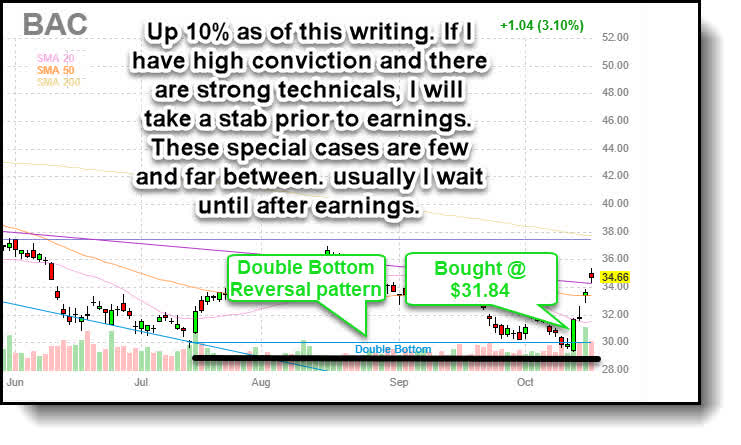

I bought a 1/2 position in Bank of America Corporation (NYSE:BAC) last Friday prior to the earnings announcement for my Seeking Alpha marketplace service, The Winter Warrior Investor. This was due to my due diligence informing me the odds favored the bank beating on the top and bottom lines and experiencing a pop due to it trading near 52 week lows. That is exactly what occurred.

Finviz

Bank of America topped consensus estimates on higher net interest income and strong consumer demand.

“Bank of America stock has risen 2.7% in Monday premarket trading as the company’s Q3 earnings exceeded Wall Street estimates, helped by rising interest rates, strong consumer and global banking units and fairly stable global markets revenue. The bank increased its provision for bad debt as it built reserves in preparation for a weaker economy.

In the company’s Global Markets division, growth in fixed income, currencies and commodities sales and trading revenue helped to offset a decline in equities sales and trading revenue.

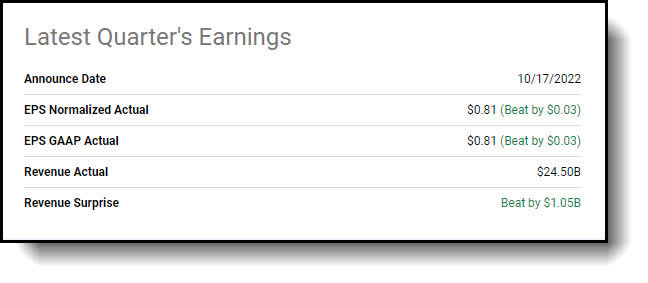

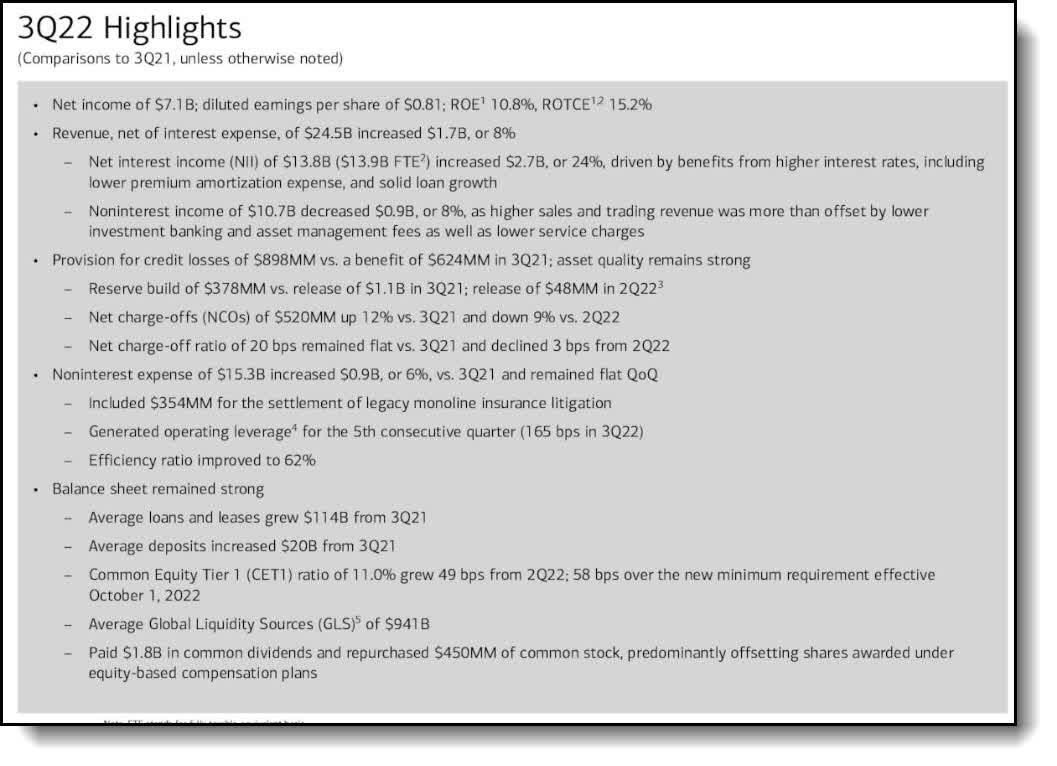

Q2 EPS of $0.81, topped the $0.78 consensus, rising from $0.73 in Q2 and dropping from $0.85 in Q3 2021.

Average loan and lease balances of $1.03T vs. $1.02T in Q2; average deposits of $1.96T vs. $2.01T in the prior quarter.

Q3 net interest income of $13.8B, surpassing the Visible Alpha consensus of $13.5B, rose from $12.4B in Q2 and from $11.1B in the year-ago quarter. Net interest margin of 2.06% widened from 1.86% in the previous quarter and from 1.68% a year ago.

Q3 noninterest income of $10.7B, beating the Visible Alpha consensus of $10.1B, increased from $10.2B in Q2 and $11.7B in Q3 2021.

Provision for credit losses was $898M, including a net reserve build of $378M, compared with $523M, including net reserve release of $48M, in the prior quarter.

Q3 noninterest expense, at $15.3B, was flat with the prior quarter and increased from $14.4B in the year-ago quarter.

Consumer Banking revenue of $9.90B rose from $9.14B in Q2 and $8.84B in Q3 2021; net income of $3.07B vs. $2.89B in the prior quarter and $3.05B in the year-ago quarter.

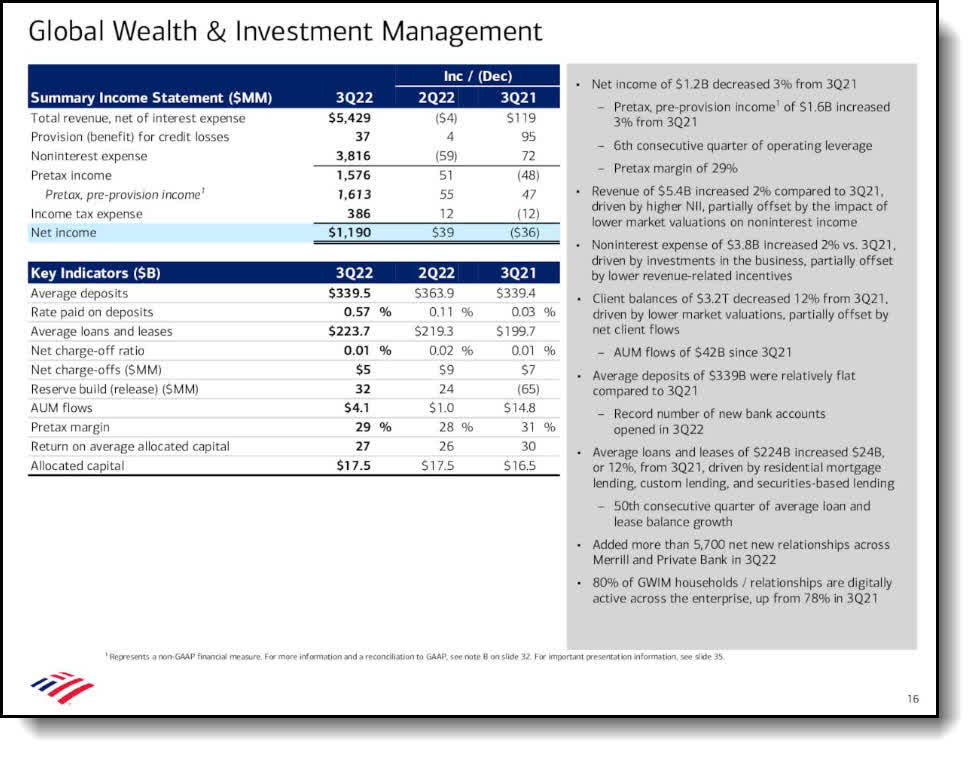

Global Wealth and Investment Management total revenue of $5.43B vs. $5.43B in Q2 and $5.31B in Q3 2021; net income of $1.19B vs. $1.15B in Q2 and $1.23B in Q3 2021.

Global Banking total revenue increased to $5.59B in Q3 2022 from $5.01B in Q2 and from $5.25B in Q3 2021. Net income increased to $2.04B from $1.51B in the prior quarter and fell from $2.55B in the year-ago quarter.

Global Markets total revenue of $4.48B vs. $4.50B in Q2 and $4.52B in the year-ago quarter. FICC sales and trading revenue, excluding net debit valuation adjustments, increased to $2.57B from $2.34B in Q2 and from $2.03B in Q3 2021. For equities, sales and trading revenue (ex-DVA) fell to $1.54B from $1.66B in the prior quarter and from $1.61B in the year-ago quarter. Global Markets net income, excluding net debit valuation adjustments, was $1.08B vs. $898M in the prior quarter and $941M in the year-ago quarter.”

Here is a quote from the earnings call from CEO Brian Moynihan:

“This quarter, Bank of America reported $7.1 billion in net income or $0.81 per diluted share. We grew revenue 8% year-over-year. We delivered our fifth straight quarter of operating leverage. Every business segment delivered operating leverage. This takes us back to our five-year run before the pandemic. The highlights this quarter were also once again marked by good organic customer activity. This was coupled with a significant increase in net interest income.

In addition, the teams adapted well to our new capital requirements. And as a result, our common equity tier 1 ratio or CET1 ratio improved by nearly 50 basis points to 11%, moving 60 basis points above its current minimums.

The decline from prior year reported net income and EPS comparisons reflect a reserve build versus a reserve release last year. At the same time, however, our asset quality remains strong as net charge-offs and several other metrics, in fact, improved from the second quarter 2022. Pretax pre-provision income grew 10% year-over-year. From a return perspective, we produced a 15% ROTCE and a 90 basis point ROA.

Our efficiency ratio this quarter dropped to 62%. Taking out the litigation, it would have been 61%. So even while investing in marketing and people and technology and physical plan, the team continues to drive operational excellence. An easy way to think about this is we currently operate Bank of America with less people than we had in 2015, seven years ago.”

Here is a linkto the earnings presentation. Below are a few of the key slides.

Key Slides

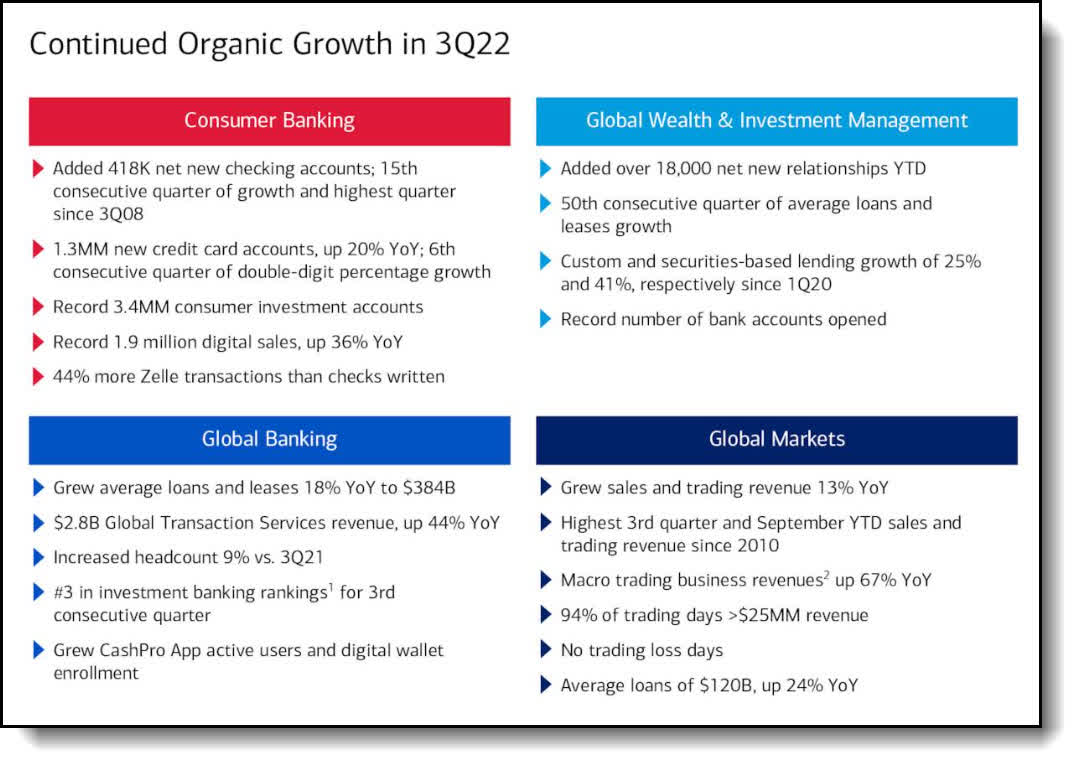

The bank experienced solid organic growth across all geographic and business segments.

BAC.com

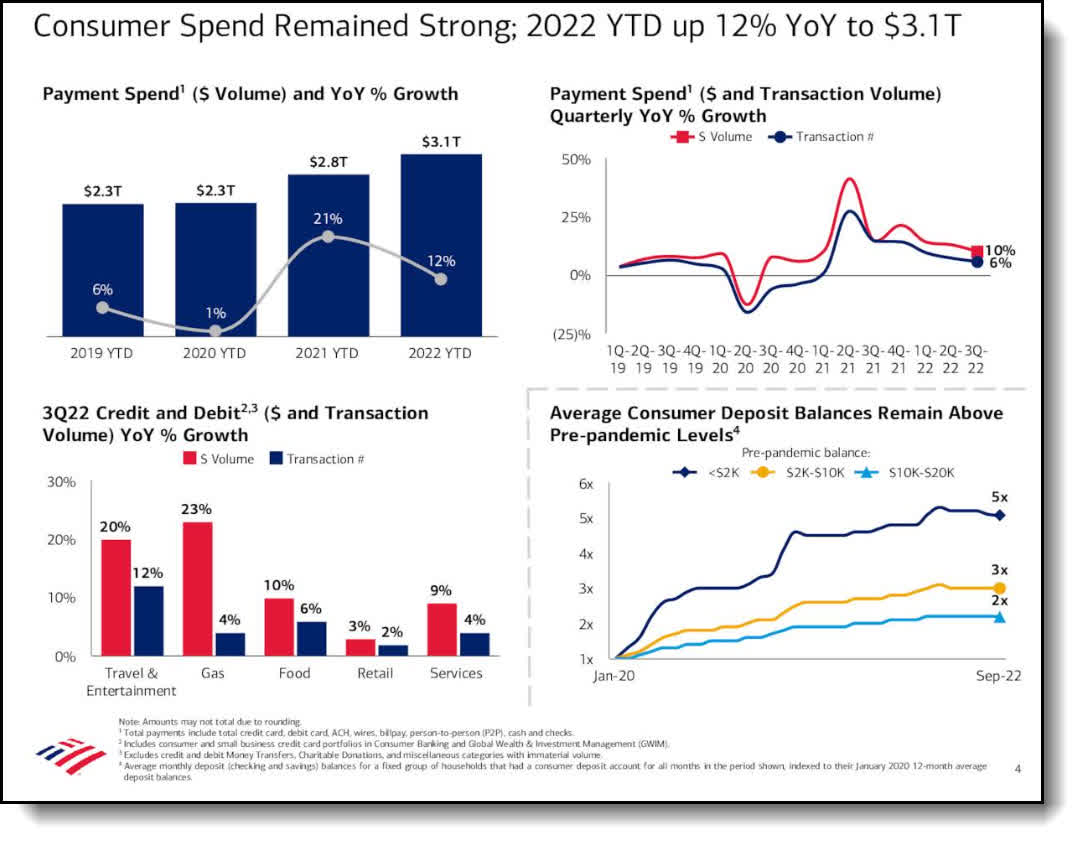

Consumers remain strong, with growth up 12% year-to-date and coming in at $3.1 trillion year-over-year.

BAC.com

Third quarter highlights Per Bank of America.

