JHVEPhoto

Bank of Nova Scotia (NYSE:BNS) has had a good start to 2023, with the stock up +14% YTD. This decidedly bullish trend is sustainable considering the Canadian bank’s strong EPS growth in recent years, consistent dividends, and attractive valuation.

BNS’ high dividend yield of 5.65% as of writing is also attractive considering BNS has stable earnings with a safe payout ratio of 45.67%, a solid balance sheet and is positioned to continue growing its EPS. BNS could potentially reward investors who take advantage of current prices or future dips.

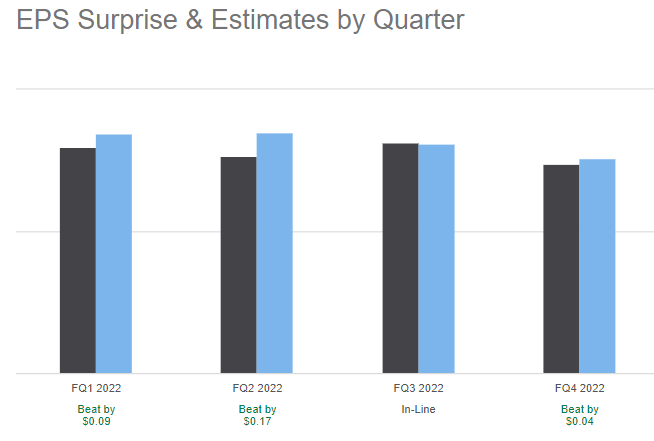

BNS has been performing above analysts’ expectations all through 2022 as far as EPS is concerned, with quarterly EPS for Q4 (financial year ending October 2022) coming in at $1.52 vs consensus of $1.38. The Canadian bank, which operates in Peru, Chile, Mexico and Columbia, posted annual EPS of $6.26 on total interest income of $24.63 billion in 2022.

Seeking Alpha

Analysts expect BNS’ revenues to come in at $25.53 billion in 2023 and $26.97 billion in 2024, with EPS growing to $6.25 and $6.45 respectively. These forecasts translate to a forward PE of 8.67x for 2023 and 8.40x for 2024, pointing to potential undervaluation given how BNS is well positioned from a fundamental analysis point of view.

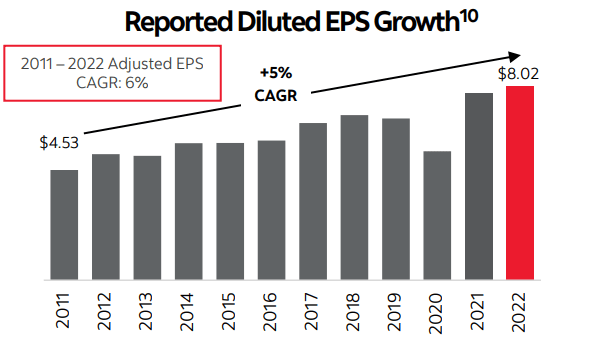

Moreover, BNS has built trust and confidence in the investor community thanks to its historical financial performance in the last 10 years. It has grown EPS at a CAGR of +5% between 2012 and 2022, as per its latest investor fact sheet. Strong EPS growth in the last decade has enabled BNS to increase its annual dividend by almost 100% to $4.06 in 2022 from $2.05 in 2012.

BNS investor factsheet

Better times ahead

BNS is up close to 20% since trading near recent lows of around $47 in October 2022. It still has room to keep gaining value in my opinion as the present multiples still underrepresents the bank’s prospects.

The forward P/E ratios for 2023 (8.67x) and 2024 (8.40) are lower than the bank’s 5 year average P/E of more than 10X. The Seeking Alpha valuation screener assigns it a grade of A (minus), which suggests its undervalued.

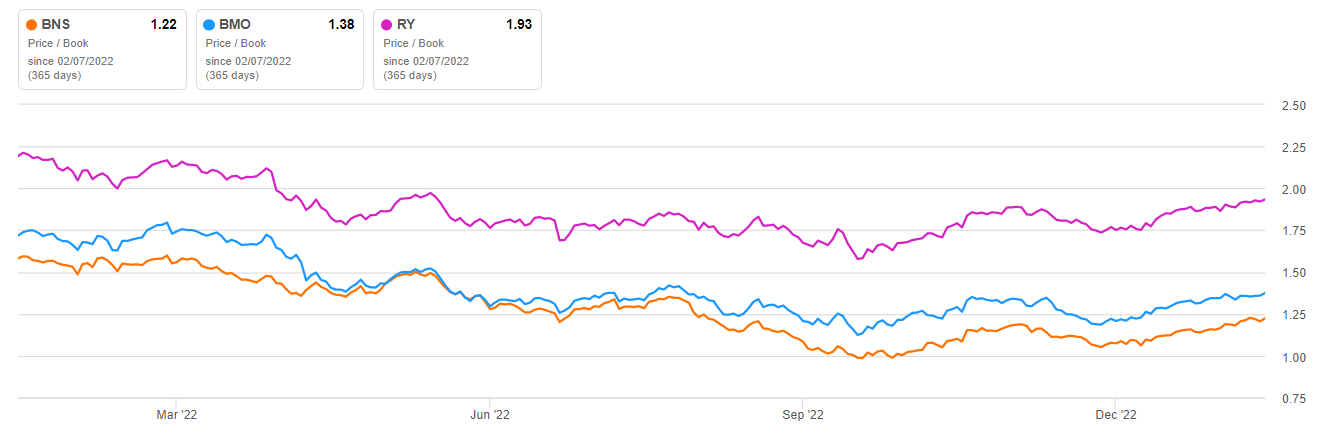

When compared with Canadian peers such as Bank of Montreal (BMO) and Royal Bank of Canada (RY), BNS has the lowest forward P/E ratio of 8.67x. BMO has a forward P/E of 10.07x while RY’s is 11.66x. BNS’ undervaluation relative to Canadian peers is also apparent when looking at price/book ratio, which is a good valuation metric for banks given their assets are usually valued at the prevailing market rates. As the chart below shows, BNS has a p/b of 1.22x vs BMO’s 1.38x and RY’s 1.83x.

BNS 1 year price to book ratio vs Canadian peers (Seeking Alpha)

Besides its relative undervaluation, BNS has the highest forward dividend yield of 5.49% compared with BMO’s 4.26% and RY’s 3.83%. The higher yield (against the backdrop of stable dividends) and lower valuation make it the better long-term investment and provides downside protection by creating demand for its stock in the event of a pullback.

Looking into the future, one of the trends that may favorably impact BNS’ earnings in 2023 is potentially lower credit loss provisions. The Canadian banking giant increased provisions in 2022 amid interest rate hikes. It had provision for credit losses of C$529M in Q4 2022, a significant increase from C$412M in Q3 and from C$168M in Q4 2021. With interest rates expected to come lower some time in 2023 amid slowing inflation, BNS could lower its credit provisions, boosting earnings.

Lower interest rates could also lead to lower cost of funding for BNS, increasing its margins. Cost of funding is one of the headwinds that BNS’ management is currently keeping a close eye on. “The cost of that funding has increased significantly. And so that is also going to be a headwind in 2023. So, as I think about 2023 earnings, I am very cautious on the outlook for 2023.” said Scott Thomson, President and CEO, at the January 9th Canadian Bank CEO Conference with RBC Capital Markets’ Darko Mihelic.

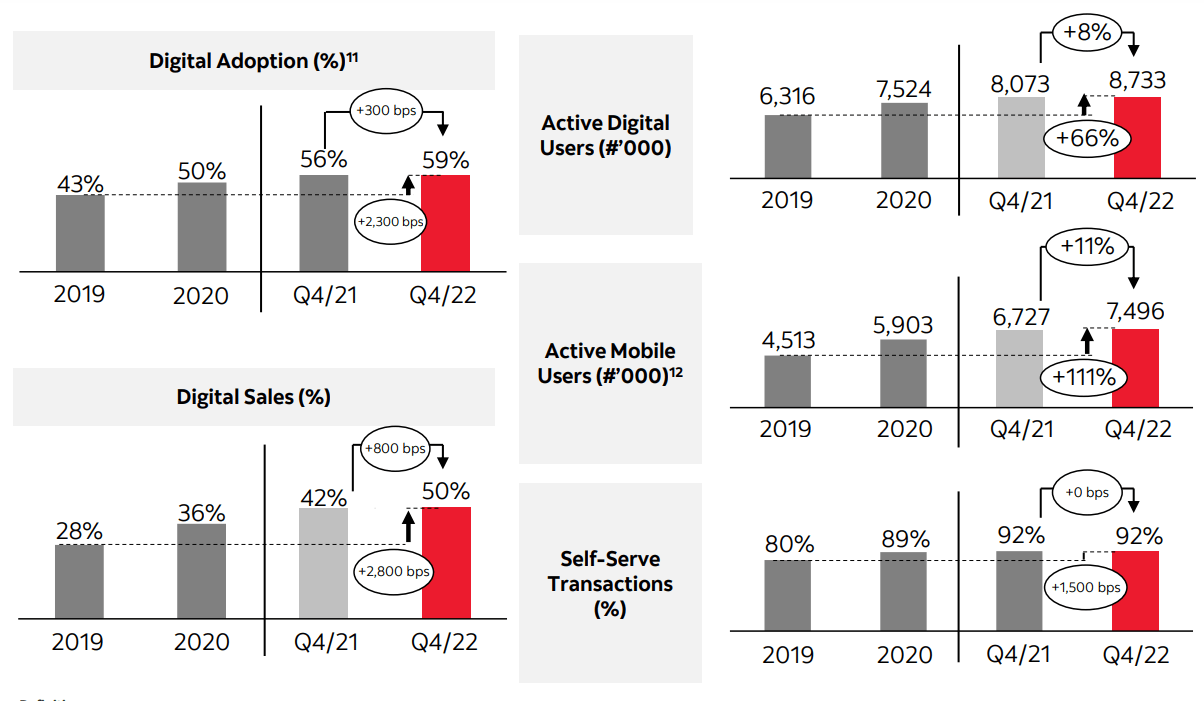

BNS’ investments in its digital capabilities could enable it to solidify its already strong regional presence in the Americas while keeping its costs under control. BNS’ digital adoption in Canada, Peru, Mexico, Chile and Columbia has been robustly growing, reaching 8.73 million active digital users in Q4 2022 vs 6.31 million in 2021, as per its investor factsheet.

BNS Investor factsheet

The coming of lower interest rates and BNS’ continued investments in digital capabilities could help the lender improve efficiencies and grow its margins going forward. BNS’ current net income margin of 33.27% is significantly higher than the sector median of 27.53%, underlining its higher efficiencies and profitability relative to the broader financial sector. This means it is positioned to outperform in terms of profitability once banking industry conditions get more conducive for net interest margin expansion.

A combination of income and value

If you are not looking for a quick return, BNS is a good investment as it is a high yielding dividend stock that is well positioned to sustain its dividends in coming years. Its current valuation is lower than its 5 year average, despite the fact that the business could reach record revenues and EPS in 2023 and 2024 amid favorable operating tailwinds like declining interest rates. BNS is a good combination of income and value at current prices and bullish investors should take advantage.

Be the first to comment