Coming off an investing cycle in FY19, Baozun (BZUN) appears set to reap the benefits of its investments in FY20. Given its dominance in a fragmented market and its core business strengths, Baozun remains well-positioned as a key beneficiary of the rapid growth in Chinese brand e-commerce. Thus, in a base case scenario, I see non-GAAP operating margins returning to FY18 levels later this year, with a demand normalization scenario also set to boost the top-line in FY20. A conservative ~1x PEG multiple on FY21 earnings yields strong upside at current valuations, and thus, I see clear upside potential to BZUN at these levels.

Strong 4Q Results Matched Expectations

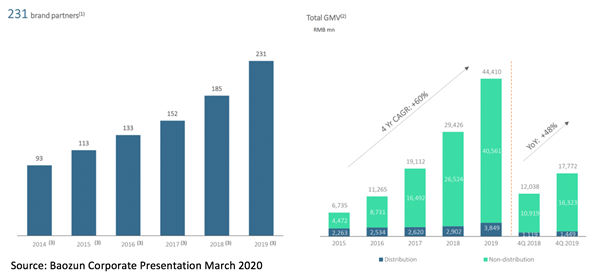

BZUN achieved 48% YoY GMV growth and 27% YoY revenue growth in 4Q19, which is solid given the recent loss of a large handset brand partner. More importantly, same-store sales growth (SSSG) rose 51% YoY, despite the challenging macro backdrop as electronics performed strongly during Singles’ Day. Clothing, on the other hand, displayed weaker growth, but sportswear has continued to perform well, along with fast-moving consumer goods (FMCG).

I would also highlight the strong new brand partner acquisition during FY19, which climbed to 231 in 4Q19 (vs. 185 and 223 from 4Q18 and 3Q19, respectively). The eight new brand partners added during Q4 (and the broader brand partner portfolio) were heavily weighted towards apparel, electronics, and food and health. While the coronavirus pandemic has adversely affected the brand acquisition process weighing on the speed of acquisition in FY20, I believe its value proposition remains intact, and thus, I am optimiztic about Baozun’s prospects as the macro outlook normalizes.

Overall, the 4Q performance was solid. Excluding a CNY42 million loss from a fire in October, Baozun achieved a non-GAAP operating margin of 9.3% due to disciplined fulfillment and lean marketing costs. Driven by effective working capital management, the company also achieved cash flow from operations of Rmb300 million in FY19, driving free cash flow to positive levels for the first time at >Rmb100m.

1Q20 Revenue Guidance In-Line, with Signs of a Recovery Emerging

Baozun guided toward 1Q20 revenue of between RMB1,400m to RMB1,450m, (+9-13% YoY), with GMV projected to grow at least 10% YoY. On a month-to-month basis, January has been strong, surpassing internal expectations, though COVID-19 has weighed on the February results, as expected. Interestingly, however, management has noted that thus far in March, the majority of Baozun’s key partners have recovered, especially during the Queens Day (March 8th) campaign, returning to approximately 80% of normal operations. Supply has also recovered quickly, with Baozun continuing to bring more inventory and products online. Compared to other e-commerce platforms that are guiding toward a negative 25-30% impact on 1Q GMV, Baozun’s 1Q outlook seems especially optimiztic as its key partners in both sportswear and soft luxury brands remain resilient.

Nonetheless, the declining take rate remains a source of concern, though management intends to reverse the trend by pursuing higher-quality growth by focusing on brands with above-average returns. It will also implement brand partner “optimization,” which may imply terminating relationships with certain partners if maintaining such a relationship is deemed economically unattractive. Additional plans to further optimize costs include the delay of new warehouse construction, an increased focus on staff productivity, and the optimization of key technology projects. Execution across key cost initiatives should drive meaningful improvement in BZUN’s margin profile, heading into the back-half of the year.

Baozun Remains an Attractively Priced Proxy to the Chinese Consumer

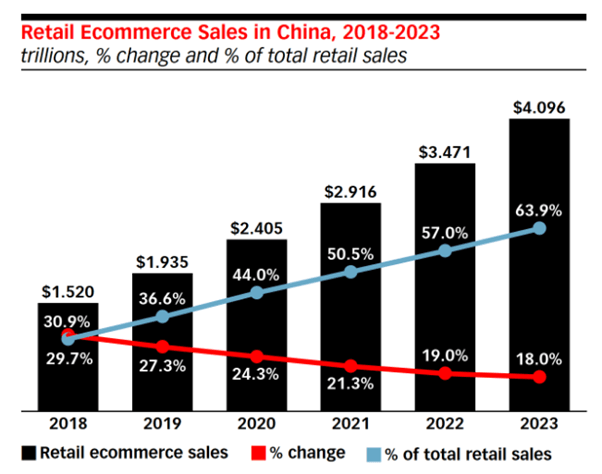

One of the key tenets of the BZUN investment thesis – its exposure to the Chinese middle-class – remains intact, offering the company a compelling long-term growth runway. Rising incomes should serve as a strong tailwind for eCommerce penetration in China, which is anticipated to reach 63.9 percent by 2023. With large international brands, such as Nike and Starbucks, leaning on partnerships with Baozun to drive their e-commerce push, I expect more large international brands entering China to look towards Baozun to grow their Chinese presence.

Source: eMarketer

Assuming a discounted PEG multiple of 1x on FY21 EPS of $1.60 (implying a 33x P/E based on 33% forward earnings growth), I would conservatively peg BZUN’s fair value at ~$52.80, assuming a base-case recovery in the second half of 2020. Key risks to the BZUN thesis relate principally to the duration of COVID-19, which could adversely affect sales growth. Retail, in particular, may be significantly impacted by the persistent disruption of logistics as well as deferred deliveries. Other risks include rising competition, and contractual risks as key global brands’ contracts come up for renewal. Looking through the near-term uncertainties, however, I firmly believe BZUN’s long-term runway remains intact, with current valuations presenting a reasonable buffer against downside risks.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment