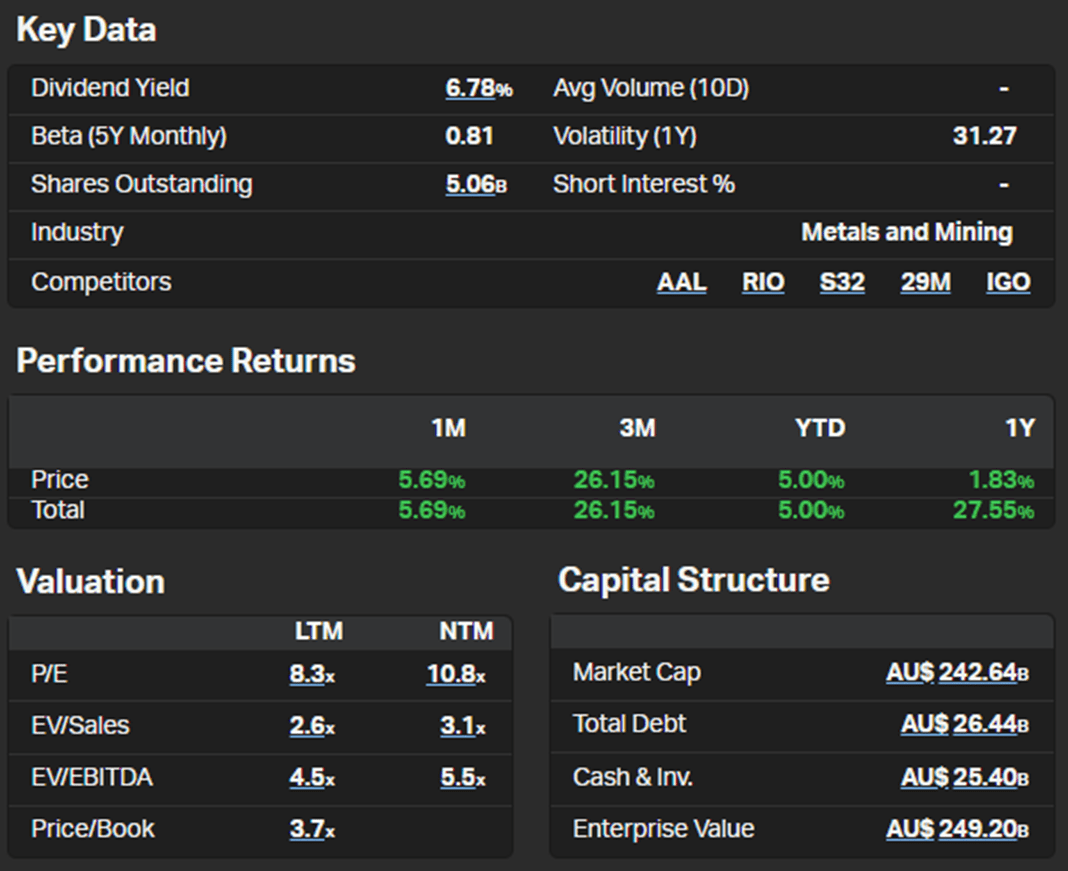

BHP is heavily followed by the money management community – present in 115 different ETFs, there are 239M shares held by US ETFs alone with prominent names such as iShares MSCI Global Metals & Mining (PICK) weighting up to 14% for just one ticker.

Price targets for the mining giant vary with analysts posting stock prices between $38.35 and $57.94. Conservatively, most of the analyst fraternity post either hold (9) or buy (6) ratings.

Koyfin

BHP continues to post some exciting numbers coupled with positive equity price action.

The numbers are compelling – increases in the topline ($39B FY 2020 to $65B FY 2022) married with 85% gross margins, and continued resilience in EBITDA margins that are hovering around 57%. Net income margins remain sizably more enticing than direct competitor Rio Tinto (RIO) – (47% net income v 30%) somewhat reflective of differences in the commodity mix marketed by the two businesses.

Those differences are perhaps explained in forward price-to-earnings ratios – BHP trades at roughly 10.8x forward earnings with Rio Tinto posting slightly less at 9.8x. BHP is a cash machine, generating substantial increases in cash flow from operations, from $15B (FY 2020), $27B (FY 2021) to $32B (FY 2022). While increases in free cash have moderated as the world navigated its way out of the pandemic, expect growth to continue on the back of dollar weakness and commodities upside.

Net interest has been pared down linearly from -$766M (FY 2018) to -$175M (FY 2022), with net cash providing about $300M in interest year over year and debt being trimmed prudently. The divestment of the company’s stake in BHP Mitsui Coal likely contributed for the $840M recognized on the income statement as a gain on sale of assets. Net earnings per share have boomed, from $1.57 (FY 2020) to $6.11 (FY 2022) with little signs of earnings generative upside abating. Dividends have also increased, from $1.20 (FY 2020 – payout ratio of 86%) to $3.25 (FY 2022 – payout ratio of 57%). All in, it’s pretty impressive.

The balance sheet is as rock solid as some of the firm’s iron ore assets – $17B in the bank, receivables reducing, payables increasing, and long-term debt being edged. Current (1.7x) and quick ratios (1.4x) highlight the prudence with which the balance sheet is being run yet $1.2B of goodwill does exist – with its impairment being perhaps the only possible material risk presently.

The miner generates $32B in operating cash flow. Cash dedicated to investments amounts to about $7B – in FY 2022, that included $221M in PP&E sales and another $1.2B in divestitures. Debt is being issued but also repaid at a faster clip, as is stock buy backs being consistently executed ($149M in FY2022) Distributions totaled roughly $17B in FY 2022 making the company not only a good bet on commodities upside, but also a reliable income stream.

Risks

Risks do exist for global commodity players. Like its competitors, BHP remains a price-taker with heavy exposure to macro-economic forced. Interest rates and the value of the US dollar which are both intrinsically linked, play a huge part in determining BHP’s future cash flows. Nickel’s growing importance is likely to lead to capital allocation in the space, perhaps through a strategic acquisition which too could be riddled with pit falls.

But the biggest risk remains China. For example, China imported $173B in iron ore in 2021 alone, equating to 70% of total imported iron ore. BHP, like Rio Tinto, remain highly wedded to economic developments in the Chinese economy with not much of a fallback should the domestic economy subside. Geopolitical risk is high – witnessed by China’s smattering of tariffs on Australia exports. Granted, these have not been on the commodities it desires the most, but there is nothing preventing China being completely shut-off from its commodities lifeline should it decide to strong arm Taiwan into submission.

Key Takeaways

BHP is the world’s largest miner. A best-in-class natural resource play that is likely to benefit from the commodities boom likely to sweep the world over the next decade. With a portfolio of assets increasingly geared towards sustainability and climate change, the company is likely to benefit from macroeconomic tailwinds as we stop drilling for oil and start mining for copper.

The irony of that is, however, the public at large has not yet figured out that we have perhaps simply solved one problem (oil pollution) by creating another (land destruction).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment