adaask

Both Enbridge (NYSE:ENB) and Brookfield Infrastructure (NYSE:BIP)(NYSE:BIPC) (where BIPC is the non K-1 issuing economic equivalent of BIP) are BBB+ rated infrastructure businesses with impressive track records.

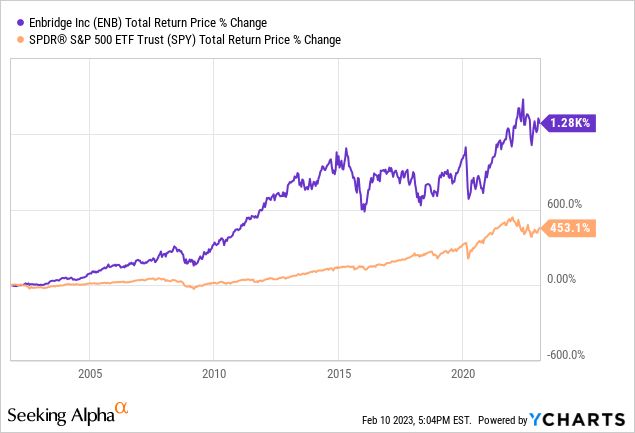

ENB has nearly tripled the performance of the S&P 500 (SPY) since going public:

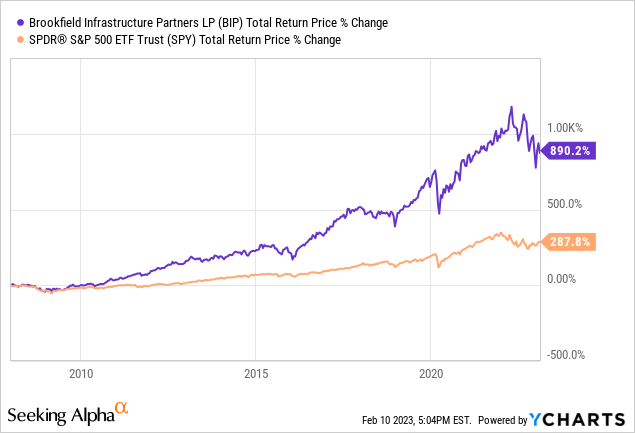

Meanwhile, BIP has more than tripled SPY’s performance since it went public:

Furthermore both businesses have lengthy streaks of growing their payouts to investors every year, with ENB offering a higher current yield and BIP growing at a faster clip.

In this article, we will compare them side by side and offer our take on which one is a better buy right now.

Enbridge Vs. Brookfield Infrastructure: Business Model

ENB’s midstream energy asset portfolio is extensive and well-diversified, providing it with competitive advantages that include:

- economies of scale

- asset, commodity, and geographic diversification

- numerous growth investment opportunities

- a very difficult to replicate and ultimately irreplaceable role in the North American energy industry

ENB’s assets include ownership of the second-longest natural gas transmission pipeline network in the United States, the largest natural gas distribution business in North America, and the longest crude oil pipeline network. ENB’s cash flow is highly stable, with 98% linked to commodity price-resistant contracts and 95% supported by investment grade counterparties.

In contrast to midstream-focused ENB, only ~30% of BIP’s business is midstream focused with the rest being spread across utilities/residential infrastructure (30%), transportation (toll roads, ports, and railroads) (30%), and data (towers and data centers) (10%).

The key to BIP’s exceptional long-term performance has been its shrewd capital allocation strategy. It leverages the competitive advantages provided by its parent company – Brookfield (BN)(BAM) – and then utilizes its own equity along with Brookfield’s institutional funds and a significant amount of long-term, non-recourse fixed-rate debt to invest in exclusive deals. This deal flow exclusivity enables BIP to avoid bidding wars with competitor investors and instead purchase assets on a value basis.

It then once again leverages the Brookfield platform (which brings with it formidable operational expertise, economies of scale, low-cost capital access, and global business network) to enhance the value of those assets. BIP is then able to exit these investments opportunistically and recycle the proceeds into the next attractive opportunity that comes through the Brookfield deal-flow channels, and the process repeats itself once again.

