U. J. Alexander

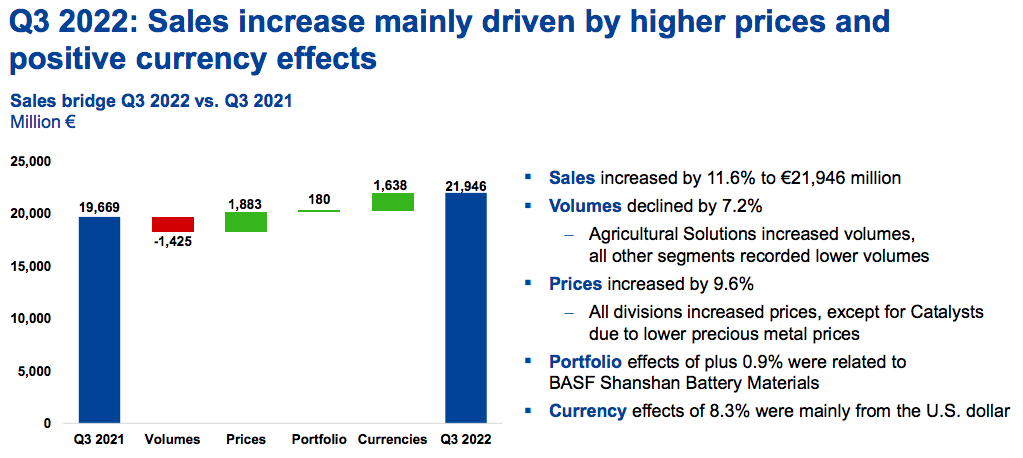

Over the year, we extensively cover the German chemical player BASF (OTCQX:BASFY, OTCQX:BFFAF), providing a specific update on the company’s direct/indirect exposure to Russia. During Q2, our internal team has commented on BASF’s preliminary figures and BASF’s full half-year performance disclosure. This time, we have decided to analyze only the Q3 full presentation; however, compared to the Q3 preliminary press release, the company reported an adjusted operating profit of €1.34 billion, outperforming the consensus estimates by 3% (at that time). Looking at the aggregate level, top-line sales increased thanks to positive FX development and higher chemical prices, recording a plus 8.3% and 9.6% respectively. Volumes were a headwind with a negative performance of 7.2%.

BASF Q3 sales development (BASF Q3 results presentation)

Q3 Results

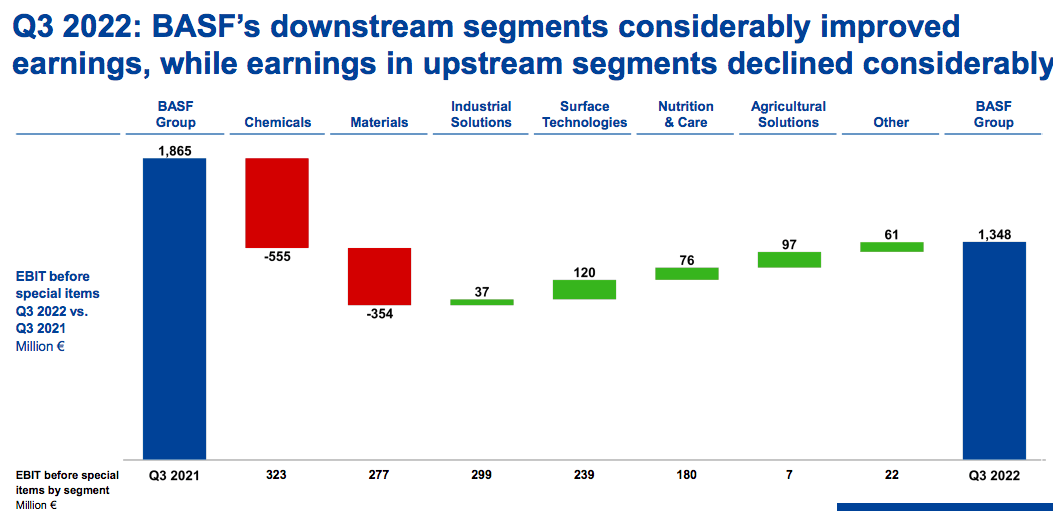

Looking at BASF’s division, we can report the following key takeaways:

- On a yearly comparison, the Chemicals and Materials divisions were down on EBIT by 63% and 56% respectively. Both segments recorded negative volume due to lower Chinese demand, but most importantly higher energy prices that are affecting BASF’s profitability in Europe (we suggest our readers check on this interesting FT publication).

- The Surface Technologies division was the clear positive outlier in Q3. The adj. operating profit increased by more than 100% year-on-year, supported by battery material and emission catalysts.

- A strong performance was recorded also in the Industrial Solutions segment thanks to a positive delta in margin growth.

- The Nutrition and Agricultural solution delivered a good set of numbers thanks to the company’s pricing power in all regions. Reading the notes, the positive catalyst was BASF’s herbicides solutions.

BASF sales development (BASF Q3 results presentation)

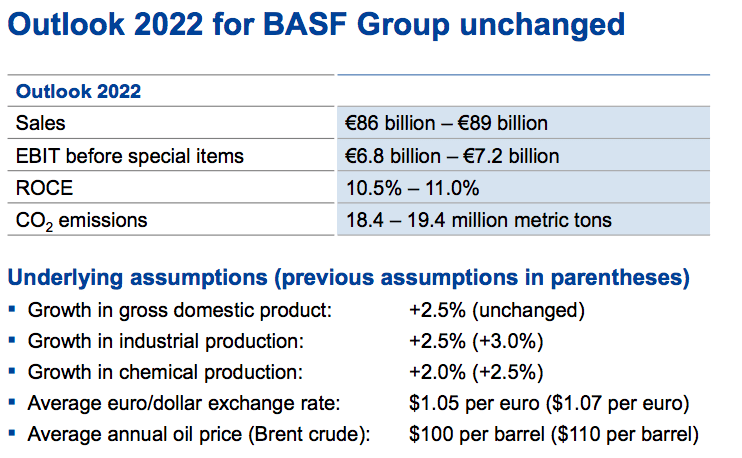

Conclusion and Valuation

To sum up, the adj. operating profit (before special items) stood at €1.3 billion, down by €517 million versus Q3 2021. Despite that, cash flow from operating activities increased, and the company confirmed its 2022 guidance, maintaining a midpoint of €87.5 billion and €7 billion in turnover and EBIT. Implicitly, we derive BASF’s guidance for the Q4 EBIT which stands at €500 million, much below consensus estimates.

BASF 2022 guidance (BASF Q3 results presentation)

To contrast energy price hikes, BASF announced a cost reduction program with cost-saving initiatives for a total amount of €500 million per year until 2024. As we can note in the presentation, the German giant recorded €2.2 billion higher natural gas costs versus the same period last year. There was no disclosure on the Wintershall Dea dividend. Last time, we lowered BASF’s valuation, and we valued Wintershall Dea at €4 per share in the company’s SotP. Today, given the company’s latest development, we decide to maintain our buy rating and lower our target price to €62 per share, pricing in a lower end market demand in the automotive and construction sectors, a higher interest rate environment (BASF released a net debt of €18.9 billion), and ongoing increases in the energy price development. Having said that, as already mentioned, BASF is one of Mare Evidence Lab’s top picks with a 40% upside and a current yield of more than 7%. With operations diversified across the globe, we value BASF with a normalized P/E of 7x, arriving at a valuation of €62 per share.

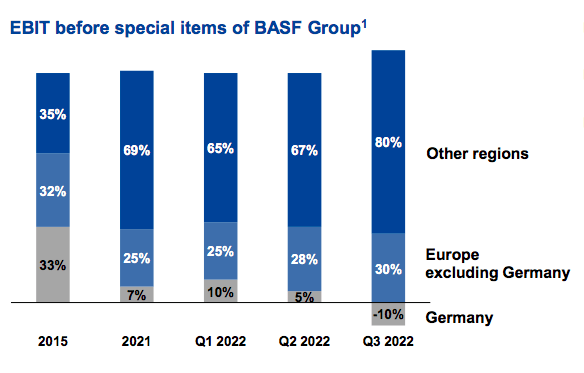

BASF EBIT by regions (BASF Q3 results presentation)

Be the first to comment