imaginima

Both Antero Midstream Corporation (NYSE:AM) and Kinder Morgan, Inc. (NYSE:KMI) are midstream businesses that offer high dividend yields. KMI has an investment grade balance sheet while AM offers a significantly higher yield. In this article, we will compare them side by side and offer our take on which one is a better buy.

Antero Midstream Vs. Kinder Morgan – Balance Sheet

KMI enjoys an investment grade credit rating (BBB with a stable outlook) from S&P, which is evidence that their balance sheet is quite strong right now. AM, on the other hand, has a mere BB credit rating with a stable outlook from S&P.

KMI is set to end 2022 with a 4.3x net debt to EBITDA ratio, which is well below its long-term target of 4.5x. Liquidity is also plentiful with $4 billion of revolver capacity along with about $500 million in cash on hand, and it plans to use some of that to pay down upcoming debt maturities in 2023.

Meanwhile, despite AM’s junk credit rating, the company is making strong progress on improving its balance sheet in pursuit of an eventual credit rating upgrade. As management stated on its latest earnings call:

During the quarter we generated $30 million of free cash flow after dividends and began paying down debt. We have been talking about this critical inflection point for several quarters and it has finally arrived…In addition, AM’s capital budgets will continue to decline, which will drive expanding free cash flow and declining leverage…we still expect to achieve that three times leverage target in 2024. Once we achieve this target, we will be in a position to evaluate or the return of capital strategies.

It is also worth noting that AM has no debt maturities prior to 2026, so it is in very solid financial shape despite its poor credit rating.

Antero Midstream Vs. Kinder Morgan – Business Model

KMI clearly has a larger asset portfolio than AM as it owns North America’s largest CO2 transportation, independent refined products transportation, independent terminal, and natural gas transmission businesses. It also happens to transport roughly 40% of all U.S. natural gas. KMI also has very defensive cash flows as 63% of its cash flow comes from take-or-pay contracts, an additional 25% comes from fee-based contracts, 6% is hedged, and only 6% is commodity-price based. Furthermore, the vast majority of its counterparties are investment grade.

AM, for its part, is much smaller than KMI but does have a multi-decade production profile underpinning its assets. Given that it primarily services Antero Resources Corporation (AR) as its sole client, however, and AR owns a large equity stake in AM, there is a strong incentive for AR to continue doing business with AM, giving AM a very stable cash flow profile for many years to come.

That said, if something were to happen to AR and it experienced financial distress, AM would suffer immensely, so there is certainly risk involved in its business model despite the positive current outlook for its cash flow stability. It is also important to note that AR has a BB+ (stable outlook) credit rating from S&P, so it, too, lacks an investment grade credit rating at this point. The good news is that AR is rapidly deleveraging its balance sheet and could see an upgrade to investment grade in the not-too-distant future.

Antero Midstream Vs. Kinder Morgan – Dividend Outlook

AM’s dividend growth outlook is pretty much nonexistent for the next few years as management is entirely focused on deleveraging the balance sheet right now and does not expect to reach its leverage target of at or below 3.0x until the end of 2024. At that point, it plans to reevaluate its capital return program and could very likely increase the dividend and/or institute a share buyback, depending on market conditions at the time. That said, the dividend looks quite safe between now and then as AM has no debt maturities prior to 2026 and the dividend is expected to be covered 1.69x by distributable cash flow in 2023.

KMI, meanwhile, remains in slow-but-steady dividend growth mode, with the dividend growing by 2.8% this year and analysts expecting 2.8% growth again next year. In fact, through 2026 analysts are expecting a 2.8% dividend CAGR for KMI. While not a fast dividend grower, KMI’s dividend is at very low risk of being cut in our view as this year’s dividend is expected to be covered 1.96x by distributable cash flow in 2023 and the balance sheet is in very solid shape.

