carlosgaw/E+ via Getty Images

Danone S.A. (OTCQX:DANOY) is a Paris, France-based consumer staples company perhaps best known for its eponymous bottled water brand. Although the company still operates the legacy water business, which has recently performed quite well, it has multiple other brands that enjoy #1 or #2 market share in their respective product categories.

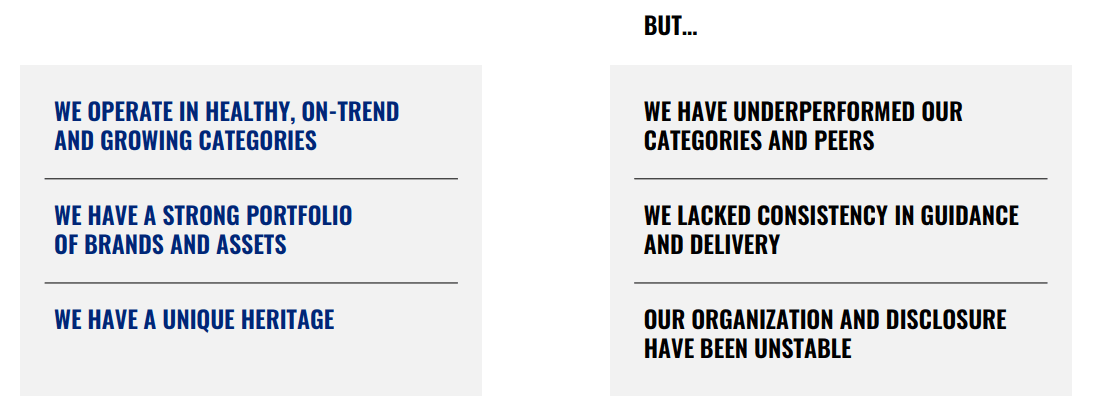

DANOY has severely underperformed peers in recent years for a number of reasons including under-investment in its brands, di-worse-ification into too many products that ended up cannibalizing each other’s sales, high input cost inflation, and economic weakness in Europe.

In the Spring of 2022, management came out with a “mea culpa,” admitting that they had been “playing not to lose” rather than “playing to win” and vowing to overhaul the company as necessary to revive growth with a plan called “Renew Danone.” That included a shakeup of the board of directors, which is now 80% independent and primarily made up of CEOs or former CEOs of other consumer products companies.

DANOY currently offers a dividend yield (based on my estimate of normalized currency exchange between the Euro and the USD) of about 4%, and management is committed to a stable or growing dividend payout over time.

At this point, DANOY has a few catalysts that should support further growth in the years ahead:

- (Eventual) recovery of its primary region of Europe

- Rebound of sales in China as the country reopens and recovers from COVID-19

- Renewed investment in product innovation and attunement with consumer preferences

- Margin recovery as inflation fades while price hikes remain sticky

While it’s difficult to say whether it’s from management’s efforts or the economic environment or a combination of both, DANOY has already begun showing signs that a recovery is underway.

Let’s dive into DANOY’s renewal plan and then take a look at how this plan has been working as of Q3 2022.

“Renew Danone”

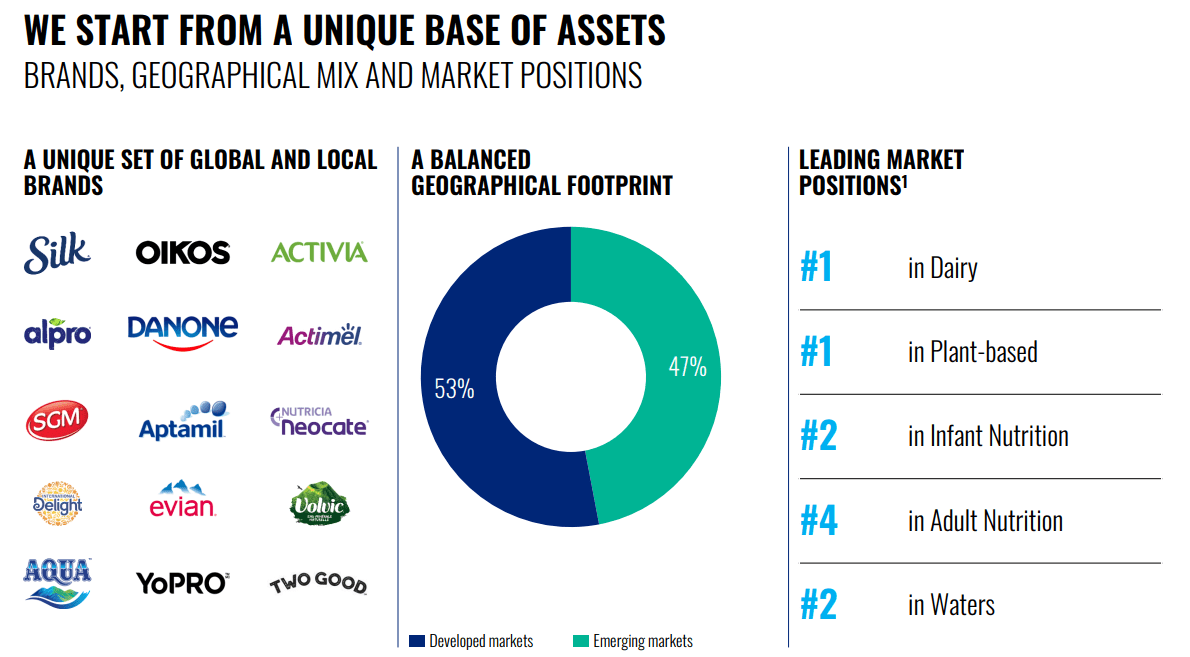

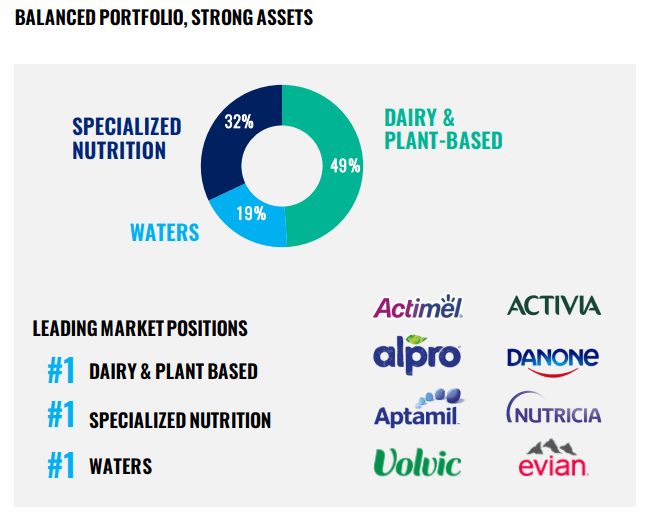

It’s important to start by noting that DANOY has some pretty strong brand names in its portfolio of consumer staples. In particular, the company holds #1 market share positions in both the packaged/bottled dairy and packaged/bottled plant-based milk categories.

Danone March 2022 Presentation

Yogurt, dairy creamers, dairy-based nutrition drinks, plant milks, and plant-based creamers are some of the product types they have in these categories. Together, these products make up about half of DANOY’s sales worldwide.

Another strong category of brands for DANOY is “specialized nutrition,” which includes both infant formula and some nutritional drinks designed for older adults. These make up about 1/3rd of DANOY’s sales.

Finally, there’s the legacy bottled water business that continues to perform well, generating nearly 1/5th of sales.

Danone March 2022 Presentation

DANOY’s sales are split almost evenly between developed markets in Europe and North America and emerging markets in Asia, the Middle East, and Africa, with the slight edge toward developed markets.

The company enjoys product sales in dozens of countries around the world, which offers the benefit of exposure to growing markets but also the potential downside of currency fluctuations. Sometimes foreign exchange is a net benefit, other times a net drawback.

Danone March 2022 Presentation

It can also distort the company’s performance results, if not accounted for. To give a pertinent example, DANOY’s sales growth in Turkey looks incredible… until you realize the country is suffering from hyperinflation right now. Forex headwinds from exchanging the Turkish Lira to Euros (and then to USD for American investors like me) offsets all or most of that purported sales growth.

So, what’s the problem with DANOY, then?

Basically, the company has rested on its laurels the last few years and allowed sales growth to lag its peers’. By the company’s own admission, DANOY under-invested in its product lines for years. It didn’t keep up with consumer preferences as much as it could have. And it held too many underperforming brands in its portfolio, some of which cannibalized sales from others.

Danone March 2022 Presentation

All the puzzle pieces are in place for a successful consumer staples company with strong pricing power and ability to grow sales and earnings over time, and yet management has not executed on DANOY’s potential.

“Renew Danone” is management’s plan to right the ship by incentivizing employees to achieve better growth, reconstituting the board of directors for better oversight, and reinvesting into its brands to keep their finger on the pulse of consumer preferences.

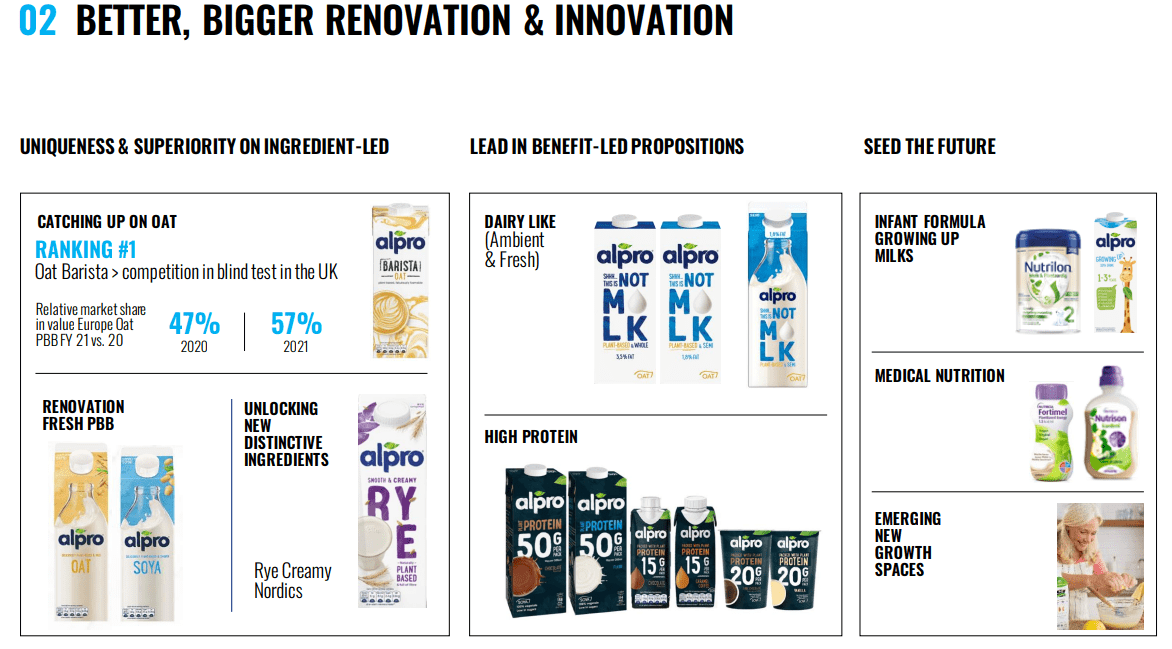

One area where I find particular value in DANOY’s portfolio is the plant-based milks, creamers, yogurts, and ice creams. They already enjoy a #1 market share position with their Silk brand in North America and their Alpro brand in Europe.

Danone March 2022 Presentation

Personally, I am a big fan of Silk’s soy-based creamer as well as So Delicious ice creams. For what it’s worth (admittedly not much), I do not believe competitors or private label brands have been able replicate either’s taste or quality, although Ben & Jerry’s makes a mean non-dairy ice cream as well.

DANOY looks to be in a good position to branch out into new product lines with its existing brands or acquire bolt-on brands, such as its recent acquisition of plant-based butter brand Follow Your Heart.

Danone March 2022 Presentation

Also, with its products specifically designed for older adults, DANOY appears to be well-positioned to benefit from the tailwind of aging demographics around the world.

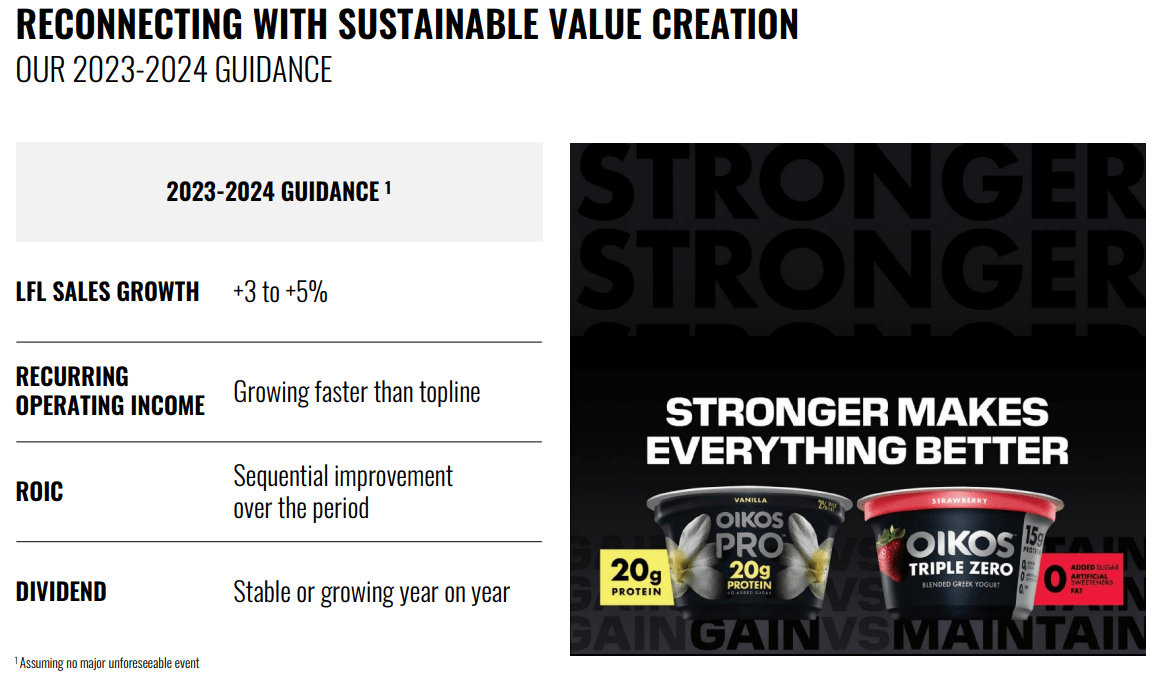

Management has guided for like-for-like (“LFL”) sales growth of 3-5% in 2023-2024, with recurring operating income expected to grow even faster than that.

Danone March 2022 Presentation

Meanwhile, as you can see above, DANOY plans to keep paying a dividend and to raise it year-over-year when it can.

Danone Delivers

How has DANOY been performing since the announcement of its “Renew Danone” effort?

Answer: even better than expected, although some of this may be due to macroeconomic factors such as the ability to hike prices during an inflationary environment.

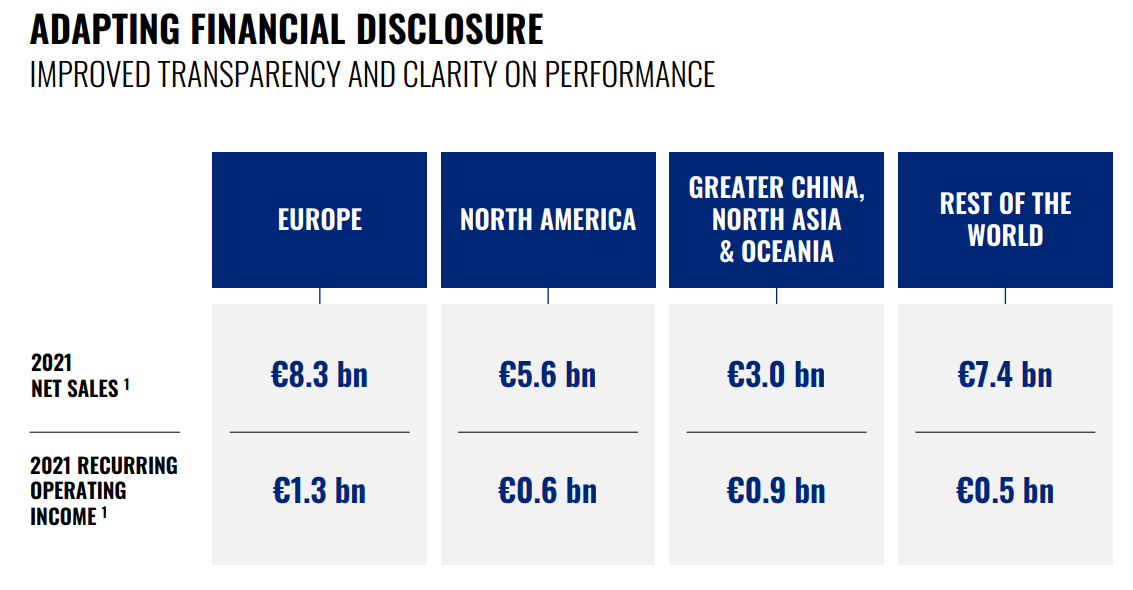

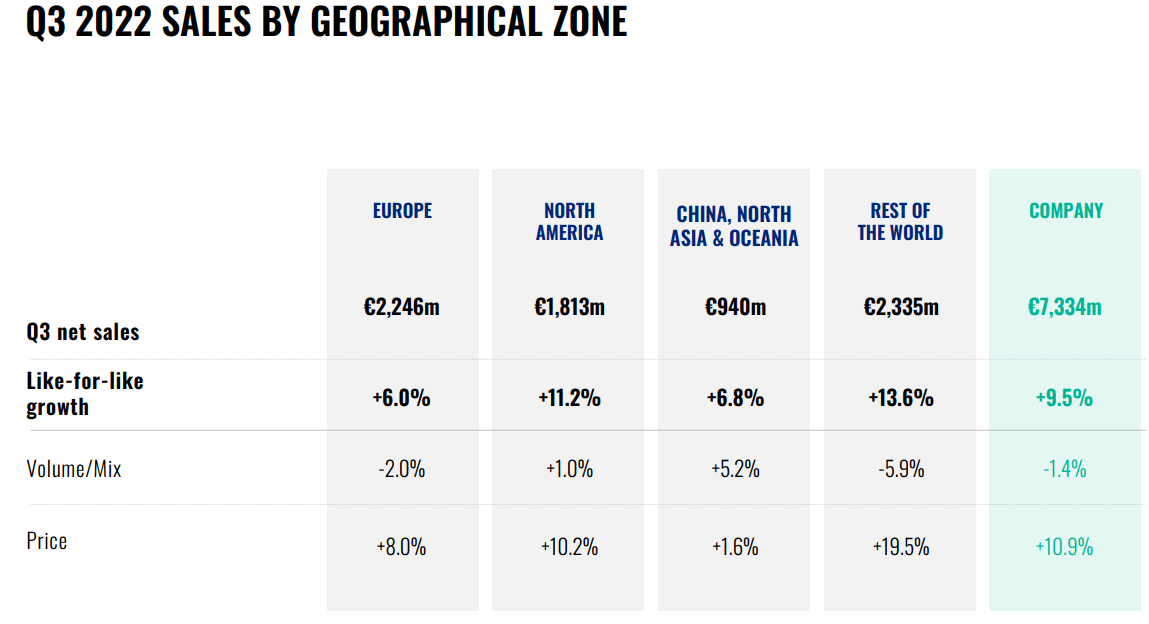

Whereas DANOY showed some slight softness (nothing major) in Europe and Asia (predominantly from China), the company made up for it from strong sales growth in North America and the rest of the world.

Danone October 2022 Presentation

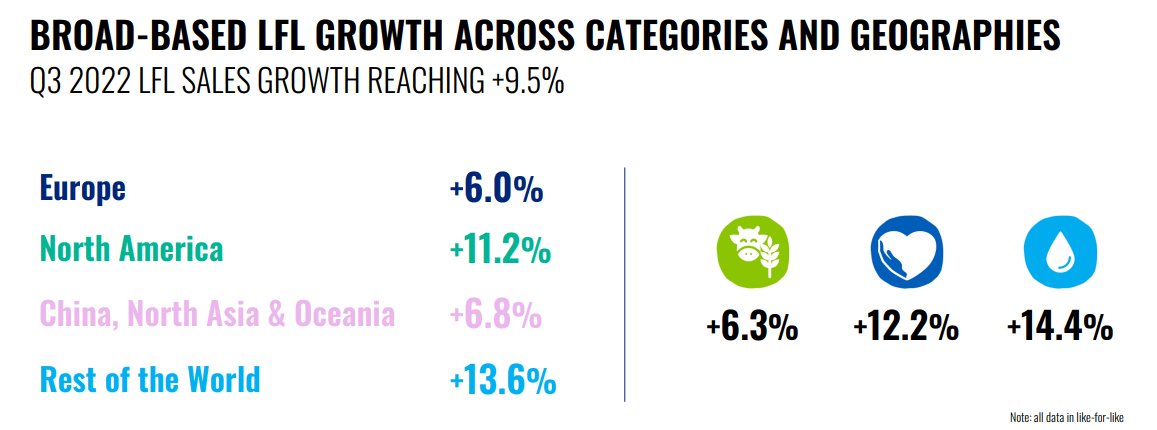

In Q3 2022, DANOY upgraded its 2022 LFL sales growth to 7-8% over 2021’s number. This momentum puts the company in a strong position to either hit the top end of its sales guidance for 2023 or to exceed that number.

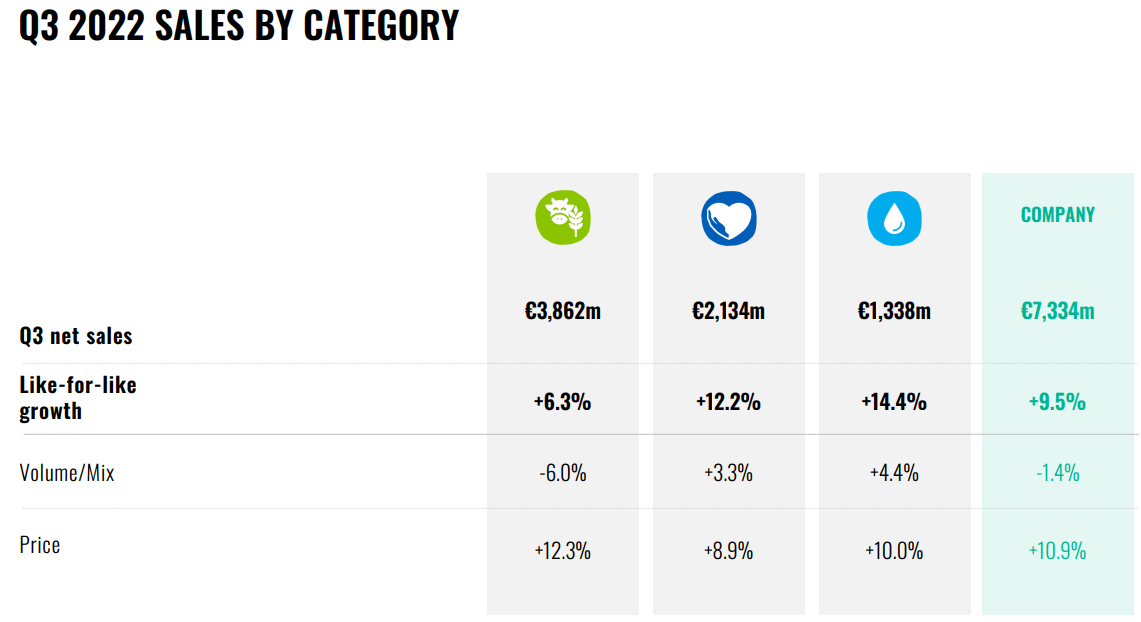

Let’s break out the sales growth by product category. On a company-wide basis, LFL sales grew 9.5% year-over-year, but most of that growth came from specialized nutrition and water.

Danone October 2022 Presentation

Who knew water could be such a driver of sales growth?

Though sales volume declined in the dairy/plant-based category, total sales still grew due to price hikes. Meanwhile, for both specialized nutrition and water, sales rose from both volume of units sold and price increases.

As far as the regional performance goes, as stated above, the bulk of the softness came from Europe, which is suffering from high inflation and economic weakness right now. Much the same could be said about many areas in the “Rest of the World” segment, wherein high inflation has forced consumers to pull back on the volume of products purchased.

Danone October 2022 Presentation

Please note, however, that much of the decline in sales volume in Europe was due to a decline in product sales in Russia. DANOY is in the process of remedying that situation by disposing of its Russian operations by transferring them to a Russian organization.

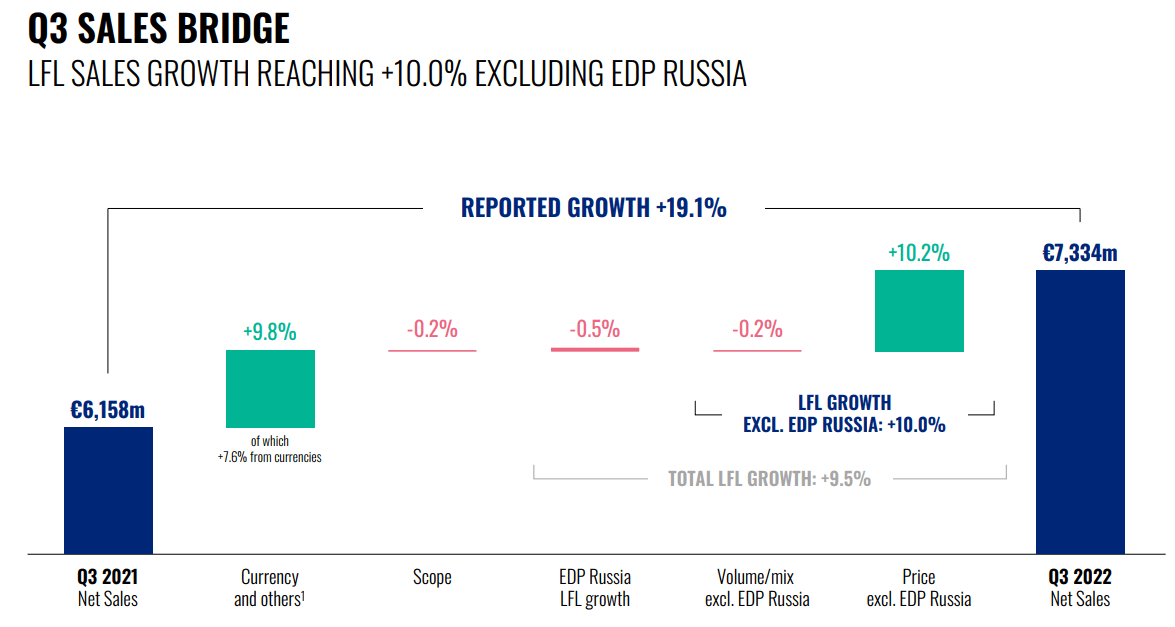

When we look at the sales bridge from Q3 2021 to Q3 2022, we find a few interesting points to note.

First, while currency exchange is a pendulum that helps sometimes, hurts other times, and should generally even out in the long run, forex was actually a net benefit in Q3 2022, boosting net sales by 10%.

Danone October 2022 Presentation

Excluding Russian product sales from the mix, volume declined by a mere 0.2% while prices surged 10.2%.

Rather than the 9.5% reported sales growth number, sales ex-Russia were even higher at 10% YoY.

Bottom Line

Much more could be said about DANOY, and I will certainly continue to monitor the company moving forward. It is an interesting consumer staples company with strong brands and ample opportunities for growth, tapping into the healthy lifestyle, aging demographics, and water shortage trends around the world.

As inflation cools and DANOY’s price hikes stick, I believe the company’s margins should improve substantially, along with other consumer staples companies.

And when the issues in Europe and China are eventually resolved, I believe there will be many opportunities for growth in those markets.

Finally, DANOY’s ~4% dividend yield appears to be an attractive entry point for long-term dividend growth investors such as myself.

All in all, DANOY is an interesting company worthy of further research.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment