Bank OZK

Introduction

The last time I covered Bank OZK (NASDAQ:OZK) was in April of last year, when we discussed the bank’s attractive yield. In this article, we’ll also do that. However, there’s more to unpack, as we’re in a rather tricky situation of deteriorating credit health, weakening economic growth, and a hawkish Fed eager to fight inflation by hiking into an economic slowing cycle. Hence, the company’s just-released Q4 quarterly results are a great opportunity to discuss the bigger picture and the company’s incredible resilience. After all, the company not only beat estimates, it showed terrific credit quality, loan growth, and subdued operating expenses.

While OZK isn’t yielding more than 4% like some high-yield stocks, it has high dividend growth and a high likelihood of sector outperformance. My opinion remains to buy OZK during corrections as it trades close to 50% below its fair value.

Now, let’s dive into the details as we discuss what makes OZK a truly special outperformer.

An Outperforming Regional Bank & A Decent Dividend

I’m not a huge fan of regional banks (in general). I’ve said that in a lot of articles, even though I own a regional bank in my dividend growth portfolio (Huntington Bancshares (HBAN)).

Someone once said that buying (regional) bank stocks is like picking up pennies in front of a steamroller.

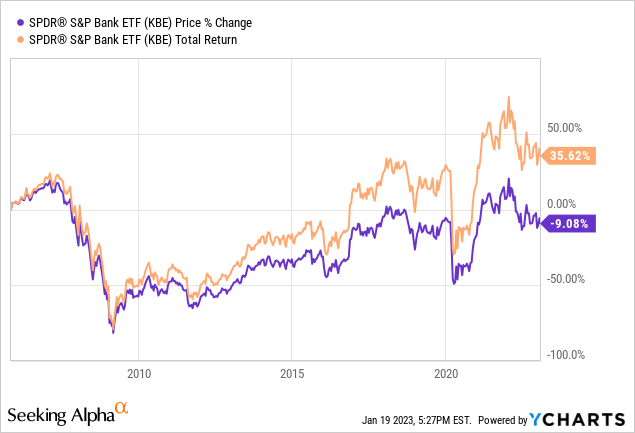

Using the SPDR S&P Bank ETF (KBE) as a benchmark, banking stocks still haven’t recovered from the Great Financial Crisis (“GFC”). Only on a total return basis (reinvesting all dividends) do we see that investors are up close to 40%. Needless to say, that is not a lot.

So, what are good reasons to own regional banks?

For starters, most offer decent dividend yields with growth rates that exceed inflation. Banks also regularly sell off quite substantially, offering investors good valuations and attractive risk/rewards.

While some banks can keep up with the market or even beat the market on a long-term basis, most are just great tools to add some income to one’s portfolio.

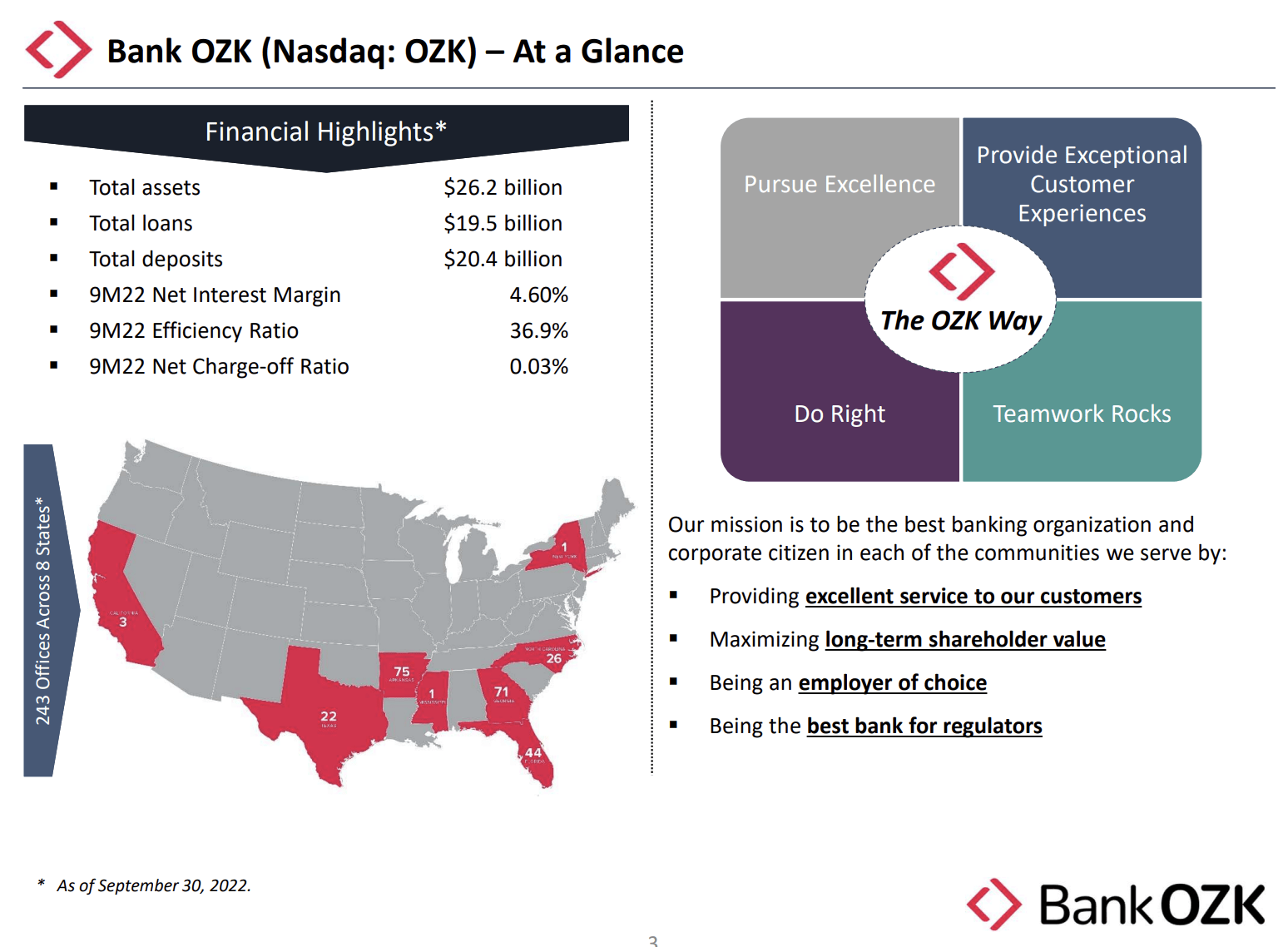

That’s where Bank OZK comes in. Headquartered in Little Rock, Arkansas, the bank is one of the smaller regional banks. Founded in 1903, OZK has a market cap of $4.7 billion. That number needs to be at least $7.6 billion to make it into the top 20.

Bank OZK

The good thing is that size doesn’t matter. At least not when it comes to bank performance.

Bank OZK, which used to be named Bank of the Ozarks before July 2018, has grown thanks to acquisitions that expanded its footprint and capabilities and organic growth.

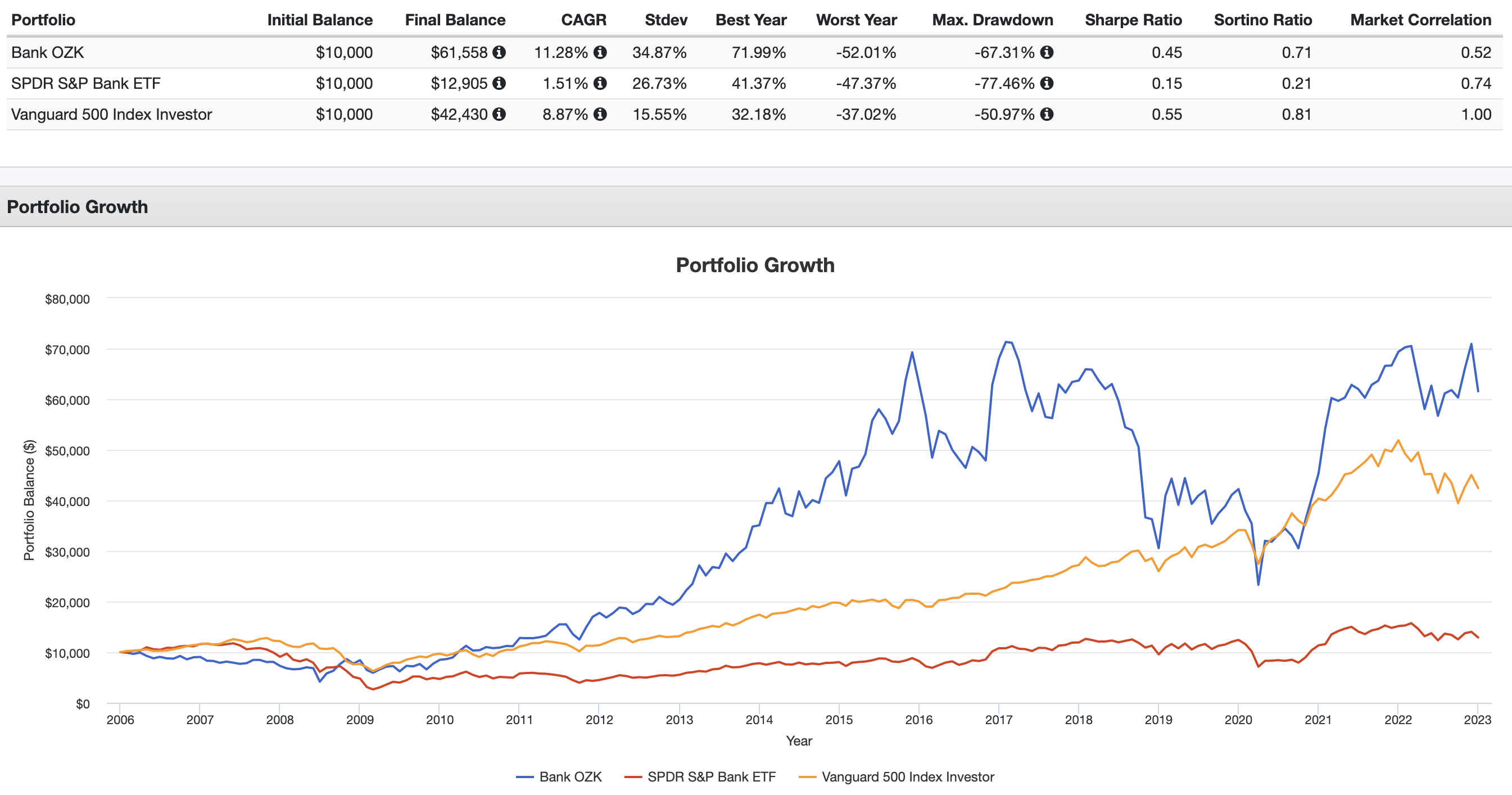

Thanks to these efforts, the bank has returned 11.3% per year since 2006. This includes the Great Financial Crisis, which temporarily erased 67% of the bank’s market cap. Due to this crisis, the aforementioned KBE ETF has returned just 1.5% per year (pennies and steamrollers).

Portfolio Visualizer

While OZK is more volatile, given its standard deviation of 35%, the bank has consistently outperformed its peers. Over the past ten years, OZK shares have returned 11.7% per year. The KBE ETF returned 8.8%. The S&P 500 returned 12.4%.

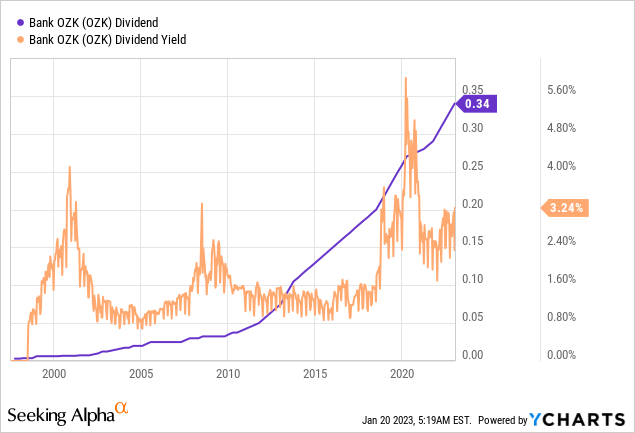

In this case, the bank also comes with a very satisfying dividend.

OZK shares currently pay $0.34 per quarter per share. This implies a 3.4% dividend yield.

This is higher than these ETFs:

Moreover, dividend growth is high and consistent. The ten-year average annual dividend growth rate is 17.0%. As this includes a big part of the post-GFC recovery, that rate has come down. Over the past three years, however, that number is still 9.9%.

These are the most recent hikes:

- January 2023: +3.0%

- October 2022: +3.1%

- July 2022: +3.2%

- April 2022: +3.3%

- January 2022: +3.4%.

As one can see, OZK shares regularly hike the payout in small steps. However, these small steps add up over time.

The payout ratio is 30%, which is slightly below the sector median of 33%.

With that said, there are two other things worth noting.

- The current yield of 3.4% is well above the long-term median. Due to faster growth, the bank used to yield less than 2.0% more often than not before the pandemic.

- The bank has not cut its dividend during the Great Financial Crisis.

With that said, the bank just reported its earnings in a rather challenging environment.

OZK Earnings – A Closer Look

In its fourth quarter, Bank OZK reported $360 million in revenue. This was 22.8% higher compared to the prior-year quarter and $17 million higher than expected. This was one of the reasons why the bank beat GAAP EPS estimates by $0.03, as EPS came in at $1.34.

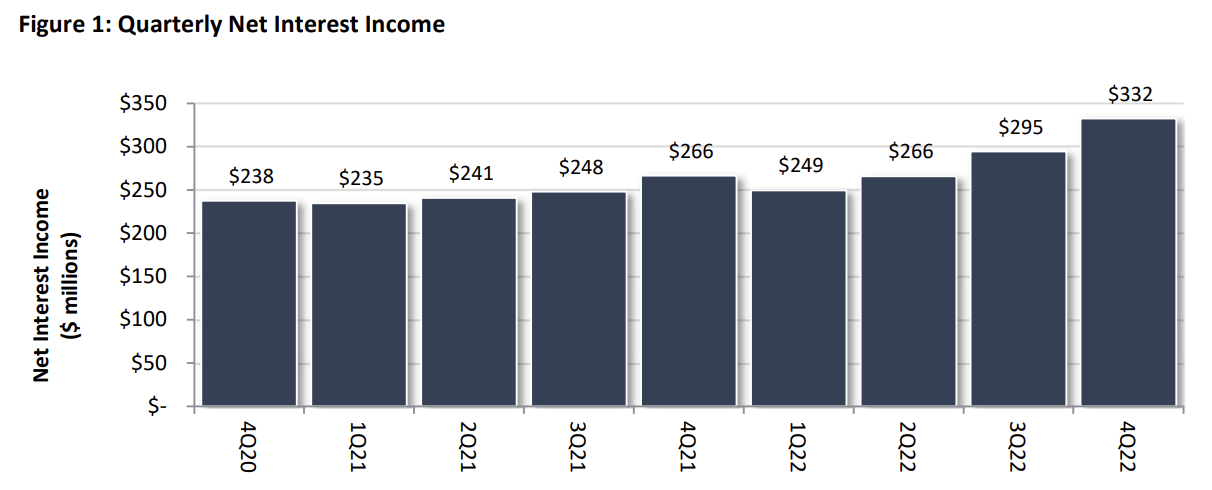

One of the most spectacular things to report is the surge in net interest income.

Net Interest Income

Net interest income surged by 24.8% on a year-on-year basis. On a sequential basis, it rose by 12.9%. The company’s core spread, which is the difference between the yield on non-purchased loans and the cost of interest-bearing deposits, increased to 6.05%, which contributed to a net interest margin of 5.5%.

Bank OZK

As great as this might be, this is not sustainable and is a result of high inflation and high rates. The economy was still moderately strong, inflation was high, and high rates further fueled interest income. Even Bank of America (BAC) said that investors should adjust their expectations in case they expect this to continue:

The pace of loan growth Bank of America has enjoyed isn’t sustainable given the current state of the economy, Chief Executive Officer Brian Moynihan said on the call.

“People are reading the same headlines we’re reading” about a potential recession, he said.

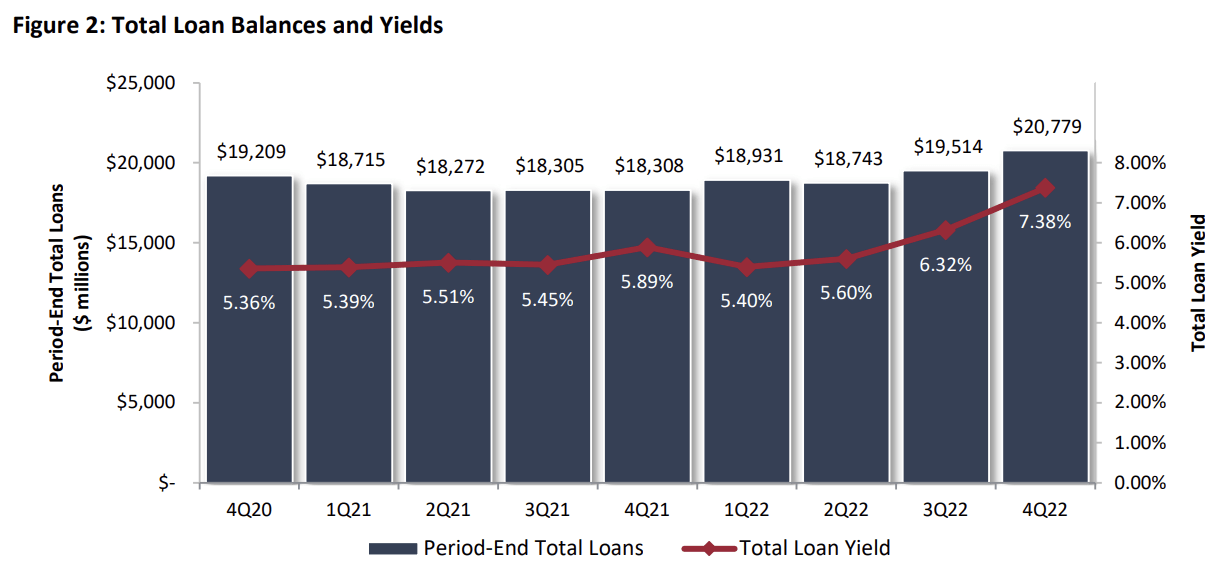

Loan Growth

Moreover, as loans are the biggest part of the bank’s earning assets, the bank benefited from higher loan growth. The average balance of loans in the fourth quarter was $20.1 billion, an increase from $18.0 billion in the prior-year quarter.

The total loan yield rose to 7.4%.

Bank OZK

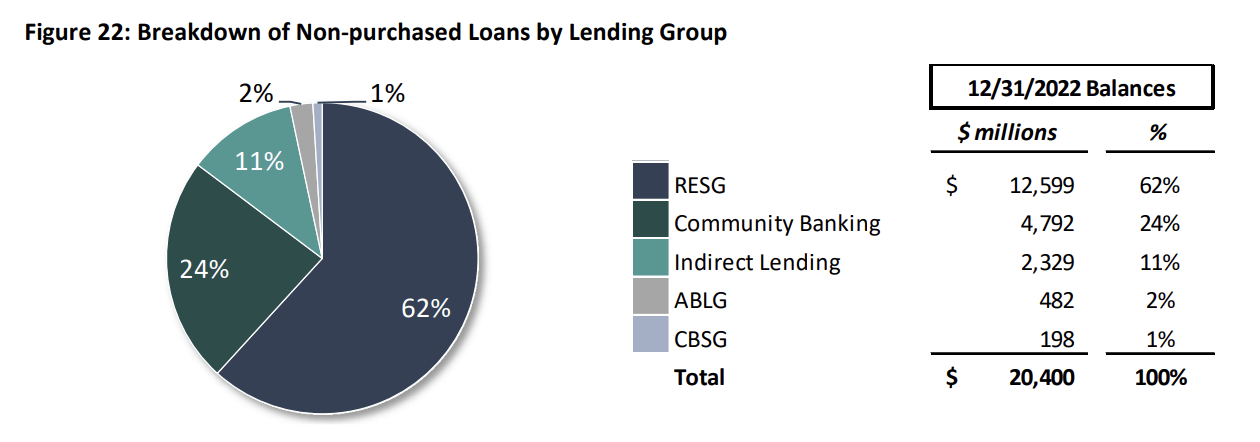

The company’s RESG – Real Estate Specialties Group – accounted for 62% of the funded balance of non-purchased loans. Non-purchased loans account for 98.1% of total loans.

Historically, a significant portion of our non-purchased loan portfolio growth has been attributable to our Real Estate Specialties Group., which focuses primarily on acquisition, development and construction lending of commercial real estate.

Bank OZK

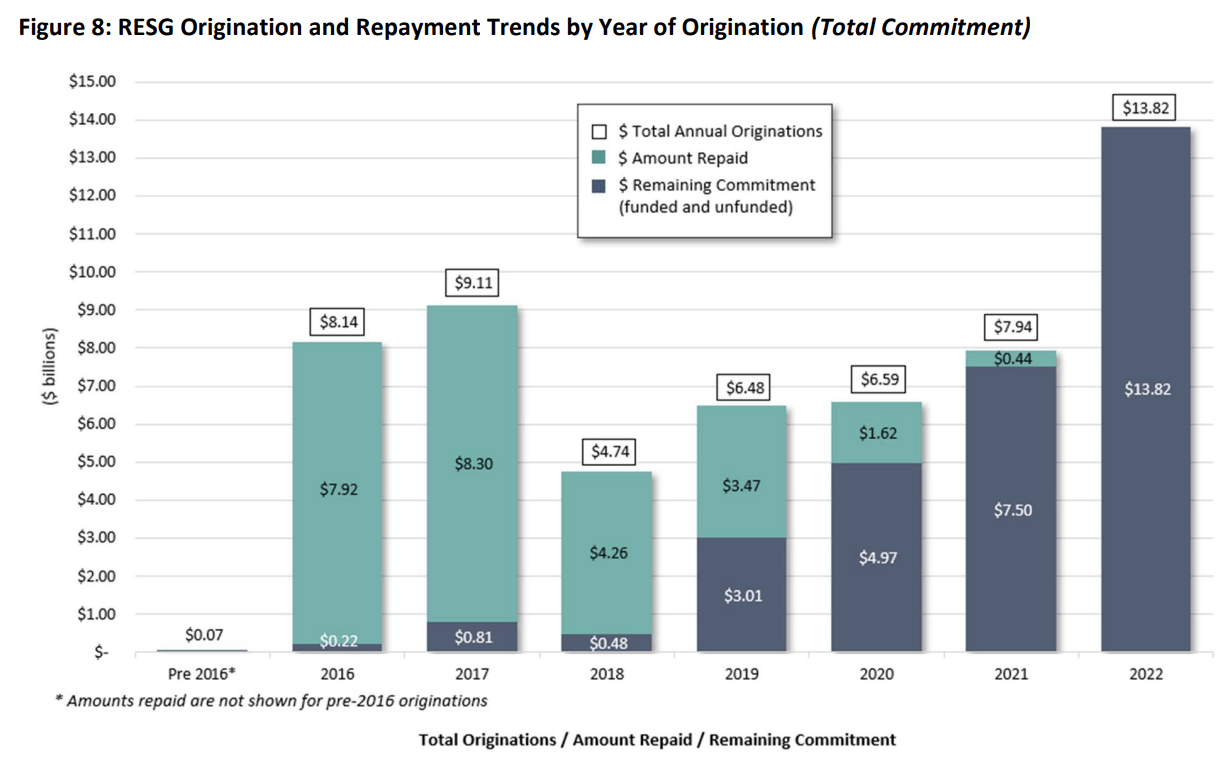

The RESG balance increased by 9.8% as new funding more than offset repayments. Loan originations in 2022 hit $13.8 billion, the biggest increase ever. Given the typical lag between RESG originations and the funding of such loans, the spike in originations should lead to meaningful funded loan growth in both 2023 and 2024.

Bank OZK

Concerning the aforementioned loan growth, Bank OZK is seeing some headwinds (normalization), which is similar to what other banks like Bank of America said.

Because of the current uncertain macroeconomic environment, including the impact of recent increases in interest rates, RESG origination volume for the full year of 2023 is expected to be back in or around the range achieved during 2020 and 2021. Origination volume may vary significantly from quarter to quarter and may be impacted by interest rates, economic conditions, competition or other factors.

Purchased loans, which are the remaining loans from acquisitions, accounted for just 1.9% of average total loans. The total balance was $379 million at the end of 4Q22. That’s down from $808 million in 4Q20. The purchased loan yield was 7.2%.

Loan Quality & Capital Ratios

With that said, the company also reported stellar loan quality. That is not a given, as we’re dealing with elevated rates, slowing economic growth, and elevated inflation. These things are not necessarily supportive of loan quality.

The company’s provision/allowance for credit losses was $32.6 million in the fourth quarter. This is up from negative ACL in the fourth quarter of 2021.

The allowance for loan losses was $208.9 million, or 1.01% of total outstanding loans. That is subdued as even Bank of America had an ALL of 1.2%.

According to OZK:

In our selection of macroeconomic scenarios, we remained weighted to the downside as the combined weightings assigned to the Moody’s S4 (Alternative Adverse Downside) and S6 (Stagflation) scenarios exceeded that of the Moody’s Baseline scenario, which had the largest single scenario weighting. Our selection and weightings of these scenarios reflected our assessment of conditions in the U.S. economy, and acknowledged the uncertainty regarding future U.S. economic conditions, including the elevated risk of a recession in the near-term, elevated inflationary pressures, increases in the Fed funds target rate, prospects for shrinking the Federal Reserve balance sheet, the impacts of the ongoing war in Ukraine, supply chain disruptions, global trade and geopolitical matters, the impacts of U.S. fiscal policy actions, uncertainties about the COVID-19 pandemic, and various other factors.

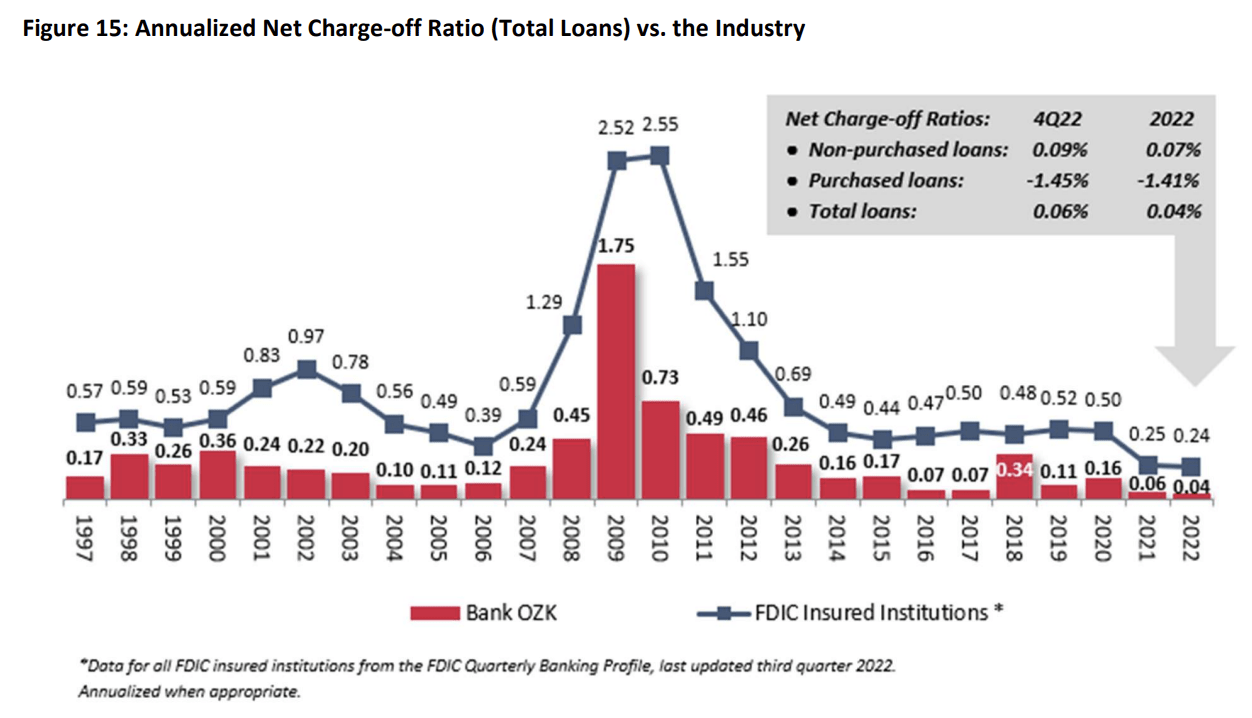

Related to the information above, OZK is known for having low net charge-offs (high loan quality). Net charge-offs in 4Q22 were 0.06% of total loans. On a full-year basis, that number was 0.04%. This is well-below the industry average, which also still enjoys high loan quality – yet not as good as OZK.

Bank OZK

Allow me to quote the company again:

Our portfolio continued to perform very well throughout the COVID-19 pandemic, the Fed’s increasing interest rates, higher rates of inflation, and numerous other sources of macroeconomic, political and geo-political turbulence. We have built our portfolio with the goal that it will perform well in adverse economic conditions, and that discipline has been evident in our results over the past few years, including our net charge-off ratio for total loans, which has recently ranged from an all-time low of 4 bps in the year just ended to 16 bps in 2020.

Based on this context, the company continues to be cautiously optimistic about its future portfolio performance in light of accumulating risks that include a higher Fed funds rate, elevated recession risks, and other uncertainties.

OZK expects that net charge-offs will be up in 2023 versus 2022, yet still well below the industry average.

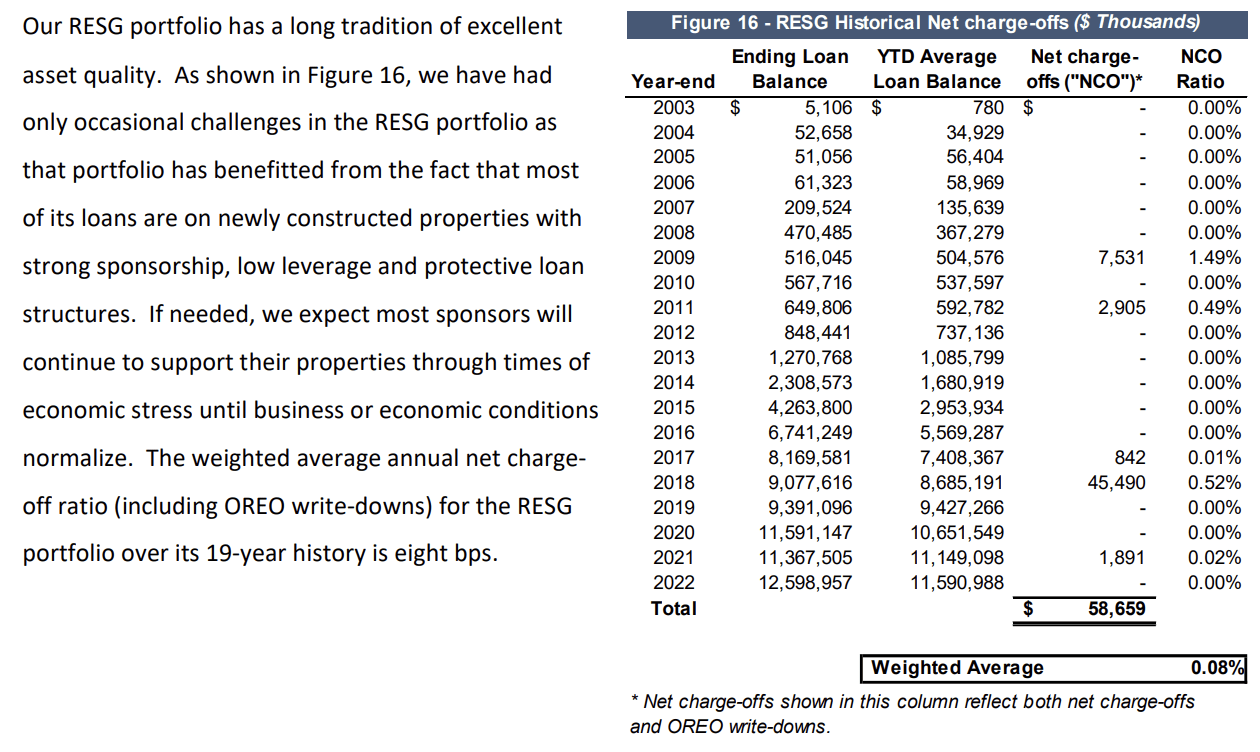

Moreover, as the table below shows, the RESG portfolio continues to enjoy incredible loan quality. The 2022 NCO ratio was 0.00. Even in 2009, that number was just 1.5%. The weighted average is 0.08%, which has been lowered in every single year since 2009.

Bank OZK

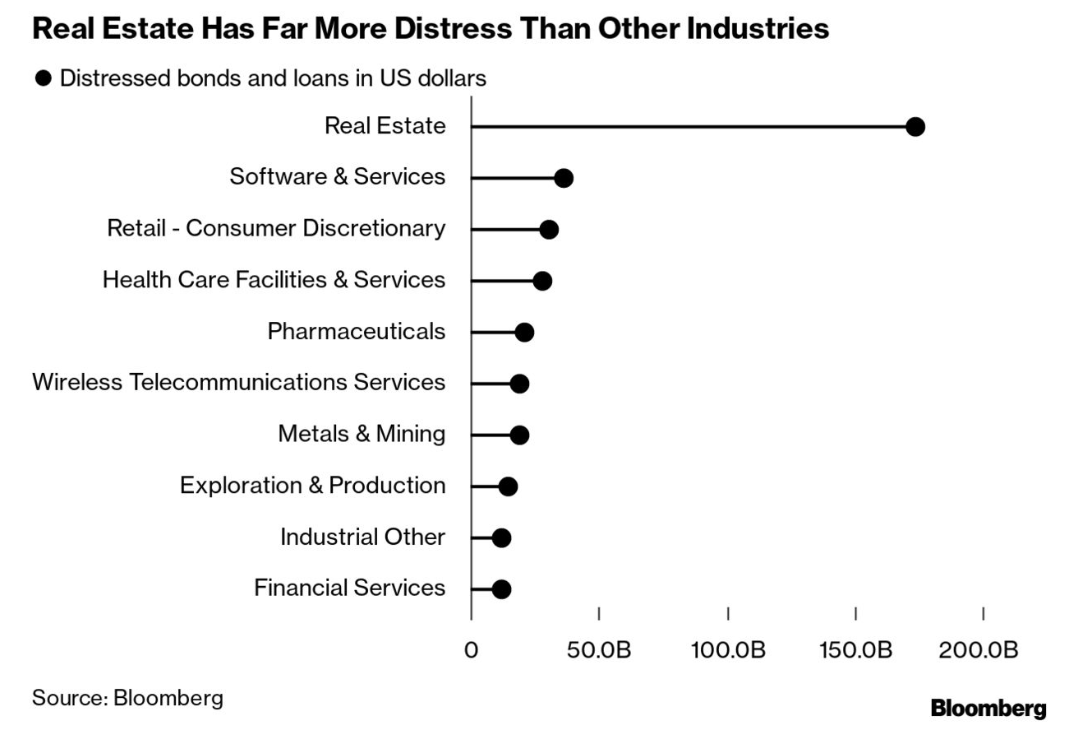

Note that this is not only impressive in general but also because real estate is usually prone to quickly deteriorating debt quality. Currently, this is the case as well.

Bloomberg

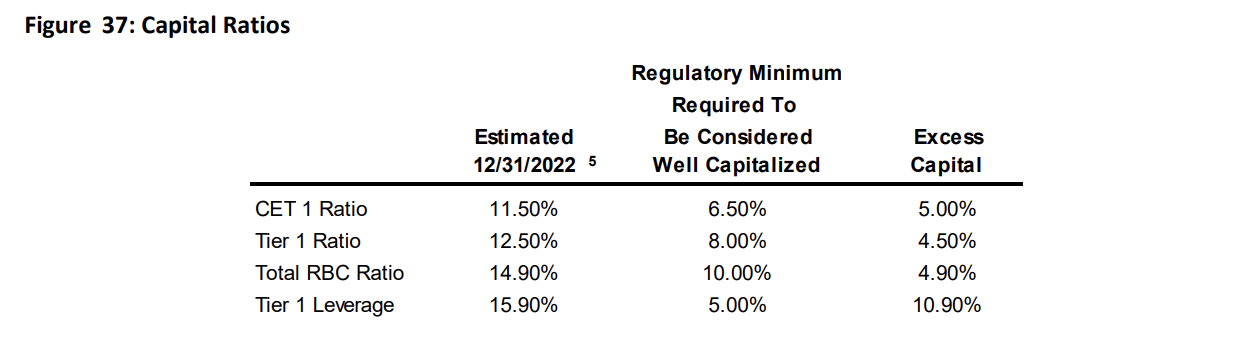

The company’s balance sheet financials were also satisfying. Its CET 1 ratio was 11.50%. The regulatory minimum is 6.5%, which means the company has excess capital.

Bank OZK

Non-Interest Income & Operating Efficiencies

With that said, non-interest income was down 7.2% in the fourth quarter to $27.5 million. This was due to lower gains on the sale of other assets, which more than offset higher gains from investments. Moreover, the company saw slightly lower service charge fees and other minor items.

Non-interest expenses were up 8.1%. Salaries were the biggest contributor as a result of inflation and a higher headcount. The company ended the year with 2,646 full-time employees (to be precise). That is up from 2,485 at the start of the year, adding more than $5 million to salary expenses.

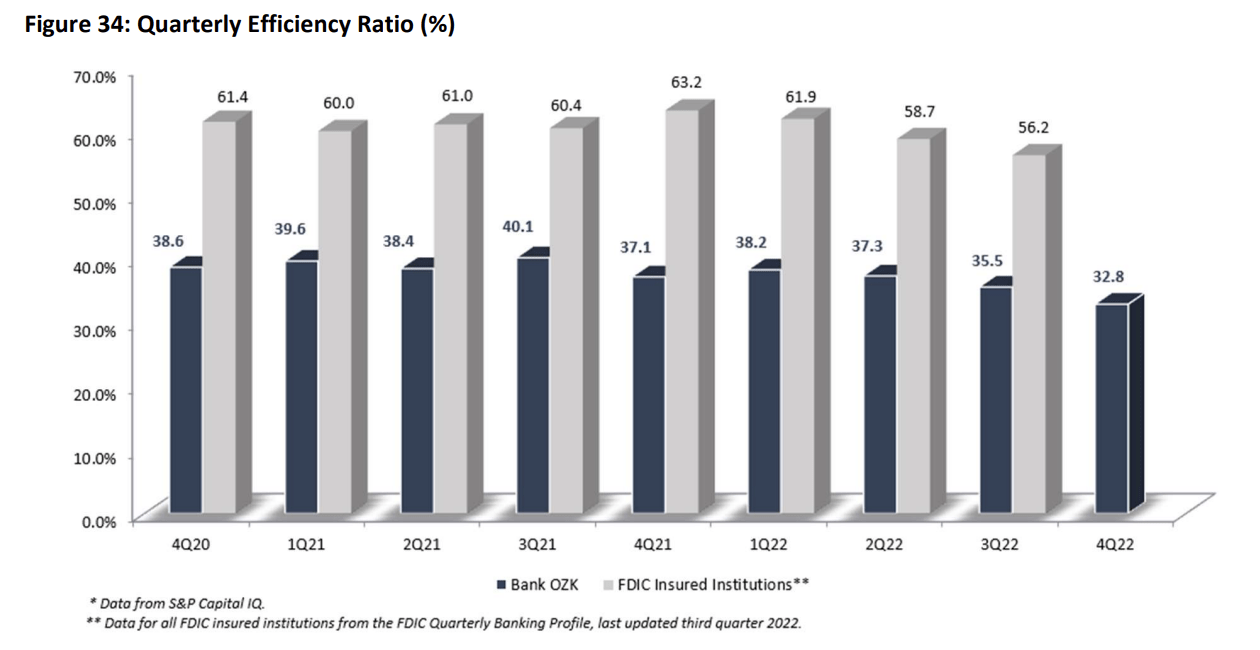

However, given the bigger picture, the efficiency ratio improved to 32.8%. Please note that the lower the ratio, the higher the operating profitability. Generally speaking, a ratio below 50.0% is optimal. Hence, OZK not only beats that number, but it also beats its average peer by a wide margin.

Bank OZK

Now, on to the valuation.

Valuation

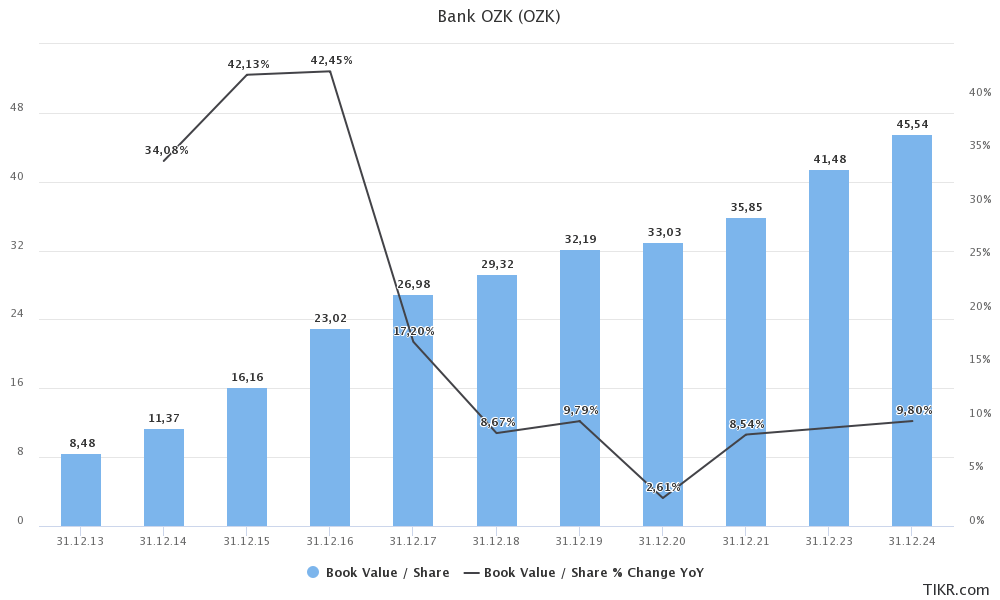

The good news continues. Bank OZK is consistently growing its book value per share. For some reason, 2022 is excluded from the chart below. However, that number is $37.13, which means the uptrend is gradual and strong.

TIKR.com

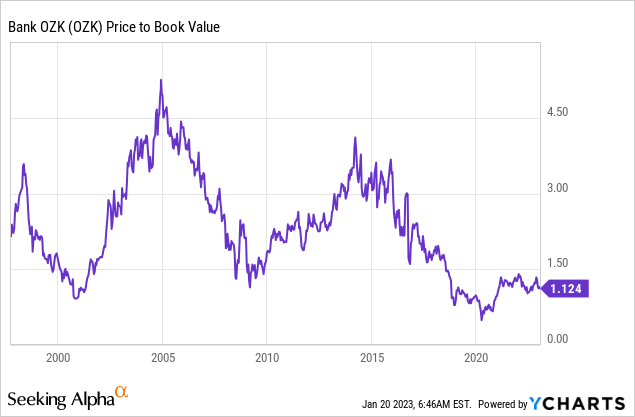

Using the numbers above, we also find that OZK is cheap.

- The bank is trading at 1.08x its 2022 book value.

- Using 2023 estimates, that forward valuation falls to 0.97.

The peer median is 1.25x book, which makes OZK significantly undervalued. I would argue that in a scenario of rebounding growth expectations, the bank should not trade at less than 1.5x book.

The current price target is $48. I do not disagree with that, as analysts often apply median-term economic developments when assessing banks.

However, on a long-term basis, I believe that the stock should not trade anywhere below $60, which I consider fair value.

Takeaway

In this article, we did two things.

- Assessing the company’s qualities as a high-yield dividend growth stock.

- Diving into the qualities that make the company so powerful, using 4Q22 earnings.

I don’t say this quickly, but I’m impressed with this bank. OZK may be small, but it sure is an impressive financial organization.

The company has a decent dividend yield of 3.4%, which falls into the lower-high-yield category. Its dividend growth is very satisfying and consistent. The bank has fantastic loan quality and a track record of doing well, even in the worst recessions.

I believe that the company will continue its impressive dividend growth, especially once economic headwinds fade, which will unlock even more liquidity from provisions and current balances.

I also believe that the OZK ticker will continue to outperform its peers.

If I were to buy more banking exposure anytime soon, OZK would likely make it into my portfolio.

On a side note, my bullish rating on Bank OZK is a long-term rating. Due to economic challenges, we might see a bit more downside before OZK stock moves higher. Please bear that in mind. Or even better, if you like the stock, use weakness in your favor.

(Dis)agree? Let me know in the comments!

Be the first to comment