jimfeng

During these uncertain economic times, it makes sense for investors to be wary about the housing market. Although there is a massive housing shortage in the US, rising interest rates and inflation that brought on the need for higher rates should ultimately blunt the demand for home buyers. Naturally, this has led to some pain for the companies dedicated to the home building space. One example of this can be seen by looking at Beazer Homes USA (NYSE:BZH). In recent months, shares of the business have plunged, but not all of this has been without cause. Although by most measures of profitability, the picture has improved for the business, revenue has started to decline because of market conditions. The good news for investors who have held on this long or who are just considering buying in is that prices look incredibly low at this point in time. Because of this, investors would be wise to consider taking a stake in the firm, even if there is the expectation that market conditions will continue to worsen for the foreseeable future.

Mixed performance

The last time I wrote an article about Beazer Homes USA was in January of this year. In that article, I acknowledged how cheap shares to the business were. But at the same time, I said that shares likely did deserve to trade at a lower multiple than many peers because of the company’s slower historical growth. Even with that, however, I felt that shares of the business were still unreasonably cheap, leading me to rate the business a ‘buy’ prospect. Since then, things have not gone exactly according to plan. While the S&P 500 has dropped by 9.6%, shares of Beazer Homes USA have plunged by 22.4%. This has come even as management tries to reward shareholders. For instance, in May of this year, the company announced a $50 million share buyback program. This may not sound like much at first glance. But given the company’s current market value, this would represent about 11.5% of all shares outstanding.

Author – SEC EDGAR Data Author – SEC EDGAR Data

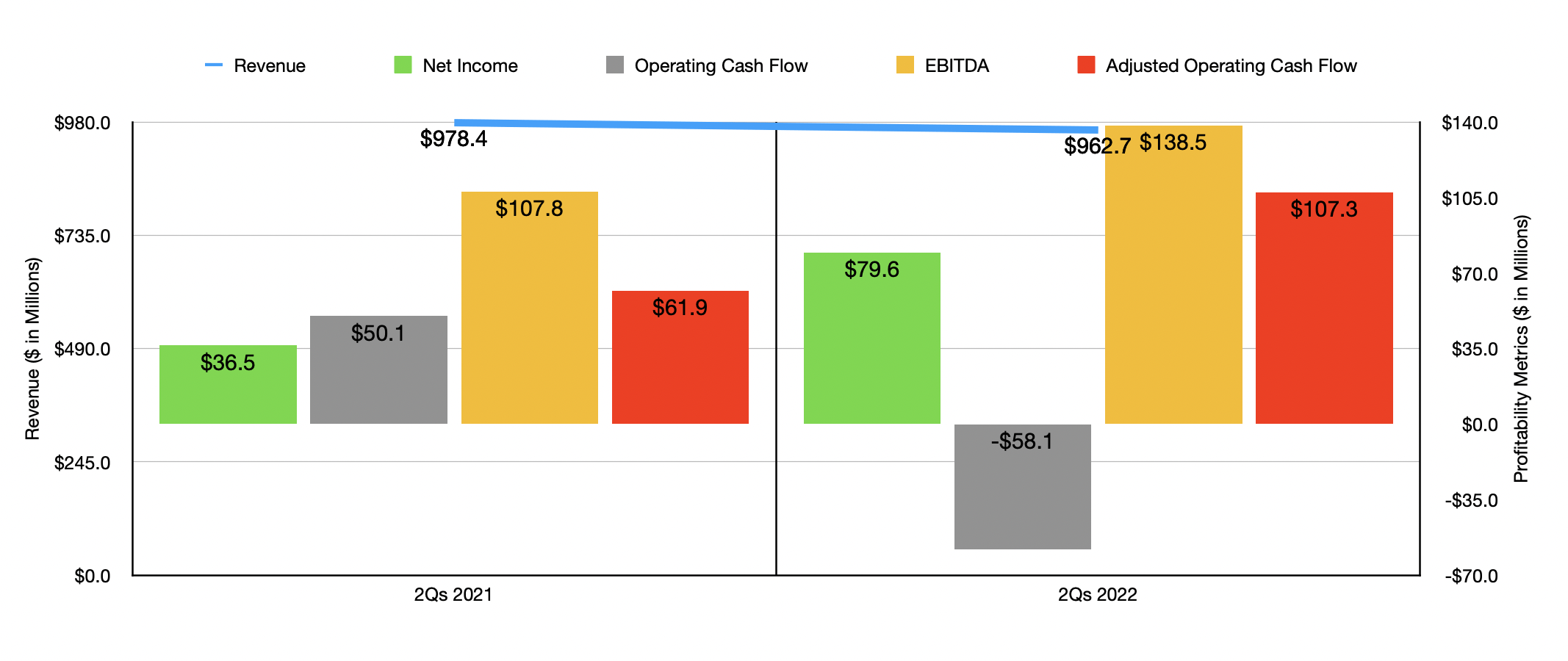

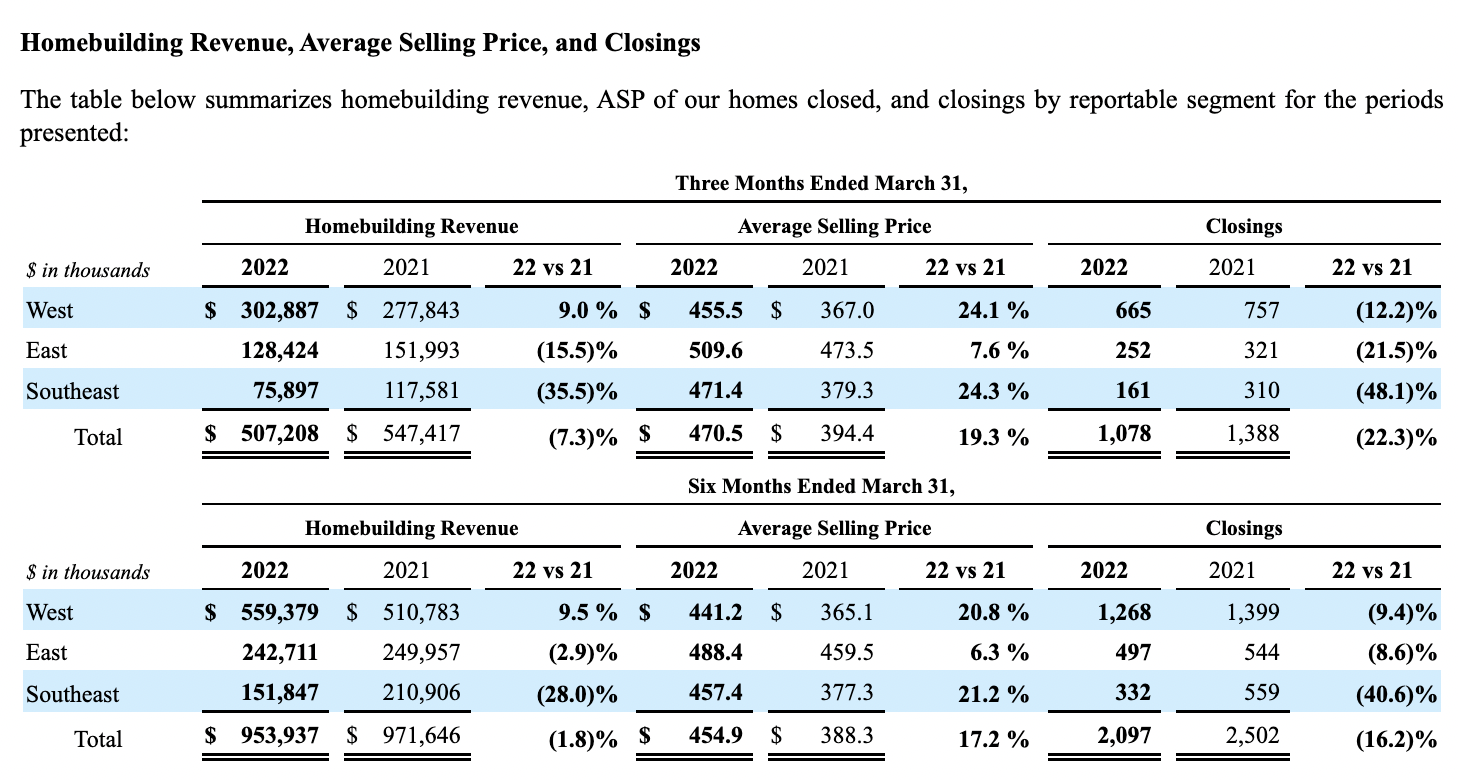

This decline in value was certainly not without warrant. Consider, for starters, how the company has fared on its top line so far this year. In the first half of its 2022 fiscal year, the company generated revenue of $962.7 million. That represents a decrease of 1.6% over the $978.4 million generated the same time one year earlier. Interestingly, this comes as a number of important metrics play out in the company’s favor. During the first half of the year, for instance, the average selling price of properties sold jumped by 17.2% year over year, rising from $388.3 thousand apiece to $454.9 thousand. Part of this has to do with management pushing rising costs onto its customers. But management also attributed this to strong demand caused in part by a short supply of homes. What really brought about the decline in revenue, then, was a 16.2% drop in closings, a number that fell from 2,502 properties in the first half of last year to 2,097 the same time this year.

Beazer Beazer Beazer

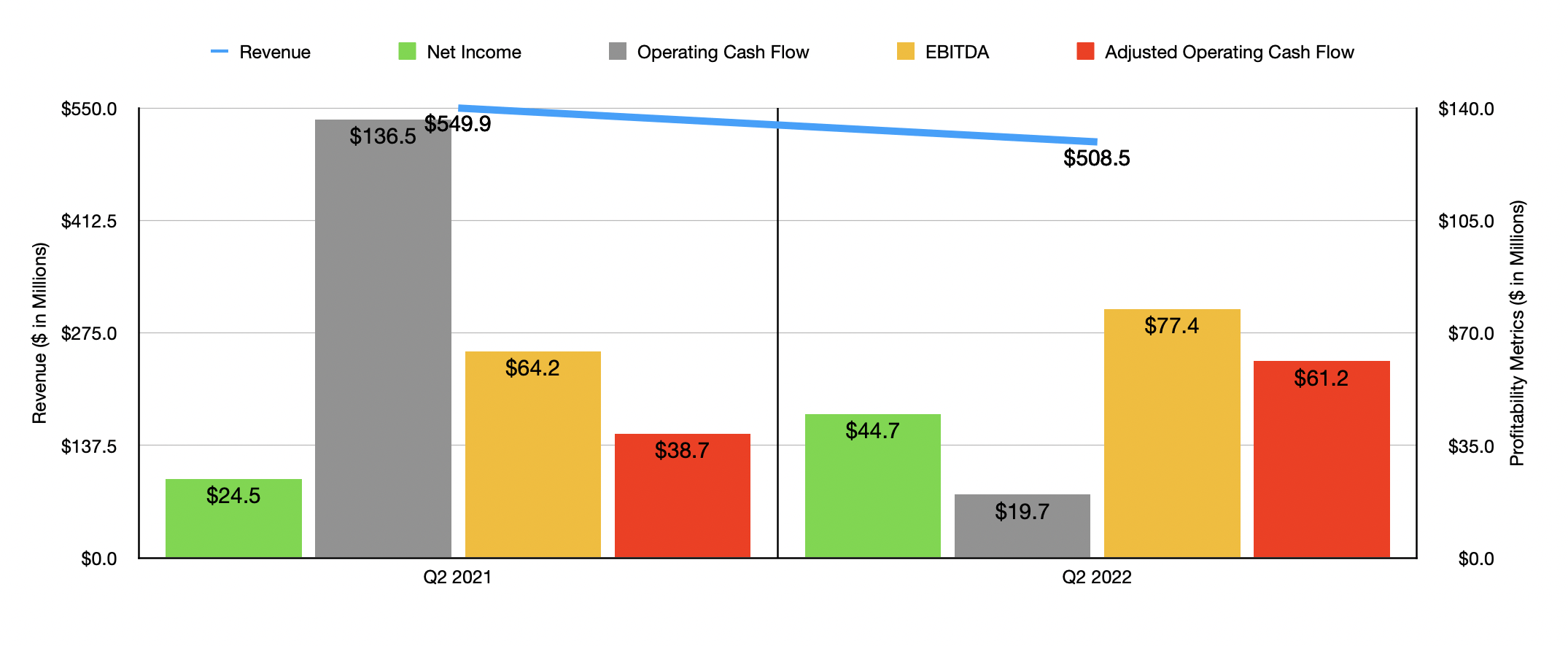

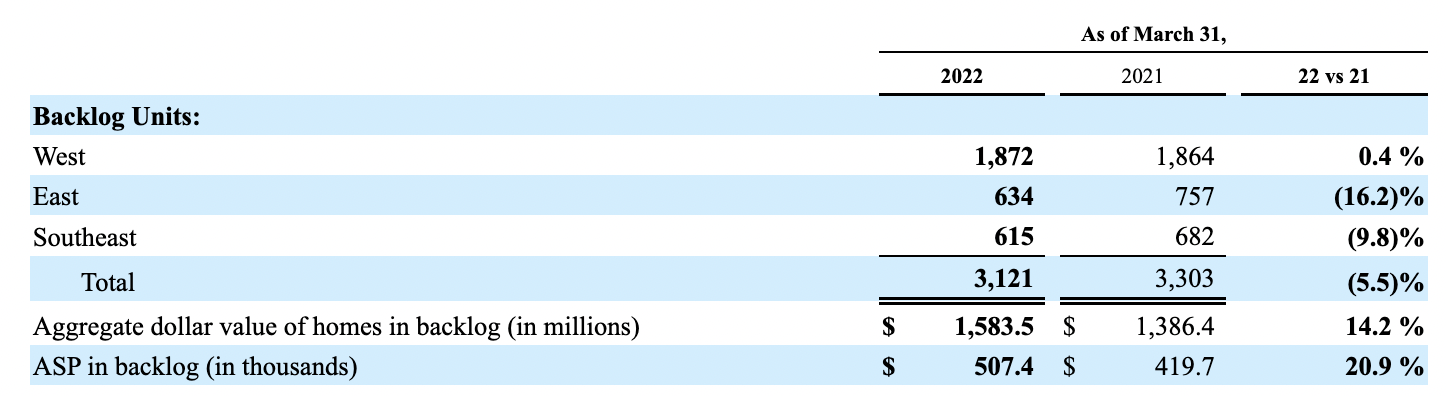

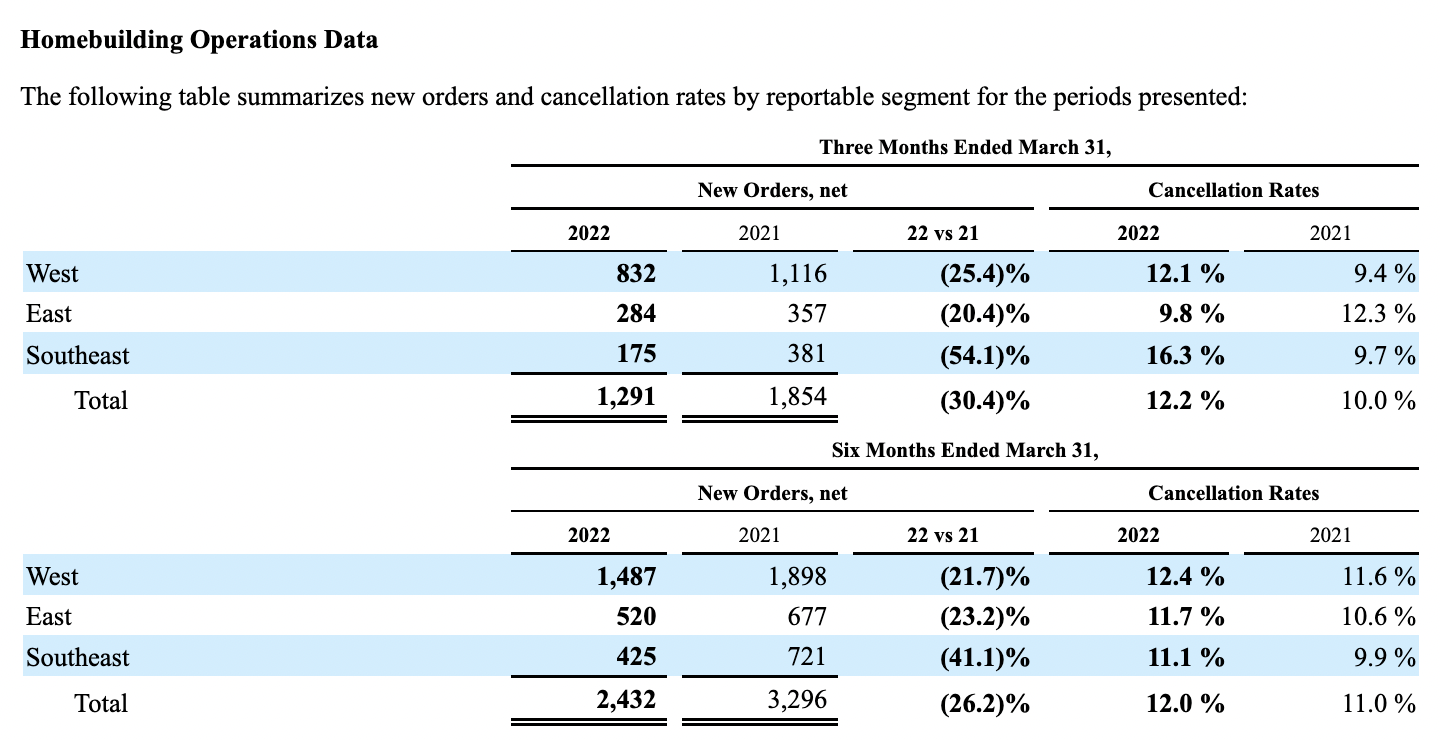

It is worth noting that while the number of closings dropped, backlog has also changed. At the end of the latest quarter, the number of units in backlog totaled 3,121. Although that is up from the 2,908 reported just one quarter earlier, it is down from the 3,303 the company reported for the end of the second quarter last year. This was driven by a 26.2% plunge in new orders during that six-month window from 3,296 units to 2,432. Even with this, however, the value of backlog increased, climbing from $1.39 billion in the first half of 2021 to $1.58 billion the same time this year. This increase in backlog, then, was only made possible by the fact that the average selling price per unit in backlog grew from $419.7 thousand to $507.4 thousand. As the data illustrated above shows, many of these figures were even worse in the second quarter of the year than in the first half combined. This suggests some deterioration in the broader market.

Even though revenue has suffered, profitability for the business has largely improved. Net income in the first half of the year totaled $79.6 million. That’s over double the $36.5 million reported at the same time one year earlier. Operating cash flow dropped from $50.1 million to negative $58.1 million. But if we adjust for changes in working capital, it would have risen from $61.9 million to $107.3 million, while EBITDA grew from $107.8 million to $138.5 million.

When it comes to the 2022 fiscal year as a whole, we don’t really know what to expect. Management has not provided any real guidance for the year, except for the expectation that earnings per share should be $6. That should translate to $188.7 million for the year. Assuming similar year-over-year improvements for the other profitability metrics, this should translate to adjusted operating cash flow of $266 million and EBITDA of $406.8 million.

Author – SEC EDGAR Data

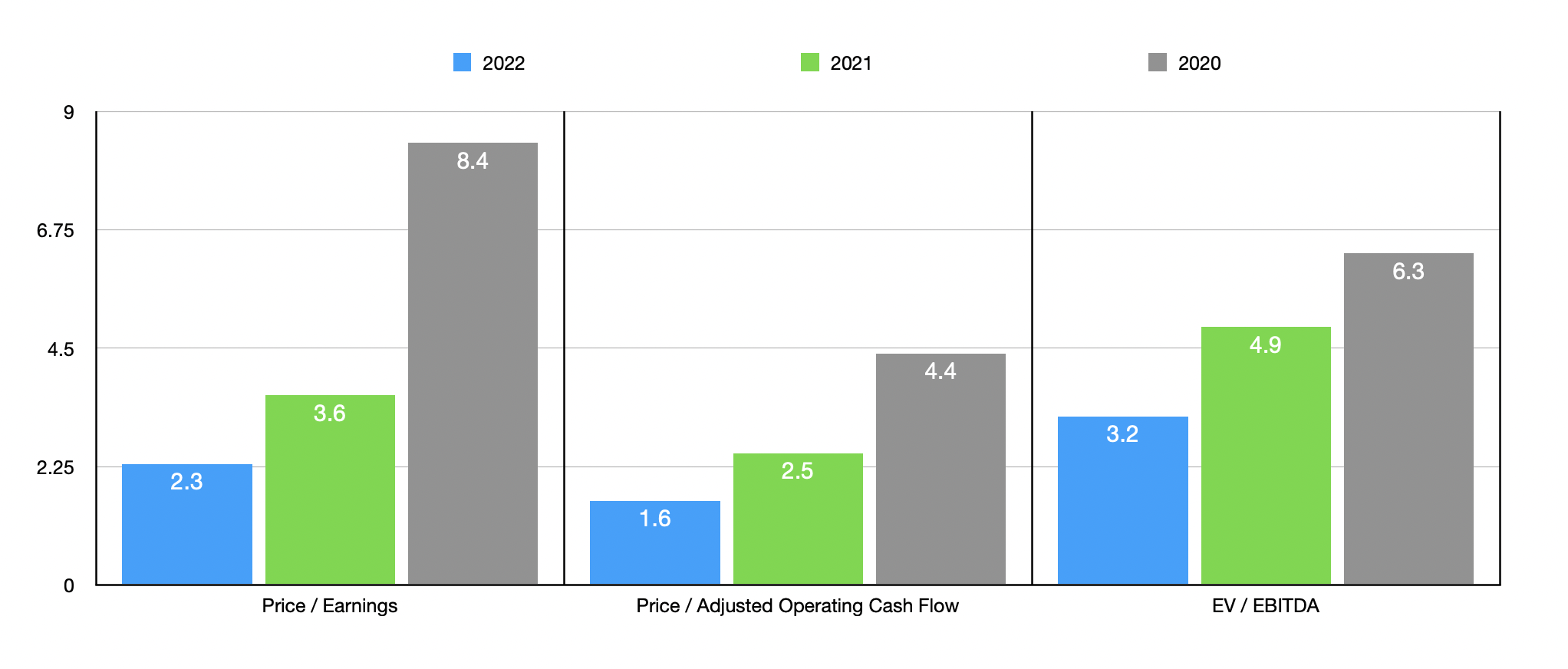

Taking these figures, we can easily value the business. On a forward basis, the company is trading at a price-to-earnings multiple of 2.3. The price to adjusted operating cash flow multiple is 1.6, and the EV to EBITDA multiple should come in at 3.2. These numbers compare favorably to the 3.6, 2.5, and 4.9, respectively, that we get if we rely on 2021 figures. Even if we see performance drop back to what was seen in 2020, these multiples would be 8.4, 4.4, and 6.3, respectively. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 3.2 to a high of 10.2. Only one of the five was cheaper than Beazer Homes USA. Using the price to operating cash flow approach, the range was from 5.7 to 29.7. Using our 2021 figures, our prospect was the cheapest of the group. And when it came to the EV to EBITDA approach, the range was from 3.4 to 5.5. In this scenario, three of the five companies were cheaper than our prospect.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Beazer Homes USA | 3.6 | 2.5 | 4.9 |

| Legacy Housing Corporation (LEGH) | 10.2 | 5.7 | 5.5 |

| Meritage Homes (MTH) | 3.9 | 25.6 | 3.4 |

| Century Communities (CCS) | 3.2 | 25.7 | 3.7 |

| Lennar Corporation (LEN) | 5.4 | 12.6 | 4.5 |

| KB Home (KBH) | 4.3 | 29.7 | 5.3 |

Takeaway

At this point in time, the market seems to be worried about the near-term outlook for Beazer Homes USA. This is perfectly logical when you consider recent financial results and when you factor in the prospect of further pain in the industry. But even if we see some weakness, shares of the enterprise look to be cheap on an absolute basis and they are quite affordable compared to similar firms. Due to these factors, I cannot help but keep my ‘buy’ rating on the company for now.

Be the first to comment