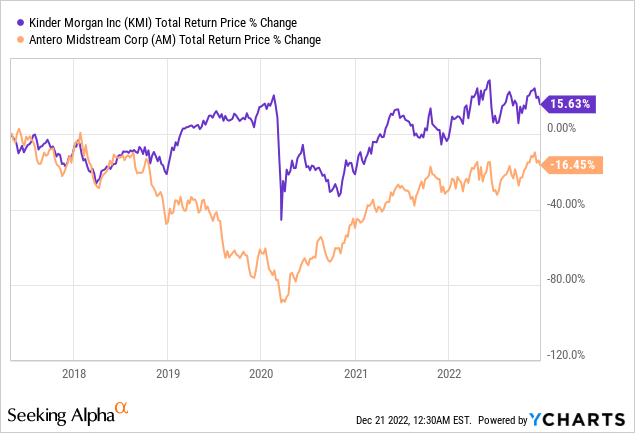

Antero Midstream Vs. Kinder Morgan – Track Record

When it comes to track record, KMI has been the clear winner over the period where both have traded publicly. This is largely due to AM’s substantial dividend cut in the wake of the COVID-19 outbreak as well as its difficulty in growing distributable cash flow per share over the past several years.

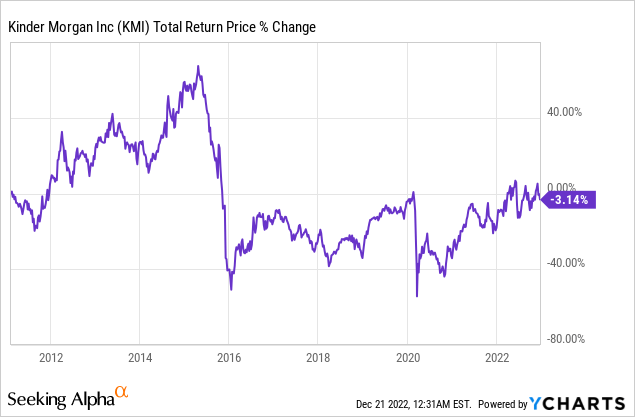

That said, KMI’s long-term track record is hardly impressive either, as it has never recovered from the massive crash in the stock price in late 2015 and early 2016 in the wake of its big dividend cut:

Antero Midstream Vs. Kinder Morgan – Risks And Catalysts

As midstream businesses, the risks and catalysts facing KMI and AM are very similar. Both are heavily focused on natural gas related businesses, so their fates largely rise and fall with the long-term outlook for natural gas and NGLs. That said, KMI also does have exposure to other energy commodities like oil, so it is a bit more diversified. Furthermore, it has much greater geographic and counterparty diversification. As a result, AM is almost entirely a bet on the future growth and financial stability of its primary client AR, whereas KMI is more of a broadly diversified bet on the midstream industry in general, with a greater weight placed on the natural gas industry.

Antero Midstream Vs. Kinder Morgan – Valuation

A quick look at the valuation metrics appears to give AM the edge, as it is cheaper on an EV/EBITDA and P/DCF basis and also pays out a meaningfully higher dividend yield. Furthermore, it is worth noting that AM is cheaper relative to its historical average EV/EBITDA multiple than KMI is.

|

Valuation Metric |

AM |

KMI |

|

Dividend Yield |

8.69% |

6.47% |

|

EV/EBITDA |

8.79x |

9.62x |

|

EV/EBITDA (5-Yr Avg) |

11.23x |

10.22x |

|

P/22E DCF |

7.67x |

8.12x |

|

P/23E DCF |

6.91x |

8.08x |

Investor Takeaway

Both Kinder Morgan, Inc. and Antero Midstream Corporation have solid balance sheets, business models, and very safe dividend payouts at the moment. KMI wins overall on quality given its substantially superior credit rating, larger and better diversified business model, superior near-term dividend growth prospects, and better recent track record. That said, AM holds its own when it comes to its rapidly improving balance sheet, and its cash flow profile looks quite promising for many years to come. While its near-term dividend growth profile and past track record leave much to be desired, it makes up for this with its attractive valuation and current dividend yield.

Overall, our view on these two midstream businesses is that investors who want a one-stop-shop midstream business should pick Kinder Morgan, Inc. over Antero Midstream Corporation due to its greater safety and diversification. However, for investors who want a specialized value pick to augment their midstream portfolio, AM is a more intriguing pick with higher total return potential without too much additional risk.

We rate both a Buy at the moment and note that both businesses issue 1099 tax forms instead of K1 tax forms given that they are C-Corps. While we are not tax experts and this is not tax advice, in our experience this makes them suitable investments for IRAs and 401ks.

Be the first to comment