BAC.com

Major upside opportunity

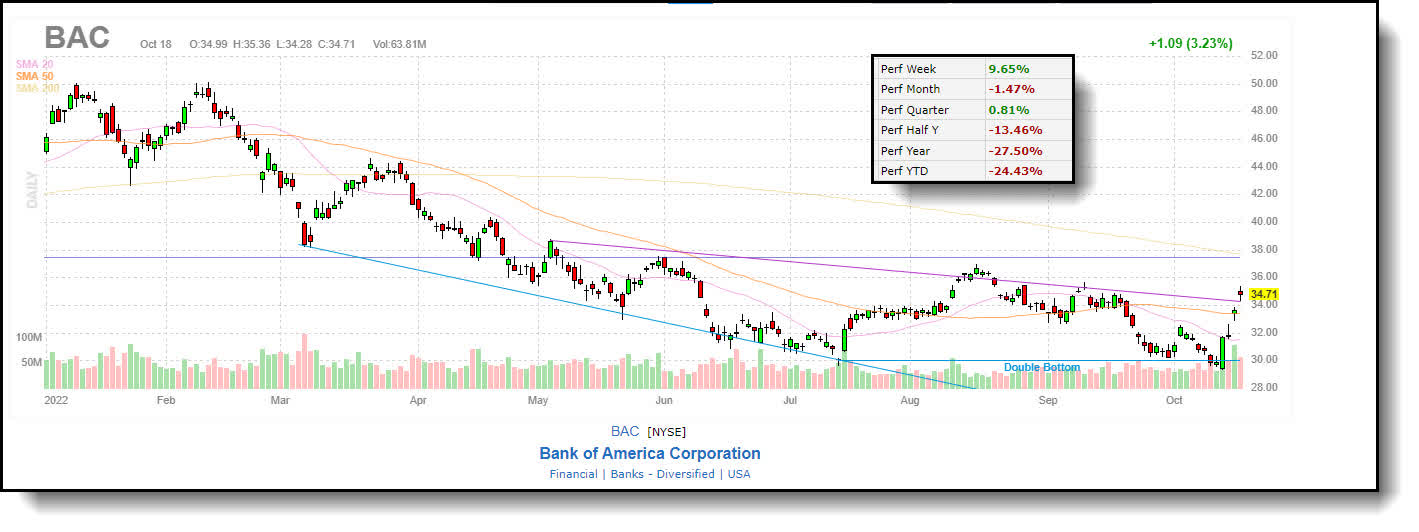

With BAC stock trading near its lows and fulfilling a double-bottom reversal pattern, the stock looks primed for a rally. Bank of America has sold off hard for the past year. The stock is down 27% from its 52 week high and 25% year to date. This has created a substantial buying opportunity for savvy investors, I’d say. It appears an initial breakout is underway. The stock looks technically solid here. Take a look the chart below.

Finviz

The stock bounced off support and is now consolidating prior to the next leg higher, I surmise. Look, all the greatest long-term investors say pretty much the same thing when it comes to buying opportunities, only in differing terminology. Warren Buffett has the most famous buying opportunity quote:

“Be fearful when others are greedy and greedy when other are fearful.”

You get the idea. Our innate instincts encourage us to depart a sinking ship. This survival tactic impacts the way we invest. Often, investors sell out at the exact time they should be doubling down. An unjustified selloff based on macro factors often creates opportunities to buy stock in solid companies with sound prospects. I submit this is the case we have with Bank of America. The stock presents an excellent dividend growth and total return opportunity at present. Let me explain.

Excellent dividend growth and total return opportunity

Seeking Alpha

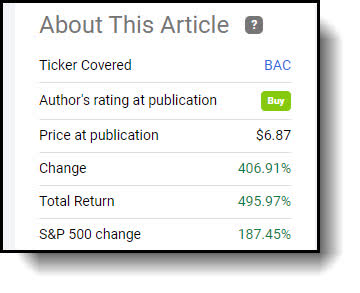

The primary thesis behind this pick is the dividend growth opportunity coupled with the potential for substantial capital gains. I have been pounding the table on the stock for the last decade. I wrote an article in January of 2012 titled, “The Time Is Now To Buy Bank Of America,” when the stock was trading for $6.84. I’m up 496% over the last 10 years, with 406% coming from capital appreciation and the balance from dividend payouts.

Finviz

So, I’m up substantially on this name in my dividend growth portfolio, but feel the stock has much more room to run. I see another great decade ahead for the stock. The primary catalyst for BAC stock over the next decade will be prospects for continued substantial dividend growth. Moreover, a major positive paradigm shift has occurred for the banking sector, or as Shakespeare would say, the worm has turned.

Federal Reserve Paradigm Shift

A massive paradigm shift has occurred. A fundamental change in approach to regulations by Washington coupled with the Fed’s newly minted hawkish stance has created the perfect environment for Bank of America to flourish. On top of this, legal woes for the bank are now clearly in the past. The market backdrop for banks has turned notably positive due to the following factors.

Major Catalysts

Rising interest rates

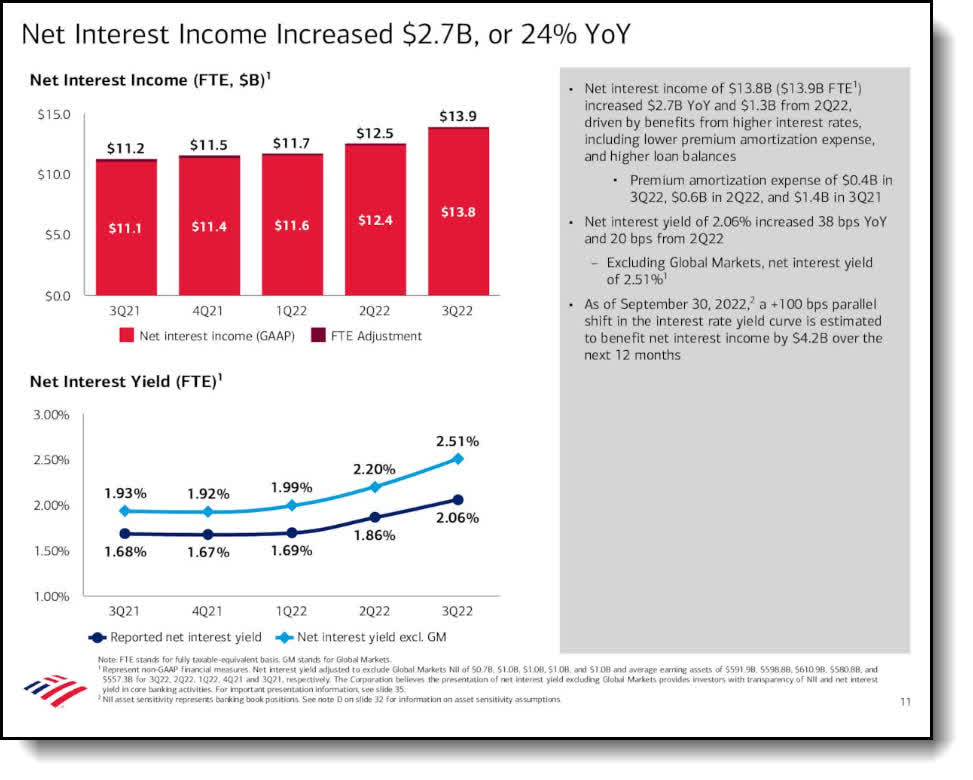

Banks make more money on loans in rising interest rate environments. The NII (Net Interest Income) should increase substantially as the rates rise. Bank of America Q3 earnings topped consensus estimates, as net interest income rose and loan and deposit growth continued.

Chief Financial Officer Alastair Borthwick stated during the call:

“Turning to Slide 11 and net interest income.

BAC.com

On a GAAP non-FTE basis, NII in Q3 was $13.8 billion, and the FTE NII number is $13.9 million. Focusing on FTE, net interest income increased $2.7 billion from Q3 ’21 or 24%, and that’s driven by benefits from higher interest rates, including lower premium amortization and from loan growth. Versus the second quarter, NII is up $1.3 billion, driven largely by the same factors, plus an additional day of interest in the quarter.

Year-over-year now, average short-term interest rates have increased 200-plus basis points, driving up the interest earned on our variable rate assets while we’ve maintained discipline on our deposit pricing, and that has driven nearly $1 billion of improvement. Long-term interest rates on mortgages have increased even more than short-term rates, and that’s improving fixed rate asset replacement and driving down refinancing of mortgage assets, therefore, slowing the recognition of premium amortization recognized in our securities portfolio. Year-over-year, that premium amortization has improved $1 billion. And additionally, lower securities balances over the past six months modestly offset the benefits of year-over-year loan growth.

The net interest yield was 2.06% and that improved 38 basis points from the third quarter of ’21. 20 basis points of that improvement occurred in the most recent quarter. And as you will note, excluding Global Markets activities, our net interest yield was 2.51% this quarter.

Looking forward, as it relates to NII guidance, I’d like to make a couple of comments. And first, I need to make a couple of caveats. Our guidance is going to assume interest rates in the most recent forward curve and that they materialize, that we see modest loan growth and modest deposit balance changes with market-based deposit pricing increasing baked in.

With that said, we expect NII in Q4 to be at least $1.25 billion higher than Q3. So last quarter when we were together, we told you we expected to see consecutive NII increases of about $1 billion in Q3 and another $1 billion in Q4. And that would make a total of $2 billion in Q3 and Q4, given we just put up $1.3 billion in Q3 and that outperformance, and refreshing our expectation for Q4 at $1.25 billion. We’re now saying that aggregate quarterly improvement won’t be the $2 billion we initially thought, it’s increased to around $2.6 billion or more.”

Furthermore, the bank expects NII to continue to grow as the Fed hikes rates even into 2023. The first question of the Q&A session was regarding the 2023 NII guidance. This is highly telling of the importance of this one area of income generation. Bank of America has one of the highest exposures to NII. When asked by Jim Mitchell with Seaport Global during the question and answer session about the NII expectations for 2023, CEO Brian Moynihan stated he expects the positive growth trajectory from the fourth quarter to continue throughout 2023. Below is an excerpt of the back and forth interaction:

“James Mitchell

Maybe just on NII. I think there’s a lot of uncertainty around deposit behavior, betas, what the catch-up rate could be with deposit pricing. But you guys indicated that you do — you’re still pretty asset sensitive. So how do you think about the trajectory of NII next year? Can it kind of keep growing from sort of the Q4 level through next year?

Brian Moynihan

Thanks…

James Mitchell

Assuming forward curve is realized? Sorry.

Brian Moynihan

Yes. Yes. So the short answer is yes, we believe so. And we believe that really for three reasons. The first one is, we still expect for future rate hikes and there’s going to be some lag to their impact. So you’ll start to feel some of that in Q1, for example, for the late hikes in this quarter. Second, we’re anticipating — loans growth is still pretty good at this stage. So we’re anticipating that we’ll keep growing on the loan side. And then third, we’ve got an opportunity to restrike our balance sheet at higher rates with every opportunity now as things come off of our existing securities portfolio.

So look, we’ve got our assumptions in there to be competitive on deposit pricing in each of the various segments. But yes, we believe we’ll grow NII next year.

James Mitchell

On 4Q run rates.

Brian Moynihan

Yes. Correct.”

Strong growth in banking business

The trading arms of banks tend to rely on market volatility for increased profits. The issue is volatility levels were somewhat subdued for the period. Even so, Bank of America’s Wealth & Investment Management division produced strong results due to a strong banking business bolstered by revenue growth from banking products.

“Wealth Management produced strong results, earning $1.2 billion, and that’s a particularly strong result given both equity and bond market levels. If they remain unchanged for the rest of the year, this would be only the first time since 1976 that both equity and bond markets were down for the year.

Now the volatility and generally lower market levels have put pressure on revenue in this business. And what’s helping to differentiate Merrill and Private Bank right now is a strong banking business; in this case, to the tune of $339 billion of deposits and $224 billion of loans. So while many of our brokerage peers faced declines in revenue and margin, we’ve seen year-over-year revenue growth of 2% and a margin of 29%, driving the sixth straight quarter of operating leverage. And we saw enough revenue growth from banking products in Q3 that more than offset declines in assets under management and brokerage fees.

Our talented group of financial advisors, coupled with our powerful digital capabilities, allowed modern Merrill to gain 5,200 net new households and the Private Bank gained 550 more in the quarter, both up nicely from net household generation in 2021.

We added $24 billion of loans since Q3 of ’21, growing 12% and this marked our 50th consecutive quarter of average loans growth in the business, consistent and sustained performance. Assets under management flows were $4 billion in the quarter and $42 billion since this time last year. Expenses increased 2%, driven by continued client facing hiring and higher other employee-related costs as our advisors are increasing their in-person engagement with clients, and that’s partially offset by lower revenue-related incentives.”

Regulatory reform

Banks are the most highly regulated of the sectors. The recent regulatory reforms should help the banks greatly in the coming years. I see this as the tip of the iceberg. Nevertheless, the primary catalyst for the stock is the dividend growth story. Let’s take a look.

Dividend growth analysis

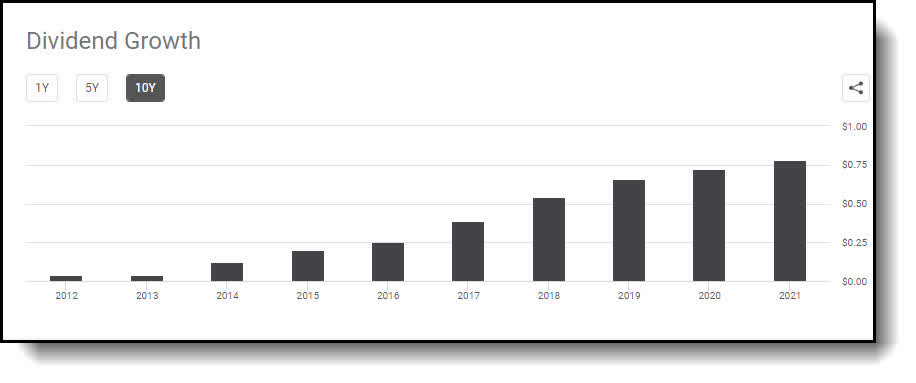

Bank of America has done an exceptional job growing the dividend over the past decade.

Seeking Alpha

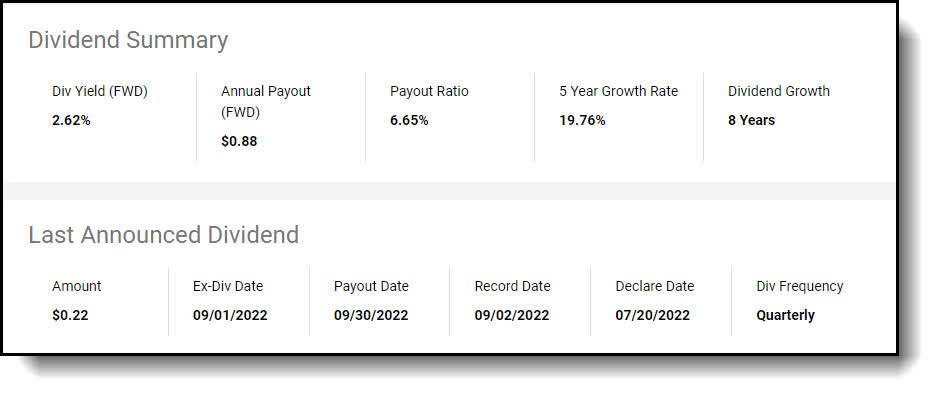

The dividend current stands at $0.84 annually and $0.21 per quarter, with a current yield of 2.32%.

Seeking Alpha

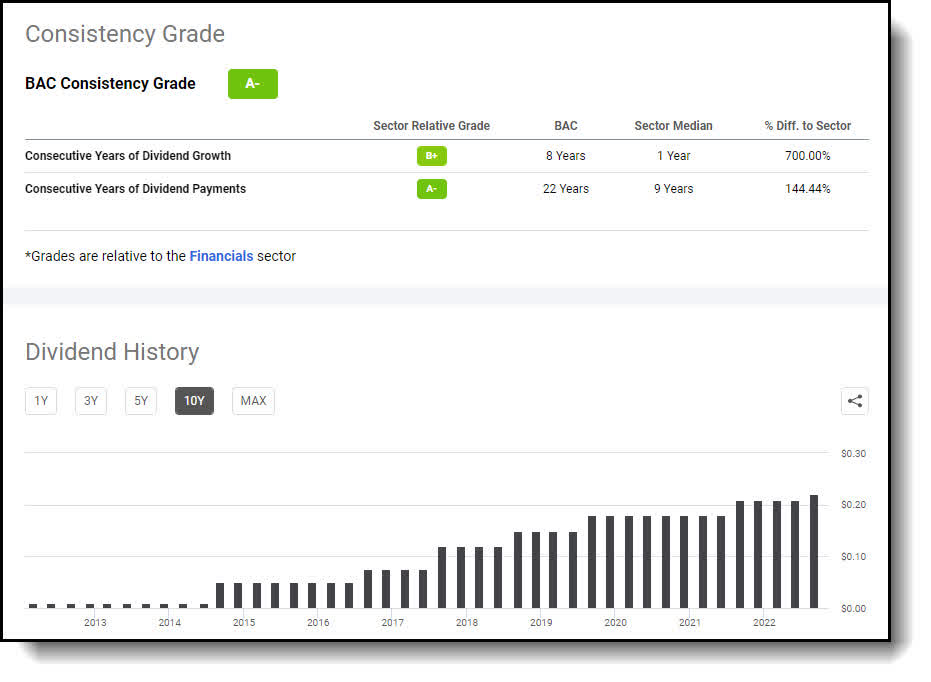

The dividend consistency grade is an A-, according to Seeking Alpha’s scorecard. 22 years of payments, 8 years of growth.

Seeking Alpha

I have no doubt Bank of America will continue the progress in this area. Furthermore, the bank is currently trading at a very attractive valuation. Let’s review.

Valuation Analysis

Bank of America is on sale. The bank is currently trading at forward P/E ratio of 9.14. What’s more, the bank is trading for 1.14 times book value, which is $29.55 per share.

Finviz

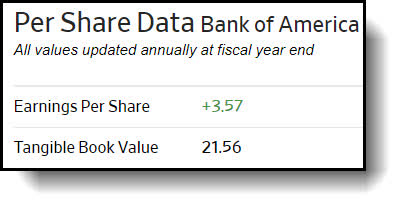

Furthermore, the stock is currently trading for 1.56 times tangible book value.

WSJ.com

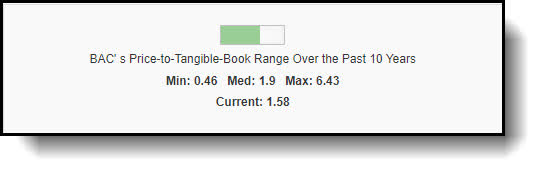

Comparing that to the 10-year historical median tangible book value of 1.9, this augurs well for an additional upside of 22%.

Guru Focus

So, the bank still has plenty of room to run before concerns regarding valuation will come into play. Now for the bottom line.

The Bottom Line

The banks have begun to break out on current earnings. I submit the Fed’s hawkish stance has marked the beginning of a rally for Bank of America. The combination of regulatory reform, a rising rate environment, accelerating loan growth, and the fintech revolution lowering costs should allow Bank of America to substantially increase the bottom line and therefore continue to raise the dividend substantially over the next decade. I posit this will, in turn, drive the stock higher creating an excellent total return opportunity.

Some of the “nattering nabobs of negativism” have reared their ugly heads and pointed to recessionary risks causing the bank’s stock price to plummet, yet, I beg to differ. The increased income from NII should more than offset any consumer banking hit the bank may take. What’s more, CEO Moynihan stated he wasn’t concerned about a huge decline, and I’ll take his word for it over the naysayers, as he has a rep of being a straight shooter. My 12-month price target is $43, implying a 24% capital gain coupled with continued dividend growth. Those are my thoughts on the matter. I look forward to reading yours.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment