Our Q2 forecast for equities had centred around a mentality shift from a “buy the dip bias” to a “sell the rip” with the Federal Reserve and central banks alike in a tightening overdrive to fight inflation pressures. Consequently, with inflation yet to have peaked and the Fed raising interest rates in 75bps increments, the majority of equity markets have fallen into bear market territory, posting one of the worst first half-year returns in history. Using the S&P 500 as a benchmark, at the time of writing the index has fallen over 22% in H1. Only 1962 and 1932 produced worse returns in H1 at -25.7% and -54.1% respectively (Figure 1).

Figure 1. S&P 500 H1 Returns (1928-2022)

Source: DailyFX, Refinitiv

Can H2 Be as Bad as H1?

Heading into Q3, the bias will remain the same, fade rallies until the Fed pivots away from its extremely hawkish tone. However, with inflation at 8.6% and inflation expectations extremely elevated, a policy put by the Fed is still some distance away. Therefore, momentum will remain with the bears. Keep in mind, as is often the case in bear markets, sharp market rallies are common and get larger the deeper the bear market.

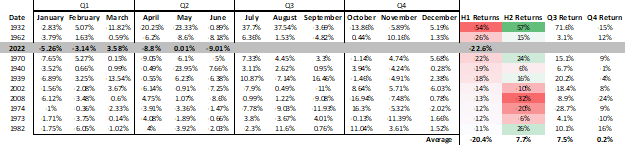

Looking back at the top 10 worst performing H1 returns in the S&P 500 (outside of 2022), H2 has tended to fare better on average as the table below highlights. What’s more, Q3 returns during these years have been pretty good, averaging 7.5%. Using current levels (3800), a 7.5% gain would suggest a move to 4080-4100. Although, should we see recession risks increasingly priced into the market, the S&P 500 risks a move to 3400-3500.

Top 10 Worst H1 Performances in the S&P 500

Source: DailyFX, Refinitiv

Be the first to comment