Both business models are highly inflation resistant, with 70% of BIP’s cash flow linked to inflation escalators and 65% of ENB’s cash flow linked to inflation escalators (along with a further 15% enjoying inflation protections).

Enbridge Vs. Brookfield Infrastructure: Balance Sheet

Both BIP and ENB enjoy very strong BBB+ credit ratings from S&P, indicating that there is little concern of financial distress for the foreseeable future.

ENB benefits from substantial liquidity. Additionally, a significant portion of its debt (90%) has fixed interest rates and does not come due until several decades in the future, ranging from the 2030s to the 2080s, providing ENB with a long runway to enjoy a low cost of debt. The company also achieved the lower half of its target debt/EBITDA range (4.5x – 5.0x) with a 4.7x leverage ratio at year-end.

Meanwhile, BIP’s balance sheet is shielded against rising interest rates due to the substantial proportion (around 90%) of fixed rate debt it holds and its seven-year weighted average debt term to maturity. Additionally, 85% of BIP’s debt is non-recourse asset-level debt, which means that in the event of macroeconomic headwinds affecting either its interest rate/debt refinancing conditions or operations, BIP can simply transfer the asset to the lender, thus avoiding the liability from spreading to the rest of the company.

Enbridge Vs. Brookfield Infrastructure: Payout Growth Outlook

Both businesses continue to invest aggressively in growth opportunities and have very impressive multi-decade dividend growth streaks going. That said, BIP has the edge when it comes to growth potential moving forward. ENB expects to grow its DCF per share at a 5% CAGR for the foreseeable future while growing its dividend at a slightly slower pace than that in order to conserve cash to invest in growth opportunities. In contrast, BIP continues to expect a high single digit cash flow per unit CAGR while also growing the payout at a 6-8% CAGR moving forward.

Enbridge Vs. Brookfield Infrastructure: Valuation

Based on the data below, we see that ENB is cheaper relative to BIP across every major metric:

| Metric | ENB | BIP |

| EV/EBITDA | 12.32x | 18.77x |

| EV/EBITDA (5-Yr Avg) | 12.56x | 21.13x |

| P/2023E DCF/AFFO | 10.0x | 13.5x |

| Dividend Yield | 6.7% | 4.5% |

That said, it is interesting to note that BIP is actually cheaper on a historical basis than ENB is given that it trades at a steep discount to its five-year average EV/EBITDA whereas ENB only trades at a small discount to its five-year average EV/EBITDA ratio. This can largely be explained by the fact that BIP has increased its exposure to the midstream substantially in recent years, thereby warranting a lower EV/EBITDA multiple since that industry generally commands a lower valuation multiple.

In fact, we can get a better picture of where BIP’s valuation stands by evaluating it from a sum-of-the-parts angle:

| Business Segment | Exposure | Fair Value Multiple | Peer Comparison |

| Midstream | 30% | 12.3x | ENB |

| Utilities/Residential | 30% | 10.7x | OTCPK:CDUAF |

| Transportation | 30% | 13.5x | CNI |

| Data | 10% | 19.9x | DLR |

| BIP | 12.9x |

When we compare its rough estimate fair value EV/EBITDA multiple of 12.9x to its current EV/EBITDA multiple of 18.8x, the company looks massively overvalued. Of course, BIP deserves to enjoy a Brookfield premium given the aforementioned competitive advantages that it enjoys which in turn provide it with a strong growth tailwind. Nevertheless, the stock still looks a bit on the pricey side.

Investor Takeaway

We love investing in infrastructure at High Yield Investor. In fact, we just bought some more recently. In this article, we compared two of the very best long-term infrastructure dividend growth compounders that hail from Canada.

Overall, we like both of these businesses and rate them both as modestly attractive Buys at the moment. Neither is set up to deliver massive outperformance, but on a risk-adjusted basis and given that we are likely headed for leaner economic times in the near term, we like their strong balance sheets, defensive cash flows, and inflation resistance. While we are finding better places to invest in infrastructure at the moment, it is hard to go wrong over the long-term with ENB and BIP.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment