Philiphotographer/iStock Unreleased via Getty Images

Investment thesis: Despite the already steep selloff in BASF (OTCQX:BASFY) stock in the past few months, there is still a great deal of potential danger for investors looking for a bargain. With a dividend yield now in the 6.7% range and an FWD P/E ratio of less than 10, this European petrochemical giant may seem like an obvious bargain. When factoring in the ever-present threat of the EU-Russia economic confrontation leading to a potential cut in Russian gas supplies, as well as the longer-term consequences to EU gas supplies, stemming from their determination to end their dependence on Russia, this stock becomes a high potential benefit but also high potential risk option for investors. BASF stock could bounce back once the threat of losing natural gas supplies dissipates. It could also go much lower from here if a sustained disruption to natural gas supplies to the EU will force it to shut down operations in Europe. The latter scenario is becoming increasingly likely to happen, as EU leaders seem to be making multiple unrealistic assumptions in regards to EU natural gas supply and demand going forward.

BASF is Europe’s profitable chemical giant, but higher natural gas prices risk wiping out all of its profits this year and beyond.

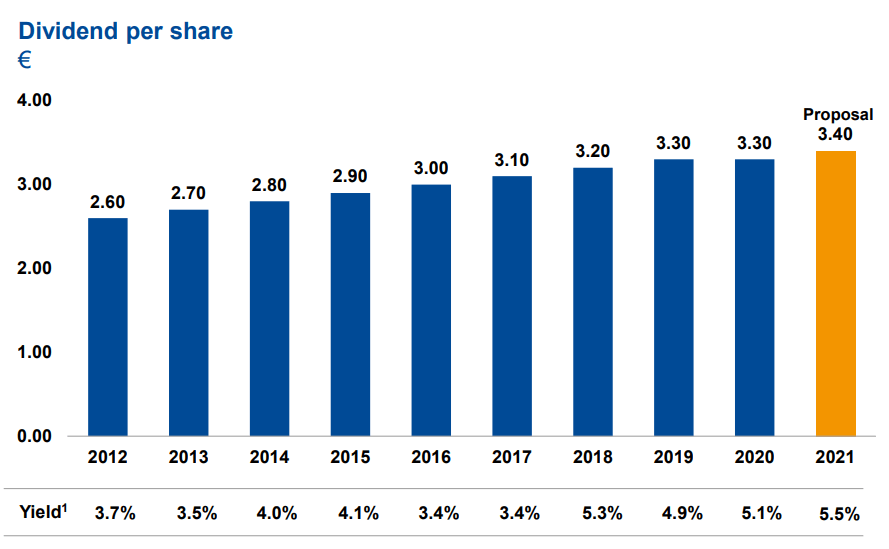

BASF stock is down over 22% YTD, as I write this article. This stock price downturn happened despite BASF’s 2021 financial results looking rather solid. It reported net earnings for the full year of 5.5 billion euros, on revenues of 78.6 billion euros. Rising dividends do not seem to be luring investors.

BASF dividends (BASF)

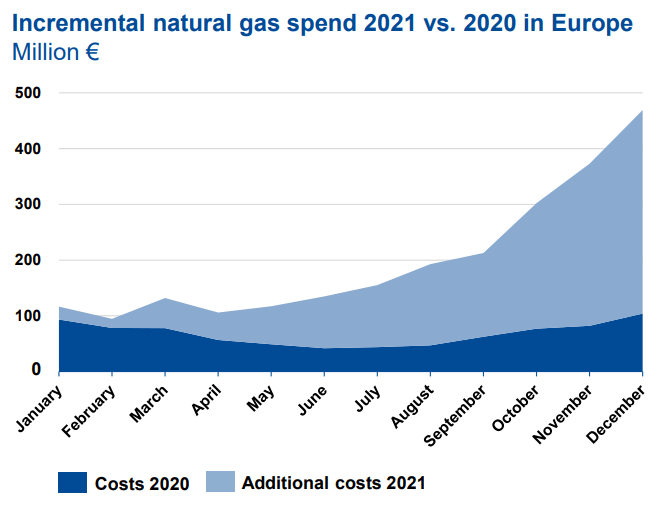

Investors seem to be worried about what the high price of natural gas may do to BASF’s profit margins.

BASF monthly natural gas cost in Europe (BASF)

As we can see, investors are right to worry about it. The higher cost of natural gas that BASF is facing in Europe has the potential to wipe out most of its profit margins this year if the trend it experienced in the fall of last year will persist throughout most or all of this year. This is a likely scenario, given the tight global natural gas supply situation, coupled with the deteriorating relationship that the EU has with its most important supplier of natural gas.

America’s LNG promises can leave the EU suffering from actual physical natural gas shortages in the coming months and years.

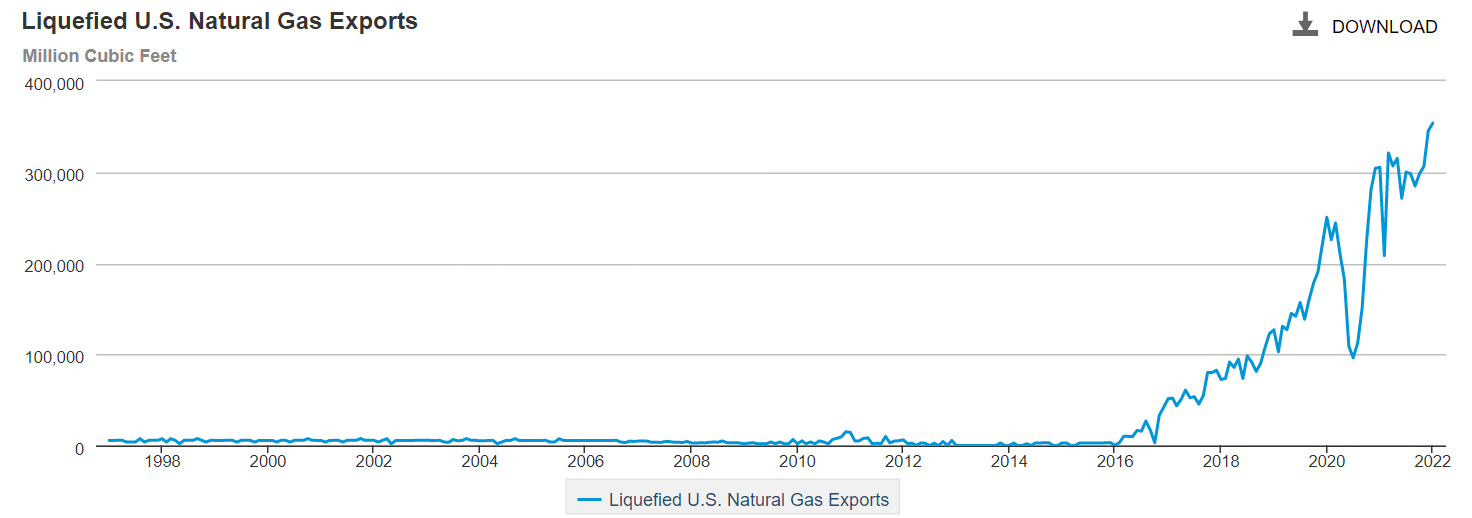

The shale revolution of the last decade turned the US from a perspective growing LNG market for other countries to export to, into a top exporter of LNG to the rest of the world.

US LNG exports (EIA)

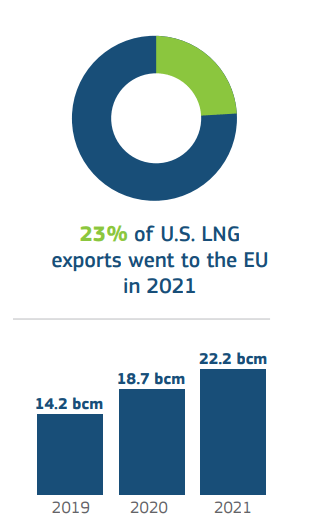

With this steep rise in US LNG exports, Europe’s reliance on US LNG also increased in the past years.

US LNG exports to the EU (EC)

Given that only 23% of America’s total LNG exports went to the EU, there is certainly a lot of potential to divert more of it to the EU, as soon as long-term contracts with Asian and other customers can be nullified, or if they expire. The EU imported about 155 Bcm of Russian gas last year. Diverting all of America’s LNG exports to the EU would by itself eliminate the need to import about 1/3 of that Russian gas.

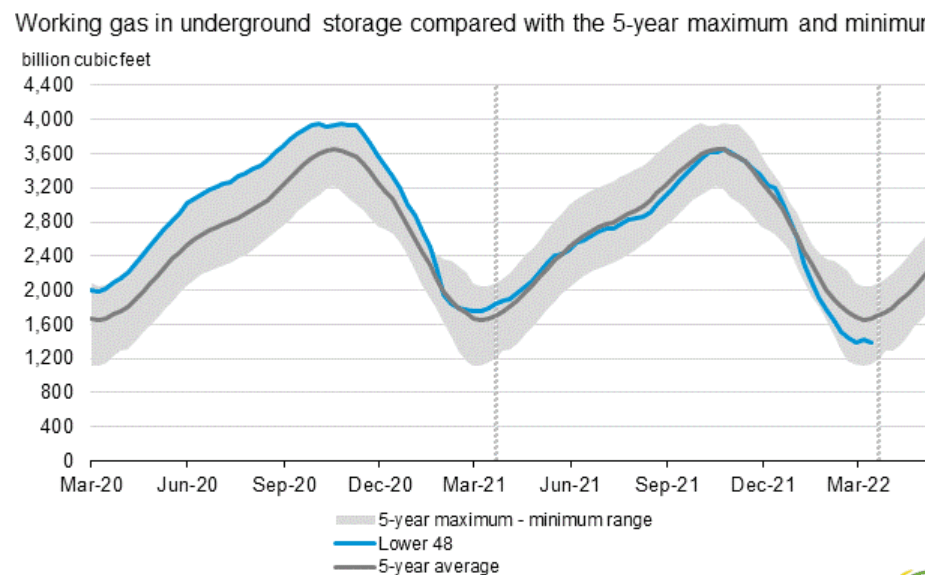

The thing that America is unlikely to do is greatly increase its total LNG exports. Based on EIA data, US natural gas production has been flat since the fall of 2019. Any production increase from current levels will be modest. The shale boom is pretty much over now and the best-case scenario for US natural gas production is a steady, but modest rise in production in the coming years. If shale drillers will run out of prime drilling locations sooner than anticipated, we could see a decline in production. As things stand right now, it is entirely possible that America’s current LNG export volumes are not sustainable, based on the fact that an inventory gap has opened up in the last few months, below the five-year average.

EIA natural gas inventories (EIA)

While inventories have fallen this far below the five-year average in the past, it does seem that there is some coincidence between the US attempts to increase LNG supplies to the EU and the widening inventory gap. At 17% below the five-year average, it is just a little bit better than the 22% gap in natural gas inventories in the EU.

It remains to be seen whether or not the US will come through with its pledge to at the very least partially offset Europe’s current dependence on Russian natural gas. The way I see it, there is a significant chance that the US will fall short on its pledges, even as Europe moves ahead with measures meant to reduce imports from Russia, while Russia is also taking steps to shift its export flows East. US natural gas production can easily disappoint in terms of growth. The more the US market gets tied to the Old World through LNG, the narrower the price gap between the two will be. High energy prices tend to lead to public discontent, given that we use on average about twice as much energy as the average European does. There have been some political grumblings already in regards to the price effect that LNG exports are having on US natural gas prices. At some point, such pressures may serve to limit exports.

There is also the very real possibility that the US will completely shift its longer-term geopolitical focus on the Pacific region, given that the economic center of gravity of the planet has shifted there in the past few decades, while Europe is growing increasingly irrelevant in this regard. In fact, I find the current geopolitical tensions in the region surprising, to say the least. It is hard to understand why both Russia and the US are so focused on jockeying for influence in the region. I am sure they both have their wider calculations in mind that make some sense to them. If so, I have the feeling that it is in fact Asia that both are thinking off for the longer term, while the whole confrontation in Europe is more of a way for both sides to distract each other. For the longer term, I do expect that the US will shift back to the Pacific, and sending most of its LNG exports there will therefore make more sense. We already know that Russia is also shifting east, building more pipelines, and redirecting its own growing LNG exports to the region. There is a chance that both the US and Russia will shift their natural gas exports away from Europe, leaving the EU in a bind.

For BASF, this can become fatal to its European operations. Not only is there a risk of the current high energy prices persisting, which is not sustainable for most petrochemical and other industries that use large volumes of natural gas, but there is the very real risk that the EU will be faced with actual volumes shortfalls, no matter how high it may be willing to go in terms of paying price for its natural gas imports. The global natural gas market seems to be tight and it is likely to remain so for the foreseeable future. There is every chance that this will become a game of musical chairs and the EU will be the one left without a seat.

Investment implications:

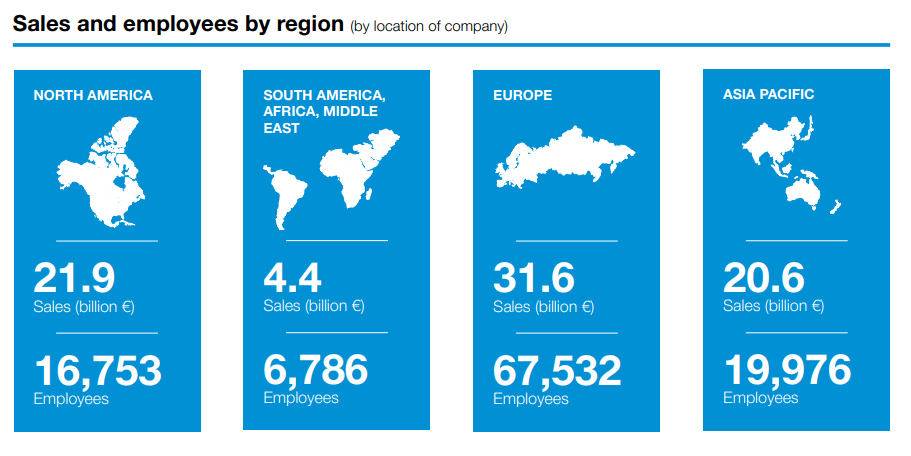

BASF sales by continent (BASF)

Even though BASF is a European company, its sales and operations are diversified throughout the world. This is the one thing that BASF has going for it, in the event that the current state of flux in the EU energy sector will leave EU industrial operations stripped of their natural gas needs.

Geographical diversification can only provide so much protection for investors in case the EU energy situation will go south going forward. Europe is home to about 37% of its sales, and the majority of its employees are also located in Europe. Its non-European operations will provide some protection, and it should be enough in case of a short-term shock in Europe. If the energy crisis will be sustained and its operations will be idled for a prolonged period, there is no telling how low BASF stock can go.

There is also a chance that the current crisis will fade and a combination of a resolution to the Ukraine war, together with some policy wisdom being demonstrated by EU officials will alleviate the current natural gas price crisis in the EU. In that case, BASF investors will lock in this very generous 6.7% dividend, while the price of the stock could easily rise by 50% or more in the short-term, retracing the losses it suffered in the past year or so, as a side-effect of the high natural gas prices that predominated in the EU market. The stock price has the potential to rise even further beyond that if all the factors will fall into place in the company’s favor going forward.

Some recent analyses on Seeking Alpha have been correctly identifying the bargain price that this stock is currently trading at. An article by SA author Brad Thomas makes for a compelling argument about the generous dividend, as well as the potential for stock price appreciation, which he sees potentially increasing by as much as a factor of three in the next few years. The threat of high natural gas prices due to the war in Ukraine was also correctly identified in the article. The threat that is not fully identified and I believe the market overall is failing to identify is the prospect of the EU energy policy going forward leaving it without Russian gas, even as other potential sources such as US or Qatar’s LNG will fall short of promises or expectations. When those shortfalls will emerge, there is a chance that it will be too late to rebuild the business relationship with Russia.

BASF, together with most of its industry peers in the EU is faced with a catastrophic situation in the worst-case scenario, where industrial activities will be shut down, in favor of keeping the heat and the lights on for households and service-oriented businesses, in the event of a sustained shortfall in natural gas supplies. Even in a best-case scenario, I foresee EU natural gas prices remaining persistently high. The rupture of relations with the EU’s largest supplier of energy is permanent, while its second-largest supplier, Norway is set to see a peak in oil & gas production within about two years, with yearly declines becoming a regular occurrence. US, Qatar, Australia, and others may make up part of the shortfalls, but they will not come close to making up the full potential shortfall that the EU could see if it all goes wrong. Demand destruction thus becomes the most likely outcome in Europe and industry is where the bulk of the demand destruction will occur.

Given that even in a best-case scenario BASF is looking at high input prices in Europe, I am not at all confident that the three-fold increase in its stock price is feasible. As profits get squeezed by high energy costs, the dividend may also not be as safe as it is currently perceived. In a best-case scenario, I do foresee its stock retracing its losses of the past year, while the dividend will be maintained. However, given geopolitical developments, with Russia’s commodities flows set to shift towards Asia at a blistering speed, I also see the odds of a worst-case scenario unfolding for the EU economy and for BASF being substantially higher than a best-case scenario. BASF can be a bargain investment at current stock price levels, but at most, it should be the object of a timid nibble at this point, rather than an investment option that investors should plunge into head-first. It is worth keeping an eye on as the geopolitical situation continues to play out because the outlook might change to positive. But for now, it is mostly a wait-and-see in my view.

Be the first to comment