Krenil Miclat/iStock via Getty Images

Introduction

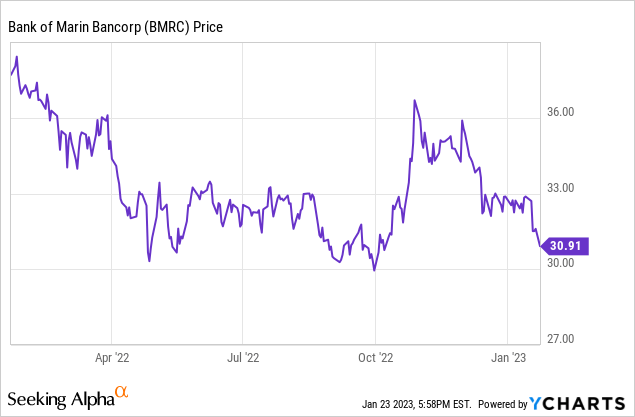

As it has been more than 18 months since I last discussed Bank of Marin (NASDAQ:BMRC), an update is long overdue. Back in June 2021 I thought the San Francisco Bay area bank was a bit too expensive and now, more than six quarters later, the share price has just been treading water as the bank is trading at pretty much the same level.

A satisfying last quarter despite a lower than expected net interest income increase

I was mainly interested in seeing how the higher interest rates are having an impact on the bank’s net interest income but unfortunately the net interest income increase was a bit underwhelming. The bank reported a total interest income of $34.2M (which is a 2% increase compared to the preceding quarter) but as the interest expenses increased by a few hundred thousand dollar as well, we saw a net interest income increase of just 1%.

Bank of Marin Investor Relations

That being said, the bank was able to keep its net non-interest expenses pretty stable. In fact, those non-interest expenses decreased by approximately $0.2M thanks to lower salaries. And as the bank didn’t have to record any loan loss provisions, its net income in the fourth quarter came in at $12.9M, which is an increase of just over 5% compared to the preceding quarter. That’s mainly thanks to the slightly higher net interest income but also due to the lack of loan loss provisions (which had a negative impact of just over $0.4M during the final quarter). The EPS for the quarter came in at $0.81 and this pushed the full-year EPS to $2.93 per share.

This means the stock is currently trading at just around 10 times earnings and perhaps even below that ratio given the relatively strong final quarter of the year which – despite a slower net interest income increase than I had anticipated – was pretty decent.

The bank announced a quarterly dividend of $0.25 which means the payout ratio is just over 30% on a full-year basis. The dividend yield of approximately 3.3% is interesting but perhaps a bit too low to make Bank of Marin a pure dividend pick.

The book value is increasing again

Paying a multiple based on the earnings is one element of the equation here. It is also important to have a look at the book value of the bank to see if a certain share price is attractive.

I think Bank of Marin’s dividend payout ratio is pretty attractive as it basically means the bank is able to add about $2/share to its book value per share. This additional equity can help to either make an existing balance sheet more attractive or even expand the balance sheet if a bank is fine with a certain specified equity ratio.

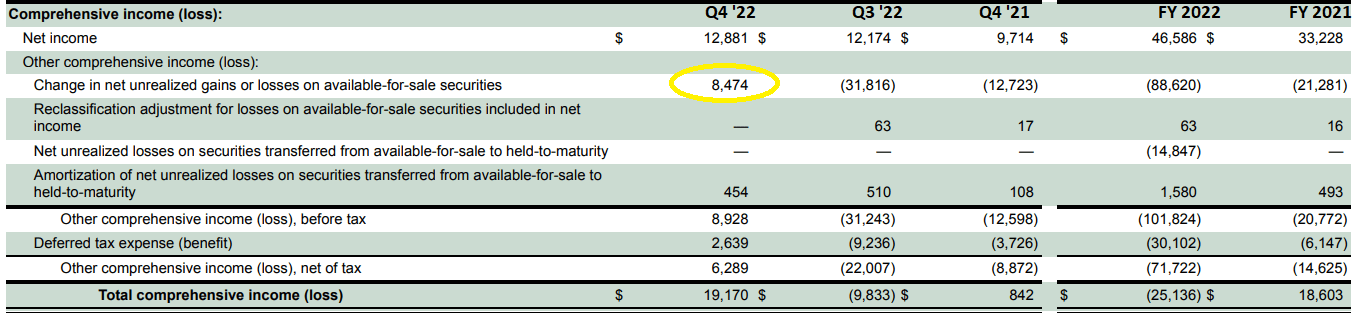

Most banks have seen a rather sizeable impact of the higher interest rates in the first three quarters of the year. Banks with securities classified as “available for sale” need to mark those assets to market and increasing interest rates obviously resulted in lower values for those securities. However, the worst seems to be behind us and bond markets and fixed income securities markets seem to have stabilized. But according to the bank’s comprehensive income statement, not only did the bank no longer have to record an unrealized loss on those securities, it was actually able to book an unrealized gain in the final quarter of the year.

Bank of Marin Investor Relations

Not only is this a massive improvement vs. the $32M loss in Q3 and the $97M impact in the first nine months of the year, this has been a tremendous help to boost the book value per share. Not only is the bank retaining about $9M in earnings (the net income minus dividends), it also was able to add the $8.5M in unrealized gains on the securities portfolio back to the equation.

While the total equity value on the balance sheet is still down compared to the end of 2021, we see a substantial increase in the final quarter of this year, and even if no additional gains will be occurring in the portfolio of securities available for sale, Bank of Marin should be able to continue to increase its book value (and tangible book value) per share by about $0.50 per quarter.

Bank of Marin Investor Relations

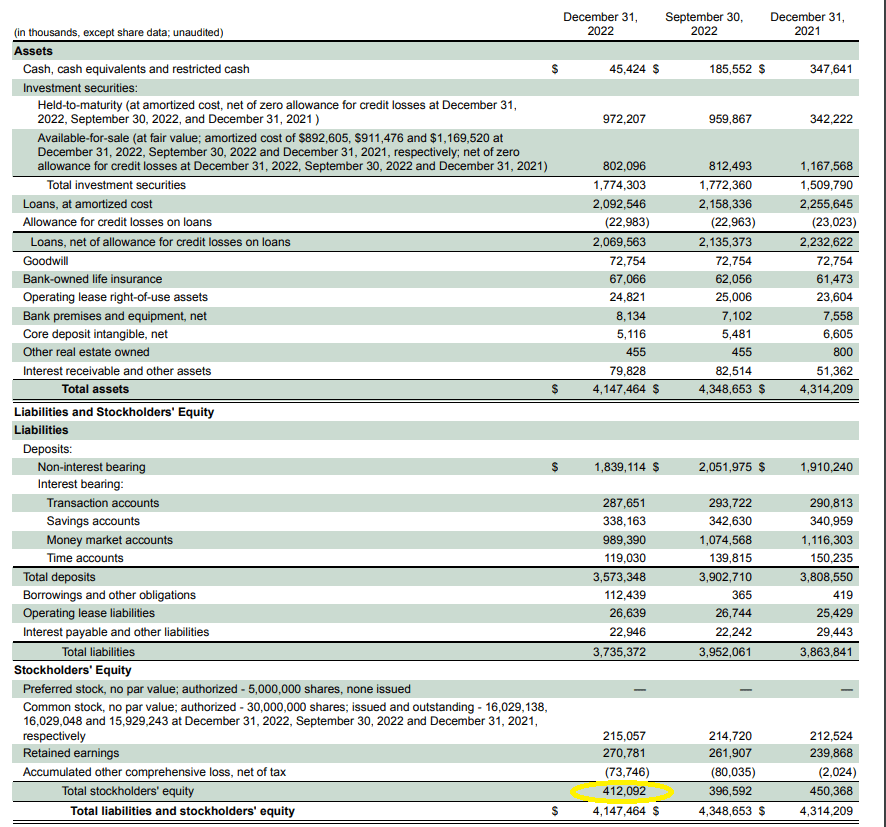

As of the end of December, BMRC’s book value was $412M resulting in a book value per share of $25.70. However, if I would deduct the $72.8M in goodwill on the balance sheet, about $4.50 per share would have to be deducted from that calculation and the tangible book value per share is likely approximately $21.20.

Investment thesis

Not the earnings report but recouping some of the unrealized losses on the securities portfolio is the most important takeaway for me from Bank of Marin’s earning’s report. I will have a closer look at the annual report as soon as it will be filed (mainly to have a more detailed look at the loan book) but I like what I see. While Bank of Marin does have exposure to $450M in office loans, the average LTV ratio of those loans is just under 44% so although I acknowledge the office markets in the Bay area are a bit shaky, Bank of Marin should be fine.

Bank of Marin is pretty attractive based on an earnings multiple and even the current premium of 40% to the tangible book value is palatable.

Be the first to comment