Drew Angerer

Disclosure

I spent 31 years at Bank of America Corporation (NYSE:NYSE:BAC), retiring in 2011. I was a member of the Management Operating Committee.

Since retiring, I have made it a personal policy to not comment on or write about BAC. Initially my reluctance stemmed from insider status.

After more than a decade away from the bank, now is a good time to offer a few thoughts on BAC. For the record, I do not currently own shares in BAC but do have certain other financial interests in the bank.

Adding BAC To My Buy-and-Hold Long Term Bank Portfolio

This article is the second in a series about “Have” and “Have Not U.S. banks. The first article can be found here.

I plan to acquire BAC common and preferred shares over the next several months. BAC shares will be held in a Long-Term Bank Portfolio.

Banks in this investment portfolio are held long-term (5+ years in every case). The current portfolio consists of: JPMorgan Chase & Co. (JPM), Cullen/Frost Bankers Inc (CFR), SVB Financial Group (SIVB), First Republic Bank (FRC), First Interstate BancSystem Inc (FIBK), Stock Yards Bancorp Inc (SYBT), Commerce Bancshares Inc (CBSH), Bar Harbor Bancshares Inc (BHB), Farmers & Merchants Bancorp (OTCQX:FMCB).

The portfolio is diversified by size, geography, business model, customer segmentation. Banks in this portfolio have demonstrated over time:

- Strong risk-adjusted return on equity

- Superior credit/risk culture

- Shareholder savvy

- High quality, low risk

Here is my case for adding BAC to the long-term bank portfolio.

“New Bank of America”

I have respect for Moynihan’s leadership. He cast the course for the bank in 2010-2011 when he coined the term, “New Bank of America.” It is a testimony to his blocking-and-tackling in-the-trenches leadership that BAC has accomplished the goals he set more than a decade ago:

- Simplify the bank

- Strike balance between Consumer and Commercial/Corporate

- Expand Affluent/Mass Affluent segment

- Pursue Operational Excellence

- Commit to disciplined Expense Management

- Deliver “high quality, low-risk” growth, aka, “Responsible Growth“

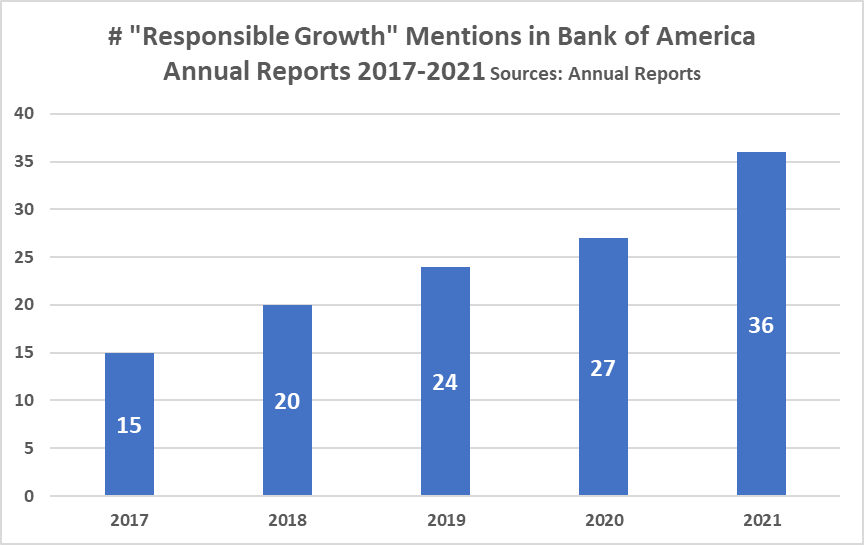

“Responsible Growth” Culture

BAC’s mantra under Moynihan’s leadership is “Responsible Growth.“

Moynihan took the helm of BAC in December 2009.

Right out of the gate he focused on “growing the right way,” a phrase he used in his first shareholder letter in the 2009 Annual Report.

Implied in this phrase was his accurate assessment that the prior CEO’s and Board’s risk appetite resulted in BAC growing the wrong way.

A review of the past five BAC annual reports reveals that Moynihan remains relentless in his promise to deliver “Responsible Growth.“

Responsible Growth (BAC Annual Reports)

The first line of Moynihan’s 2018 letter to shareholders noted, “I am pleased to report to you that by adhering to Responsible Growth…” in the 2018 Annual Report.

The headline of Moynihan’s 2019 letter to shareholders read: “Responsible Growth drove our results in 2019.” in the 2019 Annual Report.

The 2020 letter recognized Moynihan’s relentless commitment to responsible growth: “Our decade-long focus on Responsible Growth.” in the 2020 Annual Report.

And the cover of the bank’s most recent annual report stated: “Driving Responsible Growth — now and going forward.” in the 2021 Annual Report.

“High-Quality and Low-Risk Growth”

I will not own a bank in the Long-Term Portfolio that does not meet my personal risk profile: High-Quality, Low Risk.

Moynihan made this comment in the 2014 Annual Report: “The bank’s focus is high-quality and low-risk growth.”

The reality is that during the past decade BAC delivered high-quality and low risk but did not deliver growth.

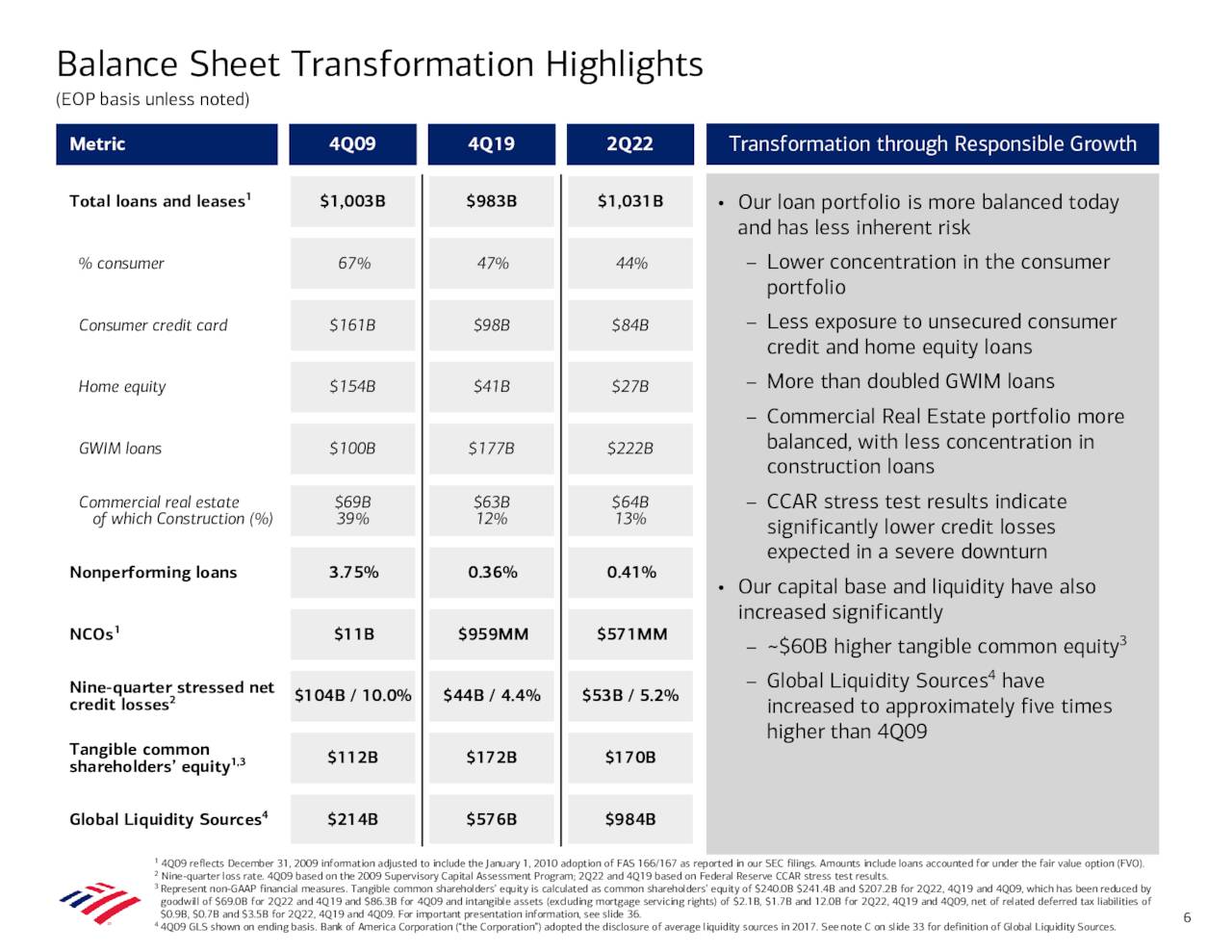

The two slides below are drawn from Bank of America’s 2Q 2022 earnings presentation deck. They starkly reflect the bank’s metamorphosis under Moynihan.

Slide 8 is an eye-opener. It is must-read for BAC shareholders.

Pay close attention to the line: “Total Loans and Leases.” Note 4Q 2009 end of period balance of $1.003 trillion and Q2 2022 end of period balance of $1.031 trillion. Loans are flat over the past twelve years.

BAC Balance Sheet Q2 2022 Presentation (BAC Press Release)

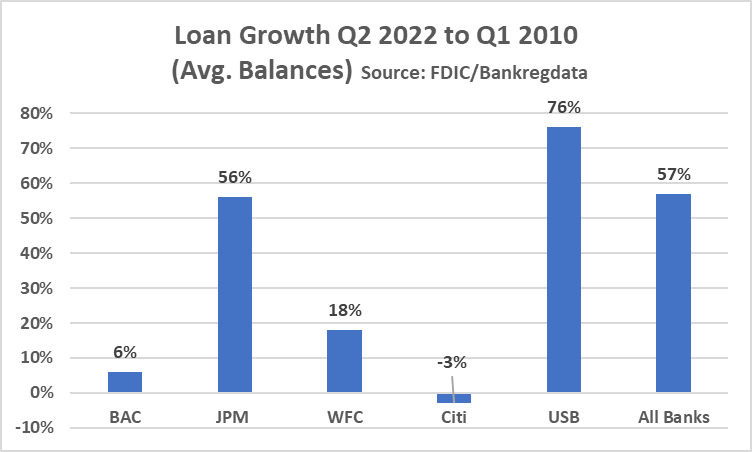

Flat Loan Growth: Key Observations

Let’s compare BAC loan growth to peers and the industry from Q1 2010 to Q2 2022. The slide below compares Q1 2010 average loans by bank to average loans in Q2 2022.

Note that industry-wide loans are up 57%. Among big banks, U.S. Bancorp (USB) leads the way at 76% (acquisitions not a factor during this time). Loan growth at JPMorgan Chase & Co. matches the industry.

Loans at Citigroup Inc. (C) have declined -3% during this time (Excluding the Costco (COST) credit card portfolio (acquired in 2016), Citi loans are actually down -5%.)

Loan Growth Big Banks (FDIC/BRD)

Reduced Risk Profile

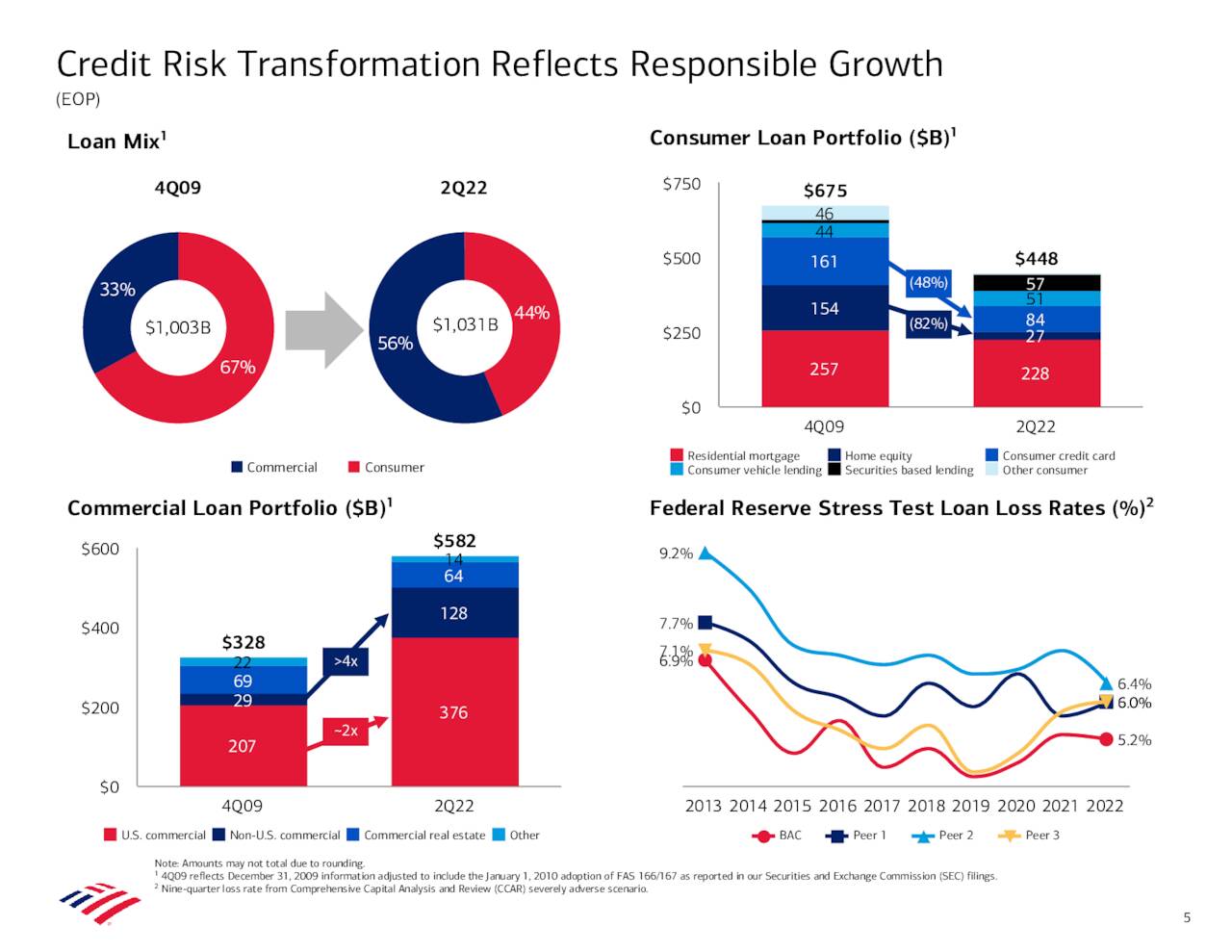

The second observation from the BAC Q2 presentation is that Moynihan has re-engineered the bank’s risk profile. How do we know?

Consumer loan exposure is now 44% of loans, down from 67% at year-end 2009.

Moynihan reduced the bank’s risk profile by dramatically driving down earning assets most vulnerable to downturns in the business cycle:

- Credit card down about 50%.

- Home equity down almost 80%.

- Construction and Development loans down 70%

In contrast, loans to Affluent/Mass Affluent borrowers (i.e. clients of the bank’s Global Wealth and Investment business) have more than doubled since year-end 2009.

Further evidence of the bank’s reduced risk profile is BAC’s growth in Commercial and Industrial loans (which excludes Construction and Development): +113% per FDIC data. A key message to be drawn from my 2016 book about bank investing is that C&I loans deliver the best risk-adjusted returns through business cycles.

Finally, check out the bank’s tangible common shareholder’s equity: +51% while risk assets are essentially flat. Moynihan has indeed built a “fortress balance sheet” that he promised to do more than a decade ago.

The fifth slide in BAC’s Q2 earnings presentation provides additional insight into the bank’s growth in commercial lending and decline in consumer loans. My research shows that commercial & industrial loans have historically generated the best risk-adjusted returns through-the-cycle of all loan categories.

BAC Risk Profile 2Q 2022 Presentation (BAC Press Release)

Bank of America Shareholder Returns

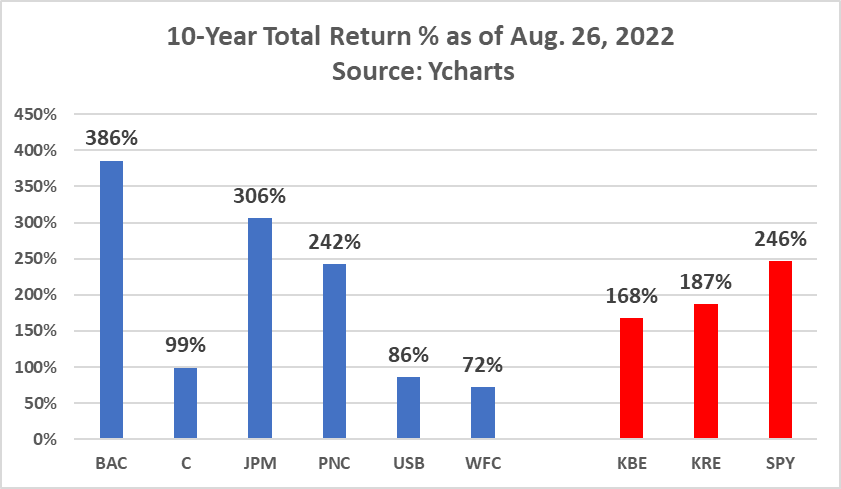

BAC’s improved risk-return profile has not been lost on investors. The bank’s 10-year total returns are among the best in the industry.

Shareholder Returns (Ycharts)

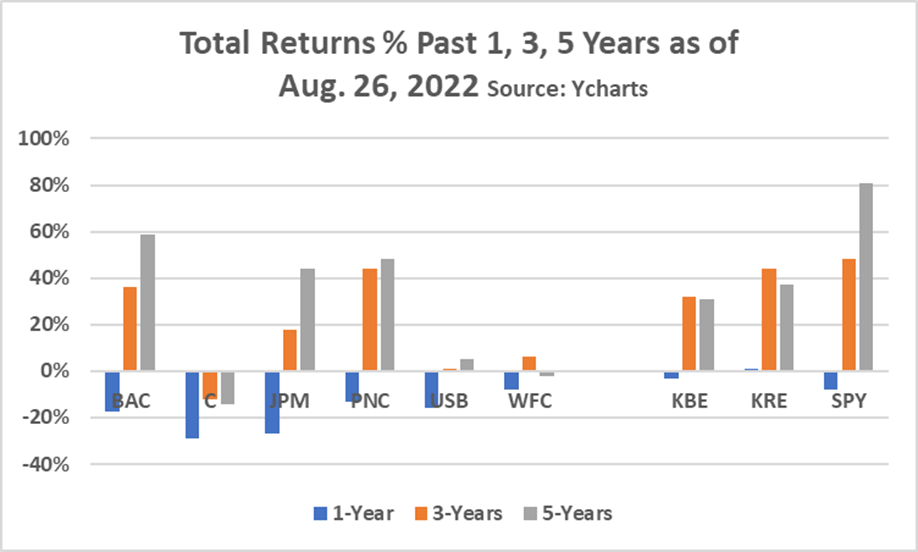

BAC’s outperformance relative to industry peers has slowed over the past five years as evidenced by the bar chart below.

Shareholder Returns (Ycharts)

Moynihan Comments Q2 2022

My sense is that Moynihan went into the Q2 earnings call with three big goals:

- Highlight the big loan growth in Q2.

- Articulate why BAC’s “Responsible Growth” strategy is worthy of more shareholder respect which should translate into higher returns and lower price volatility over time.

- Address head-on apparent investor worries that BAC is not prepared for a recession.

During the call Moynihan and the bank’s CFO evoked the term, “Responsible Growth,” six times which was unusually high number compared to prior earnings calls. Here are those references:

- “… given the debate about a future recession… we just continue to drive responsible growth at our company, and so we’re prepared.”

- “… you can see how much the loan book has changed under more than a decade of responsible growth… our loan book is quite well balanced now between consumer and commercial loans… the consumer portfolio is even more collateralized with a greater mix of mortgage and less card. In addition, much less second mortgage… all consumer portfolios have much higher FICOs.”

- “… decade-plus of responsible growth. Given all these changes, 92% of our commercial loan book today is either investment-grade or secured.”

- ” As you review the average loan data, we just want to remind you that our discipline around responsible growth has remained tight. Average loans have climbed back over $1 trillion. They’re up 12% compared to Q2 ’21, led by commercial growth of 15% and complemented by consumer growth of 8%.”

- In response to analyst question whether the bank’s Loan Loss Reserve is adequate given recession risk, Moynihan responded: “… you can see us lower than everybody else’s, that’s because many, many years of responsible growth.”

- Moynihan in closing: “As you think about Bank of America… the pre-pandemic growth engine has kicked back in. We’re mindful of the debate about a future recession, and we have prepared the company across the last decade-plus through responsible growth to be prepared for that.

Key Takeaways from 2Q Earnings Call

- Loan balances are growing: Up 12% Y/Y. This is a big deal and a dramatic turnaround from loan trends over the tenure of Moynihan’s leadership.

- The loan growth is fueled by commercial growth, up 15%, which Moynihan (and my data) believe delivers superior long-term risk-adjusted shareholder returns. As evidence of that fact, Moynihan noted that 92% of BAC’s commercial loans are investment grade or secured with collateral.

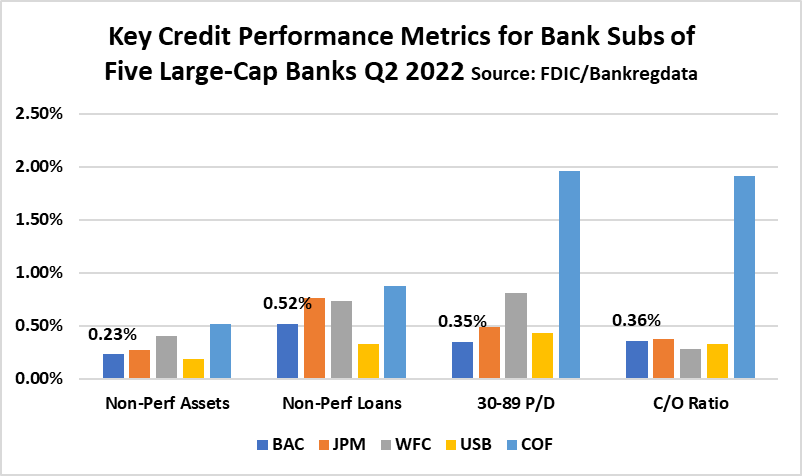

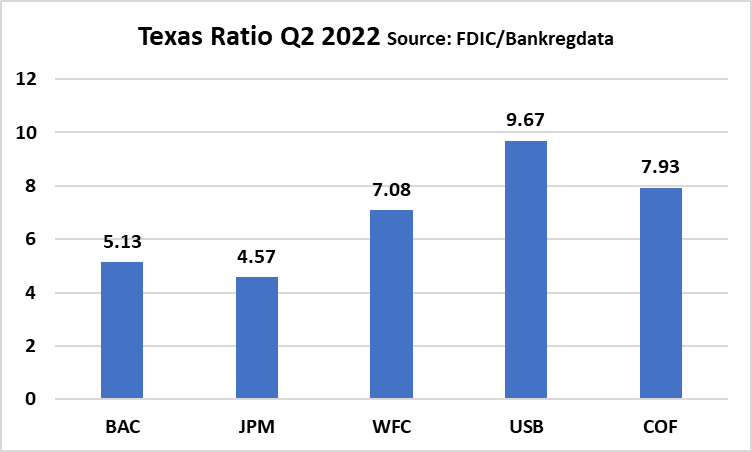

Credit Performance

The biggest risk facing bank investors over time is credit quality. For that reason, my Long-Term Portfolio only includes banks that have superior credit/risk cultures.

The next two charts address credit numbers for five big banks as of 2Q.

The first chart shows current credit metrics for BAC’s bank sub compared to the bank subsidiaries of JPM, Wells Fargo & Co (WFC), USB, and Capital One Financial Corp (COF). The second chart reflects another common credit quality metric, the Texas Ratio.

BAC’s credit looks strong, but current numbers must be taken with a grain of salt given the benign economy that has enabled all banks to show strong credit performance. The real question is how will BAC do through a down-cycle?

Credit Metrics (FDIC/BRD) Texas Ratio Big Banks 2Q 2022 (FDIC/BRD)

Fed Stress Test

I am a huge fan of the Fed Stress Tests which Dodd-Frank introduced in 2010-2011. While virtually everything about Dodd-Frank has proven either redundant or unnecessarily burdensome to U.S. banks, the Stress Test is a clear win for bank investors.

Here is a link to the most recent Federal Reserve Stress Test results. Page 17 is the money chart showing the impact of the “severely adverse scenario” on the capital structures of 33 large banks.

Note that all banks passed the 2022 test. However, despite the passing grade, the Fed did not communicate to the public that it demanded that some big banks cease buybacks until certain risk-weighted capital ratios improve.

We know this because of not-so-happy comments made by Jamie Dimon during JPM’s 2Q earnings call in July.

On September 12 during the Barclays Financial Services Conference, Brian Moynihan revealed that BAC also stopped buybacks pending a quarter or two of retained earnings that will boost tangible capital.

(As an aside, I cannot help but wonder if the regulatory push was less about true capital concerns but more about politics. My 12/30/21 “Citi Bear” article noted that the Biden (aka, Elizabeth Warren) administration planned to replace Randal Quarles (Trump appointee) as head of the Fed Stress Tests with Sarah Bloom Raskin who was on record favoring higher capital ratios for big banks. While Raskin failed to garner sufficient Senate support for her nomination, it appears that Warren succeeded nonetheless to get her “more capital” mandate into the 2022 Stress Test.)

BAC & Industry Share Repurchases

Despite the temporary pause in buybacks, Moynihan also revealed on September 12 that the bank intends to return more capital to shareholders once the targeted risk-based capital ratio (10.4%) is met.

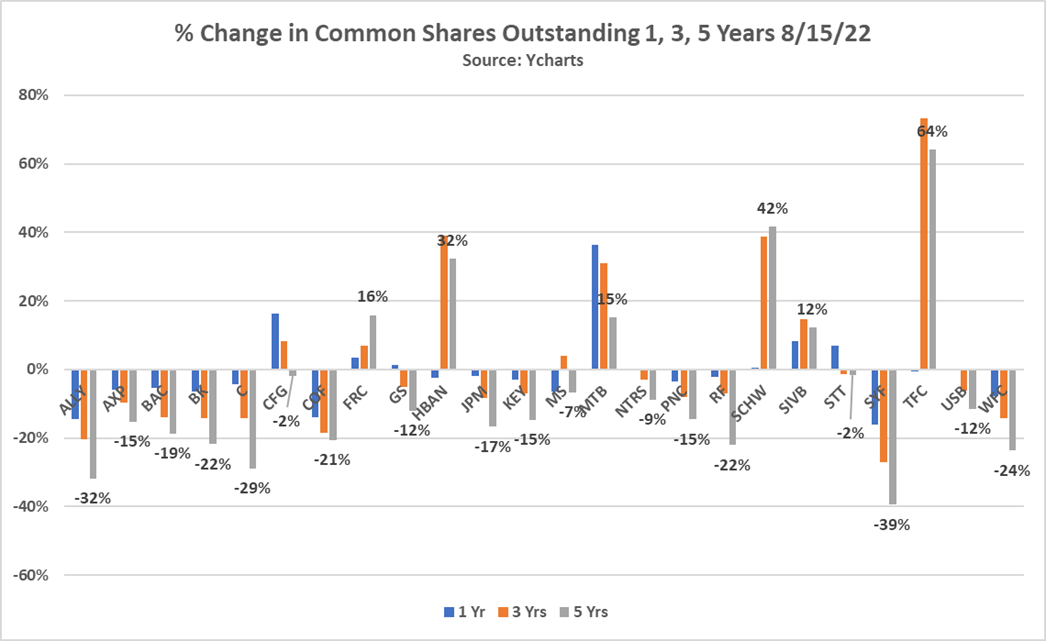

This next chart shows the change in shares outstanding over the past 1, 3, 5 years for the nation’s biggest banks. I find it difficult to overstate the significance of such massive share buybacks across the industry over the past five years.

Note BAC’s share count is down 19%, 14%, 5% respectively since 2017, 2019, 2021. The bank’s most recent 10Q (7/29/22), however, shows no reduction in shares from June 30.

Shares Outstanding (Ycharts)

BAC & Industry: Deposit Rich

My September 13 article about “Have” and “Have Not” banks framed the biggest issue facing bankers, directors, and investors today: rising interest rates will prove a boon to some banks and trouble for others.

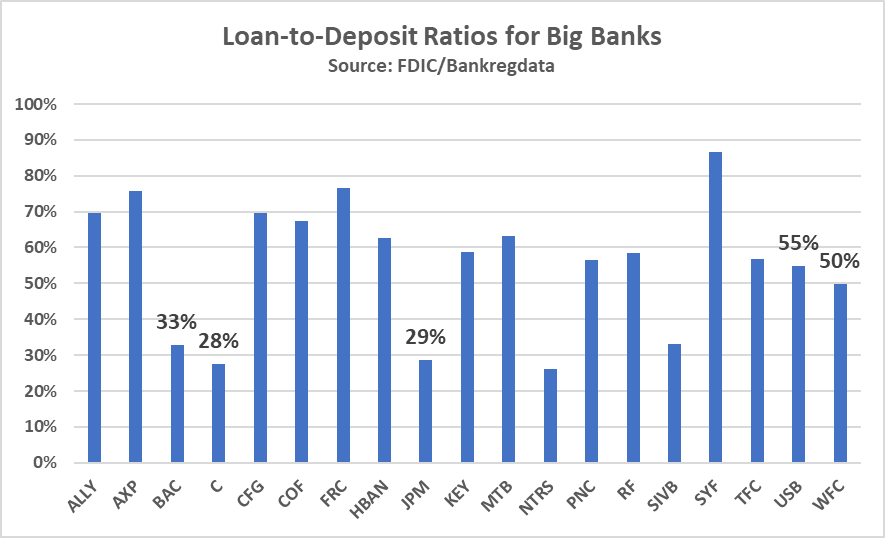

This next slide shows bank loan-to-deposit ratios for the big banks as of June 30, 2022. Implications:

- Banks across-the-board are deposit rich.

- Low loan-to-deposit ratios mean most banks will be slow to raise rates even as short-term U.S. Treasury rates increase.

- Net interest margin should improve modestly as floating rate loans re-price.

- However, intense competition for the best loans will keep a lid on loan yields.

Loan/Dep Ratio 2Q 2022 (FDIC/BRD)

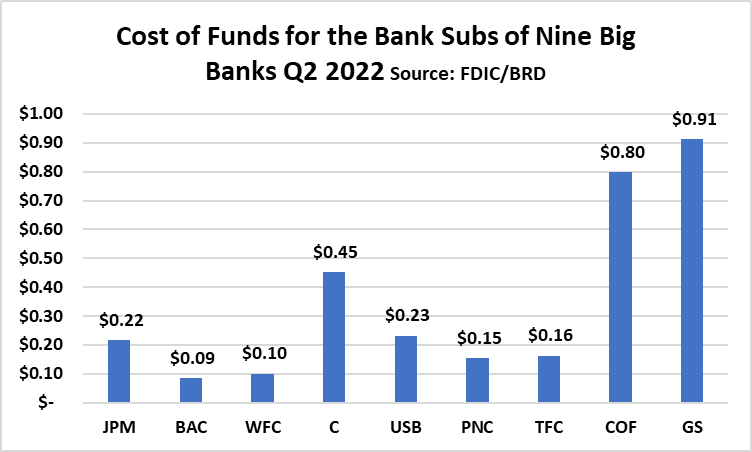

Not only does BAC have a low loan/deposit ratio, but as the next chart shows, BAC also has the lowest cost of funds among peers (Out of 758 publicly traded banks, BAC had the 95th lowest cost of funds; this fact indicates that BAC is far from alone among “Have” banks ready to benefit as rates rise).

Cost of Funds 2Q 2022 (FDIC/BRD)

Higher Volatility

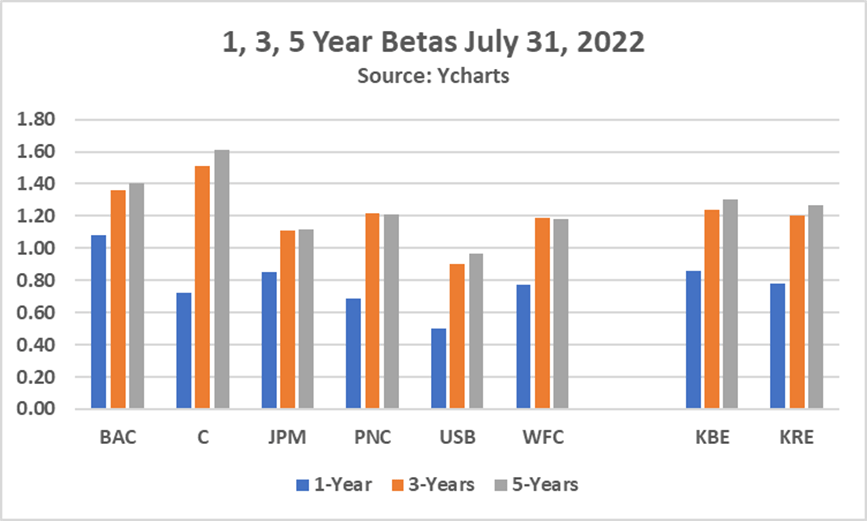

The next chart highlights something I don’t understand: BAC’s 1, 3, 5-year Betas are higher than peers despite what appears to be a continued de-risking. Citi’s high Beta is understandable, but not so with BAC.

The high Betas for BAC are perplexing and may suggest that not all investors/traders/speculators believe BAC’s board and management have a culture and strategy capable of delivering superior risk-adjusted returns over time.

BAC’s Beta will likely decline markedly compared to peers over the next five years if BAC delivers the superior risk-adjusted returns on equity that I anticipate.

Betas Big Banks (Ycharts)

Back to Loan Growth

The key to BAC’s share price appreciation is not buybacks but growth in earning assets.

The most attractive earning assets are loans. Not only did BAC see real loan growth in Q2 as noted above, Brian Moynihan indicated during the September 12 Barclays Conference that the bank is poised to grow loans in the quarters ahead. Here is what he said:

“If you look at loans, overall, we are growing through the first two quarters…we are judicious. But when you look at it, you got to tear it apart. And the loan growth rate will slow down… Some of the mortgage lending stuff slowed down just because of the dynamics of the market. But once we get through this transition period you expect us to grow loans at faster than the growth rate in the economy…. So, this quarter, I’d expect, you’ll see us look like the market for the first time. We’ve actually outgrown the market in other cohorts. So, we’ll kind of look like the market.”

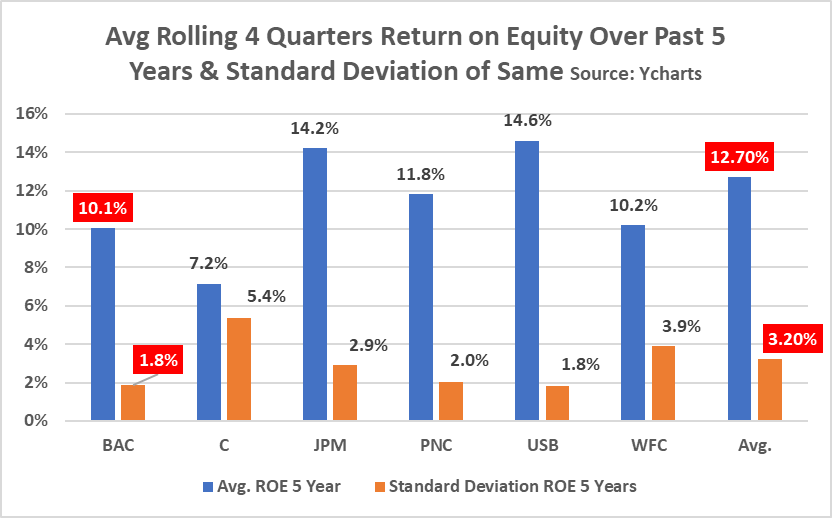

Profitability/Return on Equity

This next chart is a money chart. Bank CEOs cannot control the price of their stock, but they directly control the return on equity over time.

This is a telling chart as it shows that BAC’s average Return on Equity during the past five years trails all peers but Citi. It also shows the steadiness of the bank’s profitability as reflected by the lowest volatility of ROE during the five years (tied with USB).

My sense is that Moynihan’s emphasis for the past decade has been more on “responsible” than “growth,” thus the lower ROE. The fact that he is emphasizing “growth” in 2022 is important.

For BAC to earn a higher valuation (Price to Earnings and Price to Tangible Book), I believe the bank must push its average ROE to 12% over the next five years. If the bank can do so without increased volatility, valuation expansion combined with share repurchases and real earnings growth should fuel 10%+ annual growth in share price between now and 2027.

ROE Big Banks 5 Years (Ycharts)

Closing Thoughts

The case for BAC as a long-term hold boils down to the following:

- Low risk profile relative to valuation (i.e. low earnings volatility, fortress balance sheet, shifting loan exposure from mass market to affluent/mass affluent and investment grade corporates).

- Superior cost of funds which create competitive advantage and will result in net interest margin growth as rates rise.

- Superior deposit gathering capabilities through branch system, Merrill, and corporate banking footprint.

- Massive share buybacks and capacity to do more once Fed-imposed risk-weighted capital ratio target is exceeded, which I anticipate for 4Q.

- Highly diversified financial institution with affluent/mass affluent consumer tilt.

- Poised to realize real loan growth for first time in a decade.

- Excellent growth record in mass affluent client numbers in recent years.

- Continued investment in technology that has positioned BAC together with JPM as the leading digital banks in the country.

- Excellent CEO who has been in place since late 2009, and according to my sources, is likely to remain in the role for another five years.

What can go wrong?

- The economy falls into deep and long recession; BAC should see better credit performance than mass market lenders like COF, but it will not avoid credit losses and an interruption in earnings momentum.

- BAC incurs an extraordinarily damaging operational event which jolts investor confidence (e.g., JPM and the London Whale in 2013 or Citi and the Revlon Wire in 2020.); cyber risk is also a chief concern.

- Intensified political scrutiny that requires banks to cease share buybacks until material improvement (i.e., order of magnitude seen from 2009-2012) in risk-weighted capital ratios is achieved.

Disclosure

I am a buyer of BAC shares after this article posts. I will acquire BAC common shares and preferred on price weakness over time.

CAVEAT

I share my thoughts and investment intentions for BAC for the purpose of getting feedback that challenges my premises.

Every investor needs to understand their goals and appetite for risk before investing.

Investors considering an investment in BAC should do their due diligence which is made possible by going to Seeking Alpha and reading articles like this one as well as earnings transcripts and executive presentations like the one BAC did recently with Barclays.

Be the first to comment